Freschia Gonzales of Benefits and Pensions Monitor reports a winning portfolio can still look like a loser, CPP Investments warns:

CPP Investments argues that beating a benchmark no longer measures whether a portfolio is working.

Its

modelling shows a diversified pension fund can trail its market

benchmark almost 30 percent of the time over a decade, even when its

underlying strategy genuinely adds value.

That

figure comes from a July 2026 paper from the CPP Investments Insights

Institute, the second in a series on the total portfolio approach

(TPA).

In

a stylized illustration, the authors modelled two portfolios carrying

the same total risk: a strategic asset allocation (SAA) portfolio highly

correlated with its benchmark, and a TPA portfolio built to diversify away from it.

Even

with a higher expected value-add of 100 basis points, the diversified

portfolio showed a 29.8 percent chance of underperforming its benchmark

over 10 years, the report said, compared with 6.5 percent for the more

benchmark-hugging design.

These are false negatives, cases where a sound portfolio looks like it failed.

The paper frames the problem as one of accountability outgrowing its measuring stick.

Under

traditional SAA, the report explained, a board sets a

policy portfolio and management is judged on whether it beats that

benchmark.

Under TPA, management instead owns a broader set of interconnected choices, including how much risk to take, how to diversify, how to balance liquidity, and how to implement, and all of those decisions fall within the scope of performance assessment.

CPP Investments set out three reasons a single benchmark falls short.

First, the authors noted, short-term outperformance or underperformance often reflects luck rather than skill, a problem amplified when a portfolio is intentionally built to differ from its index.

Second,

benchmarks drift: as market concentration rises,

capitalization-weighted indices can take on exposures managers never

intended to hold.

The

report pointed to research by Sorensen, Alonso and Belanger describing

this as a benchmark's "chameleon" nature, which it said can reward

concentration when concentration is winning and penalize diversification held for long-term resilience.

Third,

as portfolios add private assets, illiquidity premia and long-duration

cash flows, comparisons to public-market indices become, in the report's

words, "apples-to-oranges."

Over the past few years, the upper deciles of feasible portfolio returns have been dominated by heavy exposure to US tech mega-cap listed equities, according to the paper, leaving diversified designs in the lower portions of the distribution.

That

does not mean diversification failed, the authors argued, but rather

that portfolios built for many environments will lag concentrated,

equity-heavy portfolios in a market that rewards listed equities far

beyond expectations.

For plan sponsors weighing whether a differentiated strategy is paying off, the report offered CPP's own sustainability record as evidence on its risk-setting decision.

Investment

performance is estimated to have cut the base CPP minimum contribution

rate from 9.54 percent in the 31st actuarial report to roughly 9.19

percent, a fourth consecutive triennial decline.

Measured

from 2012, the rate has fallen from 9.84 percent despite adverse

demographic surprises that would normally push it higher.

The

Spring Economic Update 2026 proposed reducing the legislated base

statutory contribution rate from 9.9 percent to 9.5 percent starting in

2027, the report noted, citing the improved funding position.

CPP Investments targets a level of market risk equal to a portfolio of 85 percent global equities and 15 percent Canadian government bonds for the base plan, and 55 percent equities to 45 percent bonds for the additional plan.

Rather

than replace benchmarks, the report positioned them as a diagnostic

input within a six-part framework spanning total return outcomes, risk

and capital allocation, portfolio construction and diversification,

investment selection, decision quality and process, and resilience

across market regimes.

Benchmark

outperformance does not always deliver institutional aims, the authors

wrote, since a strategy can beat its index simply by adding concentration or exposures already held elsewhere.

The

challenge reaches beyond pension investing, CPP Investments said, as

more organizations manage portfolios against multiple long-horizon goals

such as inflation protection and sustainability.

For

boards, the paper's takeaways were to align evaluation with delegated

decision rights, connect outcomes to objectives, and treat benchmarks as

one part of an overall assessment.

The

question, the authors concluded, is no longer whether a portfolio beat

its benchmark but whether every management decision improved the

delivery of long-term goals.

The paper was

written by Sally Shen, manager at the Insights Institute; Derek Walker,

managing director of total fund transformation initiatives; and

Geoffrey Rubin, senior managing director and one fund strategist.

Sally Shen, Derek Walker, and Geoffrey Rubin of CPP Investments wrote a second report entitled Measuring What Matters: Evaluating the Total Portfolio Approach:

For

decades, institutional investors operated in a relatively stable world.

Inflation was subdued, globalization deepened, and public markets

expanded. In this environment, traditional Strategic Asset Allocation

(SAA) frameworks offered a practical way to organize and measure

investment decisions: establish a “policy portfolio”, measure total-fund

returns against it, and assess active managers relative to their

benchmarks.

That world is changing.

Economic fragmentation, heightened geopolitical uncertainty and a

growing need for resilience across a wider range of market conditions

have led many investors to adopt variants of the Total Portfolio

Approach (TPA). As we explored in a previous report, TPA offers greater

flexibility to construct portfolios around long-term objectives by

managing risk, diversification, liquidity, and capital allocation at the

total-fund level rather than within asset-class silos.

Yet increasingly, the way portfolios are managed under TPA no longer

aligns neatly with how performance has traditionally been measured.

Under TPA, management becomes accountable for a much broader set of

interconnected decisions: how much risk to take, how to diversify

exposures, how to balance liquidity and illiquidity, and how to

implement those choices efficiently over time.

This leaves a fundamental question: how should realized performance

be evaluated when the portfolio itself is increasingly dynamic,

differentiated, and intentionally designed around multiple objectives?

This question is especially important for pension funds that are

accountable for delivering outcomes over decades—for CPP Investments,

over a 75-year actuarial horizon—while providing full transparency and

appropriate scrutiny.

Benchmark comparisons remain essential to evaluating active

management decisions and maintaining accountability. But under TPA they

are no longer sufficient on their own. Measuring the health of a total

portfolio requires a broader, multi-faceted framework capable of

assessing not only returns, but also the total portfolio’s resilience to

adverse market and economic circumstances, the impacts of

diversification, concentration and tactical decisions, the effectiveness

of implementation, and alignment with long-term objectives. This report

examines how CPP Investments is developing its approach.

The Limits of Benchmarks in TPA Performance Assessment

For all the enthusiasm around TPA, its credibility ultimately rests on a simple question: has it worked? Indeed, if institutions cannot assess whether an approach has worked in the past, it is difficult to maintain conviction that it will work in the future.

Traditional SAA frameworks split the overall investment decision into

two parts. First, the portfolio owner or board—often with the

assistance of a third-party consultant—chooses a policy portfolio of

asset classes and weights, with the returns forming the benchmark.

Management is then tasked with outperforming that benchmark. This

approach provides a straightforward view of management performance:

value added relative to a low-cost, investable benchmark.

However, one of the most important decisions—the choice of the policy

portfolio itself—typically escapes ongoing evaluation. This decision is

stored in the figurative “attic” while performance assessment is

focused solely on management’s deviations from the policy and active

management benchmark portfolios, rather than the policy portfolio’s

suitability for achieving the institution’s objectives (Figure 1).

TPA changes this accountability structure. Management becomes

accountable not only for active decisions relative to a benchmark, but

for the entire portfolio—from risk choices through targeting of total

portfolio exposures, to implementation. All portfolio decisions fall

within the scope of performance assessment and must be evaluated based

on how well they advanced institutional objectives. This broader

accountability requires tools that extend beyond the single benchmark

framework typically employed by SAA.

There are good reasons why benchmarks are deeply embedded in

institutional investing. First, they constitute simple, unambiguous

instructions from principal to agent. Coupled with an active risk limit

and a capital allocation, the managing agent understands that their task

is to beat the benchmark. And this same benchmark can be used for ex

post performance evaluation and incentive compensation, unifying both

measurement and management in a single, simple device.

Unfortunately, these features are insufficient for effective performance information and management under TPA.

Issue 1: Noisy Signals

Even genuinely value-additive investment strategies can

underperform a benchmark due to randomness—sometimes for extended

periods. While this challenge exists under traditional SAA frameworks,

it is more pronounced under TPA, where portfolios may intentionally

differ from conventional benchmarks in pursuit of diversification,

resilience or dynamic positioning.

Barras, Scaillet, and Wermers (2010) show that benchmark-relative

outperformance and underperformance often reflect luck over shorter

horizons. Barras, Beath, and Betermier (2026) further highlight how

noise accumulates along the total portfolio value chain, increasing the

likelihood that value-adding diversification decisions appear

unsuccessful over finite horizons.

Figure 2 illustrates this challenge. Because TPA portfolios

intentionally depart from conventional benchmarks, short-term

benchmark-relative underperformance remains plausible even when

portfolio decisions are sound and expected long-term outperformance is

intact. In short, performance relative to a benchmark provides important

evidence, but rarely a complete assessment of whether the total

portfolio is succeeding.

This figure provides a stylized illustration of benchmark

underperformance across evaluation horizons. The ellipses represent the

one-standard-deviation confidence region of 5-year outcomes for the

“SAA” and “TPA” portfolios with the same total risk target. The dot

within the ellipse represents the expected outcome.

The “SAA” portfolio in the left-hand panel is assumed to have a

value-added expectation of 90 bps (the vertical distance or “alpha” to

the diagonal line), delivered with relatively narrow error bands due to

its lower tracking error versus the benchmark. The “TPA” portfolio in

the right-hand panel is assumed to have a value-added expectation of 100

bps, but larger error bands due to substantially lower correlation of

its returns with the benchmark, arising from differentiated portfolio

construction and diversification decisions. The shaded area below the

diagonal line represents benchmark underperformance despite positive

true alpha (“false negatives”).

Over a single year, both the “SAA” and “TPA” portfolios show

significant incidence of underperformance to the benchmark (see the

table below Figure 2). At five- and 10-year horizons, the compression of

the “SAA” error bands makes false negatives increasingly unlikely. By

contrast, while the “TPA” error bands also compress over time, realized

benchmark underperformance remains plausible even at longer horizons

despite higher alpha expectations, as false-negative probabilities

remain elevated. Importantly, Figure 2 is not intended to suggest that

either the SAA portfolio or the TPA portfolio is inherently superior.

Rather, it illustrates a measurement challenge that arises when

portfolios are intentionally diversified away from a single benchmark.

Issue 2: Benchmarks That Do Not Reflect Intended Portfolio Design

A second challenge is that benchmarks can evolve significantly

over time. As market concentrations shift, capitalization-weighted

indices can come to embody risk exposures that differ materially from

those that portfolio managers intentionally seek to maintain. This

matters because TPA practitioners typically aim to diversify away from

concentrations that accumulate in widely used benchmarks.

Sorensen, Alonso, and Belanger (2023) describe this as the

benchmark’s “chameleon” nature: as market concentration rises,

diversification falls, and tight tracking-error constraints can force

managers to hold portfolios that are more concentrated than intended or

prudent.

This creates a distorted incentive problem. Benchmark-relative

evaluation can reward concentration when concentration is winning and

penalize diversification that is being maintained to support long-term

resilience. Over time, this can pull portfolios closer to the

benchmark—even when doing so undermines the broader objective of

diversification and total portfolio resilience.

Issue 3: Apples-to-Oranges Comparisons

As portfolios become more differentiated, comparisons to any

single benchmark become less informative. At CPP Investments, portfolio

outcomes reflect exposures to illiquidity premia, long-duration cash

flows, operational value creation, and other risk factors that are not

fully captured by public market benchmarks. The result: simple public

benchmark-relative performance is an apples-to-oranges comparison that

can mislead as much as it informs.

This limitation is particularly evident in private assets such as

infrastructure, where public benchmarks often fail to capture

contractual cash flows, inflation linkage, and long-term active

management of the portfolio assets. As Shen and Blanc-Brude (2022)

demonstrate, these characteristics are difficult to replicate through

conventional public-market benchmarks. As a result, private assets must

ultimately earn their place in the portfolio relative to public-market

alternatives. However, simple benchmark comparisons may not fully

capture their contribution.

These benchmarking issues, and expanded accountability for the entire

investment problem, make assessment of TPA performance difficult but

not impossible. Ex post performance assessment remains vital to

sustaining confidence and improving decisions over time.

The challenge, then, is assessing performance through multiple lenses rather than via a single verdict.

Moving Beyond Benchmarks

Ex post performance assessment under TPA begins with a clear

statement of institutional objectives. For some organizations, the

primary objective is pension plan sustainability (e.g., funded status or

contribution rate stability); for others, objectives may include

liquidity preservation, inflation protection, intergenerational

risk-sharing, or climate and other broad policy considerations. A

credible ex post assessment must evaluate success against each of those

ex ante objectives while also considering whether the decisions that

produced the outcomes were sound given the information and alternatives

available at the time.

CPP Investments’ objectives are grounded in the Canada Pension Plan Investment Board Act1:

To invest CPP assets with a view to achieving a maximum rate of

return, without undue risk of loss, having regard to the factors that

may affect the funding of the Canada Pension Plan;

To manage the fund in the best interests of CPP contributors and beneficiaries;

To assist the CPP in meeting its obligations to contributors and beneficiaries.

While these objectives are clear, they are multi-purpose and

multi-horizon. They must be translated into a more complete set of aims

that define risk appetite, outcome horizons, and the desired level of

portfolio resilience through market and economic cycles. Clarifying and

balancing those aims, and the constraints within which they must be

pursued, is a prerequisite for assessing TPA performance.

TPA performance is best understood by examining the many decisions

that collectively produce total portfolio outcomes. Decomposing

performance into its component decisions does not diminish management’s

accountability for overall results, but it does provide useful evidence

on the performance of each major link in the chain. Traditional

benchmark-based frameworks assess only parts of the investment

problem—typically the active components relative to benchmarks—while

disregarding the rest.

In practice, CPP Investments undertakes many investment decisions in

pursuit of its objectives. For the purposes of this report, we are

focusing on three that have an outsized influence on long-term

outcomes—risk level, exposure targeting, and investment selection.

Together, these decisions shape portfolio design, realized returns, and

delivery against objectives, though in different proportions (Figure 3).2

Here, we discuss each of these decisions and the approach to

understanding their performance, noting that this approach can be

extended to a wider range of decisions and institutional aims.

Decision 1: Risk Targeting: Did the chosen level of market risk optimize plan adjustment risk?

The first major TPA decision at CPP Investments is the level of

market risk the Fund should target. CPP Investments establishes a level

of market risk that optimizes the combination of positive and adverse

adjustments to the CPP that might arise from our realized investment

performance.

Lower-risk portfolios reduce short-term investment return volatility

but may deliver insufficient long-term returns to support CPP

sustainability. Higher-risk portfolios increase expected returns but

also increase the likelihood of adverse outcomes in the short-term. Risk

targeting therefore reflects a trade-off between short-term volatility

and long-term plan sustainability.

CPP Investments manages this trade-off by targeting a level of market

risk that best balances positive and adverse potential plan adjustments

over time. In this model, adverse outcomes carry more weight than

positive outcomes and nearer term outcomes carry more weight than

distant ones. For the base CPP, this work establishes a target level of

market risk equal to that of a portfolio comprised of 85% global

equities and 15% Canadian government bonds; and for the additional CPP

an equity-debt risk equivalence of 55% global equities and 45% Canadian

government bonds.3These levels of market risk generate

expected returns that exceed the minimum level required for CPP

sustainability, reducing the likelihood of adverse plan adjustments and

improving the likelihood of positive adjustments over time.

Has this decision worked? Figure 4 illustrates how these returns have

impacted base CPP sustainability and contributed to sustained

reductions in the Minimum Contribution Rate (MCR).4Most

recently, investment performance is estimated to have reduced the MCR

from 9.54% in the 31st OCA Actuarial Report (2021) to approximately

9.19%,5 marking the fourth consecutive triennial decline. The

Spring Economic Update 2026 proposed reducing the legislated base CPP

Statutory Contribution Rate from 9.9% to 9.5%, beginning in 2027,

reflecting the improved sustainability position of the CPP following the

latest triennial review.6

Decision 2: Exposure Targeting: Did portfolio design improve the investment outcome?

Portfolio design is the second major TPA decision at CPP

Investments. It includes choices related to diversification, leverage,

geography, currency, sector, and other systematic risks, while

maintaining the total risk established through risk targeting. There are

many ways to design a portfolio at the same overall risk level; CPP

Investments’ objective is to identify the portfolio most likely to

deliver objectives across a wide range of future states, rather than

maximize performance for any single objective or in any single market

environment.

Under TPA, there is no natural “default” portfolio. A benchmark,

whether a simple blend of 85% global large- and mid-cap equities and 15%

Canadian government bonds, an equal-weight index, or something more

customized, is only one feasible design among many. Portfolio design

should therefore be evaluated against a broad collection of feasible

alternatives that achieve the same risk target through different

portfolio construction approaches, resulting in materially different

exposures and trade-offs, not a single comparator.

In a sense, SAA is like a prize fight pitting the chosen portfolio

design against a single competitor, the benchmark. Management can study

this lone competitor at length, hugging or replicating the benchmark

where they possess no edge and separating and fighting where they sense

advantage. In this contest, the delivery of institutional aims is

subordinated to a singular focus on benchmark outperformance. TPA places

the chosen portfolio design in combat with all comers, aiming

to outperform all feasible alternatives in the service of institutional

aims. A more challenging prospect, for sure, but all possibilities are

equally relevant, and realized performance should be assessed against

each of these foregone alternatives.

Figure 5 illustrates CPP Investments’ approach to understanding the

performance of portfolio design. At the outset of any measurement

period, we identify a vast range of portfolios that share the targeted

level of market risk and conform to institutional constraints. These

alternatives differ by factor exposure, public and private composition,

diversification, leverage, liquidity, currency, geography and sector.

Each represents a viable design choice and will have delivered a

distinct realized return over the period. We consider many thousands of

foregone portfolio alternatives and calculate the realized returns of

each over the observation period, arraying these returns in the

distribution shown in Figure 5. The realized returns of our actual

chosen portfolio design are also included.

While TPA aims to find the single best portfolio from among the

multitude, there will always be some portfolios that outperform our

choice in any fixed observation period. In fact, the “winning” portfolio

design in any short time frame is typically suited only for the

environment that transpired, rather than the range of possible

environments that might unfold over time. The best long-horizon

portfolio design is one that maintains a position in the upper quintiles

of this distribution through many market cycles and under different

market conditions.

Over the past few years, the upper deciles of this realized return

distribution are dominated by portfolios with heavy exposure to U.S.

tech mega-cap listed equities. Given the extreme dominance of U.S.

public equities’ returns, particularly in a few industries, diversified

portfolio designs delivered returns in the lower portions of the

distribution, with private-asset heavy portfolios tending to be further

to the left. This does not necessarily imply that diversification

failed. Rather, it demonstrates that portfolios designed for many

environments will underperform concentrated equity-centric portfolios in

environments that deliver listed equity returns far in excess of

expectations.

This technique rigorously assesses the portfolio design choice

without reverting to comparisons with a single benchmark. The

positioning of realized returns within the distribution of all viable

alternatives provides critical evidence on the success of the TPA

exposure targeting choice in supporting institutional aims.

Decision 3: Investment Selection: Separating Skill-Based Value Added from Market-Driven Returns

Investment selection is the third TPA decision evaluated at CPP

Investments. It relies more heavily on benchmark comparisons. CPP

Investments compares the realized investment performance of each

investment strategy to a benchmark comprised of public market indices

with similar systematic risk exposures. Results are then aggregated to

the department level, helping distinguish skill-based value added from

the beta-driven returns generated by broader portfolio design decisions.

The aggregation of these benchmarks provides an overall “Benchmark

Portfolio” for the base and alternative CPP, providing a view of the

collective impact of investment decisions. While management remains

accountable for total portfolio outcomes; these benchmark comparisons

help assess the contributions of individual strategies and departments.

For private assets, it is critical to distinguish between two separate

sources of value added: the strategic decision to invest through private

rather than public markets, and the investment skill demonstrated

relative to an appropriate private-market benchmark.7

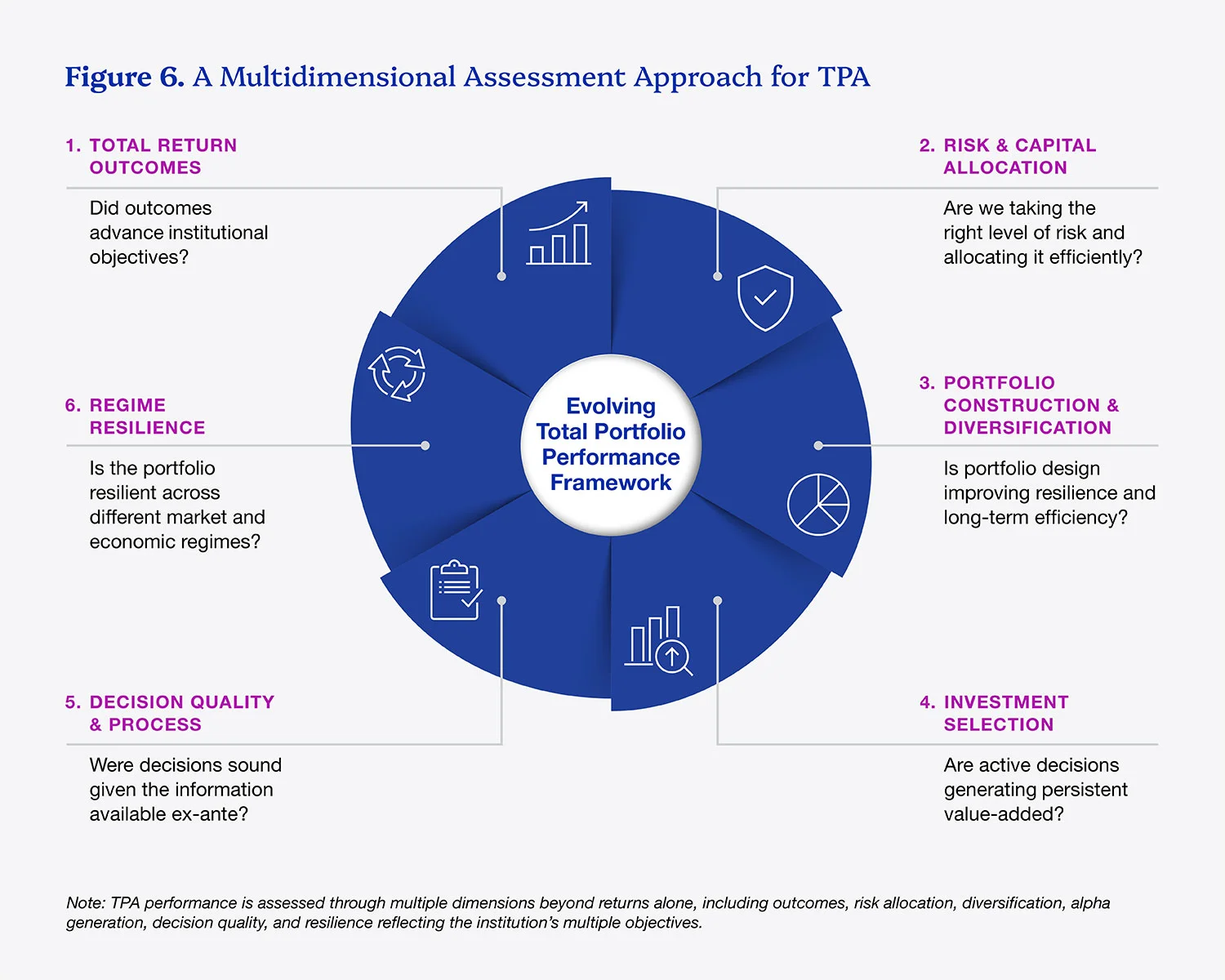

Toward a Multidimensional Assessment of TPA Performance

Under a traditional SAA framework, the benchmark often acts as

the objective, the instruction set, and the scorecard. Under TPA,

management is accountable for a broader set of decisions that require

multiple lenses. Performance assessment must go beyond absolute and

relative returns and consider risk-setting, diversification, resilience,

risk and capital allocation, portfolio construction, implementation

skill and decision quality (Figure 6). An assessment must also consider

whether governance processes are functioning effectively and whether the

portfolio remains aligned with long-term objectives.

CPP Investments assembles the pieces of performance assessment that

provide a more complete picture of whether and how TPA is improving

long-term outcomes. Different metrics answer different questions.

Reference portfolio comparisons help assess broad design choices, global

market portfolios provide context on opportunity cost, unlevered

portfolios isolate the impact of leverage, and peer comparisons offer an

external perspective.

Benchmark outperformance is an important part of this balanced view.

At the investment strategy level, benchmarks help distinguish alpha from

beta returns and assess implementation skill, and at the total

portfolio level they help explain aggregate implementation outcomes.

Under TPA, benchmarks are a diagnostic input into performance evaluation

rather than the sole measure of success. This distinction matters

because benchmark outperformance does not always deliver institutional

aims. A single strategy can outperform its benchmark by increasing

concentration or adding exposures already held elsewhere in the

portfolio. Conversely, the total portfolio may intentionally accept

benchmark-relative headwinds if doing so improves diversification,

resilience or alignment with long-term goals.

Conclusion

Performance assessment is difficult under a Total Portfolio

Approach—not because performance is less measurable, but because the

scope of accountability is broader.

A credible ex post assessment framework should be linked to

institutional aims and employ multiple lenses, including risk targeting,

diversification, portfolio construction, investment selection and

long-term sustainability outcomes. Benchmarks remain essential tools

for attribution, discipline and accountability, but under TPA they

become diagnostic inputs rather than singular verdicts on success or

failure.

This challenge extends beyond pension investing. As organizations

increasingly manage portfolios against multiple long-horizon

objectives—including environmental sustainability, development,

inflation protection, or social objectives—performance assessment cannot

be meaningfully reduced to a single benchmark-relative outcome.

For boards and portfolio owners, the key takeaways are to:

align evaluation with the delegated decision rights;

connect outcomes to objectives; and

use benchmarks as part of an overall assessment rather than as the sole measure of success.

The question is no longer simply whether a portfolio outperformed a

benchmark, but whether all management decisions, including portfolio

design and execution, improved the delivery of long-term institutional

goals.

This is another excellent report on CPP Investments' total portfolio approach (TPA) that will surely stir conversations at the Maple 8 and beyond.

Make sure you read their first report, Investing in Uncertain Times: Achieving Disciplined Flexibility in the Total Portfolio Approach, which is available here. I covered it here.

Sally Shen, Derek Walker, and Geoffrey Rubin are very smart, no doubt about it, and they really do a great job distinguishing between the strategic asset allocation (SAA) framework and the total portfolio approach (TPA) and how the latter broadens diversification in a more meaningful way, and better aligns outcomes with objectives.

The big problem with TPA -- and they allude to this -- is that it's much harder to measure its success relative to the more straightforward benchmark comparison in SAA, which is used to evaluate active management decisions:

Benchmark comparisons remain essential to evaluating active

management decisions and maintaining accountability. But under TPA they

are no longer sufficient on their own.Measuring the health of a total

portfolio requires a broader, multi-faceted framework capable of

assessing not only returns, but also the total portfolio’s resilience to

adverse market and economic circumstances, the impacts of

diversification, concentration and tactical decisions, the effectiveness

of implementation, and alignment with long-term objectives. This report

examines how CPP Investments is developing its approach.

Now, let's stop to ponder this for a second.

Critics will claim this is all rubbish. If CPP Investments cannot beat a low-cost index portfolio over a one, three, or five-year period, then why are we paying their employees big bucks to actively manage our pension assets?

For them, these discussions on TPA are nothing more than a theoretical exercise in obfuscation: "Benchmarks don't work any longer because concentration risk in equities is too high; trust our TPA approach is much more sophisticated and resilient than the traditional SAA approach."

For critics, it's simple: if you can't beat a low-cost ETF over a 5-year period, then there is no point in actively managing pension assets, even if you're delivering decent returns above the actuarial target.

And to be sure, the State Street SPDR S&P 500 ETF Trust (SPY) is up 73% over the last 5 years, led by the VanEck Semiconductor ETF (SMH), which is up 373% over that period.

In other words, five years ago, we could have closed down CPP Investments and all the other Maple 8 funds and shoved all the pension assets into the SPY, generating eye-watering returns, and saving hundreds of millions in fees to external managers and hefty compensation to the employees of these large Canadian pension funds (especially their senior managers).

Even if you put 85% or 70% of the assets in SPY or MSCI ACWI and the rest in a Canadian, US or a global aggregate bond ETF, you'd come out way ahead in terms of returns.

This is all true, but it's missing an important consideration: the risk of having such a high allocation to US or global equities when the concentration risk remains at a very high level.

Still, critics will snap back: "So what, concentration risk is fine as long as the bubble keeps inflating, and nobody knows when it will pop. It could last years"

Here is where we need to pause and ask: "Will US equities over the next 5 years produce anything close to what they produced in the last 5 years?"

And I say US because US equities dominate global equity indexes.

My answer is that it's highly unlikely that US equities come anywhere close to producing the same return over the next 5 years, and I also fear bonds will severely underperform if stagflation develops.

So, if public equities will not provide the requisite return, and neither do bonds, pension funds are left with alternative assets like infrastructure, real estate, private equity and private debt.

This is where a total portfolio approach (TPA) differs from strategic asset allocation (SAA), as it directly links an outcome (attaining a return above the actuarial rate-of-return over the long run) to the objective of the pension fund, ie. maximizing returns without undue risk of loss, with regard to the funded status of the plan.

TPA also does a better job linking pension assets with their long-dated liabilities in a more comprehensive way.

CPP Investments is managing over $800 billion in assets, you definitely don't want them to be all in equities and they are large enough to take on illiquidity risk in assets that offer more stable, inflation-protected returns.

Moreover, the diversity of the portfolio, whether it's geographic, sector or by asset class and strategy, makes the Fund more resilient to downside risks over the long run.

That is the point CEO John Graham was driving at when he recently penned a comment on why protecting the CPP means taking the long view on investment returns.

If these highly-paid, smart folks at CPP Investments can't beat their own benchmarks, why are we paying them for?

In fact, the same argument can be expanded to all the Maple 8 funds since they all underperformed their benchmark over the last three years as concentration risk in US equities has risen to historic highs.

Part of the answer is you're paying them to deliver consistent returns over their actuarial target (for most it's around 6%) over the long run, and you absolutely want them to minimize their drawdown to avoid another 2008 fiasco, where most pension funds were down 20% to 40%.

Critics will still come at you: "Who cares if stocks decline 40%, they always bounce back big."

Well, not always. Sometimes stocks keep going down for years, and it can take decades to come back to a previous peak.

This is where the real value of adopting a total portfolio approach is critical for pension funds, because when the music stops and things start heading south, you want your pension fund to sustain that hit as best as possible (they will lose money but nowhere near as much as a pure equity fund).

Moreover, sophisticated pension funds like CPP Investments manage their liquidity well, so they will be able to pounce on opportunities when market dislocations occur.

"Ok, Leo, that's all fine and dandy, but how are we supposed to measure the success of TPA properly? It's not as straightforward as SAA."

Correct, it isn't easy, and nor am I suggesting it's easy to measure the success of TPA, but the easiest way is to link it to outcomes.

Are you getting the outcome you're desiring over the long run with a diverse TPA approach?

If so, then that is really all that matters.

Is TPA perfect? Hell no! There are still a lot of issues to contend and lots of uncertainty.

For example, what if there is a structural change in private equity? How does TPA account for this structural risk properly? The same applies to other illiquid asset classes and private debt.

How does TPA account for all risks? For example, CPP Investments is underweight tech shares in global stock markets but overweight data centres in illiquid asset classes.

Is that a disconnect or an appropriate risk to take?

And benchmarks remain important, but they are far from perfect and should be comprehensively reviewed every three or five years, and changed like BCI did last fiscal year? (to introduce more sector-neutral indexes or equal-weight indexes)

Any changes to benchmarks must be clearly stated in the annual report with a full discussion and analysis.

Equally important: What is the opportunity cost of adopting a TPA framework over an SAA framework?

In the last five years, it's been huge, but was this always the case?

CPP Investments and other large pension funds espousing a TPA approach need to provide numbers and hard facts to back up their case for TPA, not just conjecture and "trust us, we know best."

If not, the critics will always lurk in the background, claiming they are bloated pension funds that keep underperforming their benchmarks while they dole out huge compensation to senior managers.

This is an important discussion and I am only scratching the surface.

I'd need to interview Sally Shen, Derek Walker, and Geoffrey Rubin to really get into it properly with them but they have done a fantastic job highlighting the important issues and why TPA is a better framework than SAA for pension funds.

Below, CPP Investments' CEO John Graham joins Nicolai Tangen, CEO of Norges Bank Investment Management, for a great discussion in his In Good Company podcast.

Take the time to listen to this podcast, John goes over many important points on their total portfolio approach, and Nicolai does another masterful job of asking all the right questions.

Comments

Post a Comment