Summer Crash of 2016?

Amazing what a difference a day makes. On Tuesday of last week, I wrote the below article which was set to be published on Marketwatch.com for the following day. Unfortunately, there were some technical issues during the submission process, and I got too busy to try to re-submit the writing Thursday. It turns out with hindsight that was perhaps my last chance to do so, as a Summer Crash (primarily in Europe) began to take place.So, is Michael right? Is the Great Crash of 2016 that we escaped at the beginning of the year still in play? Will Soros and Druckenmiller turn out to be right warning of a big market disruption?

Since it never got published prior to Friday, I’ve put the writing below. A couple of quick points before reading it though. First of all, the “Brexit” news should never have been a surprise. All polls have a margin of error which can be quite large. The market seemed to be convinced that Brexit would not happen, when factually it was always a toss-up. When real uncertainty is ignored and markets act with bravado, the result tends to be a surprise sell-off and panic. I did not speculate in the Tuesday Summer Crash writing that “Brexit” was the reason for a major sell-off to come.

Second, and perhaps more importantly, I don’t think this is over yet. Intermarket trends suggest broad defensiveness prior to Brexit becoming the focal point. We will only know with hindsight why, but I suspect another drop may be coming which is US-led given the duration of defensive posturing in the last few months, similar to behavior last seen in the lead-up to the Summer Crash of 2011.

All of our strategies are predicated on the anomaly we show in each of our 4 award winning papers that volatility is predictable and can be positioned for in advance. If the cycle for more frequent volatility has finally begun, those who have been contemplating when to pull the trigger on using our mutual funds and separate accounts may want to finally do so. Strategies which thrive on alpha generation through down-capture need to be operating in a cycle where there is downside to capture. The last few years have been all up, no down. What is missed by many who live in the small sample is that the outperformance that comes from taking less risk at the right time is far greater and far faster than trying to take more risk on the upside.

Schopenhauer’s timeless quote I believe will be quite appropriate as we enter the third stage of truth.

——————-

Summer Crash of 2016?

“All truth passes through three stages. First, it is ridiculed. Second, it is violently opposed. Third, it is accepted as being self-evident.” – Arthur Schopenhauer

Something doesn’t add up.

I’ve done my best to “evolve” over the last few years. Five years ago, when I began actively writing for websites like Marketwatch reviewing intermarket trends, I took the approach more of making a “call” on the direction of stocks and bonds (risk appetite vs defensive stance). The call that got me most attention (and got me in the media) was the “Summer Crash of 2011,” whereby 2 months before I argued defensive sector strength, Treasury behavior, and intermarket analysis all pointed to a “Great Re-Adjustment” likely in the summer (http://www.marketwatch.com/story/money-managers-called-the-summer-market-plunge-2011-08-10). August happened, and stocks went through one of their most volatile periods in history.

Lucky or smart? The reality is I have no idea. But when defensiveness rules market behavior in a big way, something is likely wrong with the overall trend and the conditions that favor volatility. Since those days of making calls, I’ve co-authored four award winning academic papers (https://pensionpartners.com/research/white-papers/) which quantitatively prove that 1) volatility is predictable, 2) anomalies and strategies have cycles, and that 3) being down less over long cycles matters more than being up more. As a matter of fact, we’ve shown that wealth comes not from taking more risk to get more return, but rather less risk at the right time.

I believe there is a growing possibility that a nasty decline is to come in the near-term not based on opinions, but based on sector and asset class behavior. This is by no means meant to be alarmist, nor is it meant to pound the table that we are going to collapse here. Just because you slow down entering a storm and a crash never happens does not mean it was wrong to take caution. And this, I believe, is a time to be cautious.

So what are the warning signs? As we showed in the 2014 Dow Award winning paper “An Intermarket Approach to Beta Rotation” when Utilities outperform the broad market on a short term basis, volatility and drawdown risk tends to rise afterwards. Utilities (XLU) relative to the S&P 500 (SPY) have remained stubbornly high, and may be on the verge of a breakout (click on image).

As shown in the 2015 NAAIM Wagner Award winning paper “Lumber: Worth Its Weight in Gold” we showed that when Lumber (cyclical) outperforms Gold (GLD), volatility (VXX) tends to rise afterwards as well, and that signal has preceded major downturns in stocks. Lumber has now recently begun to underperform the yellow metal (click on image).

Stocks remain above their moving average, so this signal has not yet flipped. Moving averages, similar to Utilities and Gold, tend to anticipate higher or lower volatility regimes. So for those more on the bullish side, this is your main argument in the here and now.

Bottom line? There is enough defensive behavior here to stand up and take notice. And given just how “resilient” stocks have been, this seems like the kind of environment whereby the stock market’s muscle just gives out. Now keep in mind that every signal has false positives, meaning there are times when Utilities outperform and Gold outperforms, but stocks don’t go down.

Will this be a false positive or not? I’ll let you know in a few months. But this is a time where complacency, combined with defensiveness on the fringe, might result in a coming storm.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Pension Partners, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Pension Partners, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

It's too early to tell but both Soros and Druckenmiller have already made great returns on their gold holdings. Just look at the explosive moves in the SPDR Gold Shares (GLD) and the VanEck Vectors Junior Gold Miners ETF (GDXJ) below (click on images):

Any trader will tell you to "buy the breakout in gold shares" as it's signalling more gains ahead but I wouldn't touch gold right now, especially after a huge run-up.

Why? Well, as Alex Rosenberg of CNBC reports, VIX, the market's fear gauge, plunges in historic one-week move, signalling investors were caught flat-footed post Brexit and when they saw the world wasn't ending, they rushed to sell implied volatility.

But that doesn't mean much as we can argue that the panic buying of last week was way overdone and there is too much complacency right now. In fact, Bank of America-Merrill Lynch is warning investors who have sighed in relief following the UK's surprising vote to leave the European Union that it's just a matter of time until companies start to reveal just how hard Brexit is hitting them—and it could soon get quite ugly for stocks.

My own reading is that the Brexit vote was Europe's Minsky moment and if central banks didn't calm markets, it would have been much uglier last week. Still, no matter what central banks do, George Soros is absolutely right, Brexit will reinforce deflationary trends that were already prevalent.

And this is the key you all need to understand, deflation isn't dead, central banks can pump massive liquidity into the system but they can't resurrect global inflation. In fact, bond guru Jeffrey Gundlach thinks that central banks are causing more deflation by introducing negative rates. He says there is a bear market in confidence in policymakers and he's been long gold and gold miners in his macro fund all year.

He might be right, there may indeed be a bear market in confidence in policymakers which is why silver just vaulted above $21 for the first time in two years and gold advanced for a fourth day on speculation of more central bank stimulus in the wake of the UK’s vote to leave the European Union. Mining shares also surged.

But if you ask me, the rally in gold (GLD), silver (SLV), oil (USO), metal and mining (XME), energy (XLE) and emerging markets (EEM) shares which registered 8.6% gain in the first-half this year, outperforming developed markets by 5.5%, the best first-half performance since 2009, is nothing more than a function of the weak US dollar (DXY). And because I see the US dollar gaining strength in the second half of the year, I would steer clear of all these sectors including gold and silver.

Instead, I continue to recommend good old US bonds (TLT) as the ultimate diversifier in case something goes awfully wrong. It's worth noting that even though global bonds are in the Twilight Zone, the yield on the 30-year US Treasury bond hit a record low on Friday amid global bond rally.

What is the bond market worried about? It's looking beyond Brexit, worried of the deflation tsunami I warned of at the beginning of the year and increasingly worried about another Asian financial crisis which will really reinforce deflation for another decade or decades to come (keep your eye on the surging yen, it could trigger another crisis).

In fact, bond markets have a message on the economy that stock investors might not want to hear. In this deflationary environment, it's very difficult to envision stocks melting up even if central banks are lining up to do the wave following Brexit.

All this to say investors everywhere are basically screwed at this point. Taking more risk might pan out but it exposes them to bigger downside risk if something goes wrong.

This is why hedge funds have no idea how to trade this market. Many are reeling after Brexit but even before that event, their day of reckoning was on the horizon.

Most pensions are also struggling in this environment. Bloomberg reports that Japan's GPIF, the world’s biggest pension fund, posted its worst quarterly loss since at least 2008 after a global stock rout in August and September wiped $64 billion off its investments. This represents a 5.6% quarterly loss for the $1.1 trillion pension fund, which isn't the end of the world but it's still a staggering sum for this mega pension fund which plowed into equities at the worst possible time, suffering its first annual loss since the financial crisis.

Given the low prospective returns in stocks and bonds, there is a growing appetite for infrastructure assets at Canadian and US pensions. In the long run, infrastructure makes sense, but even here, there are no guarantees and as more and more funds compete for fewer and fewer assets, valuations will be bid up, impacting future returns.

Back to stocks and the summer Crash of 2016. A lot of nervous investors out there worried about the post Brexit fallout. I say forget about Brexit, keep your eye on Asia and emerging markets, that is where the source of deflationary tension will be in the second half of the year. All we need is one more Big Bang out of China and this market is toast.

Still, I'm not worried of a summer or fall crash and quite frankly, I've been loading up on small biotech shares I like going forward. Again, biotech isn't for the faint of heart and best played via ETFs (XBI and IBB) and while some skeptics think the "biotech bubble" is about to burst, I say bullocks, the secular uptrend in biotech is still intact except the swings will be much more pronounced in a record low rate environment.

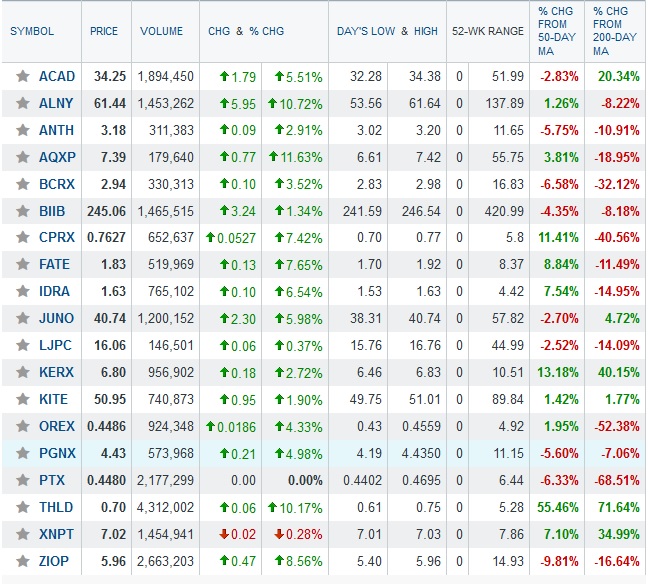

Big swings however mean big opportunities, especially if you track top funds' activity closely and pick your shares very selectively. Below, a small sample of biotech shares for traders with big risk tolerance (click on image):

Of course, opportunities aren't just in biotech. I track thousands of stocks across many industries but I always begin with my macro outlook because that dictates my personal risk tolerance and tells me which sectors to steer clear from even if they are bouncing hard after being way oversold.

Right now, the big macro theme going into the second half of the year is more global deflation and while the world economy is slowing, the US will lead the way which is why I'm long the US dollar going into the second half of the year.

More deflation is bullish for bonds (TLT) and interest sensitive sectors like utilities (XLU) and REITs (IYR) but I would steer clear of the latter sectors as valuations are stretched and momentum is slowing. Also, in a deflationary environment, real estate makes me very nervous (what happened at Standard Life's property fund can easily happen elsewhere).

More deflation means ultra low or negative rates are here to stay which is not good for big banks and big insurance companies. This is why financials (XLF) are struggling in this environment and will continue to struggle as deflation takes hold (click on image):

I am going to stop here and allow you to digest all this but my message is simple, while I don't see a summer Crash, it will be a long, hot and extremely volatile summer and I would be very selective in the sectors, countries and currencies I trade in the second half of the year.

Below, I embedded a few bearish and bullish clips for your viewing. I am taking a week off to relax and recharge. Please remember to kindly donate and/ or subscribe to this blog via PayPal on the right-hand side to show your appreciation for the work that goes into these comments.

I will be back late next week to resume my blog. Have a great week!

Comments

Post a Comment