Outlook 2018: Return to Stability?

The Dow Jones Industrial Average posted its second-biggest yearly gain of the past decade in 2017, rising a surprising 25%.

The market notched the most closing highs for the index in a single calendar year. Volatility swooned to historic lows and many global stock markets finished the year at or near records or multiyear highs.

It’s a sharp change from what many money managers and analysts anticipated at the start of 2017. At the time, many expected what they called a “sideways market,” where the overall levels of major indexes would remain little changed at year-end. Instead, the S&P 500 posted its best yearly gain since 2013.

Some of them acknowledge they were surprised by a confluence of market-supporting trends. They didn’t expect corporate earnings and revenues to grow at such a fast clip. They didn’t anticipate the economies of all 45 countries tracked by the Organization for Economic Cooperation and Development to be on pace to expand, an uncommon synchronicity. They certainly didn’t predict the Dow would rise for nine consecutive months, its longest streak of monthly gains since 1959, even in the face of geopolitical turmoil in Washington and around the world (click on image).

“There was no knocking the market off its perch,” said JJ Kinahan, chief market strategist at TD Ameritrade. “A couple times it wobbled, but we never saw a wild rush of sales in the market. Every dip was marked with big buyers.”

Heading into 2017, many analysts and investors expected moderate gains for the S&P 500. Goldman Sachs Group Inc. forecast in a January 2017 report that the index would rise to 2400 in the first quarter before fading to 2300 by year-end. Credit Suisse also estimated in early January that the index would close out 2017 at 2300. The S&P 500 closed at 2673.61 Friday.

Underpinning the index’s 19% climb in 2017 has been corporate-earnings growth, which is on pace to post its largest increase since 2011, as measured by earnings per share. At the end of the first quarter, analysts polled by FactSet were expecting companies in the S&P 500 to post 9.1% earnings growth in that period. Instead, companies grew their earnings by 14%, FactSet data show. That expansion has continued, albeit at a slower pace: In the second quarter, earnings for companies in the S&P 500 rose 10% from the year prior, and in the third quarter that growth was 6.4%.

“We’re seeing a peak rate of growth,” said Bob Doll, senior portfolio manager and chief equity strategist at Nuveen Asset Management. However, that doesn’t mean investors should rush to sell stocks, he said—even if growth slows in the next year or two, there is still upside potential, he said.

Mr. Doll, who said his own predictions for the S&P 500’s 2017 rise fell short, also attributed the outsize gains to the synchronous economic expansion around the globe. The U.S. recovered from the financial crisis more quickly than other countries, but that changed in 2017 as others caught up. The result is global stock indexes near records or multiyear highs, from Japan’s Nikkei Stock Average to the U.K.’s FTSE 100. The MSCI All Country World Index is also near a record.

The steep gains of 2017 have some analysts worried that the rally could wane in 2018, particularly if volatility, which hit historic lows this year, ticks up as many predict. Stocks are trading at above-average multiples of their past 12 months of earnings and government bonds have been sending cautionary signals about the U.S. economy’s prospects, something that could end up jolting indexes in 2018.

The yield on the benchmark 10-year Treasury note, often seen as a gauge of investors’ sentiment about the economy, closed at 2.409% on Friday, down slightly from 2.446% at the end of 2016 in defiance of analysts’ predictions that it would soar in 2017 with a surge in growth and inflation. Its premium relative to the two-year note yield has been cut by more than half over the past year (click on image).

Though analysts have debated its significance, a shrinking gap between short and long-term Treasury yields, known on Wall Street as a flattening yield curve, has often been a warning sign for investors. Five of the past six times the two-year yield surpassed the 10-year yield, known as an inverted yield curve, the economy subsequently entered a recession, according to data from the St. Louis Fed.In my last comment of 2017, I explained why I doubt 2018 will be a repeat of 2017, and went into detail on why the big rally in technology shares last year isn't a particularly good sign for markets this year (a big rally in large cap tech shares is a sign of Risk Off markets).

With few other signs of recession, however, many investors say there are reasons to doubt the yield curve’s signals, which some argue have been distorted by easy-money policies from central banks in Europe and Japan pushing yield-seeking investors into U.S. government bonds, driving down the yields on longer-term debt.

Still, many investors and analysts expect the curve to continue its flattening in 2018, given signs that the Federal Reserve will keep raising interest rates even if inflation remains stuck below its 2% annual target. That could push up the two-year yield, which is more sensitive to expectations for central-bank policy.

That, plus a potential deceleration in economic growth, could set up 2018 to be a tougher year. A bright spot some analysts point to is corporate tax cuts, which could boost earnings growth and stock prices. Yet, some analysts say they are worried the potential benefits from the tax bill are already priced into company shares, limiting upside in 2018.

“We’ve gotten used to things being very good,” said Brad McMillan, chief investment officer for Commonwealth Financial Network, who added that he doesn’t expect either big declines or big gains in 2018. “We don’t need the tailwinds to turn into headwinds, we just need a couple to go away to find ourselves in a very different market environment.”

However, early in the new year US stocks started the year off with a bang, breaking new records, and strong economic data around the world is buoying global shares to new highs as well.

This is why some market observers think despite coming off a great year, another huge rally in stocks is in the offing this year. Thomas Franck of CNBC reports, A Merrill Lynch indicator that predicted last year's surge sees another 19% gain in 2018:

Stocks could pop nearly 20 percent in 2018 according to a contrarian indicator from Bank of America Merrill Lynch which predicted last year's surprising surge.And Annie Pei of CNBC reports, The most important chart for the market next year, according to a top technician:

The investment bank's so-called Sell Side Indicator measures the average equity allocation recommended by its fellow Wall Street bank peers. The indicator shows Wall Street is still not very bullish on the market at all and until they recommend clients own even higher levels of stocks, the market will continue to gain.

"Historically, when our indicator has been this low or lower, total returns over the subsequent 12 months have been positive 93 percent of the time, with median 12-month returns of 19 percent," according to a BofA Merrill Lynch Global Research report (click on image).

In September 2016, the metric predicted a huge positive return over the next 12 months, a forecast that eventually came true and stood in contrast to the sentiment on Wall Street at the time. Now in early 2018, the model still remains upbeat.

2018 "could be the year of euphoria. Sentiment is now a more important driver of the S&P 500 than fundamentals, and sentiment suggests there is still room for stocks to move higher in the near term," wrote BofA Merrill Lynch strategists in the 2018 outlook press release in December.

To be sure, this indicator is only one input in Bank of America's bigger forecast model. Officially the bank predicts just a 5 percent rise in the S&P 500 to 2800 this year.

The strategist's target is just below the median 2,850 forecast of 13 other equity strategists surveyed by CNBC. That median projection is modest in comparison to the roughly 20 percent climb for the S&P 500 in 2017.

"We think euphoria is what's going to end this bull market and we're not there yet," Savita Subramanian, the bank's chief U.S. equity and quant strategist, told CNBC in December. "We're not at the point where the investment community is saturated in equities and there's nothing to do with stocks but sell."

In a year when equities across the world have rallied in synchrony, Ryan Detrick of LPL Financial has identified what could be the most important chart for the market next year, as it could signal that the global rally is far from done.In fact, things seem so strong in the economy and markets that Forbes contributor Bryan Rich thinks this year will mark the return of 'animal spirits':

With the S&P 500 up 20 percent this year, on pace for its best year since 2013, emerging markets up 35 percent and Europe's STOXX 600 index up 8 percent, many market watchers have applauded 2017 as the year of global growth.

A big driver of the global markets rally has been earnings. Detrick, who is a senior market strategist, says that based on one chart, the global earnings outlook is still positive for next year.

"We've seen a resurgence of global earnings in 2017 with the S&P 500, emerging markets and developed markets all positive ... [that's the first time it's happened] since 2010," he said Thursday on CNBC's "Trading Nation."

"Fortunately we're looking at all three of them being positive again next year," added Detrick.

And even though Detrick says there could be more volatility in 2018, he also sees signs of strong fundamentals in the U.S. and abroad that he believes validates the momentum of economic growth around the world.

More specifically, he points to tax reform and the rally in industrial metals such as copper, up 31 percent this year and seen as an indicator of industrial demand, as two factors that could uphold earnings growth in 2018.

"We definitely think a lot of it could be priced in so far what we've seen this year, and we could have some more rocky volatility next year," said Detrick. "But all in all, we just upped our forecast for earnings from about $143 a share to just under $150."

"As we look out 12 to 18 months, there are still a lot of positives," he added. "We've got tax reform, which should continue to drive markets higher."

Within U.S. markets, Detrick says small-caps and financials are the best buys for investors, thanks to tax reform. He also encourages investors to look at emerging markets thanks to their moderate valuations, and he predicts they will continue to grow in 2018.

We are off to what will be a very exciting year for markets and the economy.As I discussed in my last comment of 2017, I'm highly suspicious of the recent rallies in metals and mning (XME) and energy (XLE) indexes and think the rally in comodities in general is a tradeable rally but not something which is sustainable over the course of the year.

Over the past two years I've written this daily piece, discussing the big slow-moving themes that drive markets, the catalysts for change, and the probable outcomes. When we step back from all of the day to day noise that has distracted many throughout the time period, the big themes have been clear, and the case for higher stocks has been very clear. That continues to be the case as we head into the new year.

As I've said, I think we're in the early stages of an economic boom. And I suspect this year, we will feel it--Main Street will feel it, for the first time in a long time.

And I suspect we'll see a return of “animal spirits.” This is what has been destroyed over the past decade, driven primarily by the fear of indebtedness (which is typical of a debt crisis) and mistrust of the system. All along the way, throughout the recovery period, and throughout a quadrupling of the stock market off of the bottom, people have continually been waiting for another shoe to drop. The breaking of this emotional mindset has been tough. But with the likelihood of material wage growth coming this year (through a hotter economy and tax cuts), we may finally get it. And that gives way to a return of animal spirits, which haven't been calibrated in all of the economic and stock market forecasts.

With this in mind, we should expect hotter demand and some hotter inflation this year (to finally indicate that the global economy has a pulse, that demand is hot enough to create some price pressures). With that formula, it's not surprising that commodities have been on the move, into the year-end and continuing today (as the new year opens). Oil is above $60. The CRB (broad commodities index) is up 8% over the past two weeks -- and a big technical breakout is nearing (click on image).

This is where the big opportunities lie in stocks for the new year. Remember, despite a very hot performance by the stock market last year, the energy sector finished DOWN on the year (-6%). Commodity stocks remain deeply discounted, even before we add the influence of higher commodities prices and hotter global demand. With that, it's not surprising that the best billionaire investors have been spending time building positions in those areas.

In my opinion, the key thing to watch for commodities and commodity and energy shares isn't the trillion dollar US infrastructure plan which has yet to arrive but whether the rout in the US dollar continues (click on image):

Looking at that weekly chart above, there could be more weakness ahead but it's at an interesting level and it could reverse course. And if the US dollar starts rallying from here, which is my call, it will put pressure on commodity prices and currencies, energy shares and emerging market bonds, stocks and currencies.

This was my long preamble to my much-anticipated outlook 2018, and this year I've gotten a lot of help from a friend, François Trahan, a top Wall Street strategist, someone I respect a lot because not only is he a super nice guy, he really knows his macro and market indicators very well and uses them to help top institutional funds manage money by positioning them in the right sectors.

I've said it before and I'll say it again: If you can afford his research, I highly recommend you contact the folks at Cornerstone Macro where François is a partner and subscribe to all their research, including his Portfolio Insights and Strategy. Cornerstone produces high quality, independent research which covers the economy and markets extremely well. It's not cheap but it's great actionable research which will help you assess the risks and opportunities that lie ahead in markets.

What I like about François is he's a macro guy like me and uses his insights to formulate a positioning story based on solid macro research. I emphasize positioning because that's what he and his team are really good at, namely, recommending stock sectors, not where the S&P 500 or the yield on the 10-year Treasury note is going to close at the end of the year.

A long time ago, François graduated from the BCA Research school of macro, as did I and plenty of others. He was there right before my time at this macro research firm but was smart enough to leave Quebec and go on to much bigger and better things on Wall Street where he did stints at Brown Brothers Harriman, Bear Stearns, ISI and Wolfe Trahan & Co. (now Wolfe Research) before founding Cornerstone Macro with other partners.

He has also co-authored a great little book with Kathy Krantz, another former BCAer, and they titled it "The Era of Uncertainty: Global Investment Strategies for Inflation, Deflation, and the Middle Ground" (published it in 2011).

François was enjoying his holidays with his family in Quebec and was gracious enough to call me so we can catch up and discuss markets. He spent almost two hours (on two separate calls) with me to go over his views, what went right and wrong in 2017, and where he thinks we're heading.

I love talking markets and so does he which is why our conversation was long but I tried as much as possible to let him speak, even if I interjected on occasion as I just wanted him to go on and explain everything on his mind. I want to publicly thank him for taking the time to discuss his views with my blog readers.

Before I proceed, it's important to note that François's outlook comment came out earlier this week and I waited till now to share my outlook comment as I think it's only fair his clients see it first.

Also, an important legal notice to all my blog readers: The charts below are copyright material of Cornerstone Macro and I have explicit permission to use them for this blog post. Anyone forwarding these charts or using them in a presentation without explicit permission from Cornerstone Macro will be prosecuted to the full extent of the law (I'm not kidding here, be careful).

You'll recall last year in January, François was in Montreal for a CFA luncheon which I covered here. At the time, I fell into Consuelo Mack's trap stating he was the "most bearish he's ever been".

I now realize this was a mistake as the truth is François isn't known as a perma bear or perma bull, he makes Risk On and Risk Off calls on markets and uses a disciplined macro framework to recommend sector positioning. That's what he's really good at.

In 2015, he told me he was bearish but at the beginning of 2016, he turned bullish ("Risk On") as "inflation had come down and there was a turn in the business". He recommended clients go overweight cyclical sectors like energy (XLE), financials (XLF), and industrials (XLI) and underweight less cyclical sectors like healthcare (XLV), consumer staples (XLP) and utilities (XLU).

In 2017, he recommended clients prepare for "Risk Off" markets and got his sector and factor level recommendations right but missed the global economic synchronicity that led to big rallies in Eurozone and Japanese stocks.

But his clients were happy because his highest conviction call was large-cap growth (XLK), which really outperformed the overall market, and healthcare (XLV) which also did well. Both these recommendations were to position for Risk Off markets.

It's confusing to those of you who think when investors buying large-cap growth stocks (like FANG stocks) means they're bullish but Risk On and Risk Off have nothing to do with bullish or bearish, but how you want to position your portfolio in terms of sectors given the risks out there.

The fact that the S&P Technology index (XLK) had a stellar year last year, up almost 40%, shows you that most investors were positioned for Risk Off markets, so don't confuse a rally in large-cap growth stocks with bullish investor sentiment.

Now, every year, François and his team publish a brutally honest review of their investment recommendations which comes out in mid-December. As he told me: "There is zero arrogance and we are extremely harsh on ourselves, maybe overly harsh, when reviewing our recommendations.”

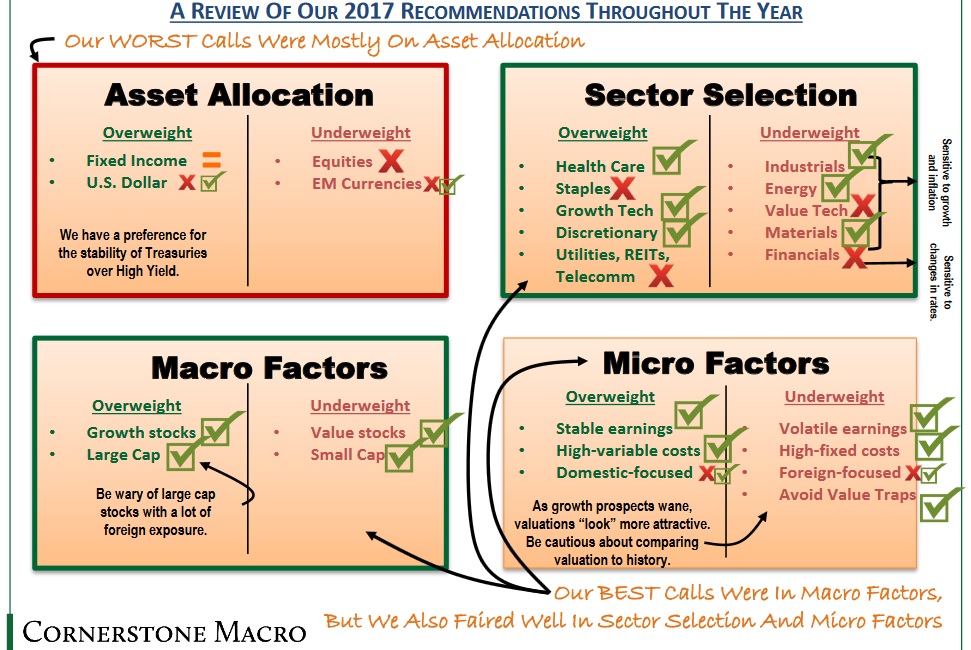

Below, I embedded a brief recap of the investment themes they discussed in this review and a summary of their 2017 investment recommendations (click on iimages):

It's important to read this full report to really understand what went right and wrong in 2017. The worst themes in 2017 were in asset allocation as they were too negative on the stock market and too bullish on the US dollar.

They were surprised by the strength in foreign data and this impacted their asset allocation calls (click on image):

But they got the macro factors (ie. size and style) right and positioned their clients early on in large-cap growth, and it's this sector positioning which their clients value the most. Their asset allocation recommendations are equally excellent but not always easy, especially in a year like 2017 when Eurozone's PMIs did very well on the back of the ECB's massive stimulus, something François openly admits he and his team underestimated.

Along with large-cap growth to capture Risk Off markets, another one of their best themes last year was to overweight stable earnings like healthcare (XLV).

Again, if you're a client, take the time to read their 2017 year-end review of their investment recommendations very carefully, it's excellent.

When looking at 2018, François and his team state the following on the intro to their outlook:

The big story of 2017 when it comes to equities was the dominance of growth. We are not only referring to the Growth Index here, albeit it performed quite well, but rather to the broader “growth” theme at large. In essence, all things associated with growth were clear winners last year. This is often seen in a world where economic prospects are beginning to, or about to, top out. If one excludes the December tax-infused pop in most PMIs, what you saw in 2017 was a broad topping process of leading indicators at very high levels. As such, the Technology sector, with 83% of its market-cap in Growth, led the market. Moreover, stock-selection factors such as long-term growth and high price-to-book generated a lot of excess performance.

The key question as we begin 2018 is whether this growth dominance can continue, and if not, what will replace it? Interestingly, the evolution of market themes in recent years and how they relate to the business cycle was actually quite textbook. The diagram above illustrates the main themes we have all experienced with a rough outline with the typical cycle. In the coming pages, and in tomorrow’s conference call, we will make the case for “stability” as the BIG story of 2018 equity leadership.

[Note: All clients should take the time to carefully go over his outlook piece and watch the conference call going over numerous key themes]

In our conversation, he told me he is going back to his more traditional indicator, the Fed funds rate inversed, advanced by 18 months as now that the Fed moved off the zero bounds, this indicator is useful once again.

[Note: In 2009, he moved away from this indicator to look at inflation. In particular, the ISM prices paid, inverted, advanced 18 months, to capture changes in monetary policy because ZIRP and QE impacted the traditional Fed funds indicator.]

There are actually four macro indicators that François uses:

- Fed funds rate

- Money supply

- Taylor rule

- Yield curve

According to him, "the yield curve remains the single greatest macro indicator in the US" which is a consumer-led economy where credit is critically important.

With the Fed raising rates and core inflation pressures rising in the US, he thinks there is a real risk of an inverted yield curve because the global PMI is topping and weakening, and this will drive long bond yields lower.

He also stated the yield curve is not a leading indicator, it's a gauge of market policy which leads other components of the Leading Economic Indicators (LEI). "As such, it belongs in the policy bucket which leads other indicators."

What this basically means is in 2018, we can expect a slowing of leading US economic indicators, even if you factor in fiscal policy, and this has implications on portfolio positioning.

- He expects a recoupling will occur in all three major economies to the path of lower pospects.

- A shift of growth to stability which means focus on healthcare (XLV), consumer staples (XLP) and utilities (XLU). Profitability will be a dominant theme in 2018.

And the chart below explains exactly which sectors they are recommending during this shift to a year of stability:

He stressed that he doesn't see any major shock in the near term and thinks growth in Europe and Japan will continue to be decent in the first half but the US yield curve will increasingly become the dominant theme of the year.

This means a slowing of leading indicators, economic data coming in below expectations, stocks will start moving down before this occurs despite the proposed tax cuts and repatriation of foreign profits.

Interestingly, he remains bullish on US long bonds (TLT) and thinks "we have yet to see secular lows on long bond yields."

This is my belief too but I told him I had a discussion with a trader I know who told me "tax cuts + infrastructure spending will lead to higher long bond rates and so will repatriation of foreign profits because it will lead to more stock buybacks and investment spending."

He responded:

I expect core inflation to accelerate ... bonds tend to be more sensitive to headline inflation which is expect to come down courtesy of lower commodity prices.On China, he says the big investment boom is over and that it's an export-led economy. "China's PMIs follow exports, so we need to watch any slowdown in its trade, especially if the US dollar starts appreciating“ (putting pressure on the renminbi and forcing another massive devaluation there which will export more disinflation/ deflation throughout the world and clobber risk assets).

Most importantly the model Roberto uses disagregates bonds into three components and inflation is only one part. The growth component is already discounting the peak of the cycle so that will only work against you, same for the term premium if PMIs in Europe start to come in. If oil starts to come down then all three parts are pressuring yields lower. It is quite possible we get lower bond yields AND a core inflation scare all the same.

[in regards to what that trader told you] In my experience traders are great at trading but understand nothing of macro. All you are saying here is that this guy is consensus and regurgitating what's in the Wall Street Journal. I have heard that story 1000 times already. Since we all know it is happening why are yields not higher? They are a discounting mechanisms so if that story were true they would already be up.

There is a big belief out there that somehow the tax plan is not fully priced into financial markets which is insane to me. I think it's typical of what you see at the top of a cycle when people are only thinking about what can go right in the world and trying to find reasons for why the good times will last. It's the opposite of early 2016 when they could only think negative with China about to have a financial crisis etc.

Time will tell.

Interestingly, on Wednesday morning, Bloomberg reported that China may halt purchases of US Treasuries, sending long bond yields higher and disrupting markets. It's obvious to me that people don't understand that China necessarily runs a current account surplus (capital account deficit) to finance the US current account deficit (capital account surplus). In other words, it's much ado about nothing!

I leave you with some important charts as we begin the new year with some of my comments (click on weekly charts to enlarge; as of Tuesday's close):

Long US long bonds: I call this the sleep well at night trade. I know, Bill Gross and Jeffrey Gundlach are warning of a potential bear market in bonds (the latter stating the key levels for investors to watch are 2.63% on the 10-year Treasury yield and 3% on the 30-year), but given the weakening in the global PMI and ever-present deflationary pressures abroad, I continue to recommend buying US long bonds (TLT) on any backup in yields/ decline in prices.

In fact, if you ask me, now is a good time to load up on US long bonds:

Given my bullish views on the US dollar (UUP), I particularly like this trade for Canadian and foreign investors.

Buy more stocks? As far as stocks, as shown below, the S&P 500 (SPY) is on a tear, led by financials (XLF), industrials (XLI) and technology (XLK):

But given my fears of global deflation, lower long bond yields, a potential inverted yield curve, I expect stocks to sell off and hit financials and industrials particularly hard. Risk Off markets will still support technology but the shift there will be toward stability (like software).

Also, with the global PMI topping out and signalling a slowdown ahead, I remain weary of cyclical sectors leveraged to global growth like metals and mining (XME), energy (XLE), emerging markets (EEM) and Chinese shares (FXI):

Importantly, if the global PMI is topping out and pointing to a global slowdown ahead, you want to be underweight or even short these sectors, especially the ones that ran up a lot since bottoming early in 2016 (I would include industrials too as they are leveraged to the global economy).

Return to stability: Since this comment is called return to stability, below are more stable sectors like healthcare (XLV), utilities (XLU), consumer staples (XLP), REITs (IYR) and telecoms (IYZ):

All these sectors offer stability, a key theme of this outlook, as they offer stable earnings and solid dividends. However, it's important to note utilities, REITs, telecoms and other dividend sectors sell off when rates rise, which is normal and a buying opportunity.

Nevertheless, buying safer stocks still carries beta risk, less so than a high-flier like biotech but stocks are stocks, so if you want to lower the volatility of your portfolio, you need to increase your allocation to US long bonds.

Speaking of biotech (XBI), it's been on a tear too, and I made a great call recommending this sector to my readers right before the US presidential election:

But biotech is super high beta and this means when it swings, it swings hard both ways. I still like this sector and think there is something structural going on but you need to stomach a lot of volatility if you buy and hold these biotech stocks (great for swing trades, but they're very risky especially when buying individual companies).

Canary in the coal mine: Lastly, the canary in the coal mine, high-yield or junk bonds (HYG), which typically move down before stocks:

So far, I don't see any imminent threat but with credit spreads at record lows and stocks at record highs, you really need to keep an eye on junk bonds.

I have shared more than enough with my readers. I want to publicly thank François Trahan and urge all my institutional readers to subscribe to the research at Cornerstone Macro and really take the time to read his team's 2018 outlook and listen to the accompanying conference call, it's well worth your time.

Again, please remember some of the charts above are copyright material of Cornerstone Macro and I have explicit permission to use them for this blog post. Anyone forwarding these charts or using them in a presentation without explicit permission from Cornerstone Macro will be prosecuted to the full extent of the law (take this warning seriously).

I hope you enjoyed reading this comment and kindly remind all my readers to please support this blog and the work that goes into it via PayPal on the top right-hand side, under my picture.

It took me a few days to put this comment together, I will not publish anything else this week, will let you digest all the information here.

Below, market optimism reaches 'potential danger' sign not seen since 1986 and Warren Buffett and Charlie Munger think things are getting bubbly out there. However, momentum tends to feed on itself, something Buffett alluded to.

In fact, Bill Miller, the legendary investor who once beat the S&P for 15 consecutive years before running into trouble, told CNBC the market can melt up 30 percent here. No doubt, there is still a lot of liquidity driving shares higher but momentum can shift abruptly so be careful chasing stocks, especially momentum stocks here.

Third, James Paulsen, The Leuthold Group chief investment strategist, and Tom Manning, F.L. Putnam Investment Management president and CEO, provide their outlook on the markets.

Paulsen thinks rising inflation will pose a risk on yields and markets but given long bond yields move with the global PMI, I wouldn't worry about a bond bear market even if US core inflation temporarily picks up (due to the lower US dollar). The global PMI is weakening and this will put pressure on US long bond yields over te next year.

Fourth, Tom McClellan, McClellan Market Report editor, gives his outlook on tech stocks and what he sees for the overall market.

Lastly, David Spika, GuideStone Capital Management, and Steve Massocca, Wedbush Equity Management, discuss how the bull run will play out in 2018 stating central bank policy going forward will prove to be a headwind for the market.

If I were the Fed, I'd be very worried of how to proceed going forward. Stay tuned, 2018 should be another interesting year! Don't panic, just prepare for a bumpier ride ahead and focus on stability.

Comments

Post a Comment