Steven Cohen's Dubious Rerun?

Don’t call it a comeback just yet.

As Bloomberg News reported on Tuesday, hedge fund manager Steven A. Cohen is preparing to raise as much as $10 billion from outside investors in 2018 for a new fund. Combined with his personal fortune of $11 billion, the fund could oversee more than $20 billion, which would make it the largest U.S. hedge fund launch in history.

Do It Again

It would also mark an extraordinary turnaround for Cohen. Just four years ago, he made history in all the wrong ways. His hedge fund firm at the time, SAC Capital Advisors LP, was charged with insider trading. The firm pleaded guilty and paid a record $1.8 billion penalty.

In addition, six current or former SAC employees were convicted of various criminal charges related to insider trading. Cohen was never charged with insider trading, but the Securities and Exchange Commission did accuse him of failing to supervise misbehaving employees. In the ensuing settlement, Cohen agreed not to manage outside money until Jan. 1, 2018.

Theories abound about why Cohen would want to get back in the game of managing other peoples’ money, ranging from ego to boredom. And in the end, he may not go through with it.

Cohen clearly doesn’t need the money. Sure, it would be nice to have outside investors help pay for his 1,000-employee family office, Point72 Asset Management LP. But the profits on his personal investments should more than cover those expenses.

Maybe, as Fortune writer Jen Wieczner put it, “Steve Cohen wants people to believe that he never did anything wrong. So how does he prove that? Well, if he can deliver the highest returns -- at least as high as he always has -- while he literally has people from the government, including a government appointed compliance monitor, in his office, then people are going to believe that he really is just that good.”

But trying to recreate the SAC magic with $20 billion would be a huge gamble. If Cohen falls short, it would only reinforce the suspicions he might be trying to dispel. And generating outsize returns with that much money won’t be easy.

Hedge funds generally don’t disclose their performance to the public, but Frontline published a chart in 2014 showing SAC’s annual returns from 1992 to 2012. Using that chart, I estimated the performance of SAC Capital Management LP -- SAC’s fund for U.S. investors -- during that period.

The fund’s performance over the entire period was spectacular. SAC tripled the return of the broad market with comparable risk. The fund returned roughly 26 percent annually over those 21 years with a standard deviation of 22 percent. Over the same time, the S&P 500 returned just 8 percent annually, including dividends, with a standard deviation of 19 percent. (Standard deviation reflects the performance volatility of an investment; a lower standard deviation indicates a less bumpy ride.)

There’s a critical detail in the numbers, however. Cohen launched SAC in 1992 with $25 million. Over the next 10 years, the fund returned roughly 43 percent annually, or 30 percentage points annually better than the S&P 500.

Then investors piled in. The firm eventually ballooned to $16 billion, and sustaining those monster returns became ever more difficult along the way. Over the 10 years that ended in 2012, the fund returned roughly 12 percent annually, or 5 percentage points annually better than the S&P 500.

It’s not just SAC. According to Hedge Fund Research Inc., hedge funds managed $100 billion in 1992. Over the next 10 years, the HFRI Fund Weighted Composite Index returned 15 percent annually. By 2012, hedge funds were managing $2.3 trillion, and the returns over the previous 10 years shrunk to 7 percent annually.

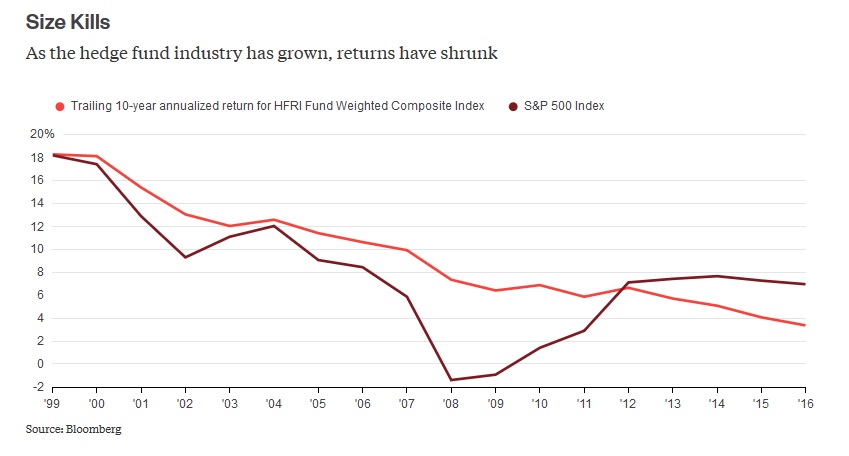

Size Kills

As the hedge fund industry has grown, returns have shrunk

It’s a recurring theme in finance: Size kills. There’s a reason why one of the best-performing hedge funds of all time, Renaissance Technologies’ Medallion Fund, obsessively caps its capacity at $10 billion. And yet it’s a lesson that both managers and investors routinely fail to heed.Rachael Levy of Business Insider also reports, Steve Cohen just took a big step forward in his comeback with a massive new hedge fund:

It's one that Cohen can't ignore as he decides whether he wants to try to reconjure the magic.

Steve Cohen, the billionaire hedge-fund manager briefly banned from the industry after an insider-trading investigation, this week sent investors documents pitching his new fund, Stamford Harbor Capital, a person who has reviewed the deck told Business Insider.

The pitch is the latest move cementing the controversial billionaire's return to managing money.

Investors will have to agree to steep terms to put their money with the famed investor — including a minimum investment of $100 million and an annual management fee of over 2.5% of those assets — this person said, asking not to be identified discussing private information.

Jonathan Gasthalter, a spokesman for Cohen, declined to comment for this story.

Cohen's new fund is arguably one of Wall Street's most anticipated new launches. Bloomberg News reported earlier this month that he could raise between $2 billion and $10 billion. At the high end, it would be the largest hedge-fund launch in history.

'Wink wink, nudge nudge'

Until now, though, investors, advisors, and others in the hedge-fund industry said Cohen's representatives had limited themselves to vague and almost bizarrely hypothetical conversations about the fund along the lines of: If a particular person named Steve Cohen happens to launch a fund, and that fund happens to open next year, what would it take for an investor to sign on?

"It was a lot of wink wink, nudge nudge," said one person, who spoke of meetings before the documents were sent this week. As Bloomberg News reported earlier this month, the official line, meanwhile, was that Cohen was undecided about his plans.

Cohen has been running a family office called Point72, with some $11 billion in assets, since 2014 after he agreed not to manage other people's money and return outside investors' capital. The agreement came after a years-long insider trading investigation at Cohen's SAC Capital that ended with a conviction for one of Cohen's subordinates but not him. His failure, according to the SEC, was to supervise those traders as head of SAC Capital. SAC also pleaded guilty and paid a record fine, $1.2 billion, to settle insider-trading claims.

The ban will be lifted in January 2018.

Now, in anticipation of this, Cohen's marketing is being led by a man named Doug Blagdon at an advisory firm called ShoreBridge Capital who previously led the marketing effort at SAC Capital. Blagdon didn't immediately respond to requests for comment.

Wealthy investors, funds of hedge funds and sovereign wealth funds are the most likely investors in Cohen's new fund, people in the industry say. Public pensions, endowments, and foundations that have become major backers of the hedge fund industry are likely to stay out because they face greater public scrutiny and may find it difficult to explain an investment with a manager who — though he generated huge profits — was tarred by an association with a huge insider trading scandal.

Cohen is also said to have lined up firms to handle the back-end of a hedge fund's operations — the prime brokers who would manage settlement of trades and other basic functions as well as the "cap intro" teams at big banks who serve as gatekeepers to investors. Still, the pitch to investors is not yet widespread, and may never be. Many investors who are usually briefed on hedge fund launches say they have yet to hear anything.

Privately, Cohen has expressed doubts about whether he should come out again, a potential investor who also knows Cohen personally said. Cohen's family office hasn't recently posted the kind of 30% annual returns that he was once famous for.

"I suspect the real question is whether Cohen can still achieve outsized alpha," said Chris Cutler, a consultant, using a hedge-fund term for outperformance. "If even he can't, what is the fate for other long/short-focused managers? I think Cohen will have a willing and ready list of LPs ready to invest with him. He doesn't need to worry about which LPs won't invest with him."

Staffers at Point72, which has been investing Cohen's billions since SAC got shut down, have been largely kept in the dark. They were unsure until recently whether Cohen would open up again. Those who know Cohen personally say the same.

Staffers said they hoped that Cohen would raise outside money – it would show a sense of permanency for their jobs and would make it less likely that Cohen would shut the operation down voluntarily, a person familiar said. Creating a hedge fund would also spread the cost of employees and support staff among other investors — as Point72 is currently managing Cohen's own money and that of some employees.

The hefty demands being made of investors — the minimum investment and fees — are a luxury only afforded to the most superstar investors. Cohen is one, famed for his consistent double-digit returns before he was rocked by the insider-trading investigation.

He has an army of admirers, often those who were made rich by him, either by working for him directly or by investing with him. Many think he has never done anything wrong, and that he's the greatest investor of all time.

Blatant 'no'Jon Shazar of Deal Breaker also reports, Kicking And Screaming Steve Cohen Being Dragged Back To Hedge Fund Industry:

But he's also a polarizing figure because of the legal issues.

For at least two investors Blagdon has reached out to, and other potential investors who have yet to hear from him, the answer is a blatant "no."

No matter that the past several years, Cohen has tried to clean up his image. He hired former Department of Justice staffers and McKinsey consultants, and started a training program for young college grads – something Business Insider was invited to tour.

To show how compliant he was, he even put a ban on hiring from Visium, an $8 billion-dollar fund that shut down amid one of the most recent insider-trading scandals, before the public knew that Visium was even under investigation.

Still, it would be "willful ignorance" to think Cohen didn't have some hand in the trading, or at least know about it, one person in the industry said.

Investors who worry about this won't be investing.

At long last, the pretense that Steve Cohen’s return to the hedge fund industry (which is not really a return at all, but whatever) is lifting: Now, in addition to the third-party marketer and fee structure and growing global footprint and ramped-up hiring and shadow-boxing with British regulators and all the rest of it, there’s something tangible and not easily deniable in a “we’re just trying to run the best damned family office we can” sort of way: a marketing deck for Stamford Harbor Capital that’s been seen by real potential investors, albeit not all that many of them.Lastly, Ronald .orol of The Street reports, The Astonishing Return Of Steven Cohen:

Until now, though, investors, advisors, and others in the hedge-fund industry said Cohen’s representatives had limited themselves to vague and almost bizarrely hypothetical conversations about the fund along the lines of: If a particular person named Steve Cohen happens to launch a fund, and that fund happens to open next year, what would it take for an investor to sign on?There is also the matter of the service providers being lined up, including cap intro folks who’ll get to pitch potentials on the twice-in-a-lifetime opportunity to invest with the great man, now at the low, low price of a 2.5% management fee and $100 million minimum investment, which are the sorts of things that family offices don’t really need but that hedge funds do.

“It was a lot of wink wink, nudge nudge,” said one person, who spoke of meetings before the documents were sent this week.

Even still, however, there are those clinging to the belief that Cohen will not, in fact, begin managing outside money again. Including, the rumors and water-cooler talk on Cummings Point Road say, Steve Cohen himself.

Privately, Cohen has expressed doubts about whether he should come out again, a potential investor who also knows Cohen personally said. Cohen’s family office hasn’t recently posted the kind of 30% annual returns that he was once famous for….So why, wracked with self-doubt and with his heart not in the project, would Papa Bear be willing to put himself out there? To risk getting hurt again? To deal with slings and arrows like the following?

Staffers at Point72, which has been investing Cohen’s billions since SAC got shut down, have been largely kept in the dark. They were unsure until recently whether Cohen would open up again. Those who know Cohen personally say the same.

For at least two investors Blagdon has reached out to, and other potential investors who have yet to hear from him, the answer is a blatant “no….”Open your eyes (and hearts), people: Steve Cohen is not doing this for himself! He doesn’t need the money, even if it would come in handy when that tax bill shows up or during his next visit to Christie’s. It’s not even about redeeming his good name. No: Coming back, in the face of the scorn and sniggers, isn’t about raking in a cynical $250 million a year just for sitting on people’s money. It’s about helping people. It’s about not disappointing his fans and his dependents. It’s practically a philanthropic effort for this man focus his time and attention on managing outside capital at these ridiculously low ratess.

It would be “willful ignorance” to think Cohen didn’t have some hand in the trading, or at least know about it, one person in the industry said.

Staffers said they hoped that Cohen would raise outside money – it would show a sense of permanency for their jobs and would make it less likely that Cohen would shut the operation down voluntarily, a person familiar said….

He has an army of admirers, often those who were made rich by him, either by working for him directly or by investing with him. Many think he has never done anything wrong, and that he’s the greatest investor of all time.

In 2013, an insider-trading scandal took apart billionaire Steve Cohen's otherwise incredibly successful hedge fund.Love him or hate him, there's no doubt Steve Cohen is one of the best hedge fund managers of all time.

But surprising, perhaps shockingly, at least for those who haven't followed the situation closely, Cohen is back. A 2016 settlement with the Securities and Exchange Commission will allow the beleaguered money-manager to accept outside money starting in January. Cohen hasn't said whether he wants to take on other investors, but the consensus opinion is that he will the second he's permitted. Expect to find lots of willing investors ready to allocate capital to his funds - and the intense glare of the nation's securities regulator watching his every move.

"I say this with a certain pessimism, but I think he'll have no difficulty marketing his fund to a certain kind of investor," said Columbia Law School Professor John Coffee. "The investors don't take the risk of criminal liability, Cohen and his fund managers do."

In 2013, Preet Bharara, then the U.S. attorney for the Southern District of New York, issued an indictment of Cohen's fund, S.A.C. Capital Advisors, the only time a whole hedge fund had been charged with insider trading. Specifically, the SEC charged Cohen with failing to supervise employees, some whom were convicted of insider trading while working for the fund.

"Bharara came within a whisker of charging Cohen," Coffee said. "It was a judgment call, and he didn't want to take the risk of losing a high-profile case."

At the center of the SEC's charges involved so-called "expert networks," firms that provide specialized information about companies and industries to hedge funds, mutual funds, and other investment firms in exchange for large fees. In the case, the SEC alleged that an S.A.C. Capital portfolio manager, Mathew Martoma, traded on confidential information about a drug trial provided by Dr. Sidney Gilman. Gilman was chairman of a safety-monitoring committee overseeing the clinical trial and a paid consultant to an expert networking firm that Cohen's hedge fund employed.

Flash forward to 2017. Cohen manages a "family office," Point72 Asset Management LP, based in Stamford, Conn., under an SEC exemption that lets him advise family members only. Cohen's family office, however, has over 1,000 employees and offices in New York, London, Hong Kong, Tokyo, and Singapore.

Point72's capital can sometimes be found at companies targeted by an activist investor. The firm reported a significant stake in Pandora Media Inc. (P - Get Report) , where Corvex Management's Keith Meister has been agitating. It also owns stakes in BroadSoft Inc. (BSFT - Get Report) , Brookdale Senior Living (BKD - Get Report) CenturyLink Inc. (CTL - Get Report) and Bob Evans Farms BOBE, all also recent targets of activist efforts. Post Holdings on Tuesday announced it was buying Bob Evans for $1.5 billion, at a significant premium.

Should the high-profile money-manager start accepting external investors, expect the SEC to be watching intensively, taking special notice if Cohen's fund engages the same kinds of expert networks that got him into trouble in the first place.

"If I were Mr. Cohen I would be quite careful about employing expert networks," said Tom Gorman, a partner at Dorsey & Whitney LLP and a former senior counsel at the SEC in Washington. "The SEC may well want to look at the sources behind the information coming from the expert networks."

Gorman suggested that the agency may have less concern about those networks if its analysts are not also employed in a particular industry. However, if, for example, the networks bring in doctors who are supervising trials for drug companies that would be a red flag, he added.

And Columbia's Coffee agrees that the commission will be watching. "The SEC is like the elephant, it never forgets. They'll always have him in mind," Coffee said.

Looking back at the Cohen case, prosecutors, ex-SEC lawyers, and academics all contend that it would likely have been a lot easier for the government to prove its insider-trading case today, following a federal appeals court decision last month to uphold Martoma's conviction.

Specifically, in a 2-1 decision, the U.S. Court of Appeals for the Second Circuit found that a lower court's ruling should stand and that the government had "presented overwhelming evidence that at least one tipper had received a financial benefit" from providing confidential information to Martoma.

"Based on this [August] result, the SEC may have gotten what they initially requested in the case -- to bar him [Cohen] from the securities business," Gorman said.

Nevertheless, Gorman noted that the August court decision wouldn't have any direct impact on Cohen's situation because he settled with the SEC in a January 2016 deal that prohibited the billionaire money manager from accepting outside money for two years. Had that settlement come after the August decision, Cohen might not be posed to return to the investment advisory game.

Now, Cohen appears to be taking steps to accept outside money. In March, he set up a hedge fund next to Point72 called Stamford Harbor Capital, of which he owns 25%.

"One reason to set up a hedge fund like Stamford Harbor Capital is to establish a track record for a particular kind of strategy before seeking to accept outside money," Gorman said. "This way the adviser can tell outside investors that the fund, with a particular trading focus, has achieved a certain return over a period of time."

Also, Cohen reportedly hired ShoreBridge Capital Partners to gauge and identify interest among outside investors in such a fund. Prospective clients have reportedly already begun receiving marketing material, and Bloomberg reports that Cohen could raise between $2 billion and $10 billion. Shorebridge did not return calls.

Many investors are sure to express an interest. Kerrisdale Capital founder Sahm Adrangi, a prolific activist, and short-seller said he expects that Cohen's fund will meet tough compliance requirements for big funds that take in outside money. That level of oversight should comfort investors interested in allocating capital but wary of Cohen's background.

"These platform shop firms have a very strict compliance infrastructure," Adrangi said. "They have a lot of officers and software and technology they use to monitor everyone across-the-board with respect to compliance."

For now, expect investors -- and the SEC -- to be paying close attention.

There is also no doubt he's coming back to run a hedge fund and he will most definitely have a say in investments and trading operations.

I actually called Point72 Asset Management this morning to arrange a short (15 minute) phone conversation with Steve Cohen and was politely turned down by Mark Herr, Managing Director, Head of Corporate Communcations at Point72:

Given how quickly Mark responded to my email inquiry, I highly doubt Steve Cohen even read my email. Or maybe he did and remembered an older comment of mine, the perfect hedge fund predator, and said "no way, this guy is nuts!"."Steve has asked me to respond to your email, seeking an interview with him for your blog.We’re going to pass.Sorry we can’t be more helpful on this."

Whatever, it doesn't matter if Steve Cohen doesn't want to talk to me, I will give you my honest and fair opinions here. Cohen most definitely wants to come back to manage outside money and it has nothing to do with money or ego, it's all about his legacy.

In his deepest moments of self-reflection, Cohen has to be thinking about his legacy and how he will be remembered. He doesn't want people to remember him as the hedge fund king who ran the world's biggest insider trading hedge fund. He wants to be remembered as one of the best, if not the best, hedge fund manager who ever lived.

Of course, his reputation is forever tarnished. He knows this, he's not an idiot. But think what you want about SAC Capital and all the shady things that went on there, there's no doubt he is an incredible trader who has a great sense of markets and he hired very talented traders and individuals.

Will he be able to produce 30%++ annual returns ever again? No, not in his wildest dreams. That's just a pipe dream not just for him but for Jim Simons, Ken Griffin, George Soros, Ray Dalio, David Tepper and many other "elite" hedge fund managers I cover here every quarter.

And what gives him the right to charge a 2.5% management fee and demand $100 million minimum investment? Nothing, he's Steve Cohen, he can charge whatever he wants, and at one time was charging 3% management fee and 50% performance fee to manage outside money (How do you think he amassed a fortune in the multi billions? It wasn't his good looks and charm!).

Will institutional investors accept those terms? Some will, some won't. I highly doubt Jagdeep Bachher over at the University of California will (maybe he will) but I can almost guarantee you Ontario Teachers' Pension Plan, the Caisse and CPPIB will have a very close look at Cohen's new hedge fund regardless of his terms and shady past.

If they don't, they won't be doing their job and fulfilling their fiduciary duty. Period.

I would even go back to Cohen and say "Why don't we agree on a 3% management fee contingent on a 15% hurdle rate above Libor? If you don't attain the bogey, management fee drops to 50 basis points. How do you like them apples, big guy?"

In all seriousness, every large institutional investor in the world should be looking very hard at Steve Cohen's new fund, send a due diligence team down there, kick the tires thoroughly and talk to a lot of senior and junior staffers, even Papa Bear himself if he's willing to take some time from his busy schedule to talk to you.

Last Friday, I warned my readers to prepare for the worst bear market ever. I believe that now is the time to get to work to find great hedge fund and private equity partners who are able to deliver alpha over a very long period.

Forget Warren Buffett's bet, forget everything you think is proven right because markets keep making record highs, you need to prepare for a long, arduous bear market across public and private markets.

Now more than ever, you need to be allocating risk a lot more intelligently even if it means paying big fees to outside managers with proven track records. Period.

And if my fears of deflation coming to the US prove right, you need to find hedge funds that know how to trade and deliver alpha in highly volatile markets (the lower rates go, the more volatile things will get).

In short, you need a guy like Steve Cohen to add alpha to your portfolio but also to leverage off his deep insights on markets. You don't have to love him. You are a number to him and he should be the same to you but try to learn from him as much as possible by investing with him and other elite hedge fund managers.

That's all I have to say about Steve Cohen's "dubious rerun". I'll send my comment over to Papa Bear and if he has anything to add, I will update you.

Below, Bloomberg's Simone Foxman discusses Steve Cohen's pitch for a comeback. I agree that he was targeted and singled out among a group of hedge funds back then.

Also, Fox Business News' Charlie Gasparino reports billionaire investor Steve Cohen could be plotting a comeback. Gasparino and Liz Claman talk on Closing Bell and he provides interesting insights on Cohen's next moves.

Lastly, watch the PBS Frontline investigation, To Catch a Trader, and Sheelah Kolhatkar, author of Black Edge, discusses the government's wide-reaching fraud investigation against Cohen on Lunch Break with Tanya Rivero as well as how Cohen emerged from the investigation as one of the world's wealthiest men.

You should watch these clips with a shaker of salt. They're not wrong but blatantly biased and let me assure you, SAC wasn't the only big hedge fund that routinely engaged in shady activities to gain an edge. It got caught while others never attracted the attention to get caught.

Also, people make mistakes in life, they learn from them and move on. Cohen had plenty of time to think about the mistakes he made and how he wants to rebrand himself and run his new fund, making sure everything is kosher and upfront no matter what.

Let me leave you on another note. The multi-strategy hedge fund that really impresses me these days is Balyasny Asset Management which has been hiring from Citadel, Point72 and J.P. Morgan. Steve Cohen isn't the only big player out there and there's a lot more competition out there nowadays.

Cohen knows this all too well but I think he's ready to put the past behind him and make the comeback of his life.

And yes, if I had a choice to work at Bridgewater and deal with Ray Dalio's obsessive focus on culture and principles or working with a bunch of great traders under Cohen's watch, I'd opt for the second, hands down. Both are high-pressure, cutthroat shops but one is a lot more fun to work at.

Update: Things aren't starting off well for hedge fund king Cohen. According to the New York Times, just months before starting his new fund, Cohen lost his top trader, Phil Villhauer.

Comments

Post a Comment