Market Worried About New Covid or Inflation Variant?

U.S. stocks dropped sharply on Friday as a new Covid variant found in South Africa triggered a global shift away from risk assets.

The Dow Jones Industrial Average dropped 905.04 points, or 2.53%, for its worst day of the year, closing at 34,899.34. The S&P 500 lost 2.27% to close at 4,594.62, while the Nasdaq Composite slipped 2.23% to finish at 15,491.66. The Dow was down more than 1,000 points at session lows.

The downward moves came after WHO officials on Thursday warned of a new Covid-19 variant that’s been detected in South Africa. The new variant contains more mutations to the spike protein, the component of the virus that binds to cells, than the highly contagious delta variant. Because of these mutations, scientists fear it could have increased resistance to vaccines, though WHO said further investigation is needed. On Friday, the WHO deemed the new strain a variant of concern and named it omicron.The United Kingdom temporarily suspended flights from six African countries due to the variant. Israel barred travel to several nations after reporting one case in a traveler. Two cases were identified in Hong Kong. Belgium also confirmed a case.

“When I read that there’s one [case] in Belgium and one in Botswana, we’re going to wake up next week and find one in this country. And I’m not going to recommend anyone buy anything today until we’re sure that isn’t going to happen, and I can’t be sure that it won’t,” CNBC’s Jim Cramer said.

Bond prices rose and yields tumbled amid a flight to safety. The yield on the benchmark U.S. 10-year Treasury note fell 15 basis points to 1.49% (1 basis point equals 0.01%). This was a sharp reversal, as yields jumped earlier in the week to above 1.68% at one point. Bond yields move inversely to prices.

Asia markets were hit hard in Friday trade, with Japan’s Nikkei 225 and Hong Kong’s Hang Seng index both falling more than 2%. Germany’s Dax index slid more than 4%. Bitcoin fell 8%.

The Cboe Volatility Index, often referred to as Wall Street’s “fear gauge,” rose to 28, its highest level in two months. Oil prices also tumbled, with U.S. crude futures down 12% and breaking below $70 per barrel.

Travel-related stocks were hit hardest with Carnival Corp. and Royal Caribbean down 11% and 13.2%, respectively. United Airlines dropped more than 9%, while American Airlines dropped 8.8%. Boeing lost more than 5% and Marriott International fell nearly 6.5%.

Bank shares retreated on fears of the slowdown in economic activity and the retreat in rates. Bank of America dropped 3.9% and Citigroup slid 2.7%.

Industrials linked to the global economy declined led by Caterpillar off by 4%. Chevron dropped 2.3% as energy stocks reacted to the rollover in crude prices.

On the flip side, investors huddled into the vaccine makers. Moderna shares surged more than 20%. Pfizer shares added 6.1%.

Some of the stay-at-home plays that gained in the earlier months of the pandemic were higher again. Zoom Video and Peloton each added more than 5%.

Friday was a shortened trading day because of the Thanksgiving holiday with U.S. markets closing at 1 p.m. ET. Holiday weeks often have relatively light trading volume, which can amplify moves in the market.

“It’s important to stress that very little is known at this point about this latest strain, including whether it can evade vaccines or how severe it is relative to other mutations. Therefore, it’s hard to make any informed investment decisions at this point,” Bespoke Investment Group’s Paul Hickey said in a note to clients. “Historically speaking, chasing a rally or selling into a sharp decline (especially on a very illiquid trading day) rarely ends up being profitable, but that isn’t stopping a lot of people this morning.”

Several investment professionals told CNBC on Friday that the sell-off could be a buying opportunity.“Friday is the day after Thanksgiving, probably not as many traders on the desks with an early close today. So potentially lower liquidity is causing some of the pullback,” Ajene Oden of BNY Mellon Investor Solutions said on CNBC’s “Squawk Box.” “But the reaction we’re seeing is a buying opportunity for investors. We have to think long-term.”

A Black Friday to remember, or should I say red Friday.

Nothing like news of a heavily mutated Covid variant emerging from southern Africa to raise everyone's anxiety level:

A heavily-mutated Covid variant emerges in southern Africa: Here's what we know so far https://t.co/m8Z9emEdWN

— Leo Kolivakis (@PensionPulse) November 26, 2021

For weeks, South Africa was reporting around 200 COVID cases a day. On Thursday, that number hit 2,459 new cases. As scientists worked to determine the cause of the spike, they identified a new coronavirus variant. https://t.co/eAt4bRGHLO

— Toronto Star (@TorontoStar) November 26, 2021

What I find somewhat perplexing is how aloof people became about Covid.

I'm not just talking about the unvaccinated, I'm also talking about the vaccinated who wrongly thought "everything is fine, I might just need a booster shot but life is resuming back to normal."

Think again. If this Covid pandemic taught us anything, it's that this virus is very dangerous, it's constantly mutating and the world is a lot smaller than we think.

Travel bans won't stop the spread of any mutations, this much I can assure you.

By the time they implement them, it's already too late.

Yes, testing is critically important and we need to beef up testing.

But there are parts of this world that are literally breeding grounds for Covid viruses, especially in southern Africa where massive poverty and inequality are endemic and there are a lot of immuno-comprimised AIDS patients.

This is why scientists have been pounding the table, it's a global virus and that will entail a global response.

Anyway, here's what we know so far about this new variant:

- The World Health Organization said a heavily mutated version of the virus that causes Covid-19 poses a possible increased risk of reinfection.

- The WHO labeled the strain as omicron and said it’s a variant of concern.

- South African scientist Tulio de Oliveira said in a media briefing that the variant contains more than 30 mutations to the spike protein, the component of the virus that binds to cells.

Of course, the knee-jerk reaction in markets is a massive RISK-OFF move, sell everything, buy US Treasuries and hunker down waiting for Armageddon.

Add to this it's a short trading week because it's US Thanksgiving and the only people trading on Wall Street are algorithmic robots and presto, you have massive panic and huge volatility.

By this time next week, I expect things will calm down considerably.

Having said this, we don't know what this new variant will mean. Will there be more lockdowns? Will we need new boosters? Will there be a much deadlier wave coming this winter?

I certainly hope not but you can't exclude any of this right now as we simply don't know enough about the new variant and how fast it will spread throughout the world.

The knee-jerk reaction on Wall Street was predictable and somewhat exaggerated.

At one point, Moderna's shares were up almost 30%. 30%!!

Don't get me wrong, on Friday November 5, I discussed whether the US recovery will kill the market and recommended buying Moderna shares because I thought the selloff was overdone.

But today's action on Moderna and other vaccine stocks was just plain algorithmic silliness:

Like I said, this is what happens when algorithmic trading dominates markets and everything is based on news flow.

Once humans get back to work next week, things will calm down, as long as news about this new Covid variant doesn't go from bad to disastrous.

Not surprisingly, travel stocks took a beating, with cruise lines, casinos, hotels and airlines all getting hammered hard today:

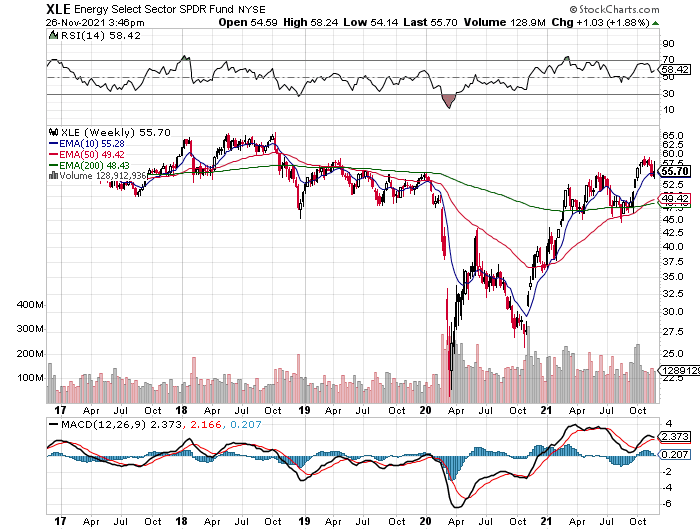

What else got hit? Energy stocks as oil dropped 11% to below $70 in one of the worst days of 2021:

Oil drops 11% in worst day of 2021, breaks below $70 as new Covid variant sparks global demand concerns https://t.co/DaQmqdht8i

— Leo Kolivakis (@PensionPulse) November 26, 2021

However, while energy was the worst performing sector today, all sectors got hit hard except Healthcare which was down marginally:

As far as the overall market, always know your levels to gauge risks. I do this by looking at daily and weekly levels on the S&P 500 ETF (SPY) very closely:

Experienced traders also use monthly levels but the main point I am going to make is while today's price action was ugly, this is just another correction, the trend in stocks remains solidly up.

The TINA effect (there is no alternative) is what's behind the uptrend in stocks.

Jennifer Beaty posted the chart below on Linkedin stating this: "Almost $900 billion has been invested into equity exchange-traded and long-only funds in 2021 - exceeding the combined total from the past 19 years!"

I couldn't resist to add my two cents on Linkedin, stating this:

The Fed has convinced everyone that stocks can ONLY go up, up and away and that bonds are worthless. Follow the masses, for now, but be prepared for a MAJOR reversal of fortune..

Now, this exchange occurred yesterday and of course, I had no idea stocks were going to sell off hard today.

My point is when everyone is dancing on one side of the dance floor and the foundations are weak, something will give way and the results will be tragic.

Yes, the Fed is accommodative and stands ready for any emergency but don't kid yourself, the Fed will taper and only delay rate increases if this new Covid variant proves really nasty.

In case you haven't been paying attention, there's another variant worth worrying about, the new inflation variant.

Everyone is trying to determine whether this new inflation variant is sticky or transitory.

Brian Raabe of Trahan Macro Research posted this on Linkedin which Francois Trahan shared:

Inflation is biting all over the world and many central banks are raising rates:

How one rate hike by a small African nation could derail Powell’s Fed inflation-fighting plans and sink stocks https://t.co/aJbwyb7X6Q via @Yahoo

— Leo Kolivakis (@PensionPulse) November 25, 2021

In the US, the surge in inflation is forcing big investors to recalibrate their strategies.

How will the new Covid variant impact inflation? If it's bad, it will hit economic activity, lowering inflation pressures but it might then add to supply chain woes and we can have a nastier bout of inflation.

All this remains to be seen.

I leave you with some more food for thought on this Black Friday.

Catalin Zimbresteanu, a former colleague of mine at PSP, told me to have a look at the price index (not total return) of the iShares High Yield Corporate Bond ETF (_HYG) which is breaking down here:

Trouble in credit land typically precedes trouble in stocks.

In fact, Pierre-Philippe St-Marie, co-CIO at Optimum Asset Management, shared this with me on credit risk three days ago (before new variant hit):

The pandemic situation in Europe is for the moment degrading, unexpectedly and degrading fast. Given how vaccinated the population is, it is somewhat concerning.

European spreads we follow moved from 82 to 97 in the last few days. This is a significant widening after an extended period of calm at the tight of the range.

In the United States, with Jerome Powell being re-nominated when the alternative (Lael Brainard), was in our opinion perceived by the market as being more dovish, market sentiment might also be turning in North America.

We are according to our analysis globally at tight spreads if you are looking at historical levels. We could have a retracement, perhaps a significant one, without seeing an all out rout.

It’s never a good time to be asleep at the wheel in institutional investment, now even less than usual.

I thank Pierre-Philippe for his astute market insights and he definitely knows what he's talking about and has a long track record to back up his comments (at one point, he and his team were generating all the trading revenues at the National Bank of Canada, trust me, he's really good and very modest).

Alright, let me wrap it up there but before I do, please take the time to read this article on monetary and inflationary traps by Raghuram G. Rajan, former governor of the Reserve Bank of India, and Professor of Finance at the University of Chicago Booth School of Business (h/t: Jean-Francois Sabourin).

It is packed with food for thought but this passage rings true:

But it is not just the new framework that limits the effectiveness of the Fed’s actions. Anticipating loose monetary-policy and financial conditions for the indefinite future, asset markets have been on a tear, supported by heavy borrowing. Market participants, rightly or wrongly, believe that the Fed has their back and will retreat from a path of rate increases if asset prices fall.

This means that when the Fed does decide to move, it may have to raise rates higher in order to normalize financial conditions, implying a higher risk of an adverse market reaction when market participants finally realize that the Fed means business. Once again, the downside risks of a path of rate hikes, both to the economy and to the Fed’s reputation, are considerable.

Will the Fed bungle it up? Maybe, that remains to be seen.

Mohamed El-Erian seems to think the Fed's inflation screwup will 'go down in history'.

I'm not convinced and still fear the risks of deflation are much, much bigger now than the risks of permanent inflation.

How so? If the Fed does start raising rates aggressively and markets crash, we will see a financial shock ripple across the world creating economic devastation, much like we saw during the 2008 GFC.

There are a lot of moving parts to these markets, but one thing I did notice this week is apart from today, the greenback is gaining strength:

There are a lot of reasons why including the Fed tapering and that global investors are buying US public and private assets and want to hold more US dollars in case of a crisis erupts.

But also keep in mind, a strengthening US dollar is disinflationary because it will lead to lower import prices as Americans buy a lot of foreign goods.

All this to say, yes, we have inflation, no doubt about it, but unless I see it sticky wage inflation, I'm far from convinced it is a serious bout of inflation.

Then again, professor Cam Harvey posted this on Linkedin:

We are in an inflation surge. If you follow me, you know that I have been very critical of the “don’t worry, it is transitory” spin on the recent inflation reports. Even today’s media coverage mainly focuses on the transitory items. Sure, some of the inflation is transitory – that is obvious – but not all. Yes, used cars are up 26.4% YoY but that is only 3.3% of the CPI basket. I have focused on the important shelter component which constitutes one third of the CPI. The latest CPI report shows rent and owners’ equivalent rent up only 2.7% and 3.1% YoY. Yet, Case-Shiller 20 City house price index is up 19.7% and Apartment List median rent is up 16.4% (Jan-Oct). Unfortunately, there is likely more inflation to come. This is the 9th surge in 95 years of US data.

I will leave it at that but Cam Harvey is a really smart guy. I know, I almost invested in his CTA fund 20 years ago and the man really impressed me.

Alright, let me wrap it up there.

Below, Michael Yee from Jefferies and Jared Holz from Oppenheimer join 'Closing Bell' to discuss the impact of the new Covid variant and what that means for markets.

Second, Dr. Scott Gottlieb, former FDA commissioner, joins 'Closing Bell' to discuss the new Covid-19 variant. He says if the majority of the population is vaccinated it can be effective in protecting people from the new Covid variant.

Of note: The 4 cases of new variant identified in Botswana were incidentally detected in well people tested before air travel, and South African Medical Association chief said - so far - symptoms seen are "mostly mild symptoms, and we haven’t seen a spike in hospital admissions." pic.twitter.com/KwiraY3V0u

— Scott Gottlieb, MD (@ScottGottliebMD) November 26, 2021

Third, Tom Lee, Fundstrat global advisors, joins 'Closing Bell' to discuss where investors should put their money amid the markets sell-off.

Lastly, please take the time to listen to a great discussion between Glenn Loury and Laurence Kotlikoff on the Glenn Show discussing fending off inflation (h/t: Fred Lecoq).

Comments

Post a Comment