Barbara Shecter of the Financial Post reports Quebec pension giant Caisse takes $33.6 billion investment hit in worst markets in 50 years:

The

Caisse de dépôt et placement du Québec posted a negative return of 7.9

per cent for the first six months of the year, in what chief executive

Charles Emond noted was the worst period for stock and bond markets over

the past 50 years.

As of June 30, the Caisse had net assets of

$392 billion, with the $28.2-billion decrease due to investment losses

of $33.6 billion offset by $5.4 billion in net deposits. The losses

included a full write off of the fund’s US$150 million investment in

crypto lender Celsius Network LLC, which is now in Chapter 11 bankruptcy

proceedings in the United States.

“The first six months of the

year were very challenging,” Emond said in a statement. “The mix of

factors we faced had not been witnessed in several decades: spiking

inflation that triggered rapid and sharp interest rate hikes, rare

simultaneous corrections in both stock and bond markets, fears of an

economic downturn and the war in Ukraine with its many collateral

effects.”

Over the same period, the Ontario Teachers’ Pension Plan Board reported a positive return of 1.2 per cent on Monday.

During

a news conference Wednesday to discuss the Caisse results, Emond said

the Quebec pension fund wrote off the Celsius crypto investment even

though it is considering its legal options and intends to preserve its

rights in the court-monitored U.S. bankruptcy proceedings.

“We decided to take it now” out of prudence, Emond said of the writeoff. “The last chapter hasn’t been written.”

He said his team conducted extensive due diligence with outside experts

and consultants. They were aware of management and regulatory issues at

Celsius and underestimated the time it would take to resolve them, he

said, adding the Caisse was keen on “seizing the potential of block

chain technology” and perhaps the investment in Celsius had been made

“too soon” in the company’s development.

He noted that the investment was a very small part of a large venture

portfolio that has produced 35 per cent returns over the past five

years.

“In these disruptive technologies, there’s ups and downs…. Some big winners and many losers,” Emond said.

Although

the Caisse posted an overall return in negative territory for the first

six months of the year, the performance exceeded that of its benchmark

portfolio — which posted a negative return of 10.5 per cent.

Over five and 10 years, annualized returns were 6.1 per cent and 8.3

per cent respectively, also outpacing benchmark portfolio returns,” the

pension manager noted.

Emond said the Caisse is managing

the “turbulence” with a combination of asset diversification and

strategic adjustments made since the COVID-19 pandemic began.

“For

the past two years, we’ve been working in an environment of extremes

characterized by particularly fast and pronounced changes. These unusual

and unstable conditions will persist for some time,” he said.

“In the short term, we’ll be watching what central banks do to contain inflation and how that impacts the economy.”

During the first six months of the year, negative returns in equities

and fixed income were partially offset by gains in the Caisse’s

investments in real assets including infrastructure and real estate.

The

pension giant posted a negative return of 13.1 per cent in fixed

income, which beat the negative 15.1 per cent return for its benchmark

portfolio. This represented nearly $3 billion in “value added”

attributable to all credit activities, the Caisse said.

A negative return of 16 per cent in equities beat the negative 17.2 per cent return in the benchmark portfolio.

The

Caisse’s real estate and infrastructure portfolios, meanwhile,

generated a 7.9 per cent six-month return, “demonstrating their

diversifying role which contributes to limiting inflation’s impact on

the total portfolio.”

The real asset class performance also beat the benchmark portfolio’s return, which was 2.4 per cent.

“So that asset class played its role. The two portfolios are doing well,” Emond said.

He

said it is challenging to compare the short-term performance of

Canadian pension funds because they have e different mandates and

investment models. The Ontario Teachers’ Pension Plan, for example, has

less exposure to equity markets than the Caisse and more exposure to

natural resources and commodities, which performed well in the first

half of the year.

Clémence Pavic of Le Devoir also reports on CDPQ's net $28 billion loss for the first half of the year (translated from French):

Affected by the simultaneous correction of the stock and bond markets, the Caisse de dépôt et placement du Québec (CDPQ) posted a negative overall return of 7.9% for the first six months of 2022.

In total, the Caisse de dépôt's net assets now stand at $392 billion, a drop of $28.2 billion. "We never rejoice in a negative return, but we did better than the market," said CDPQ President and CEO Charles Emond in a press briefing.

For the first half of the year, la Caisse performed better than its benchmark portfolio, which fell by 10.5%. Its five-year and ten-year annualized returns, at 6.1% and 8.3% respectively, are also higher than this index.

The current unstable context “is a difficult situation for many people,” acknowledged Mr. Emond. “Not only is everything more expensive, but people are also seeing their savings drop,” he said. The CEO. of the CDPQ wanted to reassure Quebecers: “Their pensions are absolutely not at risk”.

He also recalled that the figures presented on Wednesday stop at the end of June, just before the rebound that the markets experienced in July. “If we took the photo today, a month and a few later, the portrait would be markedly different. In fact, we would have 15 billion more in our assets, which is about half of the decline of the first six months,” he pointed out.

However, the good performance in July is no guarantee for the coming months, he agrees, and the rest of the year is still likely to be “extremely difficult”.

Differentiated results

Shares of listed companies were the asset class that suffered the most during the first six months of the year (-16.0%). “Investors had to navigate through the worst half of the last 50 years,” reminded Mr. Emond.

In an exceptional context of simultaneous correction of the stock and bond markets, the Caisse de dépôt also recorded a drop in yield in fixed income for the first half of the year (-13.1%).

On the real asset side, however, the real estate and infrastructure portfolios posted positive returns (10.2% and 5.8% respectively), “a sign that they are playing their role of diversification well by limiting the "impact of inflation on the overall portfolio", we detail in the Caisse's press release.

Moreover, even if oil assets have been increasing sharply for several months, boosted by robust energy demand and tight supply, the CEO. of the CDPQ says he has "no" regrets about the institution's complete exit from the oil sector.

"I would not like there to be an impression in the population that there have been losses [by selling our oil assets]", affirmed Mr. Emond, in reaction to an article in La Presse which amounted to nearly a billion dollars the money that the CDPQ could have collected if it had waited longer before disposing of the majority of these titles. “We sold at a profit,” he insisted, explaining that there was no perfect time to do so.

“We got six billion dollars of return, over a period of two to three years, in renewable energies and two billion dollars with natural gas, which is a transition energy source”, also underlined Mr. Emond to justify the strategy of the Quebec institution.

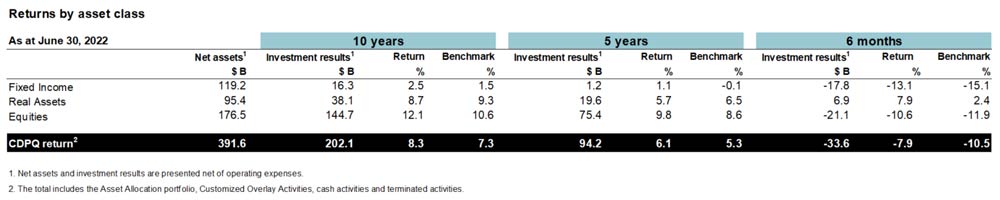

CDPQ put out a press release on its mid-year results stating it posted -7.9% six-month return and 6.1% five-year return, outperforming its benchmark portfolio over all periods:

CDPQ today presented an update of its results as at June30,2022. In the worst six-month period of the last 50years

for stock and bond markets, CDPQ generated an average return of -7.9%,

significantly above its benchmark portfolio’s return of -10.5%. Over

five and ten years, annualized returns were 6.1% and 8.3% respectively,

also outpacing benchmark portfolio returns. Net assets were $392billion.

“The first six months of the year were very challenging. The mix of

factors we faced had not been witnessed in several decades: spiking

inflation that triggered rapid and sharp interest rate hikes, rare

simultaneous corrections in both stock and bond markets, fears of an

economic downturn and the war in Ukraine with its many collateral

effects,” said Charles Emond, President and Chief Executive Officer of CDPQ.

“Despite this turbulence, CDPQ’s portfolio continued to clearly

outperform its benchmark portfolio due to the strategy’s evolution since

the pandemic started, sound asset diversification and the quality of

execution by ourteams.”

“For the past two years, we’ve been working in an environment of

extremes characterized by particularly fast and pronounced changes.

These unusual and unstable conditions will persist for some time. In the

short term, we’ll be watching what central banks do to contain

inflation and how that impacts the economy. Our portfolio continues to

be robust, and we remain disciplined in order to perform well in

different market conditions,” concluded CharlesEmond.

Return highlights andachievements

The $28.2-billion decrease in net assets is due to investment results of -$33.6billion and $5.4billion in netdeposits.

Each CDPQ depositor has its own investment horizon and tolerance for

risk. As such, their results vary based on their investment policies. As

at June30,2022,

the returns of CDPQ’s eight largest depositors ranged from -7.0% to

-9.9% for six months. Their annualized returns ranged from 4.6% to 6.9%

over five years and 6.8% to 9.4% over tenyears.

Fixed Income: Historic rate hikes impacted returns, but credit activities generate value added

Several events—including the reopening of the economy, the war in

Ukraine, supply chain challenges and the labour shortage—prompted an

upsurge in inflation that is lasting longer than expected, driving

central banks to raise rates sharply. In this context, the first half of

the year saw bond markets turn in their worst performance since the

1920s. Over six months, CDPQ posted a -13.1% return in Fixed Income,

compared to -15.1% for its benchmark portfolio, representing nearly $3billion

in value added attributable to all credit activities. Over five years,

the asset class recorded an annualized 1.1% return, higher than its

benchmark portfolio’s -0.1% return, and generated nearly $7billion in value added. All credit activities contributed to this performance, especially Real Estate Debt and Corporate Credit.

Private credit investments and commitments continued in the first half of2022, amounting to $8.5billion. Of note, in Infrastructure Financing, the team invested $190million

in Everstream Solutions, a fibre-optics telecommunications company

serving businesses based in the United States, to fund the expansion of

its network in the country. In Corporate Credit, up to $150million

in financing was provided to Duca Financial Services Credit Union Ltd.,

an Ontario-based financial cooperative. Through subsidiary Otéra

Capital, a USD360-million loan was also granted for the construction of over 500residences in Santa Clara, in the United States, a priority country for our real estate debt strategy.

Real Assets: The Real Estate and Infrastructure portfolios perform amid rising inflation

Real Assets, a class that includes the Real Estate and Infrastructure

portfolios, generated a 7.9% six-month return, demonstrating their

diversifying role which contributes to limiting inflation’s impact on

the total portfolio. The asset class’s return was significantly higher

than its benchmark portfolio’s return of 2.4%. With a five-year

annualized return of 5.7%, the gap with its benchmark portfolio, which

had a 6.5% return, continues to gradually narrow. The asset class is

driven by the excellent performance of Infrastructure assets and the

logistics real estate segment, but continues to be limited by the

pandemic’s impact on shopping centres and office buildings.

Real Estate

The Real Estate portfolio recorded a 10.2% return in the first six

months, driven by its repositioning over the last two years, compared

with 11.4% for its benchmark portfolio. Over five years, the annualized

return was 2.9%, below the benchmark portfolio’s 6.7%, which is in part

due to the portfolio’s historically high weighting in shopping centres.

This weighting of 22%, representing the largest sector in the portfolio

in January2020, has now been reduced to the smallest, at12%.

In the first half of the year, Ivanhoé Cambridge’s teams executed around 40transactions aligned with strategic priorities totalling $9.2billion.

For example, CDPQ’s real estate subsidiary increased its exposure to

logistics, including through a green digital infrastructure partnership

of USD1billion

with Bain Capital and Lodha, the leading real estate developer in India.

In the United States, Ivanhoé Cambridge benefited from its successful

partnership with Lendlease in Boston to start development of 60Guest

Street and launch a new life sciences joint venture that will provide

ultramodern laboratories, offices and production facilities with an

initial investment of USD 500million. The

real estate subsidiary also created a new partnership with Stockland in

Australia to develop the M_Park campus dedicated to life sciences and

technology. Ivanhoé Cambridge will hold 49% of this net-zeroproject.

Infrastructure

The Infrastructure portfolio generated a 5.8% return over six months,

beating its benchmark portfolio’s -5.5%. Over five years, it posted a

9.6% return, well above the 6.3% of its benchmark portfolio, which

represents $6.5billion in value added. This

performance stems from a careful selection of assets, diligent

post-investment asset management and good sectoral diversification,

including in renewable energy, telecommunications and transportation.

Included in the latter are ports and the passenger transportation

industry, which is beginning to recover from the severe impact of

pandemic-induced confinement measures around theworld.

In the first six months, the Infrastructure team was disciplined in executing transactions, with nearly $7billion

in new investments and commitments. For example, CDPQ secured,

alongside its long-term partner Invenergy and a group of investors, a

lease for an offshore wind farm in the New York Bight auction, with the

winning bid of USD645million.

CDPQ also formalized the project to merge Eurostar, of which it already

owned shares, and Thalys, making the new company the largest player in

sustainable high-speed mobility in Western Europe. CDPQ invested USD2.5billion in port infrastructure in the United Arab Emirates with DP World, with which it launched a global investment platform in2016. This infrastructure is strategically positioned to benefit from global trade routes and supply chains.

Equities: A return above the indexes in an exceptionally difficult

environment for Equity Markets; a quality portfolio in the right sectors

in Private Equity

The Equities asset class, which includes the Equity Markets and

Private Equity portfolios, generated a six-month return of -10.6%, above

its benchmark portfolio of -11.9%. Over five years, this asset class’s

annualized return was 9.8%, compared with 8.6% for the benchmark

portfolio. That represents $10billion in value added stemming from the superior performance of the quality companies in PrivateEquity.

Equity Markets

Inflationary pressure, surging interest rates and fears of a

pronounced economic downturn have resulted in a severe correction in

global stock markets during the first six months of the year. The

flagship S&P 500 Index, which has lost nearly 20% from the start of2022, its worst six-month period since1970,

is a good representation of this. In these difficult conditions, the

Equity Markets portfolio recorded a six-month return of-16.0%, above its

benchmark portfolio’s -17.2%. Over five years, the portfolio produced

an annualized return of 5.5%, below its benchmark portfolio, which stood

at 6.0%. The difference is largely due to the portfolio’s significant

underexposure to certain technology giants throughout most of theperiod.

Private Equity

The bearish environment during the first six months also weighed on

the private equity market. For six months, the portfolio’s return was

-2.4%, above the -4.1% return of its benchmark portfolio. Over five

years, the portfolio produced an annualized return of 17.6%,

outperforming its benchmark portfolio, which stood at 12.4%. This

positive difference is the result of good sectoral allocation, including

investments in health care, insurance and technology, combined with the

quality of asset management, which is a core element of the investment

approach. In an uncertain environment, the team also successfully

continued providing customized support to portfolio companies on their

strategies, acquisitions andoperations.

Québec: Strategic transactions to support even more Québec companies in the first half of theyear

The first six months were active for CDPQ in Québec, with some thirty

investments and commitments, including transactions stemming directly

from Ambition ME, a suite of financing solutions and support services to

help Québec mid-market companies grow. One example is the investment in

Bouthillette Parizeau, an engineering firm with numerous projects that

provide solutions to fight climate change. CDPQ also invested in

Laval-based COREALIS Pharma, a company that has become the leader in its

sector in NorthAmerica.

Also of note is the investment in Innocap for the acquisition of

HedgeMark, a BNY Mellon company, thereby creating the world’s largest

alternative investment platform. The first half of the year also saw

CDPQ acquire, alongside equal partner Fonds de solidarité FTQ, a 65%

stake in Bonduelle Americas Long Life, which specializes in the

processing and marketing of vegetables, thereby keeping the company’s

headquarters inBrossard.

A key step was achieved for the Réseau express métropolitain (REM),

with the electrification of the South Shore branch, representing the

16-kilometre section between Montréal and Brossard. More recently, the

REM began conducting test runs, with cars crossing the Samuel-De

Champlain Bridge, a major project milestone. For the next phase, PMM,

the consortium responsible for operating and maintaining the network for

the next 30years, will take over to conduct the tests and trials required forcommissioning.

Lastly, Ivanhoé Cambridge and its partners invested close to $200million

in Haleco, a unique project at the intersection of Old Montréal and

Griffintown, which stands out for its mixed-use approach (residential,

commercial and offices) and will include community housing to create a

quality neighbourhood catering to residents’ needs. The project also

plans to obtain LEED Platinum certification and incorporates a

low-energy design. Ivanhoé Cambridge also rolled out initiatives

supporting downtown Montréal’s economic recovery and dynamism, including

unveiling The Ring at the Esplanade PVM, and the launch of Nouveau

Centre, an unparalleled offering of summer experiences in the heart of

thecity.

Financial reporting

In conducting its activities, CDPQ incurs operating expenses, external management fees and transaction costs. As at June30,2022, these annualized costs were estimated at 52cents per $100 of average net assets, compared with 57cents per $100 of average net assets in2021. CDPQ’s cost ratio compares favourably with that of itspeers.

In addition, CDPQ is rated investment-grade with a stable outlook by

the credit rating agencies, namely AAA (DBRS), AAA (S&P), Aaa

(Moody’s) and AAA(Fitch).

ABOUT CDPQ

At CDPQ, we invest constructively to generate sustainable returns

over the long term. As a global investment group managing funds for

public pension and insurance plans, we work alongside our partners to

build enterprises that drive performance and progress. We are active in

the major financial markets, private equity, infrastructure, real estate

and private debt. As at June30,2022, CDPQ’s net assets totalled CAD392billion. For more information, visit cdpq.com, follow us on Twitter or consult our Facebook or LinkedIn pages.

Let me begin by stating these results are not surprising given the challenging markets in the first half of the year. As stated in the press release, the returns of CDPQ’s eight largest depositors ranged from -7.0% to

-9.9% for six months depending on their risk tolerance.

The CPP Fund experienced a loss of roughly 7% in the first six months of this calendar year (I don't have precise figures, just estimating based on public figures), which makes sense given the significant selloff in global bond and stock markets during that time.

Still, nothing changes in terms of my thoughts and analysis Just like CDPQ, CPP Investments is extremely well diversified globally and has more equity exposure than other large pension funds which helps explain the loss. However, the loss would have been a lot worse had it not been for its active management strategy and global diversification.

Both funds are similar but you can't compare them directly because they have different clients, liquidity profiles (CDPQ is more mature), asset class weights and mandates but they are both delivering meaningful added value over their reference portfolios over the long run and this is what ultimately counts for their contributors and beneficiaries.

As one senior pension manager told me earlier: "The key thing to understand is these portfolios are acting as they should by design, so it shouldn't be surprising to see losses when you have bonds and stocks selling off strongly during a period where inflation hit a multi-decade high."

Discussion with Charles Emond, President and CEO of CDPQ

Yesterday, I had a chance to talk to Charles Emond, CDPQ's President and CEO.

Charles was kind enough to call me after I reached out and I want to thank him for taking the time to speak with me.

I told Charles that I am not a big fan of quarterly or mid-year results because pensions have a long investment horizon.

He told me it's all about "reassuring people" and he also told me since CDPQ and others issue bonds and are rated by credit agencies, they need to disclose information at least twice a year.

Charles began by stating some key messages he wanted to relay:

First, this is the worst first half of the year in 50 years for equity and bond markets which went down anywhere between 10-30%. So we are at -7.9%, we beat the market and our benchmark is at -10.5%. That's an important differential and what I was telling journalists is the average retail investor with a 60/40 stock/bond portfolio experienced losses of 15% during the first half of the year.

The second point is the six-month window is a very small window. We have been in a series of extreme market conditions for the past few years. The market goes up with tech and then the market went down and the only thing that went up is oil, rates go down to historic lows in a matter of weeks during the onset of the pandemic, then they go up quickly as inflation hits a 40-year high, then there is a war, the pandemic, etc. So as a theme, I am asking myself whether our strategy is working during this crisis of extremes?

And as a proof of that, the first six months we were down $30 billion and I told people since June 30th, 40 days later, we recovered half of that so don't freak out too much on taking a snapshot of the market as of now because market volatility will be with us for quite a while, get used to it and buckle up.

As a CEO, I am watching and talking to my depositors and Board and discussing whether the strategies in place are working. As you know, there have been some changes, we repositioned the real estate portfolio, we implemented changes in public equities, so how have we done during the last two years during this multi crises period?

I want to reassure people that pensions are safe. I told journalists, look at the last two years during this turbulent period, we had an annualized return of 7.3%, our assets are up $60 billion and that's twice better than our benchmark at 3.6%.

The goal is to build a portfolio that goes up more than the market and resists better when the market goes down. And it's important, there is value outperfomance, it's not just theoretical, we need absolute returns, we can't pick the environment, and if we had just followed our benchmark, the assets wouldn't be at $392 billion, they'd be at $364 billion, so it actually matters because you can rebound better and that's what happened in July.

I try to tell people to have some perspective. The assets went up $100 billion over the last two years, we lost $30 billion and are still up $60 billion (net) and our returns are there over a 5 and 10-year period.

And it's important because there was a trauma at the Caisse in 2008. It's completely the opposite now. The 60/40 portfolio was down 15% in the second hald of 2008 but the Caisse lost 24% back then during that time and now we lost 7.9% and are much larger ($120 billion to $400 billion). We are significanltly above our benchmark and it was quite the opposite the last time around.

I am trying to tell people not to get distracted by dollar figures, it's just a point of time and has nothing to do with the past which was a completely different environment.

I understand, these are big figures, so it was a matter of reassuring people and hopefully we accomplished that to a certain extent.

I completely agree, CDPQ now has noting to do with CDPQ in 2008, it's a much bigger and better run organization which is a lot better diversified across asset classes, sectors, strategies, geographies and there is a relentless focus on risk-adjusted returns.

It doesn't mean the organization can't experience a loss, it obviously will, but over the long run, it will add significant value over its reference portfolio and the proof is in the pudding.

I'm not one to talk about what others are doing right or wrong, I have enough on my plate. As you know, Teachers' manages assets and liabilities so inflation matters more to them. They are a more mature plan. I told the journalist they have about 10% in public equities so obviously they didn't experience the downturn of the first six months of 2022 and they also have 15% in commodities and natural resources which performed great during this time. We have none and these two positions benefited them during this time.

The point is the following. We have different scope of mandates, different responsibilities, different levels of maturities, different levels of leverage, different number of depositors (with different risk tolerance), so I am always telling journalists, be careful because we all look the same but we are quite different and there are reasons why certain comparative studies are being taken and why others are not.

Personally, I hate when people compare pensions because they are not able to compare them properly starting by understanding their assets in relation to their liabilities and how it influences their asset mix and risk tolerance.

Again, OTPP is delivering on its mandate, performing exceptionally well, but it's not right to make direct comparisons with CDPQ and others for all sorts of reasons.

The other thing I noted with Charles is CDPQ provides a lot more details in its semi-annual update than other large Canadian pensions.

He agreed, told me they have detailed performance by asset classes and provide details relative to their benchmarks and have a big press review."This is another reason why it's tough to compare performances between pensions until they release their annual results."

We then briefly chatted about the whole Celsius fallout and Charles told me he got a lot of questions by journalists and reiterated some of the same points with me.

First, nobody is happy with this outcome at the risk of stating the obvious. But I told journalists this morning a few things. First, this is an exception in our venture capital portfolio. Our VC portfolio is high performing, delivering 35-40% returns over the last 5 years and we are very cautious. The loss rate in the industry due to external forces lasts several years and is in the vicinity of 40-50%. Ours is 10% so we are play this very cautiously.

Now, on Celsius, there have been a couple of lessons learned. Obviously we came in too early. The sector is in transition from a regulatory standpoint and the company was in hyper growth. It's a company that grew to a billion in revenues in a few years but it weakened itself financially just before there was some of the risk off in markets. We brought in a very experienced management team which included the former CFO at RBC (Rod Bolger) and people from Morgan Stanley's risk department but with the crisis unfolding so fast, it all happened too quickly for the new management team to execute the value creation plan they had in mind.

Our intentions were good, we are not the only institutional player in the space. BlackRock made announcements, as did some pensions and around 20 banks have all showed interest. What we were aiming for isn't the crypto, it's the potential on the blockchain and we actually also wanted to help on the regulation of the sector which we feel is important. But I think we underestimated the length of time and order of magnitude of the obstacles to get through that. We had a plan and ran out of time. The reality as I told the media is I have to restrain my comments as we want to preserve our right to recourse as we might be considering legal options.

I told Charles I don't want to focus too much on Celsius as it's such a grossly insignificant part of the total portfolio and writing off this investment will not make a difference to overall results.

He agreed but added: "It's important that we learned some lessons and if we make mistakes, they are not fatal."

Now, in terms of what went right, Real Assets came in nicely as Real Estate and Infrastructure together generated 7.9%, outperforming the benchmark of 2.4%:

In Real Estate we are continuing to reposition the portfolio. We were at -15% in 2020, +12% last year, +10.2% in the first half, a little bit below its index but it's because the index is lagging and includes a bit of 2021. Real assets did their job in an inflationary environment. Inflation is a negative but some assets react well to it contractually.

I think Ivanhoe Cambridge and CDPQ's Infrastructure team are doing an excellent job as are all the investment departments at CDPQ.

Lastly, I asked Charles if he sees tough times ahead:

Yes, absolutely, we have the foundations to get through it. The last two years' performance proves it because if we had to do a stress test to go over what we went through the last 24 months, I would have laughed at my team almost. But we are very cautious on markets here. Inflation concerns were the story the first half. Now we may move into economic slowdown concerns and it will be important to see how central banks land all that, so we remain cautious despite the positive upward move in the market over the past month and half. At the same time, if we move towards a slowdown or recession, we will start seeing some assets react the way we are used to, that is the bond mix will recover where equities will struggle a little bit depending on what's priced in whereas in the first six months, there was no place to hide, there was a rare and simultaneous correction in both bonds and equities and that impacted the overall portfolio. We feel pretty good about the overall portfolio but I feel there is a good 12 months of turbulence ahead of us. For the market and economy finding its balance after the big Covid trade, there is an unwinding all of that and we are trying to see where we land in all of these scenarios.

I thank Charles for getting back to me on short notice and graciously providing me with so many great insights.

Below, a Radio-Canada Zone Économie interview with Charles Emond which took place yesterday (in French). He addresses a lot of concerns, including exiting oil & gas and their investment in Celsius head on. He also touches on other issues including the REM and exporting CDPQ Infra's model to other places.

But the most important point he makes is that CDPQ's strategy is working over the last two years of extremes and the portfolio is a lot more resilient now and in better shape to confront any turbulence ahead.

I can't state this point enough times, I have zero concerns about CDPQ and CPP Investments experiencing losses during the first six months of the calendar year and think way too much media attention is being placed on way too short a time frame from a pension perspective.

Comments

Post a Comment