Prepare For a US Slowdown?

U.S. job growth slowed in May and employment gains in the prior two months were not as strong as previously reported, suggesting the labor market was losing momentum despite the unemployment rate falling to a 16-year low of 4.3 percent.Jeffry Bartash of MarketWatch also reports, U.S. jobs growth slows to 138,000 in May:

Nonfarm payrolls increased 138,000 last month as the manufacturing, government and retail sectors lost jobs, the Labor Department said on Friday. The economy created 66,000 fewer jobs than previously reported in March and April.

May's job gains marked a sharp deceleration from the 181,000 monthly average over the past 12 months. Job growth is slowing as the labor market nears full employment. Last month's job gains could still be sufficient for the Federal Reserve to raise interest rates this month.

"The weak job growth number isn't a disaster because it still keeps up with population growth," said Paul Diggle, senior economist at Aberdeen Asset Management. "Today's numbers probably won't stop the Fed from raising rates this month. But they might well influence what happens next."

The economy needs to create 75,000 to 100,000 jobs per month to keep up with growth in the working-age population.

The unemployment rate fell one-tenth of a percentage point to its lowest level since May 2001. It has dropped five-tenths of a percentage point this year. Last month's decline came as people left the labor force. The survey of households from which the jobless rate is derived also showed a drop in employment.

Economists polled by Reuters had forecast payrolls increasing by 185,000 jobs last month and the unemployment rate holding steady at 4.4 percent. The closely watched employment report was released less than two weeks before the Fed's June 13-14 policy meeting.

U.S. financial markets are almost pricing in a 25 basis point increase in the Fed's benchmark overnight interest rate at that meeting, according to CME FedWatch.

The dollar fell against a basket of currencies on the data, while U.S. government bond prices rose. U.S. stock index futures trimmed gains.

The modest payrolls increase could raise concerns the economy was struggling to gain speed after growth slowed in the first quarter.

Minutes of the Fed's May 2-3 policy meeting, which were published last week, showed that while policymakers agreed they should hold off hiking rates until there was evidence the growth slowdown was transitory, "most participants" believed "it would soon be appropriate" to raise borrowing costs.

The U.S. central bank raised interest rates by 25 basis points in March. Data on consumer spending and manufacturing have offered hope that growth picked up early in the second quarter after gross domestic product increased at a tepid 1.2 percent annualized rate at the start of the year.

The Atlanta Fed is forecasting GDP increasing at a 4.0 percent pace in the second quarter.

SLUGGISH WAGE GROWTH

Persistently sluggish wage growth could cast a shadow on further monetary policy tightening. Average hourly earnings rose four cents or 0.2 percent in May after a similar gain in April.

That left the year-on-year increase in wages at 2.5 percent.

But with the labor market expected to hit full employment this year, there is optimism that wage growth will accelerate.

There is growing anecdotal evidence of companies struggling to find qualified workers.

Republican President Donald Trump, who inherited a strong job market from the Obama administration, has vowed to sharply boost economic growth and further strengthen the labor market by slashing taxes and cutting regulation.

There are, however, fears that political scandals could derail the Trump administration's economic agenda.

A broad measure of unemployment, which includes people who want to work but have given up searching and those working part-time because they cannot find full-time employment, fell two-tenths of a percentage point to 8.4 percent, the lowest since November 2007.

The labor force participation rate, or the share of working-age Americans who are employed or at least looking for a job, fell two-tenths of a percentage point to 62.7 percent. It has rebounded from a multi-decade low of 62.4 percent in September 2015 and economists see limited room for further gains as the pool of discouraged workers shrinks.

Manufacturing employment fell by 1,000 jobs last month as payrolls in the automobile sector dropped 1,500 amid falling sales. Ford Motor Co (F) said last month it planned to cut 1,400 salaried jobs in North America and Asia through voluntary early retirement and other financial incentives.

Construction payrolls rose 11,000 last month. Retail employment fell 6,100, declining for a fourth straight month. Department store operators like J.C. Penney Co Inc , Macy's Inc (M), and Abercrombie & Fitch (AFN) are struggling against stiff competition from online retailers led by Amazon (AMZN).

Government employment decreased 9,000 last month.

The U.S. added a modest 138,000 new jobs in May and hiring earlier in the spring was weaker than initially reported, adding to evidence that the tightest labor market in years is making it harder for companies to fill open jobs.If you read that last article, you'd think the US economy is roaring. Unfortunately, it's not. Employment growth continues to decelerate at a steady pace and the US economic slowdown is only beginning.

The unemployment rate, meanwhile, fell again to 4.3% from 4.4% and touched the lowest level since 2001, the Labor Department reported. Yet the decline stemmed more from people leaving the labor force than an increase in the number who found jobs.

The increase in hiring last month was well below Wall Street’s forecast, but the Dow Jones industrial Average rose in early Friday trading, perhaps a signal the Federal Reserve won’t be aggressive in raising interest rates. Economists surveyed by MarketWatch estimated a 185,000 increase in nonfarm jobs.

The steady rate of hiring, ultra-low unemployment rate and growing evidence of pressure on companies to raise wages is likely to keep the Federal Reserve on track to raise interest rates when senior bank officials meet in mid-June. The bigger question how far and how fast the Fed goes, especially since broader inflationary pressures have receded in the past few months.

Whatever the case, the economy is on very solid ground. The U.S. is about to enter its ninth full year of expansion — making it the third longest since the 1850s — and there’s few cracks in the foundation.

In May, white-collar firms, health-care providers, restaurants and energy producers led the way in hiring. The only notable weakness was among traditional retailers that continue to lose ground to internet rivals. They cut jobs for the fourth straight month (click on image).

Average hourly pay rose 0.2% in May to $26.22. Although a tight labor market hasn’t resulted in the kind of rapidly rising wages experienced in the past, workers are collected somewhat bigger paychecks. Over the past 12 months hourly pay has increased 2.5%, significantly faster compared to a few years ago (click on image).

Many economists predict wages will rise faster in the months ahead as companies take a more aggressive approach to filling open positions as competition for a dwindling supply of labor intensifies.

“Business complaints of labor shortages have become increasingly widespread,” noted economist Ted Wieseman of Morgan Stanley.

The dearth of skilled workers available for hire might even be a chief cause of the recent slowdown in hiring, some say.

In the first five months of 2017, the U.S. has added an average of 162,000 jobs a month. That’s down from 187,000 in 2016 and as many as 250,000 a month in 2014, a postrecession high.

The recent soft patch in hiring has been especially pronounced in the spring. The government cut its estimate of new jobs created in April to 174,000 from 211,000. And March’s gain was reduced to 50,000 from 79,000.

Still, the labor market overall is the healthiest it’s been in more than a decade, and the economy shows no signs of slowing down. The current expansion has lasted 96 months and is now the third longest since World War Two.

The tight labor market has also been increasingly reflected by a broader measure of unemployment that includes those who can only find part-time work as well as discouraged job seekers. The so-called U6 rate fell again, to 8.4% in May, and is closing in on the precession low of 7.9%.

Charles Mills, who works in marketing and sales at Outdoor Landscaping and Design in Pennsylvania, said the economy is probably the best he can recall since the early 2000s before a nationwide real estate bubble burst.

“I think we are just on a upswing,” he said. People are better off financially and less afraid they are going to lose their jobs and their homes, he said.

The rock-solid if run-of-the-mill recovery has persuaded the Fed to embark on a series of gradual increases in interest rates that raise the cost of borrowing for consumers and businesses, a strategy designed to prolong the current expansion by preventing the economy from overheating.

And it's still a tale of two economies where far too many people are being left behind. While those students in the image at the top wait in line to attend TechFair LA, a technology job fair, in Los Angeles, that city is dealing with a staggering number of homeless trying to get by.

Now, before I begin my analysis, take the time to read a comment I posted back in mid April on why the next economic shoe is dropping. The problem with most economists is they tend to focus on lagging and coincident economic indicators (like inflation and employment), not leading indicators (like PMIs, stocks, credit spreads, inflation expectations) and they generally get it wrong at major inflection points.

And in terms of the US economy, we are at a major inflection point, one that will have a profound impact on global economies and financial markets.

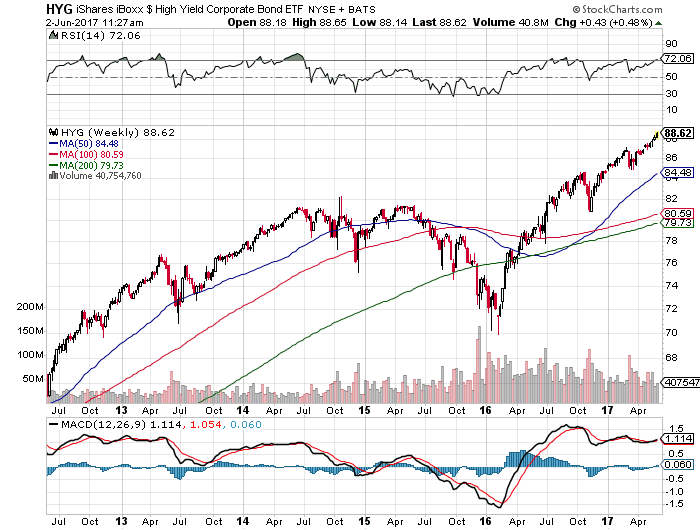

But the stock market is going up, up, UP! And? So what? It's called LIQUIDITY. There is a lot of money out there chasing risk assets, not just stocks, but also in the incredibly shrinking junk-bond market.

Have a look at the weekly chart of the iShares iBoxx $ High Yield Corporate Bond ETF (HYG):

It's been on a tear, making new highs, and shows no signs of abating. And as long as the high yield market keeps roaring, US stocks keep grinding higher.

But as the US economy slows, you can expect trouble to hit the high yield market, and that will spill over into the stock market. Why? Because companies have been borrowing heavily to repurchase their shares, to "reward investors" but also to boost earnings-per-share and executive compensation (see Harvard's study, Profits Without Prosperity).

This is why trouble in the corporate bond market doesn't bode well for stocks. As the economy slows, companies will not be able to borrow as much to repurchase their shares. In fact, stock buybacks have been driving companies further into debt, but thus far the bond market hasn't taken notice.

Now, getting back to Friday's jobs report. Typically what happens when the jobs number comes in less than expected, you will see US government long bonds (TLT) rally, the long bond yields decline (and the yield curve flattens), the US dollar sells off, and stocks bounce as investors expect the Fed to slow its planned rate hikes.

At the beginning of year, I told my readers to be weary of the reflation chimera and warned it's not the beginning of the end for US long bonds.

In fact, I've been very vocal to all my readers that if you want to sleep well at night, you should be loading up on US long bonds (TLT). And so far this year, I've been right on that call:

And I believe the best is yet to come for US long bonds, especially if another major financial crisis hits us in the fall or in 2018. Remember, in a deflationary world, US government long bonds are the ultimate diversifier, and will protect your portfolio from huge losses.

Now, let me stop here and talk a bit about the US dollar. Late last year, I discussed the 2017 US dollar crisis where I painstakingly went over the main macro trends and why the US was temporarily shouldering the world's deflation problems through a higher dollar.

Since the beginning of the year, as the US economy slows, the US dollar has been weak relative to the euro and yen. Some think it's the end of the dollar bull run but I think that is nonsense and explained why here.

The crucial thing to remember is the US economy leads the rest of the world by six to nine months. So, initially you will see the US dollar pull back but make no mistake, the uptrend is far from over.

Importantly, as the rest of the world slows, there will be increasing pressure on their currencies to shoulder the weight of the slowdown. And if another crisis hits us, everyone will be scrambling for US assets, especially US Treasuries.

All this to tell you I remain a dollar bull and would be using the pullback from the start of the year to load up on the greenback and US dollar assets. Below, I embed a weekly chart of the Powershares DB US Dollar Index Bullish Fund (UUP):

Despite the selloff since the start of the year, the uptrend remains, and I wouldn't be surprised if it starts climbing from these levels, even if the Fed doesn't hike rates three times this year.

As far as the Fed is concerned, nothing has changed in my mind. The Fed is petrified of global deflation, and is trying to raise rates to have enough ammunition to lower them once the next crisis hits.

The problem, of course, is if the Fed goes too far and raises rates too high, it will send the US dollar soaring, creating a huge crisis in emerging markets, which will exacerbate global deflation. We shall see but I doubt the latest jobs report augurs well for a third rate hike later this year.

As far as markets, nothing has changed in my views since I wrote my comment on a Goldilocks situation for stocks.

Given my views on the reflation trade and the US dollar, I would be taking profits and actively shorting emerging markets (EEM), Chinese (FXI), Industrials (XLI), Metal & Mining (XME), Energy (XLE) and Financial (XLF) shares on any strength.

The only sector I trade now, and it's very volatile, is biotech (XBI) which continues to grind higher on the weekly chart (click on image):

There are tremendous opportunities in biotech. I track over 200 biotech stocks (a thorough but incomplete list can be found here) and can tell you many of them are the top performers this year (click here to see YTD data from barchart). And the scary thing is there are many more which are just beginning to break out in a meaningful way.

Of course, biotech is only a small part of the story driving the Nasdaq to record highs. Along with the rise of biotech, shares of Apple (APPL), Amazon (AMZN), Facebook (F), Google/ Alphabet (GOOG) and other tech companies are propelling technology (XLK) shares to record levels:

These are bullish charts but you should keep in mind that nothing goes up forever. I still maintain that if you want to sleep well, you need to protect your downside risks. This is why I continue to recommend buying US long bonds (TLT) on any pullback as I think we have yet to see the secular lows in bond yields.

In fact, I'm not the only one who claims we have yet to see the secular lows in bond yields. Below, Erik Townsend speaks with Dr. Lacy Hunt of Hoisington Investment Management on MacroVoices (minute 15). Listen carefully to what Lacy Hunt says on extreme over-indebtedness, debt accumulation, and asset prices.

Interestingly, Lacy Hunt focuses on debt as the main problem where as for me, excessive debt is part of the inequality problem, and just one of the six structural factors that lead me to believe we are headed for a prolonged period of debt deflation:

- The global jobs crisis (high structural unemployment, less and less good paying jobs with benefits)

- Ageing demographics (more and more older people with little savings spending less)

- Pension crisis (related to the second factor, shift out of DB to DC is deflationary)

- Excessive private and public debt (constrains government and consumer spending)

- Growing inequality (impacts aggregate demand and is deflationary)

- Technological shifts which are deflationary (Amazon, Ubber, Priceline, AI, robotics, etc.)

Lastly, please take the time to subscribe/ donate to this blog on the right-hand side under my picture. I work hard to bring you the very best insights on pensions and investments and thank all of you who take the time to show your financial support, it's greatly appreciated.

Comments

Post a Comment