Quant Style Crash Finally Arrives?

If you’ve been cursing at technology stocks for the past two days, there’s another corner of the market that’s perhaps just as deserving of your anger.It's the final day of trading for the week, month and quarter. Everybody is on edge after a very volatile week where we saw FANG stocks like Facebook (FB) and Amazon (AMZN) sell off hard and a particularly violent sell-off in Tesla (TSLA), down 18% this week (as of Wednesday's close).

It’s called momentum -- quant jargon for stocks that have performed the best over the past year or so -- and it’s gone through a rare bout of pain this week.

The lagging performance didn’t come out of thin air. Strategists from Morgan Stanley to Lazard Asset Management Ltd. have recently stoked worries about the popular quantitative strategy. Their primary concern? That investors piling into the same winners, including lofty technology stocks, had heightened the risk of a rush to the exits.

Those warnings, it seems, were scarily prescient. A long-short momentum portfolio, which hedges out greater market movements, had logged its biggest two-day plunge since November 2016 at yesterday’s close, according to data compiled by Bloomberg (see chart above).

And the concerns have yet to abate.

“If we have momentum selling off further, if we have cyclicals selling off further, then also tech will suffer further,” Max Kettner, a Commerzbank AG cross-asset strategist, said during an interview with Bloomberg TV. “I’m getting slightly scared with regards to tech right now.”

Though company-specific news from Twitter Inc. to Nvidia Corp. may have been the catalyst for the sell-off, a plunge in the quant trade highlights the tremors being sent through all of the market leaders. In the momentum portfolio, it’s not just technology companies that contributed to the Tuesday losses. The biggest drag after Twitter was drugmaker AbbVie Inc.

Momentum had been seemingly impervious to equity weakness. Even with the two days of selling, the factor is in the green so far this year. However, that strong performance set up momentum stocks to be among the biggest losers as soon as things turned sour, according to Steven DeSanctis, an equity strategist at Jefferies LLC.

“The momentum trade performed well even in the recent downturn, and thus it was destined to get hit,” DeSanctis said. “Style performance and tech ETF flows were all at extremes.”

Still, much like in prior pullbacks, DeSanctis added, the stocks are likely to rebound before long.

Even Twitter (TWTR) sold off hard earlier this week following a spectacular start to the year, crimping my Long Twitter / Short Facebook pairs trade. I still prefer the former over latter but regulatory risk has arrived and threatens all big tech companies, including the Goliath:

I have stated my concerns with Amazon long before the Election. Unlike others, they pay little or no taxes to state & local governments, use our Postal System as their Delivery Boy (causing tremendous loss to the U.S.), and are putting many thousands of retailers out of business!— Donald J. Trump (@realDonaldTrump) March 29, 2018

A tweet from President Trump is all it took this morning to validate people's nervousness (you have to wonder if he gave his hedge fund buddies an advanced warning so they can short Amazon last week).

So, is this it? Is this the big tech sell-off so many bears have been warning of? Are hedge fund quants taking over the world about to lose their reign as momentum strategies blow up?

I don't know, I'm still defensive but some of these moves are so violent that I wouldn’t be surprised if top hedge funds pounced and bought big tech stocks this week.

Unfortunately, we won't know what top funds bought and sold in Q1 until mid-May, but by that time the data will be mostly irrelevant because the way stocks move, they can significantly rise or decline over the next six weeks.

One person who isn't buying the quant style "crash" theory is AQR's Clifford Asness:

This is ridiculous. “Worst since November” is a ridiculous thing to write. How about “worst since last Thursday”?— Clifford Asness (@CliffordAsness) March 28, 2018

“Crash”? Really? We will see a crash one day, maybe soon, maybe not, this ain’t it.

Momentum still up on the year. Innumerate silliness. https://t.co/5FjUA12FDj

I agree with Cliff, he's a smart man, really knows his stuff which is why I read his Perspectives regularly, even though I don't always understand what he's writing about.

I keep my momentum trading simple, use daily and weekly charts with simple moving averages and use other data to make decisions, often spur of the moment decisions.

For example, check out the one-year daily charts of Amazon (AMZN), Facebook (FB), Twitter (TWTR) and Tesla (TSLA) using very simple 50, 100 and 200-day moving averages (click on each image to enlarge):

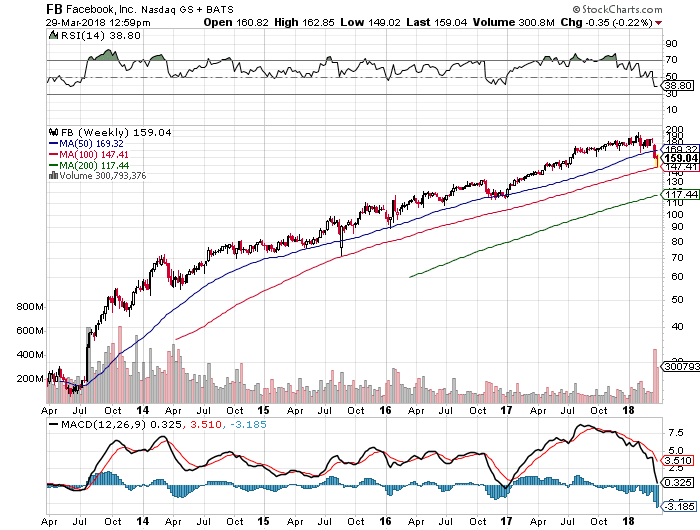

Now, let's step back and check out the five-year weekly charts of Amazon (AMZN), Facebook (FB), Twitter (TWTR) and Tesla (TSLA) using the same 50, 100 and 200-week moving averages (click on each image to enlarge):

The five-year weekly charts give me a better long-term perspective. Just by looking at these charts, it confirms that Amazon is still in beast mode but rolling over, Facebook has important support at $147 (it hit a low of $149 earlier this week), Twitter has nice support at $27 and Tesla has nice support at $253 (hit a low of $248 on Wednesday).

From looking at the weekly charts, Amazon might make you most nervous but short-sellers have piled into Tesla (20% of the float is being shorted) because that's the one they think will fall furthest from these levels. And if it declines and keeps going below its 200-week moving average, it's in big trouble.

Now, there is nothing scientific about the charts and moving averages I used above. Sometimes I use 10-, 20-, 50 day or week moving averages, it all depends and this is just a tool anyone can use by going on StockCharts.com, it cannot be used as the sole factor to make an investment or trading decision.

Why? Because markets are continuously in motion, there are macro, geopolitical, regulatory and other risks which can impact stocks at any given moment. I use charts to gauge some important levels but it's certainly not the only thing I use to gauge my investment and trading decisions.

By far, macro risks are the most important risks impacting markets which is why I always tell people, get your macro calls right or else in you're in big trouble.

I focus a lot on macro in this blog because I worry about investors who don't understand the inflation disconnect being suckered into a market phishing for inflation phools, underestimating the risks of a confounding market, not knowing where to invest.

When I read Bill Gross says the Fed can’t raise rates as fast as everyone thinks, I stop to ponder his points and agree, there's too much leverage in the system for the Fed to hike aggressively, but it still doesn't mean the yield curve won't invert in the second half of the year as short rates stay high and long rates decline as global PMIs decelerate.

Importantly, the real risk to tech shares coming due is a slowing global economy, not some blow-up in large hedge fund quants chasing momentum strategies. Big tech stocks do well in the initital stages of a slowing economy but if things get bad, they too succumb to the pressure.

Interestingly, it was old tech like Microsoft (MSFT) which did particularly well this week, and this falls in line with what Francois Trahan recommended in my Outlook 2018: Return to Stability, namely, focus on safer tech like software going into the new year.

One thing I will warn you of, be very careful buying the dips on large cap tech stocks (XLK), do not buy the dips blindly because you will get your head handed to you:

Some of you who think trading is easy, "just buy the dips on large-cap tech stocks", are cruising for a bruising and I don't care who you are and what your track record is, you need to pay attention here.

Last week, I told you to stay defensive and that my highest conviction long on a risk-adjusted basis remains good old boring US long bonds (TLT) which are doing great despite the bond teddy bear market in Q1:

Sure, there are big opportunities trading stocks, especially small cap biotech stocks like Geron (GERN) which hit a low of $3.49 on Wednesday before bouncing back up big on huge volume, but are you willing to take the binary risk that goes along with trading small cap biotechs?(click on image):

Before you answer "Hell Yes! I want to trade small cap biotechs too!", check out what happened to shares of Edge Therapeutics (EDGE) this week, they got annihilated, down more than 90% (click on image):

Technical analysis would have told you to "buy the breakout" and then you would have felt like this poor chap if you had put all your money in "Edge" Therapeutics:

All joking aside, be careful here, as I keep warning you, the second half of the year will be challenging and many momo chasers will get clobbered thinking it's business as usual, just buy the dips or rips.

I could be wrong, markets are up nicely on the last trading day of the quarter, and there are some big movers on my watch list late Thursday afternoon (click on image):

Just be careful, I trade and watch these markets like a hawk, there is a lot more volatiity and that's not typically a good sign at this stage of the cycle.

Those of you who hate trading, just forget about these crazy markets, put 50% of your money in the S&P (SPY) or S&P Low Vol (SPLV) and 50% into US long bonds (TLT). In fact, I would even recommend 60% or 70% US long bonds here.

In terms of where to invest, I think US long bonds (TLT) are the ultimate diversifier and the US dollar (UUP) will appreciate over the coming two years, and I'm positioned more defensively in equities focusing on stable sectors like healthcare (XLV) and consumer staples (XLP) and interest-rate sensitive sectors like utilities (XLU), telecoms (IYZ) and REITs (IYR).

Given this defensive stance, I'm underweight cyclicals like energy (XLE), financials (XLF), metals and mining (XME) and industrials (XLI).

Right now, I'm also short tech (XLK) and semiconductors (SMH) and would steer clear of value traps like oil service stocks (OIH) which remain cheap despite the rise in oil prices, and will remain cheap as the global economy slows.

I'll be back next Tuesday, going to take the long weekend off. Please kindly remember to contribute to this blog via PayPal on the top right-hand side, under my picture and help support my efforts in bringing you great insights on pensions and investments.

Below, Sam Stovall, CFRA chief investment strategist, and David Joy, Ameriprise Financial chief market strategist, discuss the volatility trends in the market right now and what investors are thinking as the first quarter comes to close.

And Jim Paulsen, the Leuthold Group's chief investment strategist, discusses the state of the market with Michelle Caruso-Cabrera (from Wednesday).

I agree, there's not enough panic yet, but with six rate hikes already under our belt, it won't take much to push this market into panic mode, which is why I remain defensive.

Lastly, the “Fast Money” traders discuss whether investors should trust the bounce in the markets. Until you see these markets making new 52-week highs, don't trust any bounce in the short run.

Comments

Post a Comment