Jacob Serebrin of the Montreal Gazette reports the Caisse posts 9.4% return for 2024, sees economic uncertainty ahead:

The CEO of Quebec’s

public pension fund manager said he is counting on its diverse portfolio

to help it navigate increasing economic uncertainty as he announced

investment returns of nearly $40 billion in 2024.

The

Caisse de dépôt et placement du Québec reported a 9.4-per-cent return

on its investments in 2024 on Wednesday, which it credited to surging

tech stocks in the United States but which was held back by losses in

its real-estate portfolio.

While the return was

up from the 7.2-per-cent return the CDPQ posted in 2023, it lagged the

fund manager’s benchmark portfolio — a similar basket of investments it

uses to measure performance — which had a return of 11.8 per cent.

Charles

Emond, the president and CEO of the CDPQ, said that while he expects

turbulence and volatility in the near future, the past five years have

also been marked by instability.

Despite

the pandemic, increases in inflation and interest rates, the fund has

increased by $133 billion over the past five years.

“The

reality is we have a strong portfolio that has been proven many times,

and what matters is making sure that we have enough money all the time

for the pension liabilities our clients need to deliver, and from that

perspective we have very good starting point,” he said.

Emond

said he expects U.S. President Donald Trump’s policies to have an

effect across the economy, with lower growth, higher inflation and

higher interest rates.

Emond also defended

the management of the Réseau express métropolitain, which is owned and

managed by the fund’s CDPQ Infra subsidiary and has suffered frequent service outages this winter.

“I

can easily understand why when users are not happy with the service

right now. It’s been unacceptable from our standards,” he said, adding

that Alstom and AtkinsRéalis, the companies that hold the contracts to

provide the REM with rolling stock as well as operations and

maintenance, are aware of this at “the highest levels.”

“It’s

important not to throw away the baby with the bathwater. In the last

two, three weeks, the service wasn’t there, but our operators recognize

our responsibilities,” he said. “We’re going to continue to assume our

own responsibilities, making sure they deliver on a service that is

supposed to work in Quebec during winter.”

Those

companies have committed to making changes that have been suggested by

the CDPQ, Emond said, and despite the REM’s recent struggles, he

maintained it was built at a competitive price and at a much faster pace

than any comparable project worldwide.

The Quebec Pension

Plan, which accounts for about one-third of the CDPQ’s investments, had a

return of 11 per cent in 2024. It has now had a return of 7.3 per cent

over five years and 8.1 per cent over 10 years.

The CDPQ also manages investments for 47 other public and para-public pension funds and insurance plans.

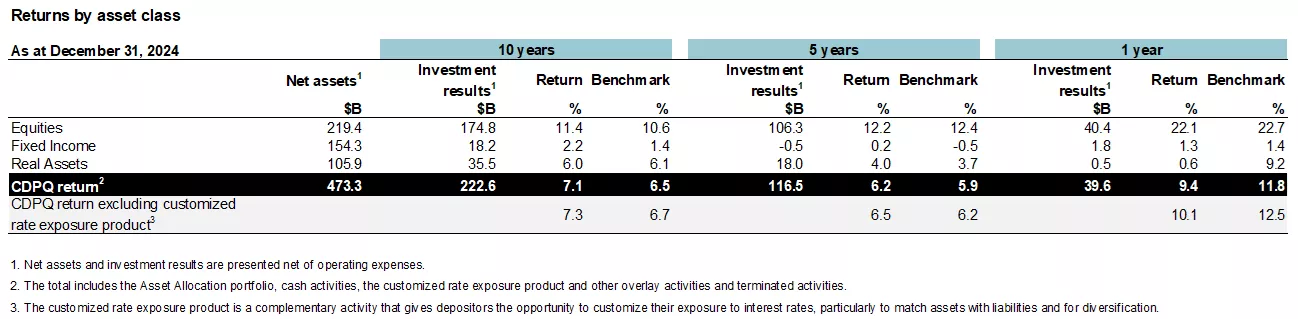

Equity

investments, which account for about a quarter of the CDPQ’s portfolio,

had a 25.5-per-cent return in 2024, which was driven by a handful of

large U.S. tech companies that had major gains on the stock market.

While

2024 was good for investments in the stock market, Vincent Delisle, the

CDPQ’s head of liquid markets, said the fund has reduced the risk of

its investments since the beginning of 2025.

The CDPQ’s private equity investments generated a 17.2-per-cent return as companies in its portfolio increased profits.

However,

those gains were muted by lower returns in fixed income. The asset

class, which includes bonds, returned 1.3 per cent as increasing

long-term bond yields led investors to buy new bonds, pushing down the

value of existing bonds.

The

fund’s real-estate portfolio continued to report losses, with a loss of

10.8 per cent in 2024, which Emond said was due to the struggling

office sector in New York and Chicago.

Over the past five years, the portfolio has lost an average of 2.2 per cent a year.

Layan Odeh of Bloomberg also reports CDPQ misses benchmark in 2024 as real estate losses worsen:

Canadian pension manager Caisse de Depot et Placement du Quebec posted a

9.4% return last year as gains from its investments in private equity

and stocks offset losses in real estate.

The returns, which came below its benchmark of 11.8%, brought the

pension plan’s net assets to C$473 billion ($330 billion) as of Dec. 31.

“Our performance was driven by our equity market, private

equity and infrastructure activities,” Chief Executive Officer Charles

Emond said in a statement Wednesday. He added that returns were

“affected by persistent headwinds in real estate, particularly in the US

office sector.”

Private equity holdings gained 17.2% amid growth in portfolio

companies, particularly in the industrials and consumer goods sectors.

Its public equity portfolio fared better, returning 25.5% and beating

its benchmark of 24.1% in what was a sizzling year for stocks.

CDPQ’s

real estate investments delivered a 10.8% loss, mainly because its

office portfolio is heavily concentrated in New York and Chicago, two

hard-hit cities. That performance is worse than the segment’s 2023 loss

of 6.2% and is the third loss in five years.

The CDPQ is moving to

being an investor in real estate rather than being an operator, Emond

told reporters in Montreal Wednesday, adding that he’s looking for more

liquidity and partners in the segment.

He expects the real estate

portfolio to eventually outperform its benchmark as the fund implements

improvement measures in the next 18 to 24 months. The CEO acknowledged

that would be a huge undertaking.

Canada’s second-largest pension

fund is leaning toward reducing its exposure to real estate while also

focusing on repositioning the portfolio. “The reality is it’s not so

much the percentage of what we own that’ll be the main driver, but

rather how do we invest it,” Emond said in an interview. The pension

fund manager aims to be a net seller of offices and will deploy a

majority of real estate capital into new sectors such as logistics,

including warehouses and self storage, he added.

CDPQ expects uncertainty and volatility to continue this year as the

US administration implements drastic changes, including imposing tariffs

on neighboring countries, as well as Europe and China. Around 5% to 6%

of the pension fund manager’s overall portfolio would be directly

impacted by tariffs, according to Emond.

Domestically, CDPQ

deployed C$4.3 billion in new investments and commitments, increasing

its assets in Quebec to C$93 billion. The pension fund manager expects

to reach C$100 billion in 2026 as planned.

Some of its

investments in the province last year included a C$500 million

investment to support National Bank of Canada in acquiring Canadian

Western Bank and a C$158 million investment in WSP Global Inc. to help

it buy US-based Power Engineers.

Northvolt Writedown

The

pension fund wrote down its $150 million investment in Northvolt AB to

zero, Kim Thomassin, CDPQ’s head of Quebec, told reporters. The electric

vehicle battery maker filed for bankruptcy protection last year.

Canada’s

largest pension plans poured money into the Swedish firm, which

announced plans in 2023 to build a factory not far from Montreal to

serve auto companies in the North American market. Ontario Municipal

Employees Retirement System made three “major” investments, according to

a LinkedIn post last year. Canada Pension Plan Investment Board and the

Investment Management Corp. of Ontario also allocated money to

Northvolt.

IMCO wrote down its $400 million investment, Bloomberg

reported earlier this month, joining investors such as BlackRock Inc.

and the Danish pension fund ATP.

The Canadian Press also reports US real estate ate into CDPQ returns in 2024:

Office towers in major U.S. cities have eaten

into the results of the Caisse de dépôt et placement du Québec (CDPQ),

which on Wednesday reported a return below its benchmark index.

Quebecers'

nest egg reported a return of 9.4 per cent for 2024, below its

benchmark portfolio of 11.8 per cent, according to annual results

released on Wednesday.

Over five years, the annualized return was 6.2 per cent, which was higher than the benchmark of 5.9 per cent.

The

basic plan of the Quebec Pension Plan (QPP), administered by Retraite

Québec, posted a return of 11.0 per cent. The returns of its nine

largest depositors ranged from 6.7 per cent to 11.1 per cent.

CDPQ

president and CEO Charles Emond explained that the office sector was

facing “persistent headwinds” in his introductory remarks at a press

conference.

The return on the property

portfolio declined by 10.8 per cent in 2024. This was significantly

below its benchmark index, which showed a slight increase of 1 per cent.

The Caisse attributed this setback to its heavy concentration in the office property sector in New York and Chicago.

Overall,

the Caisse beat its benchmark for equity markets, but underperformed in

private equity, fixed income, real estate and infrastructure.

The Caisse’s management fees were 0.6 per cent, compared with 0.83 per cent a year earlier.

Earlier today, CDPQ issued a press release stating it posted a 9.4% return in 2024, net assets increased nearly $40 billion to $473 billion:

The base plan of the Québec Pension Plan, which represents the

pensions of more than six million Quebecers and is the largest fund

invested with CDPQ, posted a return of 11.0%

The financial health of depositors’ plans remains excellent

Investments in Québec reached $93 billion, on the way to achieving the ambition of $100 billion in 2026

CDPQ today presented its financial results for the

year ended December 31, 2024. The weighted average return on its

depositors’ funds was 9.4% for one year, below its benchmark portfolio’s

11.8% return. Over five years, the annualized return was 6.2%, above

the 5.9% return of its benchmark portfolio. Over ten years, it

earned 7.1%, also above the benchmark portfolio’s 6.5%. As at

December 31, 2024, CDPQ’s net assets totalled $473 billion.

“The

2024 market environment was characterized by the vitality of the U.S.

economy, rising long-term bond yields and a historic level of

concentration in the main stock indexes, boosted by technology

companies. During this period, our performance was driven by our equity

market, private equity and infrastructure activities, but was affected

by persistent headwinds in real estate, particularly in the U.S. office

sector,” said Charles Emond, President and Chief Executive Officer of CDPQ.

“For one year, the Québec Pension Plan, which represents the pensions

of more than six million Quebecers, posted a return of 11.0%.”

“While

uncertainty is high, particularly due to ongoing tariff negotiations,

discipline and the sound diversification of our portfolio will remain

key to delivering the long-term returns our depositors need. Their plans

remain in excellent financial health, and our results for one, five and

ten years have made a significant contribution, despite the

turbulence,” concluded Mr. Emond.

Return highlights

As

at December 31, 2024, CDPQ’s investment results totalled $40 billion

for one year, $116 billion over five years and $223 billion over

ten years.

CDPQ manages the funds of 48 depositors—mainly for

pension and insurance plans. The overall portfolio’s one-year, five-year

and ten-year returns represent the weighted average of these funds. To

meet their objectives, investment strategies are adapted to their

individual risk tolerances and investment policies. In 2024, there was a

pronounced difference between the returns of the nine largest funds of

CDPQ’s depositors, reflecting variations in their asset allocation

choices. For one year, the returns ranged from 6.7% to 11.1%. Over

longer periods, the annualized returns varied between 4.2% and 7.3% over

five years, and between 5.7% and 8.1% over ten years.

The largest

fund invested with CDPQ, the base plan of the Québec Pension Plan,

administered by Retraite Québec, posted a return of 11.0% for one year,

7.3% over five years and 8.1% over ten years. As at December 31, 2024,

its net assets were $142 billion, including the additional plan.

It is worth noting in 2024 the significant impact

that the customized rate exposure product—a tool depositors have been

using increasingly in the last two years—had on the overall portfolio’s

performance. This product provides depositors with an opportunity to be

more exposed to the rate factor, in particular to ensure better matching

with their long-term liabilities, thereby providing more stability to

the funding of their plan, but making the return on their funds more

sensitive to rate fluctuations.

With rising rates as seen in

recent years, these activities have limited the performance of CDPQ’s

overall portfolio. Conversely, depositor plan liabilities declined in

general, which, combined with the return on assets, improved their

financial health.

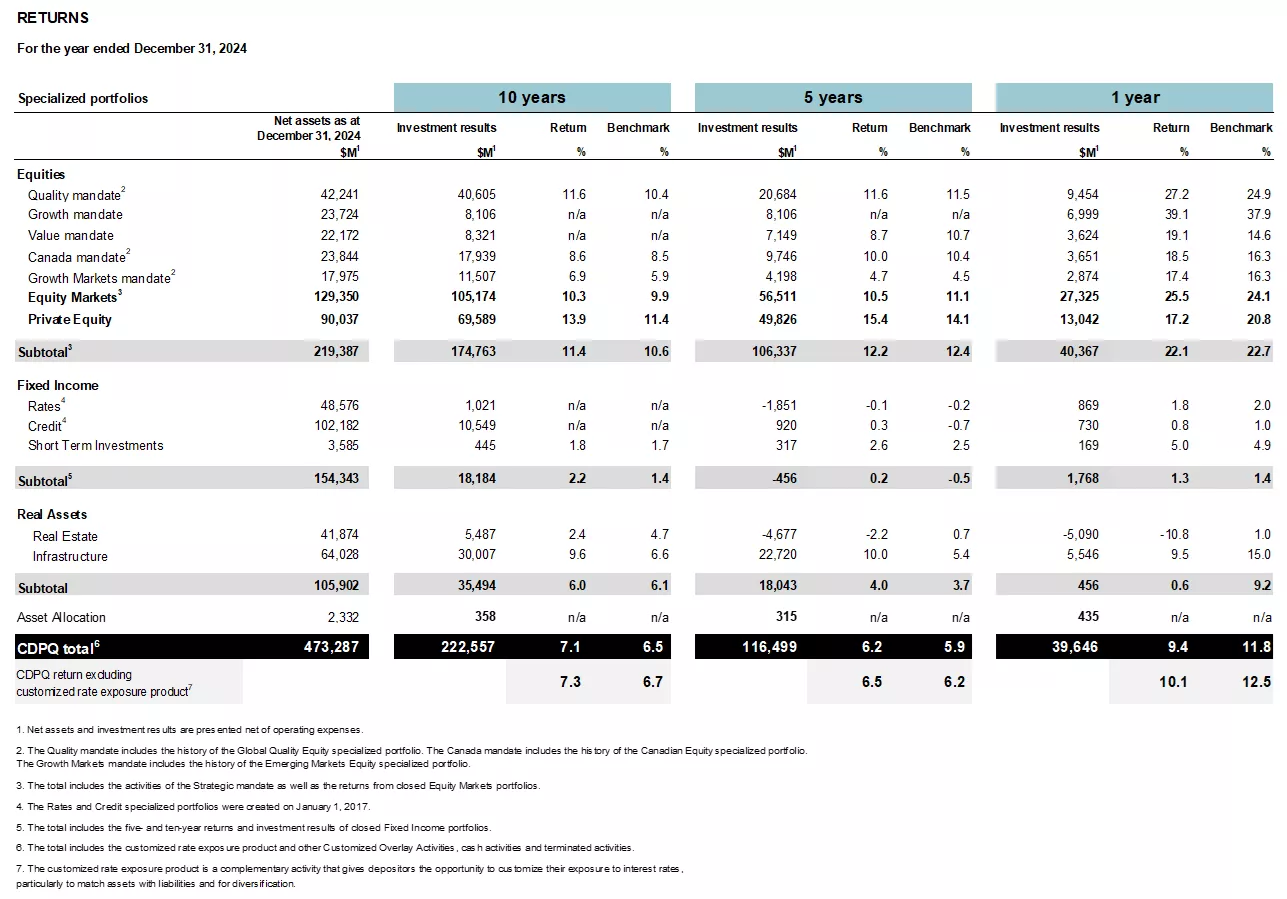

Equities

Equity Markets: Excellent performance in markets where gains remain highly concentrated

Against

a backdrop of surging stock market indexes whose gains remain very

concentrated in U.S. tech stocks, the Equity Markets portfolio has done

well while holding the course on a diversified approach. In 2024, the

portfolio was the main performance driver among CDPQ’s major portfolios.

It recorded a 25.5% return and surpassed its benchmark index’s 24.1%.

The performance is explained by the quality of execution by portfolio

managers. The portfolio has also benefited from increased exposure in

recent years to growth and tech stocks, propelled by advances in

artificial intelligence.

Over five years, the portfolio’s

annualized return was 10.5%, below the index’s 11.1% return. The

difference is mainly explained by its significant underweighting in

major U.S. tech stocks in 2020.

Private Equity: Strong recovery due to companies’ growth

After

being affected by the high interest rate environment in 2023, the

Private Equity portfolio rebounded in 2024. For the one-year period, it

generated a 17.2% return, thanks to sustained growth in the

profitability of portfolio companies, particularly in the industrials

and consumer goods sectors. Its index recorded a higher return,

at 20.8%, reflecting its greater exposure to public markets driven by

large tech companies.

Over five years, the allocation to the

financial, consumer goods and technology sectors, combined with an

advantageous positioning in Québec, allowed the portfolio to post an

annualized return of 15.4%, compared to 14.1% for its index.

Fixed Income: Hike in long-term rates slows performance

Despite

a context of monetary easing that resulted in the main central banks

cutting key rates, U.S. bond yields moved in the opposite direction

in 2024. Economic vitality in the United States and uncertainties

surrounding the fiscal and trade policies favoured by the country’s new

administration led to a significant increase in long-term rates. In this

environment, the Fixed Income asset class posted a 1.3% one-year

return, slightly below the index’s 1.4%. The current yield was high,

at 6.2%, benefiting from the high premiums on private credit. However,

performance was affected by the impact of higher rates.

Over five

years, the asset class posted an annualized return of 0.2%, due to the

historic market correction in 2022 which is still being felt, compared

to the index, which was at -0.5%. The good performance of credit

activities over the period compensated for the decline in value.

Real Assets

Infrastructure: A portfolio that delivers year after year

The

Infrastructure portfolio continued to deliver solid results in 2024,

with a 9.5% return supported by the excellent performance of port and

energy assets, as well as high current yield. With a return of 15.0%,

the index was driven by the public stocks included in it, particularly

in the energy and electricity sectors, with the latter rising strongly

during the year, stimulated by the needs related to the outlook in

artificial intelligence. In a very competitive market, the teams

executed transactions in a disciplined manner during the year, including

significant sales in the airport sector in Europe and additional

investments in high-performing companies.

Over five years, the

annualized return was 10.0%, against the index’s 5.4% return. The

portfolio benefited from good asset diversification and consistent

current yield. Renewable energy, ports and telecommunications were the

largest contributors to performance.

Real Estate: Longstanding exposure to U.S. office sector weighs on performance

Challenges

in the real estate industry continued in 2024, mainly due to persistent

issues in the office sector. Holding more office building assets in the

United States than its benchmark index, and with a strong concentration

in New York and Chicago, the two hardest-hit cities, the portfolio

posted a -10.8% one-year return, below its index’s 1.0%. In contrast,

the logistics sector, despite a global slowdown, has been resilient, as

has the shopping centre sector, where teams have made strategic

dispositions since 2020 and invested in well-positioned assets in

the portfolio.

Over five years, the portfolio’s annualized return

was -2.2%, below the index’s 0.7% return. The negative performance is

again explained by the longstanding concentration in the U.S. office

sector and by overexposure to shopping centres at the beginning of the

period. However, the exposure to logistics, which has increased over

five years, was profitable during the period.

Québec: Ongoing team mobilization supports businesses and projects that contribute to economic development

In

2024, CDPQ deployed $4.3 billion in new investments and commitments,

increasing its assets in Québec to $93 billion. This progress is still

in line with its ambition, announced two years ago, to reach

$100 billion in 2026 and reflects the mobilization of teams across all

asset classes.

Among the teams’ accomplishments during the year, we note:

Support to grow companies

A $500-million investment to support National Bank in its structuring acquisition of Canadian Western Bank

Support for Nuvei,

one of the most advanced technology providers in the global payments

industry, in its transformation into a privately held company, bringing

its value to over USD 6 billion

Acquisition of an equity stake in QSL International, a key maritime logistics player headquartered in Québec City

A $158-million investment in WSP to support the acquisition of U.S.-based POWER Engineers

An increased stake in Saputo,

one of the world’s largest dairy processors, through a $378-million

share purchase that makes CDPQ one of the largest shareholders

A $25-million investment in the initial public offering of Groupe Dynamite, a clothing retailer with approximately 300 stores, with ambitions for international growth

Infrastructure and real estate projects

Agreements between the Government of Québec, CDPQ Infra and Québec City to plan the TramCité project, including the tramway component of Phase 1 of the CITÉ plan

Continuation of dynamic testing on the Deux-Montagnes and Anse-à-l’Orme branches of the Réseau express métropolitain (REM) and planning for the next commissioning of the network in fall 2025

A $103-million loan to support the expansion of Vantage Data Centers’ facility in Québec City

Transition toward a more sustainable economy

Financial backing for Norda Stelo,

a renowned engineering firm operating in more than 50 countries, for

its acquisition of InnovExplo, creating a new force in the field of

critical minerals that are essential to the energy transition

A $35-million commitment to MKB Partners Fund III, created by MKB, a growth capital firm that invests in pioneering energy transition companies

In addition, at the end of 2023, CDPQ announced its ambition to more than double the size of amounts entrusted to external Québec managers

to reach $8 billion by 2028, thereby promoting the growth of Québec’s

asset management industry. As at December 31, 2024, these amounts were

$4.8 billion.

Capital aligned with a sustainable strategy

In

2024, through its initiatives, including advancing its climate

strategy, and international honours, CDPQ continued to exercise strong

leadership in sustainable investing.

A few examples:

For

a second straight year, CDPQ ranked at the top of the list of pension

funds included in Global SWF’s 2024 GSR Scoreboard, an internationally

recognized benchmark, which assesses the governance, sustainability and

resilience practices of 200 sovereign wealth and pension funds worldwide

CDPQ

ranked 4th on sustainability and transparency issues in a list of

75 international investment funds established by Top1000funds.com and

CEM Benchmarking

More recently, CDPQ ranked 2nd among nearly

sixty pension funds on the World Benchmarking Alliance’s Financial

System Benchmark, which assesses best practices in sustainable finance

More

details on CDPQ’s sustainable investing strategy, notably on its

progress on climate targets, will be presented in the Sustainable

Investing Report published in the spring.

Financial reporting

CDPQ

incurs costs to conduct its activities, including operating expenses,

external management fees and transaction costs. As at December 31, 2024,

the total cost for internal and external investment management

following the integration of the real estate subsidiaries is down

considerably, standing at 67 cents per $100 of average net assets,

compared to 83 cents per $100 of average net assets in 2023. The 2023

amounts have been adjusted to include the costs of real estate

subsidiaries in order to make them comparable to the 2024 amounts. This

total is down from the previous year due to efforts made following the

integration of real estate subsidiaries during the year and lower

external management fees compared to those paid in 2023. It should be

noted that, based on external data, CDPQ’s cost ratio is among the

lowest in its industry. Operating expenses were 23 cents per $100 of

average net assets for 2024, compared to 26 cents in 2023, on a

comparable basis.

The credit rating agencies reaffirmed CDPQ’s

investment-grade ratings with a stable outlook, namely AAA (DBRS),

AAA (S&P), Aaa (Moody’s) and AAA (Fitch Ratings).

ABOUT CDPQ

At CDPQ, we invest constructively to generate sustainable returns

over the long term. As a global investment group managing funds for

public pension and insurance plans, we work alongside our partners to

build enterprises that drive performance and progress. We are active in

the major financial markets, private equity, infrastructure, real estate

and private debt. As at December 31, 2024, CDPQ’s net assets totalled

CAD 473 billion. For more information, visit cdpq.com, consult our LinkedIn or Instagram pages, or follow us on X.

CDPQ is a registered trademark owned by Caisse de dépôt et placement du Québec and licensed for use by its subsidiaries.

Alright, CDPQ's 2024 results are out and not surprisingly, they're excellent despite the ongoing issues in real estate.

How did I know they'd be good? Because of its asset mix, CDPQ has more exposure to public equities than its peers and their performance there was stellar.

Earlier today, I had a chance to go over the results with Vincent Delisle, CDPQ's Head of Liquid Markets.

I want to begin by thanking him for taking the time to talk to me and also thank Kate Monfette for setting up this discussion.

We had a great discussion, especially on public markets which is what he's in charge of.

We started talking about Real Estate and came back to it later.

I told him one reporter called me and said that Charles Emond stated their Office portfolio is 80% concentrated in New York and Chicago, which I found to be high.

Vincent couldn't confirm that detail as it's not his portfolio but I went on to discuss how Charles stated they're shifting the strategy in Real Estate to be investors, not operators, allowing other companies to worry about operations.

The reporter also stated that Charles Emond said they have thousands of assets in Real Estate, a lot less in Infrastructure which is concentrated in fewer assets.

I also noted I just talked to OMERS CEO Blake Hutcheson on Monday going over OMERS' 2024 results, and he noted the cost of capital hit cap rates and values but quality real estate remains very much in demand across all sectors and those assets got hit a lot less.

Just by looking at Oxford's results over last two years compared to those at Ivanhoe Cambridge, tells me Rana Ghorayeb and her team have their work cut out for them in restructuring that portfolio.

Vincent responded:

Yes, she did inherit a bit of a challenge. Just to give you some colour on Charles's comments on the differences between Infrastructure and our Real Estate portfolio. We had 70 assets in the Infra book, 70 large ticket assets. Whereas the Real Estate portfolio is a few hundred lines.

That makes it more complicated.

But what Charles mentioned this morning, funds are part of the strategy in most of our portfolios, however, the clear shift in our Real Estate portfolio has been and continues to be going from an operating real estate company to investing in real estate.

That shift was initiated under Nathalie (Palladicheff) a few years ago and that shift in process and philosophy is still ongoing.

That's the key highlight in Real Estate, we're going from operating buildings to investing in real estate.

So basically the operational side of the real estate business (leasing and maintenance) is now being handled by a third party (ex. CBRE, JLL, etc.).

I then shifted my focus to overall results and told Vincent I wasn't surprised they were strong led by Public Equities where CDPQ has more tech exposure than its peers, a strong fundamental team and internal quant team (latter implemented under his watch).

He responded:

The 9.4% return, we are very happy. Depositors' needs run around 6-7% so the 9.4% is a number we are happy with.

This (9.4%) is the average of all depositors. Our CPP equivalent -- Regime de Retraite du Quebec (RRQ) -- came in at 11%. More risk taken in this portfolio.

We obviously had a good year in Public Equities because they had a good year in general.

We have indeed increased our exposure to technology because we had nothing five years ago (it was all in the Private Equity portfolio).

But stock selection really took us over the line here. We are underweight the Mag-7s.

This is not a Mag-7 story for us, this is very strong stock selection from our internal and external teams.

And the quant team which we talked about a year ago had another stellar year in 2024.

We've moved to a long/ short version -- 130/30 for that portfolio -- and all of our mandates beat their benchmark.

Obviously having more technology was helpful but it was really a year where all of our players scored goals and that makes me very, very happy.

I'll also remind you that 70% of our Public Equities assets are managed here on the sixth floor -- global equities, emerging market equities and obviously Canadian equities. Good year for execution there.

I was shocked to learn they were underweight Mag-7 stocks and still beat their benchmark by 140 basis points (25.5% vs 24.1%).

That is extremely impressive any way you slice it.

140 basis points value add on Public Equities when you're underweight Mag-7 proves everything went right, stock selection, manager selection, internal fundamental and quant teams all delivering alpha.

Vincent also told me to take all the 13-F noise on what they do with Mag-7 with a grain of salt because it's an end-of-quarter snapshot and "it captures monthly rebalancing, their financing activity (repos/ securities lending) and it captures a portion of our shift in conviction.”

[Note: You can view CDPQ's latest 13-F quarterly filing here and keep his comments in mind.]

He noted they have been in technology since 2021 and that obviously helped but they are still a very diversified portfolio.

I asked him how much currency gains factored into their overall results.

He didn't give me a figure not to give away too much of their hedging and non hedging activity but stated "suffice it to say on a year where public equities are up 25% and the US dollar is strong, it did add an impact of a few hundred basis points additional kick to the overall return."

Next, I shifted my attention to Private Equity which had an excellent year, up 17.2%.

Vincent added more insights here:

People look at Private Equity gaining 17.2% last year, whether it's us or others, you obviously can't beat Public Equities because of Mag-7 concentration.

When you look at it very naively (relative to Public Equities), Private Equity had a very bad year but the 17% is very strong. When you look at the companies in our portfolio, very strong profitability, 12% increase in EBITDA.

If you strip out the Mag-7 stocks from the S&P500, the S&P 493, profit growth last year was mid single-digit so we are making the right investments in Private Equity. Martin Longchamps reshuffled the process a couple of years ago when he got here, more fund investments and co-investments.

Solid execution there as well. It's tough to beat Public Equities but we had a very solid year there as well.

In Fixed Income, tough macro environment with rates gong up and staying higher most of last year, I noted Marc Cormier left the organization and returns were alright given the background.

Vincent thanked me for asking about Fixed Income because as he rightly notes, what happens to yields and rates drives everything and he rarely gets questions there.

He added:

On the performance side, tough few years in the asset class with rates moving higher.

We are still increasing our exposure to Private Credit, we are executing there very well, but move in yields higher offset the premium there.

Marc Cormier retired. He was with us for 30 years and we haven't decided yet what structure we will implement.

Fixed Income has gone from 100% government bonds up until 2016 and today we $100 billion in Credit, $50 billion in government bonds. Out of the $100 billion in Credit, 70% is private, 30% is public.

I'm looking at how we differentiate the private aspect vs the public aspect but Marc just left in early February and we are looking at what type of organizational structure we want to reflect new reality in bonds.

I told Vincent I am also fixated on rates and I see serious risks that inflation will pick up and this will be a problem for the Fed, the bond market, the stock market, CDPQ and other investors.

He replied:

Tariff discussions are complicated. They are complicated because a lot of people determine the most obvious scenario is the one we are going to have.

Tariffs leading to inflation is obviously a major concern. Tariffs leading to a weaker Canadian dollar is a very likely scenario. Tariffs leading to a lower S&P is a very likely scenario but on yields, I'm not so sure.

I'm not so sure because the more tariff chaos Trump brings to his allies, is now bringing some chaos to the US. The most recent survey, whether it's consumer confidence or ISM, have declined sharply from a few months ago. And the bond market is telling you right now it's more worried about growth risk than inflation risks.

All this to say when we look at how we can position ourselves for the tariffs risks, it's clearer to us what the outcome will be on currencies (stronger USD), it's clearer to us what the outcome will be on the S&P (stronger USD, lower S&P), on yields, I listen to the market so I wouldn't try be a hero here and stick to an inflation scare just because it's the most obvious scenario.

We'd rather play it through currency exposure, maybe get some optionality on a weaker S&P 500.

That's more at the global level.

We are also very attentive at the way leadership has shifted recently and I'm not talking exclusively about Mag-7s, they've underperformed in recent weeks, but all things US have underperformed, the Trump rally has completely evaporated, small caps, US banks, etc.

I was looking at my screen last week and the shocking thing I saw, Europe and Mexico are up 10% YTD, China/ Hong Kong is up 15% and Nasdaq is basically flattish YTD.

The leadership change of US vs rest of the world is something we need to be very attentive to because we benefited from US tech exposure last year and have to be agile if leadership is changing.

Vincent stressed that they need to be as open minded as possible on how the market wants to interpret what is going on and for him it feels like the Trump tariff chaos is now resonating more on the US than the rest of the world.

I agree and I am looking at the unwinding of momentum in the market and how it is hitting Mag-7 and other tech stocks more broadly as the bond market hints that it's increasingly worried about a hard landing in the US.

I moved back to Real Estate and asked him if better days lie ahead and he said "absolutely and Charles mentioned it this morning, we need this portfolio and the execution to get better."

He added:

It's slower to pivot that portfolio mainly because of where the geographical choices were made five to ten years ago but also many of these assets were there from an operational premise rather than an investment premise. Even though Rana inherited a challenge, I'm optimistic that she'll n=be able to get us to better days of outperformance.

We've seen it done in Private Equity and Infrastructure internally and she just got there a few months ago and they are moving to shift the focus to investing rather than being an operator.

Laslty, we didn't speak about Infrastructure but it had another solid year and I asked Vincent if the India bribing scandal is now behind them, meaning they are not part of some ongoing SEC investigation and they cleaned up shop in India.

Kate Monfette stepped in to say the SEC investigation is still ongoing for the three former execs but CDPQ is not part of any ongoing investigation as far as she knows and she agreed with me, there was a cleanup in India at the executive levels.

Alright, it's late, very late, let me wrap it up there and once again thank Vincent for another insightful discussion and thank Kate as well (can tell she was a bit hesitant to discuss India and trust me, I don't want to ever talk about that scandal again, it irritates me more than you can possibly imagine).

I am ending on a sad note, CDPQ put out this statement on LinkedIn announcing their former CEO, Jean Campeau, has passed away:

Mr. Campeau was well respected and admired by many in the private and public sector.

He was also the father-in-law of Gordon Fyfe, BCI's CEO and CIO. I extend my condolences to his wife and family during this difficult time.

Below, an interview in French with CDPQ's CEO Charles Emond going over their results and more.

Click here to watch it, I will see if they make it available on YouTube tomorrow so I can embed it.

And Marathon Asset Management CEO, chairman, and co-founder Bruce Richards joins CNBC's 'Closing Bell' to discuss market outlooks.

I also embedded a wonderful panel discussion paying tribute to Jean Campeau (in French) that took place earlier today.

Comments

Post a Comment