BlackRock's Canucks Shaking Up PE

BlackRock’s new private equity fund is nearing its first purchase of a company, with a chance it could do something unusual in the industry: Never sell it.This is an excellent article where two top former Canadian pension fund managers express what's the main problem with private equity funds and how they are addressing long-standing issues to get better alignment of interests with investors.

It’s sure to be a highly scrutinized deal, coming as the firm seeks billions of dollars for the pool of capital, which is designed to push the evolution of the buyout industry.

“We’re under exclusivity for one transaction right now,” says André Bourbonnais, the head of BlackRock’s long-term private capital team, known as LTPC. The fund, which aims to raise $10 billion to $12 billion, may complete the deal within weeks.

BlackRock formed the LTPC fund to hold companies for “up to forever,” structuring it with input from cornerstone investors to create a better alignment of interests than in traditional private equity, according to Mark Wiseman, chairman of BlackRock’s alternative-investment unit and global head of active equities. That means lower fees, no pressure to sell companies, and investing in multibillion-dollar deals that BlackRock considers less risky.

This step by the world’s largest asset manager may change the landscape formed by some of the oldest and most high-profile names in private equity, like KKR & Co. and the Blackstone Group.

Wiseman, who says he began sketching his idea for LTPC in late 2017, has been working with Bourbonnais over the past year to fix what the two view as an outdated leveraged-buyout model. Their previous jobs in the vaunted Canadian pension system fueled their gripes about the model, which — to the detriment of investors — hasn’t changed much over the past 35 years.

“It’s anachronistic,” says Wiseman, who started at BlackRock in 2016. “We’re trying to solve a lot of the things that drove us crazy.”

Bourbonnais, previously the chief executive officer of the Public Sector Pension Investment Board in Montreal, joined BlackRock about a year ago to lead the firm’s long-term private capital team. Before becoming CEO at PSP Investments, Bourbonnais had been at the Canada Pension Plan Investment Board, where he and Wiseman were colleagues for years.

There, private equity fees got under their collective skin.

That’s why BlackRock’s new pool scraps the 2 percent management fee traditionally charged to investors such as pensions, endowments, and foundations. Paying 2 percent of assets when the private equity industry was young made sense, according to Wiseman, because the fees were truer to purpose: covering the cost of operating a buyout firm. Today those fees are excessive, with firms profiting from multiple funds that have grown significantly over the past few decades, he says.

“It’s nonsensical,” Wiseman adds. “The funds got larger, larger, and larger, but the cost of running the firms didn’t grow proportionally.”

Managers would begin raising a third investment pool when the first and second funds were still running, meaning they were now collecting three times the cost of managing the firm, says Wiseman. Sure, the cost of running a $10 billion fund is greater than that for a $500 million pool because more people are needed to monitor it, but it’s not 20 times higher, he notes.

In his view, cutting the management fee by a small percentage doesn’t go far enough to align the interests of private equity firms and their investors. Shrinking it to 1.5 percent, for example, is a “tiny” concession when considering the massive amount of fees still being collected, Wiseman explains.

Instead, the burden will be on BlackRock to accurately project the costs of running LTPC — or risk eating a portion of them. “You better be good at budgeting,” he says.

The firm will provide its clients with a transparent budget to approve annually, according to Wiseman. “If more than the budget is spent, the excess cost is to BlackRock,” he says. And should expenses fall under budget, investors still benefit because they’re paying an explicit percentage over the cost of managing it, Wiseman says.

Under the traditional fee structure — the so-called 2-and-20 model — a private equity firm pockets a 2 percent management fee and also takes a 20 percent cut of the profit from its deals.

“The 2-and-20 model is broken,” says Christopher Ailman, chief investment officer of California State Teachers’ Retirement System, which oversaw $234 billion of assets at the end of April. “It is just far too expensive.”

A long tail of management fees throws off the alignment of interests. “When you’re on fund nine, the idea of paying you a 2 percent management fee to run your operation” is tough to take, Ailman notes. “You should be living on your carry.”

The structure traditionally used by private equity firms creates a fee spread of about 400 basis points to 700 basis points, according to Bourbonnais. “That’s why they need to underwrite to a 20-plus return for their deals: to deliver a mid-to-high-teens return on a net basis to the investor,” he says.

BlackRock is willing to charge much less — 150 basis points — because the $10 billion to $12 billion targeted by LTPC will put it in a good position to make a profit despite the lower fees. “Because it’s permanent capital and it scales, the rewards in dollar terms to us as a manager are tremendous, even at 150 basis points,” says Wiseman.

Ailman, who has been in conversation with BlackRock about LTPC, likes that the giant asset manager has gone much further than buyout firms in aligning with the interests of investors. “It’s a game changer,” he says.

The question now becomes: Will BlackRock once again succeed in shaking up the asset management industry it has come to dominate with more than $6 trillion of assets?

It’s not like investors never expressed a desire for longer holding periods in private equity to save money, says Ailman, CIO of CalSTRS in Sacramento, California, since 2000. He previously worked in institutional investment management for more than 27 years.

“A lot of us have been clamoring for a long time for a longer holding period and more what I like to call ‘private capital’ structure,” notes Ailman. “You’re starting to see a few of those, but they’re coming out of the traditional private equity shops and they look a lot like the traditional partnerships, which we think are ineffective.”

That’s why he says he was excited to see BlackRock step into private equity with an innovative structure that addresses the long-term interests of institutional investors.

Most buyout funds have holding periods of less than seven years, says Ailman, which is not ideal for CalSTRS’s 30-year investment horizon. When firms exit their deals, the money returned to the pension has to be put back to work — again and again and again.

Traditional partnerships between private equity firms and their investors may seem long-term based on a fund’s life cycle, but in reality they’re not. “The partnerships last for 14 to 15 years, sure, but the actual investment in a company, and the growth, is short,” says Ailman.

Rather than own a good asset for decades, Wiseman says, private equity managers are incentivized to exit companies within a relatively short time frame to “crystallize their carry” and post higher internal rates of return. The constant selling of companies amounts to “massive frictional costs” for investors in buyout funds, he says.

It can be worse. It’s not uncommon for private equity firms to sell companies to each other as a way to cash out. The problem is that the same investor may be in both the fund that’s selling the business and the fund that’s buying it.

“Now I own the same thing I owned before, except I’ve paid a whole bunch of transaction costs and 20 percent carry to end up in the same position,” says Wiseman. “As the investor, why don’t I just hold it? Why does it have to pass from hand to hand to hand to hand?”

Each sale involves millions of dollars in dealmaking fees being paid to bankers, lawyers, and accountants, according to Wiseman, who notes that “all of that is coming out of the pockets of the underlying investors because they’re realizing a lower net return on their transaction.”

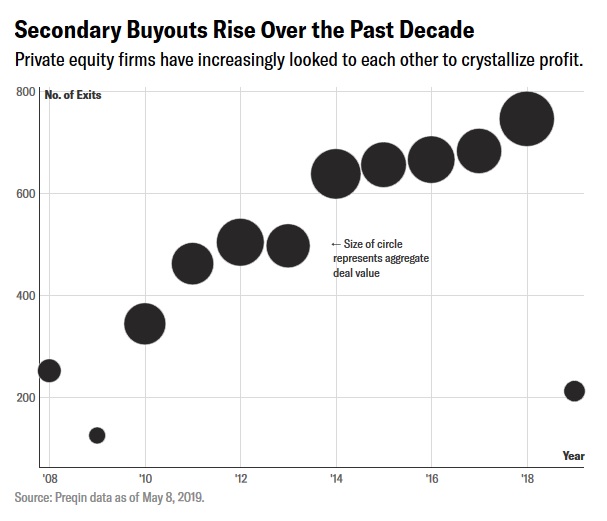

Secondary buyouts have climbed globally in number and volume, reaching the highest levels in more than a decade, according to alternative-assets data provider Preqin, which began tracking such data in 2008. Although recycling assets within the buyout industry pays off for the private equity firm cashing out, the CIOs of pension funds, for example, would rather avoid it.

“It’s terrible for a long-term investor,” says Wiseman. “If I have a good asset, I want to hold it forever.”

Preqin tracked 746 secondary buyouts last year totaling $128 billion globally, with the volume swelling 50 percent from 2017. The average holding period for buyout funds is about five years, according to the data provider.

BlackRock’s LTPC fund expects to hold ten to 15 companies initially, says Wiseman. “We’ll sell the company if someone is willing to pay us more than we think is fair value for it, but otherwise we’ll hold it and keep clicking along.”

The fund will invest in companies with long track records and resilience through economic cycles “so we can forecast the future a little bit better,” according to Bourbonnais. “We’ll stay away from things that we believe can be disrupted,” as well as commodity-related deals and new technologies.

The LTPC team is looking at companies with an enterprise value of $5 billion to $7 billion, says Bourbonnais, and will typically invest $500 million to $1.5 billion from the fund. There’s potential to write larger checks with the help of co-investors. “With our partners we can probably put in two to three billion,” he says.

BlackRock expects its deals to be less risky than many LBOs, partly because of the amount of leverage it plans to use. Deals will be financed with debt levels of about 4 times a company’s earnings — less risky than many buyout deals stacked with debt equaling 6 times earnings, says Bourbonnais.

“We’re going to use leverage for growth purposes, and not to juice up the returns,” he adds, explaining that debt-funded dividends are not part of LTPC’s strategy. For a “transformational acquisition” BlackRock may bring leverage to 5 to 5.5 times, he says. “But then we will want to go back to our 4 times leverage.”

The for-now-anonymous business that BlackRock is getting ready to purchase wants to avoid excessive leverage and changing ownership anytime soon.

“It wasn’t a big auction,” says Wiseman. The founder of the business, which is private equity–owned, picked BlackRock in a “reduced” sales process.

“He doesn’t want to go on the private equity treadmill again because he doesn’t want to be levered 6-plus times,” says Wiseman. “He doesn’t want to have to find another partner in five years” or be tied to an “aggressive acquisition plan” designed to meet a private equity firm’s 20 percent return target.

LTPC’s investment strategy falls between those of traditional LBO funds and Warren Buffett’s Berkshire Hathaway, according to Bourbonnais, who leads a team of about 17 people. “We are going to buy very good companies with very good management,” he says. “For us cost-cutting is not a growth strategy.”

BlackRock intends to pursue less risky deals for lower gross returns than private equity offers, but on a net basis the difference in gains will be similar because LTPC is cheaper for investors. Wiseman projects that its new fund can produce net returns of about 15 percent while reining in risk-taking.

Looking across CalSTRS’s portfolio, Ailman, who seeks a steady 7 percent over 30 years, expects LTPC’s gains to land between those of public stocks and traditional private equity.

“We’re already a huge investor into traditional private equity,” he says. “If we can find a new opportunity in this private capital area where you buy and hold, I think that would look attractive to our asset allocation.”

There’ll be no pressure for BlackRock to sell companies, partly because the fund is unitized.

“We don’t have to exit our underlying companies in order for investors to gain liquidity,” which is an important aspect of the fund’s structure, explains Wiseman. “It’s a permanent capital vehicle. If an individual investor wants liquidity, the investor can sell its units in the vehicle.”

The units help keep BlackRock’s performance incentives in line with investors’ interests.

Unlike in traditional private equity, BlackRock’s team won’t be incentivized to exit deals in order to get paid. “Here, we never cash out,” says Wiseman. “We’re paid our incentive in units,” with performance based on the net asset value of the companies held by LTPC. It’s in everyone’s interest to see the value of the units climb, he notes.

With fundraising still underway, BlackRock is seeing strong interest in LTPC globally, though the novelty of the structure may slow the pace a bit as investors take time to understand it, according to Bourbonnais. The firm has already attracted $2.75 billion of commitments from its cornerstone investors, including pension and sovereign wealth funds, whose input helped design LTPC.

“We went out to investors with this as an idea,” says Wiseman. “We said, ‘Here’s a concept paper. Would you like to spend some time sitting down with us and help us build it?’”

Ailman likes that a giant asset manager — finally — is approaching investors with a structure that’s far more than a step away from how things have been done in private equity for decades.

“I’m glad to see new entrants come into the market,” he says. “I hope to see more.”

Mark Wiseman is right, 2&20 makes sense for young funds looking to cover operating costs, not private equity and hedge fund goliaths that are gathering billions in assets.

In private equity, there is clear misalignment of interests with long-term investors. Go back to read my comment on Peloton's differentiated approach where Mike Murray told me the typical private equity fund has a three to five year holding period which isn't always optimal for investors and the management teams of the underlying companies:

"PE funds are often forced to sell winners. At Teachers', we would often see a buyout fund hold an underlying company for three years, make 3X their money, sell it to another buyout fund which holds it for another three years, makes 3X their money, etc. This introduces a tremendous amount of friction costs to investors and distracts management of the underlying company. Our approach eliminates friction costs and extends compounding to generate superior long-term results."Friction/ transaction costs add up and it drives investors nuts when PE funds keep selling winners to other PE funds and they don't reap the long-term gains.

For private companies, BlackRock's LTPC makes great sense too as it's not based on the traditional buyout model.

Anyway, it's clear Mark Wiseman and André Bourbonnais are trying to disrupt the traditional private equity model. Whether or not they succeed remains to be seen but they have some big investors interested in their platform.

Both CalPERs and CalSTRS are looking to reduce fees so I'm not surprised they are both showing interest. CalPERS recently committed $1.15 billion to two private equity funds but its CIO, Ben Meng, said he will wait for Greg Ruiz to assume his postion as the Head of Private Equity this summer before committing to the direct-style private equity program.

Ruiz will be in charge of a $27 billion program, the largest in the US, and he will need to ramp up co-investments and look to get better alignment of interests with all of CalPERS's PE managers. He will have a lot of work ahead of him and I'm sure he's already aware of BlackRock's LTPC.

For pensions and other institutional investors, the only way forward in private equity is by reducing fees, either through more co-investments or by investing in long-term funds which offer a long investment horizon and better fee structure, all while delivering great returns.

Below, BlackRock’s Senior Managing Director, Global Head of Active Equities, and Chairman of BlackRock Alternative Investors Mark Wiseman sits down with Bloomberg’s Erik Schatzker at the Bloomberg Invest Summit in New York to discuss the importance of long-term capital.

Comments

Post a Comment