Are Public Sector Pensions Too Generous?

Polly Curtis of the Guardian reports, Are public sector pensions too generous?:

Polly Curtis of the Guardian reports, Are public sector pensions too generous?:Unfortunately, a race to the bottom seems to be the where we're heading in terms of global pension reform. Go back to read my comment on Ontario Teachers' CEO offering a dose of reality.Public state employees including police, lecturers and border control staff are striking today over government plans to shave billions from the the pensions bill by worsening the terms of their pensions.

The minister Francis Maude says the deal is done and striking is futile and some unions agree. Only five of the 30 unions that took part in last November's national strike are walking out today. But Mark Serwotka, the general secretary of the PCS union of civil servants, said that "the tide has turned" and renewed action showed that the trade union movement was not giving up.

The government's argument is apparently supported by reports in the press today of research by the Intergenerational Foundation, which campaigns for fairness for all generations. The press release, available here, highlights the 78,000 retired state employees who currently receive a pension in excess of £25,900, the average UK earnings according to the 2010 annual survey of hours and earnings from the ONS.

This report gave rise to several newspaper articles including:

• The Daily Mail, which describes the report as "shocking"

• The Telegraph which describes the reports findings as "pensions apartheid"

• And Channel 4 news, which highlights that the typical private sector worker retires on a pension of £3,700 a year, compared to £7,000 in the public sector.

The central argument of the Intergenerational Foundation report is that the country is facing a £1.2 trillion pound liability for pensions – equivalent of £45,000 per household – which is unaffordable for younger generations struggling with high housing costs, unemployment and students debts, to pay for.

Angus Hanton, co-founder of the Foundation, said:

This is not a matter of part politics but a matter of rising longevity, a demographic bulge and successive government's' continued assurances that public sector pensions are affordable, realistic and sustainable... Younger generations are facing unemployment of more than 1m, having to pay through the nose for their education and have little hope of affording homes of their own, yet somehow they will be expected to find £45,000 per household to fund these unaffordable pensions.

Ed Howker, also co-founder of the Foundation, added:

This paper shows that the pension prospects of public and private sector workers are out of whack, and that future taxpayers face the difficult prospect of paying large public sector pension bills of a size and scale which is much larger than they are likely to receive themselves.

The question of whether public sector pensions are affordable are at the heart of the row and Reality check has previously looked at that issue here concluding that it is simply a question of whether the government wants to prioritise public sector pensions or not. This government has decided not to.

But are public sector pensions too generous? I'm going to look into the figures contained in the Intergenerational Foundation research further to see what they really tell us.

Analysis

This is from the report:

The average public sector pension of £7,000 is equivalent in cost to a private sector worker having accumulated a personal pension fund worth £140,000 by the time he or she retires. To achieve an annual pension close to the national minimum wage of £12,646 they would need £250,000 saved, and for the average annual salary of £25,900 they would need a pension pot of £518,000.

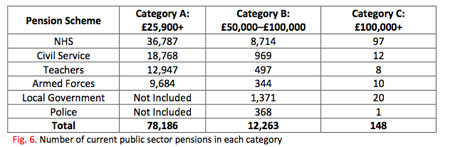

IF used a combination of Freedom of Information requests to government departments and a Parliamentary question in the House of Commons to find the following figures.

• Number of public sector retirees collecting in excess of £25,000 annual pension: 78,186

• Number of public sector retirees collecting in excess of £50,000 annual pension: 12,263

• Number of public sector retirees collecting in excess of £100,000 annual pension: 148Of those collecting over £50,000, doctors dominate with 8,714 (72%) irrespective of private practice work undertaken.

I wanted to put these figures in context. The Treasury this morning told me that 4m people currently receive public sector pensions. (Another 5.5m are "active members" meaning they are working and contributing to the scheme and 3m are "deferred members" who have left the scheme but will still benefit from it when they retire.)

So the 78,186 public sector retirees who receive more than the national average salary in their pension constitutes 1.95% of all public sector retirees.

The 12,263 people who receive more than £50,000 are 0.3% of the total and the 148 who receive more than £100,000 is 0.003% of the total.

The average public sector pension is £7,000 – nearly double the £3,700 in the private sector. It's right to have a debate about whether that's fair and whether the country can afford to pay such pensions. But I don't think it's fair to use a tiny minority of the total recipients pensions who receive the higher amounts to argue against the current public sector pension schemes in general.

I'm going to look for a more detailed breakdown of the amounts public sector retirees receive in pension and report back. The Intergenerational Foundation has just called to say there is far more detail on their figures in the full report, which isn't currently available on their website. I'll look at that shortly too. Do you have any evidence that can help? Get in touch below the line, on Twitter at @pollycurtis or email me at polly.curtis@guardian.co.uk.

This is the full report [pdf] from the Intergenerational Foundation. It contains the following table showing the FOI responses from each of the public sector schemes.

Intergenerational Foundation pensionsI've just been speaking with Liz Emerson, the press office for the Foundation who has clarified that the 78,900 figure for the number of state retirees receiving more than the national average salary is not complete because it doesn't include local government, police or fire-fighters. These schemes are not centrally funded so the figure was too difficult to obtain. That figure is therefore likely to be higher.

She said:

We are saying there is a part of the public sector who are doing very well thank you very much. Maybe the poorer public sector workers need to get more in their pensions? The middle class section needs to understand that paying 6-7% and getting over 40% back is not sustainable in an unfunded system.

I have found some fuller audited statistics for some of the schemes, which previously featured in this blog here. The following three tables from this National Audit Office report on public sector pensions, which shows how much people received from three of those schemes.

Appendix 4b

Appendix 4c

Appendix 4dThese also show that actually relatively very few public sector workers retire on particularly large pensions.

Several people have asked me for comparable figures for the private sector and I'm looking for those. If anyone knows of some do get in touch. Below the line and via email there is some support for one of the principle ideas in the report, that the gap between public and private sector pensions are unfair.

@Existangst writes:

The average public sector pension is £7,000 – nearly double the £3,700 in the private sector.

That says it all. £7000 is not a lot of money, but a damn site more than the £3500 my father gets, having worked for 45 years in the private sector and paid into their pension scheme for all of those years.

However, several people also argue that you can't compare public and private sector jobs in a straight forward way because they are fundamentally different in nature.

Kay emailed in:

Comparing average pensions also requires comparing like with like. Since the 1980s, the public services have been steadily outsourcing the less skilled jobs. One would expect a cleaner to have a lower pension than a graduate teacher, nurse or civil engineer; if one sector has a higher proportion of cleaners and the other a higher sector of graduate jobs, one would expect a difference in average pension. Breakdown of current jobs in public and private sector (which is available somewhere since it's come into arguments about relative pay) would give some handle on this if breakdown of ex-employment of retirees is not available.

@Rich2012 writes below the line:

The key point is that you can't easily compare public and private sector jobs. Public sector jobs are overwhelmingly higher skilled and staffed by graduates. As another poster said lower paid jobs have been systematically privatised and outsourced to the private sector. It is obvious that on average such public sector jobs will get better pensions than a total national average because the comparison is not like with like.

A much fairer comparison would be to look at the relative pensions of public and private sector doctors or a local authority accountant or solicitor vs private sector. The difference would be much less and when considered with the pay differential between public\private for these skilled jobs makes much more sense. Irrespective of this do we really want to make woefully inadequate private sector pension provision 'fair' by a race to the bottom?

In his speech at Hamilton, Jim Leech commented on the futility of the "pension envy" debate between those who have defined-benefit (DB) pensions versus those relying on defined contribution (DC) pension plans:

Let me return for a moment to the DB-DC debate and sound a word of caution: We must not allow “pension envy” to define that debate.After my last comment on Canada's secret pension plan, I received this insightful comment from a well informed Canadian citizen:

There is a danger that this could happen, however, as the private sector increasingly moves toward Defined Contribution plans - and away from the Defined Benefit model - saying it is unaffordable.

The truth is that DB Plans are far better vehicles for pension saving. I know that this flies in the face of conventional wisdom, but it is true.

A report by the US National Institute on Retirement Security finds that there are four main reasons for this:The social costs that the private sector’s shift to defined contribution plans will impose in the future have not been widely acknowledged. Members of such plans will likely retire with inadequate retirement incomes. Their combined individual defined contribution shortfalls will likely dwarf any potential valuation shortfalls of defined benefit plans, possibly imposing obligations on future governments (read: taxpayers) for further retirement income assistance.

- Individuals in a DC Plan must plan to live a long life – out to the maximum on the actuarial table, as you don’t want to run out of money part way through your retirement! Because individuals can’t pool longevity risk, like DB plans do, they’re forced to accumulate more in their DC plan than would be necessary to fund an equivalent DB plan, which can be based on actuarial averages.

- Because DB plans are ageless, they can perpetually maintain an optimally balanced investment portfolio. Individuals, on the other hand, must downshift dramatically in order to lower their risk/return as they age. Transaction costs of such rebalancing are very high.

- By pooling their savings in a DB Plan, the participants can afford to engage professional investment advisors – something that the average worker with a DC Plan or RRSP cannot afford. When I compare the returns I have realized in my own self-managed RRSP with those of Teachers’, I know I could use some expert advice.

- DC Plans and RRSPs are usually invested in retail products that carry large administrative fees – sometimes as high as 2% per annum. Contrast that with the cost at Teachers’ of only 25 basis points. The extra 1.75% over a working lifetime is a huge cost - amounting to just under 40% of the total funds you could have for your retirement.

Interesting coverage on SPP. Unfortunately, I remember when Saskatchewan actually introduced revolutionary public policy as in Medicare, SGI, Potash Corp., even a provincial bus service when few people had access to individual transportation (no longer in existence and no longer needed) and balanced budgets (Yes, Tommy and his social democratic successors took Sask from an fiscal basket case to one of the most respected governments in the western world and an incubator of top rate public servants – many of whom went on to Ottawa when Ross Thatcher came to power and viciously purged many of them).We'll see what will happen in Alberta and rest of Canada but I'm not impressed with the boneheaded moves our politicians are making, pandering to the banks and insurance companies.

As you note, baring better alternatives such as an Enhanced CPP or well governed DB plans, something like the SPP might make sense.

But we should be far beyond that by now. Sadly, were electing governments whose goal seems to be to destroy vital programs (be they starving CPP of enhancement, ignoring the value of the DB pensions model, or killing environmental protection and oversight) rather than create something that enables ordinary citizens to live comfortably in a relatively stable environment.

Yesterday I came across this piece on the failure of DC plans to “pay a decent pension” in the San Francisco Chronicle. I’ve been looking for some empirical evidence on the performance of DC plans and it is hard to come by. You would think outfits like the EBRI would produce some data on what they actually produce in pension income, but they don’t. However, kudos to Investopedia for publishing this paper and to outfis like Dalbar who reveal average investor returns.

In my opinion, promoting the finance sectors PRPPs, SPP and their ilk is a huge rube which will end up making the finance industry billions in fees but leaving their contributors a life of poverty in retirement.

On the domestic scene, with Redford’s near death experience win in Alberta, I wonder if she might be open to reversing Alberta’s leading the opposition to enhancing the CPP to promoting an enhanced CPP over PRPPs.

My biggest fear is that the great pension slaughter will continue, exacerbating the global disconnect. When people ask me whether public sector pensions are too generous, I reply: "No, except for a small percentage of flagrant pension abuses, by and large public sector pensions provide and adequate but hardly generous income to retire on. In an ideal world, everyone should fight for the same privileges, enabling them to retire in dignity and security."

I'll tell you what's too generous bordering on obscene, the compensation on Wall Street where big banks and elite hedge funds hire the 'best and brightest' to frontrun pensions (using pension contributions!). But the masses are waking up, social media will augur a new revolution against the excesses of the privileged few at the expense of the restless many. And jobs and pensions will be at the heart of this global debate.

Below, watch an absolutely stupid explanation of the UK pension strikes. Notice how the debate is framed between public vs. private and that "private workers need to work longer to sustain public sector workers' pensions". Absolutely silly and ridiculous. This is the sort of nonsense Zero Hedge loves to post. The debate shouldn't be about "pension envy", it should be about how we can improve the pension fortunes of all our citizens, not just those working in the public sector.

Comments

Post a Comment