CPP Investments' CEO Discusses Fiscal Year 2022 Results

Barbara Shecter of the National Post reports the Canada Pension Plan fund tops half trillion after posting 6.8% return:

The Canada Pension Plan Investment Board crossed the half-trillion threshold in its most recent fiscal year, reaching $539-billion as of March 31.

The net return for the year was 6.8 per cent on last year’s $497-billion, with $8-billion of the $42-billion increase coming in the form of net transfers from the Canada Pension Plan.

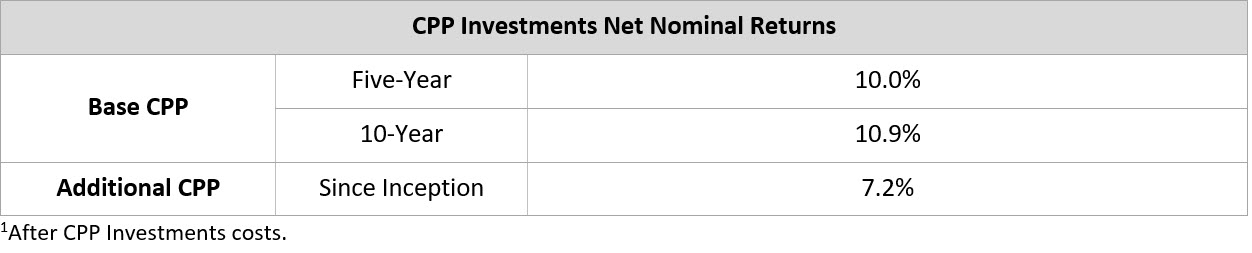

The CPP fund’s five-year return is 10 per cent, with the 10-year return coming in at 10.8 per cent.

“CPP Investments delivered solid returns in fiscal 2022 despite turbulent market conditions in the wake of Russia’s war on Ukraine, supply chain disruptions caused by the pandemic and rising inflation,” said John Graham, the pension management organization’s chief executive.

“Our 10-year performance of nearly 11 per cent, the same as it stood at the end of the last fiscal year, demonstrates the enduring growth of the (CPP) Fund over the long haul … with steady resilience during uncertain times.”

Private equity, infrastructure, real estate and credit investments were the predominant contributors to the Fund’s overall performance in fiscal 2022.

The pension giant said returns in the first nine months of the year were muted by “volatility affecting public equities during the final quarter, at levels not seen since the outset of the pandemic.”

For reference, CPPIB noted that the fund’s return in the 12 months of 2021, rather than the fiscal year that bled into 2022, was 13.8 per cent.

Bond prices also declined at a pace not seen in more than 40 years during the fourth quarter.

In addition, several factors led to a $4-billion currency loss during the fiscal year that hit returns, including the appreciation of the Canadian dollar against the U.S. dollar and other major currencies, influenced by rising commodity prices and the impact of evolving monetary and fiscal policies across global economies.

“Looking ahead, we confront uncertain business and investment conditions with higher inflation expectations, potentially worsening supply chain interruptions, tepid global economic growth estimates and international reactions to the war in Europe, all against the backdrop of a persistent global pandemic and climate change,” said Graham.

However, he said the pension management organization’s diversification strategy and market breadth, combined with local presence and a global brand, put it in “a position of strength” moving forward.

Layan Odeh of Bloomberg News also reports China's stock market muted CPP Investments' returns:

Canada Pension Plan Investment Board said the selloff in stock markets, particularly in China, muted its annual returns.

The fund’s emerging-market holdings posted a loss “predominately driven by investments in China where public equity markets were negatively impacted by unanticipated regulatory reforms and a resurgence of COVID-19 cases,” according to a statement Thursday.

Turmoil in global markets during the last quarter exacerbated the pressure.

“The volatility affecting public equities during the final quarter, at levels not seen since the outset of the pandemic, muted returns achieved through the first nine months of the fiscal year,” the firm said. Investments in public equities returned 1.3 per cent in the fiscal year ended March 31.

CPPIB earned 6.8 per cent in fiscal 2022, pushing net assets to $539 billion (US$420.4 billion).

China’s stock market took a hit last year amid a government clamp down on technology firms, tightening regulations on real estate sector and a resurgence of Covid-19 cases. But since the beginning of 2022, global equities have been battered as well, by inflation, stricter monetary policy and the war in Ukraine. Shanghai’s stock exchange plunged more than 15 per cent this year, while the S&P 500 has dropped 17.7 per cent and Canada’s benchmark stock index is down 5.3 per cent.

The decline in bond prices -- the fastest drop in more than 40 years -- also hurt returns, the fund said. CPPIB’s calendar-year return in 2021 was 13.8 per cent.

CPPIB’s private equity investments returned 18.6 per cent, driven by improved portfolio company earnings and outlooks in the information technology, financial and health care sectors in the U.S. and in Europe.

The pension plan continued to go deeper into private deals with acquisitions including cybersecurity company McAfee and Chinese mattress company AI Dream. CPPIB has teamed up with homebuilder Lennar Corp. to construct apartment buildings in the US.

Today, CPP Investments announced its results for fiscal 2022.

Late this afternoon, I had a chance to talk to John Graham, CPP Investments' CEO, to go over the results and more.

I will get to that conversation below but I'd like to first cover the results properly.

CPP Investments put out a press release earlier today stating its net assets total $539 billion at 2022 fiscal year-end (added emphasis is mine):

Highlights:

- Net return of 6.8%

- Five-year net return of 10.0%

- 10-year net return of 10.8%

- Net assets increase by $42 billion for fiscal year

- One-year dollar value-added of $10 billion or 2.1% above the Reference Portfolios

TORONTO, ON (May 19, 2022): Canada Pension Plan Investment Board (CPP Investments) ended its fiscal year on March 31, 2022, with net assets of $539 billion, compared to $497 billion at the end of fiscal 2021. The $42 billion increase in net assets consisted of $34 billion in net income and $8 billion in net transfers from the Canada Pension Plan (CPP).

The Fund, which includes the combination of the base CPP and additional CPP accounts, achieved a net return of 6.8% for the fiscal year, and five-year and 10-year annualized net returns of 10.0% and 10.8%, respectively.

In managing the Fund in the best interests of contributors and beneficiaries, CPP Investments continues to build a portfolio designed to achieve a maximum rate of return, without undue risk of loss, while considering the factors that may affect the funding of the CPP and its ability to pay current benefits. Since the CPP is designed to serve multiple generations of beneficiaries, evaluating the performance of CPP Investments over extended periods is more suitable than single years.

In the five-year period up to and including fiscal 2022, CPP Investments has contributed $199 billion in cumulative net income to the Fund. Since its inception in 1999, CPP Investments has contributed $378 billion to the Fund on a net basis.

“CPP Investments delivered solid returns in fiscal 2022 despite turbulent market conditions in the wake of Russia’s war on Ukraine, supply chain disruptions caused by the pandemic and rising inflation,” said John Graham, President & CEO. “Our 10-year performance of nearly 11%, the same as it stood at the end of the last fiscal year, demonstrates the enduring growth of the Fund over the long haul on the one hand, with steady resilience during uncertain times, on the other.”

Private equity, infrastructure, real estate and credit investments were the predominant contributors to the Fund’s overall performance in fiscal 2022. The volatility affecting public equities during the final quarter, at levels not seen since the outset of the pandemic, muted returns achieved through the first nine months of the fiscal year. Bond prices also declined in the fourth quarter at a pace unseen in more than 40 years. For reference, CPP Investments’ calendar-year return for 2021 was 13.8%.

“We move forward from a position of strength, focusing on our sound diversification strategy and a disciplined outlook beyond current events. Our confidence is grounded in the robust CPP Investments platform, designed for resiliency, with mature programs at scale, market breadth and local presence, amply supported by an admired global brand. Our purpose-driven people are dedicated – with a demonstrable track record of investment performance and operational excellence – to helping current and future beneficiaries achieve retirement security,” added Graham.

The appreciation of the Canadian dollar against the U.S. dollar and other major currencies during the year, influenced by rising commodity prices and the impact of evolving monetary and fiscal policies across global economies, negatively impacted investment returns with a foreign currency loss of $4 billion.

“Looking ahead, we confront uncertain business and investment conditions with higher inflation expectations, potentially worsening supply chain interruptions, tepid global economic growth estimates and international reactions to the war in Europe, all against the backdrop of a persistent global pandemic and climate change,” concluded Graham.

Performance of the Base and Additional CPP Accounts

The base CPP account ended the fiscal year on March 31, 2022, with net assets of $527 billion, compared to $491 billion at the end of fiscal 2021. The $36 billion increase in net assets consisted of $34 billion in net income and $2 billion in net transfers from the CPP. The base CPP account achieved a 6.9% net return for the fiscal year and a five-year annualized net return of 10.0%.

The additional CPP account ended the fiscal year on March 31, 2022, with net assets of $12 billion, compared to $6 billion at the end of fiscal 2021. The more than $6 billion increase in net assets consisted of $147 million in net income and $6 billion in net transfers from CPP. The additional CPP account achieved a 2.8% net return for the fiscal year, and an annualized net return of 7.2% since its inception in 2019.

The additional CPP was designed with a different legislative funding profile and contribution rate compared to the base CPP. Given the differences in their design, the additional CPP has had a different market risk target and investment profile since its inception in 2019. The performance of the additional CPP differs from that of the base CPP. Furthermore, due to the differences in their net contribution profiles, the assets in the additional CPP account are also expected to grow at a much faster rate than those in the base CPP account.

Fund Five- and 10-Year Returns1

(for the year ended March 31, 2022)

Long-Term Sustainability

Every three years, the Office of the Chief Actuary of Canada (OCA) conducts an independent review on the sustainability of the CPP over the next 75 years. In the most recent triennial review published in December 2019, the Chief Actuary reaffirmed that, as at December 31, 2018, both the base and additional CPP continue to be sustainable over the 75-year projection period at the legislated contribution rates.

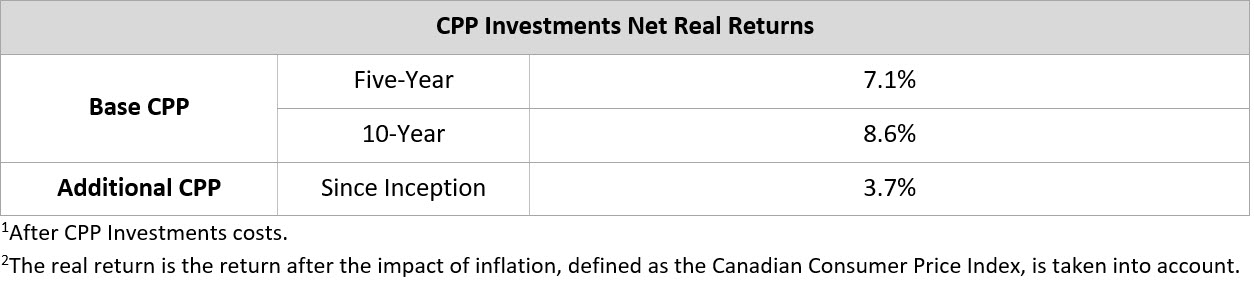

The Chief Actuary’s projections assume that, over the 75 years following 2018, the base CPP account will earn an average annual rate of return of 3.95% above the rate of Canadian consumer price inflation. The corresponding assumption is that the additional CPP account will earn an average annual real rate of return of 3.38%.

Fund Five- and 10-Year Real Returns1, 2

(for the year ended March 31, 2022)

Our Key Sources of Returns

Contributions made to the CPP not needed to pay current benefits are transferred to CPP Investments. To help the CPP remain sustainable, we seek to grow assets by achieving returns commensurate with prudent levels of risk. Risk appetite is one of the most important decisions made by CPP Investments. Just as excessive risk could adversely affect the safety and soundness of the CPP, so could being too cautious. We represent the minimum required level of market risk as a simple two-asset portfolio of global public equities and Canadian government bonds for both the base CPP and additional CPP. This serves as our starting point against which we evaluate the incremental impact of our biggest investment decisions. Importantly, CPP Investments goes beyond this minimum, pursuant to its legislative objectives, by seeking to achieve a maximum rate of return while taking a prudent level of risk. The decisions we have made in accordance with our legislated mandate are to:

- Target a higher level of market risk than the minimum required as represented by our Reference Portfolios;

- Use leverage to construct a more diversified portfolio at our targeted level of market risk; and

- Pursue investment selection and seek returns above and beyond what can be obtained from investing in a public market index.

These represent our key sources of returns because, depending on the level of market risk we choose to target or how we choose to diversify the Fund, the outcomes of these decisions have the most material impact on the overall performance of the Fund. We evaluate the successive impact of these decisions primarily over a five-year period, in line with the long-term nature of our mandate to maximize returns without undue risk of loss.

Over the last five years, the simple two-asset portfolio representing the minimum level of market risk assumed to maintain plan sustainability generated an annualized net nominal return of 6.1%, resulting from the strong performance of global public equities. Targeting a higher level of market risk, pursuant to our legislative objectives, helped add an incremental annualized return of 3.1%, driven by the higher level of global public equity content in our Reference Portfolios for both the base and additional CPP.

Our decision to use leverage to further diversify the Fund incrementally detracted an estimated annualized return of 1.9% from the Fund over the last five years. The Fund’s more diversified portfolio did not keep pace with the returns of the Reference Portfolios, which are more heavily weighted in global public equities. While our decision to diversify into a broader range of asset classes may have detracted value relative to the Reference Portfolios over the past five years, we continue to believe diversification will add value over a longer-term period and provide resiliency during market downturns.

Our decision to pursue investment selection added an annualized 2.7% of additional value over the past five years. The value gained or lost through investment selection is measured against comparable risk-adjusted passive public market benchmarks to enable an objective evaluation of the contributions of each active strategy to Fund performance.

Overall, the Fund’s performance relative to the Reference Portfolios can be measured in both percentage terms or dollar terms, which we refer to as percentage value-added and dollar value-added, respectively. On a relative basis, the Fund delivered a percentage value-added of 2.1% or a dollar value-added of $10 billion this fiscal year. Over the past five years, the Fund generated an overall net value-added of 0.8% or $10 billion.

While not all key sources of return may yield positive results in every period, we believe our comparative advantages support our ability to generate value with a long-term focus. Our investment performance to date supports our belief that pursuing additional sources of returns can increase returns over the long term. Seeking to maximize returns without undue risk of loss from all sources collectively allows us to do our part in contributing to the long-term sustainability of the CPP.

For further information on our Key Sources of Returns, please refer to page 20 of the CPP Investments Fiscal 2022 Annual Report.

Asset and Geography Mix

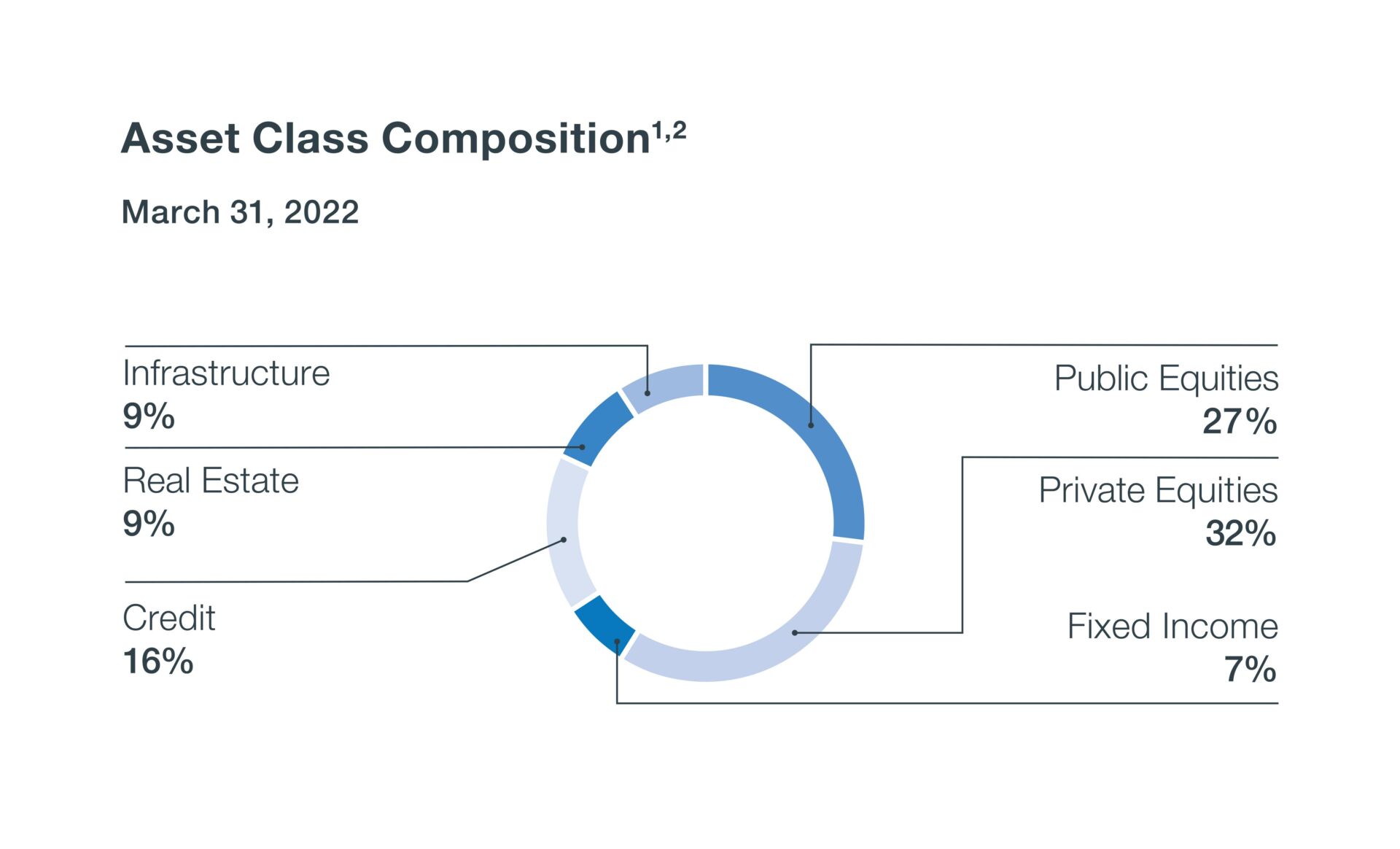

CPP Investments, inclusive of both the base CPP and additional CPP Investment Portfolios, is diversified across asset classes and geographies:

1Fixed income consists of cash and cash equivalents, money market securities and government bonds, net of debt financing liabilities. Public Equities include absolute return strategies and related investment liabilities.

2As at March 31, 2022, $49 billion of real estate, $48 billion of infrastructure and $26 billion of our private equity investments associated with sustainable energies, which collectively represented 23% of net assets, are managed by the Real Assets investment department.Performance by Asset Class and Geography

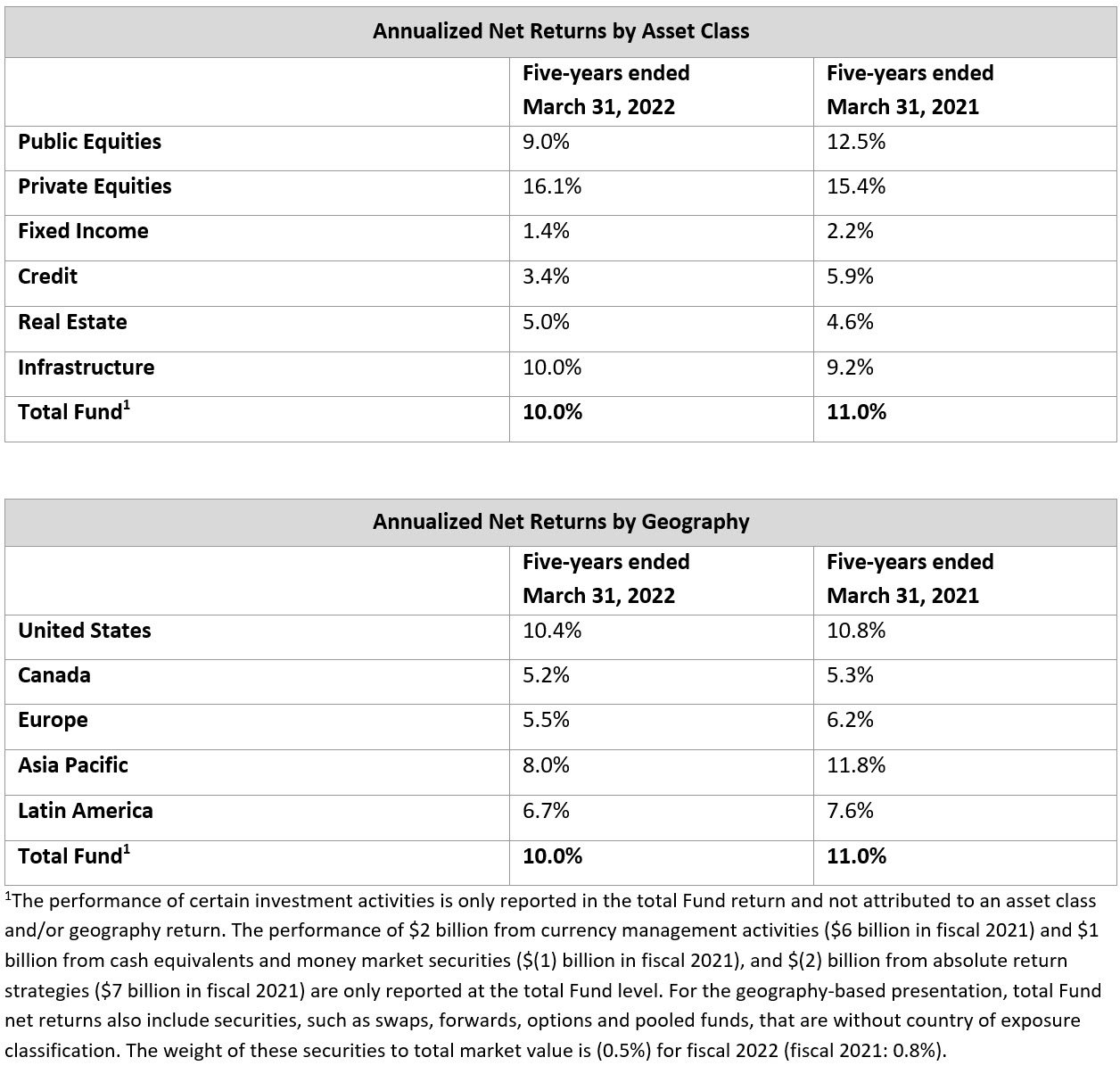

Five-year Fund returns by asset class and geography are reported in the tables below. A more detailed breakdown of performance by investment department is included on page 54 of the Fiscal 2022 Annual Report.

Managing CPP Investments Costs

We treat cost management as a tenet of our public accountability as we seek to build an internationally competitive investment platform to maximize long-term returns. While total costs are down compared to the previous year, operating expenses increased by $106 million due to an increase in full-time globally positioned talent, higher incentive compensation, in line with better year-over-year long-term Fund performance, and continued investments in building our technology and data infrastructure. Our operating expense ratio of 27.1 basis points (bps) declined from 29.3 bps the previous year and is also below our five-year average of 29.1 bps. Management fees decreased by $125 million, due to the recognition of management fees last fiscal year which were subject to deferred payment arrangements. Performance fees increased by $98 million driven by strong realizations in our private equity portfolio. Transaction-related expenses, which increased by $172 million, vary from year to year according to the number, size and complexity of our investing activities. Other categories affecting our total cost profile include taxes and expenses associated with various forms of leverage. Page 33 of the Fiscal 2022 Annual Report provides a discussion of how we manage our costs. For a complete overview of the CPP Investments combined cost profile, including year-over-year comparisons, refer to page 52.

Operational Highlights for the Year

Executive announcements

- Announced the following Senior Management Team appointments:

- Maximilian Biagosch as Senior Managing Director, Head of Europe & Direct Private Equity;

- Suyi Kim as Senior Managing Director & Global Head of Private Equity;

- Deborah Orida as our first Chief Sustainability Officer. Ms. Orida also continues to serve as our Senior Managing Director & Head of Real Assets;

- Agus Tandiono as Senior Managing Director, Head of Asia Pacific & Active Equities Asia; and

- Subsequent to the fiscal year end, Priti Singh was appointed Senior Managing Director & Global Head of Capital Markets and Factor Investing, effective May 2, 2022.

Board appointments

- We welcomed the appointment of Barry Perry to the Board of Directors. Appointed in August 2021, Mr. Perry was formerly President and CEO at Fortis Inc., and is a widely respected executive with deep experience in the utilities sector.

- We welcomed the appointment of Dean Connor to the Board of Directors. Appointed in August 2021, Mr. Connor served for a decade as President and CEO of Sun Life Financial and has been recognized in Canada and internationally as an outstanding business leader.

Strategic developments

- Announced that our portfolio and operations commit to be net zero of greenhouse gas emissions across all scopes by 2050. Our commitment includes: continuing to invest and exert our influence in the whole economy transition as active investors, rather than through blanket divestment; achieving carbon neutrality for our internal operations by the end of fiscal 2023; expanding our investments in green and transition assets from $67 billion to at least $130 billion by 2030; and building on our new decarbonization investment approach.

- Updated our Proxy Voting Principles and Guidelines to elevate expectations for board diversity and annual director elections among portfolio companies. The changes extend the 30% threshold for board gender diversity to new countries and signal future ambitions for emerging markets. We will also consider voting against all directors up for election where the board is classified and there are oversight failures related to climate change, board gender diversity or deficient corporate governance.

- Created Sustainable Energies, which combines the organization’s expertise in renewables, conventional energy and new technology and service solutions into a single investment group, positioning us as a leading global energy investor.

Bond issuance

- In fiscal 2022, CPP Investments continued its leadership role in the global transition to the new reference rates through its U.S. Dollar (USD) issuance platform, with a 3-year USD secured overnight financing rate (SOFR) benchmark totalling US$1.4 billion – the largest 3-year SOFR benchmark by any sovereign, supranational or agency issuer to date. Debt issuance gives CPP Investments flexibility to fund investments that may not match our contribution cycle. Net proceeds from the issuances will be used by CPP Investments for general corporate purposes.

- With our continued commitment to sustainable investing, CPP Investments grew its green bond presence in the Australian-dollar market with a benchmark 7-year green bond valued at A$750 million. The total issuance of green bonds since inception of the program is now C$6.2 billion. Green bonds enable CPP Investments to invest further in eligible assets such as renewables, water and green real estate projects, and to diversify the investor base.

Investment Highlights for the Year

Active Equities

- Invested an additional US$50 million in the US$1.6 billion Series H funding of Databricks, a data, analytics and AI company based in San Francisco, bringing our stake to 0.3%. We previously invested US$65 million in the company’s US$1 billion Series G funding in February 2021.

- Invested US$350 million in Advanced Drainage Systems, a leading provider of water management solutions for use in the construction and agriculture marketplace, increasing our ownership stake in the company to 4.6%.

- Invested C$200 million as an anchor investor in the IPO of Volvo Cars, a front-runner in the global shift to electric vehicles, representing a 0.9% ownership stake.

- Invested US$25 million for a 0.75% ownership stake in ITM Power, a U.K.-based manufacturer of electrolyzer systems based on proton exchange membrane technology that generates green hydrogen for energy storage, transport, renewable heat and industrial sectors.

- Invested an additional €362 million in a rights offering by Cellnex Telecom S.A., a leading mobile-tower owner and operator based in Spain, holding total ownership in the company of approximately 5.2%.

- Invested US$800 million in The Flipkart Group, one of India’s leading digital commerce entities, which includes group companies Flipkart, Myntra, Flipkart Wholesale, Flipkart Health+ and Cleartrip. The group is also a majority shareholder in PhonePe, a leading digital payments and financial services app in India.

- Invested US$150 million in the National Stock Exchange of India, the leading equity and derivatives exchange in India.

Credit Investments

- Committed US$150 million to Cypress Creek Renewables’ US$450 million debt facility to refinance existing debt and fund the growth of the company’s robust solar and storage project pipeline. Cypress Creek Renewables is one of the largest independent vertically integrated solar and storage developers in the U.S.

- Committed US$220 million in a senior secured financing facility for the development of utility-scale solar projects in the U.S. through a partnership with HPS Investment Partners, a leading global investment firm.

- Closed on a US$421 million whole loan to Spear Street Capital, a U.S.-based owner and operator of office properties in Canada, the U.S. and Europe, for the redevelopment of an existing office complex into a life science development in Watertown, Massachusetts.

- Committed to provide up to US$500 million in financing to Prodigy Finance, a provider of postgraduate student loans for international students attending top schools.

- Invested US$325 million in the unitranche loan for Straive, a business process outsourcing company focused on the education, data and publishing verticals, with operations primarily in India and the Philippines.

- Committed C$112 million to an investment in the first lien term loan of BAPE Hong Kong Limited, a Hong Kong-based streetwear apparel company that designs, sources and retails the BAPE and AAPE brands.

Private Equity

- Supported the combination of Inmarsat, a leading provider of mobile satellite services, with global communications company Viasat, as part of a four-party consortium in a transaction valued at approximately US$4 billion. The consortium will hold a 37.5% ownership in the combined entity, and we will hold 9.4%. Our initial stake in Inmarsat was acquired in 2019.

- Committed to an investment in FNZ, the global wealth management platform, alongside Motive Partners, in one of the largest-ever primary equity raises in the wealth management sector. The fundraising values FNZ at over US$20 billion and CPP Investments committed a total of US$1.1 billion. Subsequent to our fiscal year end, US$200 million was syndicated to other investors.

- Entered into a definitive agreement to acquire all outstanding common shares of McAfee, a global leader in online protection for consumers, alongside an investor group comprising Advent, Permira, Crosspoint Capital, GIC and ADIA, in an all-cash transaction valued at approximately US$14 billion on an enterprise value basis.

- Invested US$23 million alongside Genesis Capital for an approximate 3.5% stake in Bluepha, a leading synthetic biology company in China engaged in the development and production of PHA, a type of biodegradable plastic.

- Committed C$303 million to BGH Capital Fund II. BGH Capital is an Australia- and New Zealand-focused private equity manager active in the mid-to-large cap buyout space.

- Committed US$325 million to Anchor Equity Partners Fund IV, a Korean mid-market private equity firm focused on control-oriented consolidation investments and significant minority growth-stage opportunities.

- Invested US$120 million into Eruditus, an Indian Education Technology company that partners with top-tier universities worldwide to deliver online courses and other programs to a global learner base, resulting in a 3.8% stake in the company.

- Committed US$600 million to the Baring Asia Private Equity Fund VIII, L.P. Baring Private Equity Asia is a pan-Asian private equity investment firm focusing on control buyouts and minority growth investments.

Real Assets

- Formed a US$979 million joint venture with Lennar Multifamily Communities, a leader in apartment development and management, to develop Class-A multifamily residential communities across high-growth metropolitan areas in the U.S. We hold a 96% stake in the joint venture.

- Invested more than US$3 billion to acquire a 100% ownership interest in Ports America, North America’s largest independent marine terminal operator with diversified operations, including 70 locations in 33 ports on each of the United States’ three coasts.

- Invested US$10 million in Project Canary’s Series B institutional fundraising. Project Canary is a Denver-based emissions tracking business that provides real-time methane emissions monitoring and independent ESG certification for oil and gas well sites.

- Formed a US$1.1 billion joint venture with Bridge Industrial, a vertically integrated real estate operating company and investment manager, to develop industrial properties in several core markets across the United States. We own a 95% stake in the joint venture.

- Committed US$20 million to a partnership with Conservation International, an organization that works to protect the critical benefits that nature provides to people, to invest in nature-based climate solutions.

- Announced a C$340 million investment in partnership with Votorantim S.A. to support the asset consolidation and public listing of several Brazilian energy assets through two independent transactions to create Auren, one of Brazil’s largest energy producers and traders. We own an approximate 32% equity interest in Auren.

- Committed to an investment of C$380 million in Brazilian water and wastewater company Iguá Saneamento S.A., in which we hold a 46.7% aggregate equity stake, to support the privatization of water and sewage services from CEDAE, Rio de Janeiro’s state water and sanitation utility.

- Announced a strategic partnership with U.K.-based Octopus Energy Group (Octopus), a global clean energy technology pioneer, including a US$300 million investment for a 6% stake to support Octopus’ global expansion and to support its Kraken technology platform to deploy smart energy across the full energy supply chain, increasing Octopus Energy Group’s valuation to approximately US$5 billion.

- Formed two joint ventures with Greystar Real Estate Partners, a global leader in the investment, development and management of high-quality real estate. Allocated an initial US$1.2 billion in equity to form a joint venture to pursue life science development opportunities in target markets in the United States, starting with the acquisition of 74M, a project located in Somerville, Massachusetts, where we will own a 90% stake. Also formed a joint venture to develop and acquire purpose-built single-family rental communities in the United States, allocating approximately US$840 million in equity, where we own a 95% stake.

- Invested in three GLP vehicles. GLP is a global investment manager and business builder in logistics, real estate, infrastructure, finance and related technologies. We committed US$210 million for a 39.6% interest in the GLP Brazil Development Partners II fund to develop nine logistics parks in São Paulo submarkets experiencing high demand for modern logistics facilities. We committed €900 million of equity to GLP Continental Europe Development Partners I (GLP CDP I), representing a 45% share to develop modern logistics assets, expanding GLP CPD I into a truly pan-European vehicle. We committed C$1.3 billion to the newly established GLP Japan Development Partners IV, our fourth modern logistics partnership in Japan with GLP.

- Established two new joint ventures, with a 50% ownership stake in each, alongside Lendlease, an international real estate group. Formed a joint venture dedicated to the development of a new office-led neighbourhood at International Quarter London, initially committing to developing the Turing Building with an allocation of £215 million. We also formed a joint venture in a dedicated Italian real estate alternative investment fund pursuing the development of Phase 1 of the Milano Innovation District, investing approximately €200 million of equity.

- Established a new joint venture with Round Hill Capital, a global real estate investor, developer and manager, to invest in the purpose-built student accommodation sector across continental Europe. Our initial equity allocation will be €475 million for a 95% interest.

- Committed C$2.1 billion to BAI Communications (BAI), a global communications infrastructure provider, to support BAI’s global growth strategy, including the acquisition of Mobilitie, one of the largest privately held wireless telecommunications infrastructure companies in the U.S. We have been a majority shareholder in BAI since 2009 with an approximate 86% ownership stake.

- Entered into a joint venture with CSI Properties, a Hong Kong listed property developer, to redevelop a mixed-use real estate project comprising residential and commercial spaces in Kowloon, Hong Kong with an equity commitment of C$169 million for a 48% stake.

- Allocated approximately C$400 million in equity to our new Japanese Data Centre Development venture with Mitsui & Co. Ltd., one of Japan’s largest general trading and investment companies, for hyper-scale data centre developments in Japan.

- Entered into two joint ventures with RMZ Corp, one of India’s largest privately-owned real estate owners, investors and developers. Formed a joint venture to develop and hold commercial office space in Chennai and Hyderabad, India, with a US$210 million equity allocation for a 50% ownership interest. Committed C$449 million for an up to 80% stake in a second joint venture to support the development and acquisition of commercial projects across India, starting with StarTech, a 1.37 million-square-foot Grade A office building located in Koramangala, Bangalore.

Disposition highlights for the year

- Sold our 31.6% stake in Puget Holdings for net proceeds of approximately US$2.7 billion. The company’s operating subsidiary, Puget Sound Energy, is the oldest and largest electric and natural gas utility in Washington State, serving approximately 1.2 million electric customers and 900,000 natural gas customers. Our ownership interest was initially acquired in 2007.

- Closed the sale of Royal Bank Plaza in Toronto, Ontario alongside our joint venture partner Oxford Properties, with net proceeds of approximately C$300 million to CPP Investments. The joint venture initially acquired the property in 2005.

- Sold our 85% stake in Buildings 1, 2 and 3 of the Henday Industrial Park in Edmonton, Alberta. Net proceeds from the sale were C$80 million. Our ownership interest in the site was initially acquired in 2014 and we continue to hold a stake in the remaining development site.

- Agreed to sell our 15-18% stake in six Raffles City real estate projects in China. Net proceeds from the sale will be approximately C$800 million before closing adjustments. Our initial investment in the first Raffles City China development, majority owned and managed by CapitaLand, was made in 2008.

- Sold our 40% interest in Avalon North Point and Avalon North Point Lofts, two multifamily real estate assets in Cambridge, Massachusetts. Net proceeds from the sale were US$128 million. We acquired Avalon North Point in 2011 and Avalon North Point Lofts in 2012.

- Sold our 2.9% stake in SBI Life Insurance Company in India. Net proceeds from the sale were approximately C$562 million. We initially invested in the company in 2017.

- Sold our stake in Velvet Energy, a privately held light-oil Montney producer with operations in north-west Alberta. Net proceeds from the sale were C$183 million. We initially invested in Velvet Energy in 2017.

- Exited our 37% interest in AMP Capital Retail Trust (ACRT) alongside other ACRT unitholders at a transaction value of C$2 billion. AMP Capital (rebranded to Collimate Capital) is an Australia-based global investment manager and we initially invested in ACRT in 2012.

Transaction highlights following the quarter

- Committed to an investment of US$25 million in Hydrostor, a long-duration energy storage solution provider, to support the Toronto-based company’s development and operation of storage facilities globally.

- Announced a new joint venture with TATA Realty and Infrastructure Limited to develop and own commercial office space across India. The total aggregate equity value of the joint venture will be C$866 million, with CPP Investments’ equity commitment at C$438 million.

- Closed a US$375 million capital investment in The Amherst Group, a vertically integrated real estate platform in the single-family residential industry, to support a share buyback and loan repayment.

- Invested US$425 million for a 13.8% stake in VerSe Innovation Private Limited, one of the fastest growing local language artificial intelligence-driven content platforms in India.

About CPP Investments

Canada Pension Plan Investment Board (CPP Investments™) is a professional investment management organization that manages the Fund in the best interest of the 21 million contributors and beneficiaries of the Canada Pension Plan. In order to build diversified portfolios of assets, investments are made around the world in public equities, private equities, real estate, infrastructure and fixed income. Headquartered in Toronto, with offices in Hong Kong, London, Luxembourg, Mumbai, New York City, San Francisco, São Paulo and Sydney, CPP Investments is governed and managed independently of the Canada Pension Plan and at arm’s length from governments. At March 31, 2022, the Fund totalled $539 billion. For more information, please visit www.cppinvestments.com or follow us on LinkedIn, Facebook or Twitter.

As you can read, the people working at CPP Investments were extremely busy in fiscal 2022.

The critical points I want to make on fiscal 2022 results are the following:

- First, for a multi-generation fund, long-term performance is what ultimately counts. In fiscal 2021, CPP Investments gained a record 20.4%. In fiscal 2022, CPP Investments gained 6.8%. The 5-year annualized net return is 10% which is excellent. More importantly, in both fiscal 2021 and 2022, the 10-year annualized net return remains at 10.8%.

- The Canada Pension Plan is sustainable over the long run. The 10-year annualized net real return of the base CPP account is 8.6%, well above the 3.95% annualized real rate the Chief Actuary of Canada projected in 2018 is required for the Canada Pension Plan to be sustainable over the next 75 years. For the additional CPP account, the annualized net real return since inception (2019) is 3.7%, above the required annualized real rate of return of 3.38% to keep it sustainable over the long run.

- The world has dramatically changed since other pensions reported on a calendar year basis in 2021. Russia's invasion of Ukraine exacerbated inflation pressures forcing the Fed and other central banks to start raising rates. As stocks and bonds rise and fall in tandem this year, calls to rethink the popular asset-allocation strategy known as the 60/40 portfolio — a mix of 60% stocks and 40% bonds — are growing. Q1 2022 didn't help the CPP Fund this year just like Q1 2021 did help it. Still, CPP Investments’ calendar-year return for 2021 was 13.8%, which is in line with the performance its large Canadian peers reported for the same period. Again, it's important to stop comparing the performance among large Canadian pensions (they are similar but not the same) and start looking at long-term performance and sustainability of the plans.

- CPP Investments' active management is working and producing solid long-term gains. Overall, the Fund’s performance relative to the Reference Portfolios can

be measured in both percentage terms or dollar terms, which they refer to

as percentage value-added and dollar value-added, respectively. On a

relative basis, the Fund delivered a percentage value-added of 2.1% or a

dollar value-added of $10 billion this fiscal year. Over the past five

years, the Fund generated an overall net value-added of 0.8% or $10

billion. Since inception of the active management strategy back in 2006, the Fund has generated billions of dollar value-added over its passive Reference Portfolio with a lot less volatility.

- The Fund is well diversified across strategies and geographies. CPP Investments is a global fund investing all over the world. The bulk of its assets are in the US (36%) and Asia Pacific (26%), Europe and Canada each account for 16% and Latin America the rest (6%). In terms of asset classes, Private Equities now account for 32% of total assets (the highest allocation to PE among Canadian and US large pension funds), Credit represents 16% of total assets (again, highest allocation among peers) and Infrastructure and Real Estate each make up 9% of total assets (in line with its large peers).

- Leverage and liquidity are important to total fund management over the long run. The decision to use leverage to further diversify the Fund incrementally detracted an estimated annualized return of 1.9% from the Fund over the last five years. The Fund’s more diversified portfolio did not keep pace with the returns of the Reference Portfolios, which are more heavily weighted in global public equities. While their decision to diversify into a broader range of asset classes may have detracted value relative to the Reference Portfolios over the past five years, they continue to believe diversification will add value over a longer-term period and provide resiliency during market downturns.

- Currency losses can happen on any given year but are not a factor over long run. The appreciation of the Canadian dollar against the US dollar and other major currencies during the year, influenced by rising commodity prices and the impact of evolving monetary and fiscal policies across global economies, negatively impacted investment returns with a foreign currency loss of $4 billion. It's important to note that CPP Investments doesn't hedge currency risk which effectively means it's more bullish on the US dollar over the long run where most of its assets reside. Also worth noting, there is a cost to hedging currency risk, it takes collateral away from the balance sheet and that impacts the use of leverage and the diversification program. While we can argue about whether CPP Investments can better mitigate currency risk, if the focus is on the long-term, it's immaterial to the Fund's long-term performance.

Those are the key points I want to bring to your attention on fiscal 2022 results.

It's critically important to understand the Fund is designed to capture global growth while also demonstrating resilience during periods of market uncertainty.

This is why the Fund does well over the long run because it won't suffer the same downside risks as traditional stock and bond portfolios as it is much better diversified across public and private markets all over the world.

Now, please take the time to read CPP Investments' fiscal 2022 Annual Report which is available here.

This annual report is a little over 130 pages and it is packed with a lot of great information.

I've said this before and I'll say it again, CPP Investments is the largest and most important public pension fund in Canada and it takes transparency and accountability very seriously.

Everything you need to know about the Fund's operations is contained in this annual report.

It took me an hour this morning to skim through it and it flows well and is very well written.

Let me provide you with the table of contents which will help you navigate this annual report better:

At a minimum, I urge you to read Dr. Heather Munroe-Blum's (the Chairperson) report:

Also, take the time to read John Graham's (President & CEO) message to contributors and beneficiaries:

The critical elements I discussed above also factor into CPP Investments' comparative advantages which all Canadians need to understand and appreciate:

Discussion with John Graham, President & CEO

Late this afternoon, I got to speak with John Graham, CPP Investments' President & CEO.

I want to begin by thanking him for taking the time to speak to me on this very busy day and I'd also like to thank Frank Switzer, Managing Director, Investor Relations for setting this call up and for sending me material early this morning.

John began by stating they focus on risk-adjusted returns so when markets rip like last year, it's hard to keep up with fast money but when they fall off, the Fund won't fall off as much.

The point isn't to outperform public markets every single year, the point is to maintain the sustainability of the Fund over the long run.

John agreed and said:

"That's right, it's to maximize returns without taking undue risks and taking into account the funding of CPP and to really think how we add value. And I think you'll probably enjoy we added more information around our sources of return. I think you got the document today but you'll appreciate what we tried to communicate through the annual report."

The Annual Report is excellent and well worth reading here.

On performance of the Fund, John stated this:

"The 6.8% net return we would describe as a strong return. Our calendar year was 13.8%, fiscal 6.8% net with a very volatile Q1 in the new year with the Russian invasion of Ukraine, rising inflation and the capitulation in the market. So we are happy with how we performed in the fiscal year but as you highlight, it's really the long-term performance that is important and the 10-year return is 10.8%."

He went on to discuss some of the highlights for the year:

"First, our net-zero commitment. This is something we spent a lot of time on, thinking how we move forward with a net-zero commitment which is fit for purpose for CPP Investments and aligned with our investment mandate. And it's one which we see as the cornerstone of interesting opportunities as the whole economy transitions to net-zero. We made it very clear we are not going to pursue blanket divestment, we are not going to divest from oil & gas. I think one of the interesting things is the transition to net-zero isn't going to be linear, there are going to be lots of ups and downs. You're still going to need lots of base metals like copper, cobalt and nickel to electrify the global economy."

He added:

"As we look forward, I would describe our outlook as cautiously optimistic with high inflation and expectations of rising rates, it will impact global growth and that will put a headwind into investment returns. There are not a lot of safe harbors in the global capital markets, so we are cautious. That being said, as you know, CPP Investments is made to invest in markets like these. We are well capitalized, we have lots of liquidity. We spent 10-15 years building out our capabilities. We are a global investor, we invest across global asset classes.So, from a security selection perspective, we are starting to see some opportunities, it's probably too early right now but we are cautiously optimistic."

I agree, there will be dislocations in markets which will present great opportunities for CPP Investments and other large investors with a long investment horizon.

I told John one of the big differences between CPP Investments and others is the high allocation to Private Equity (32%) and Credit (16%), giving them an advantage to pounce on opportunities as they arise.

John commented:

"I agree, we have the capabilities and the right partners. On the Credit side, I used to run that department, 2/3 of that is direct lending/ private credit and 1/3 is in the public credit space. As I stated earlier, the bid-ask spread in private markets is still big, but over time, it will narrow as people get accustomed to the new normal, and that's when you'll see interesting opportunities."

It is worth noting their PE portfolio had a great year and has performed well over the last five years:

Private Equities delivered 18.6% in F2022 and 16.1% over the last five

years, and given its allocation in the asset mix, this helped the

overall Fund.

In Real Assets, both Real Estate and Infrastructure delivered solid gains of 10.2% and 10.8%% respectively.

We then talked about the 2025 strategy:

"I think there a couple of things there worth highlighting. The 2025 strategy we actually put in place in 2018, so we are coming to the end of that strategy. I was at the table and worked on it. There are two key pillars of that strategy. One is to be a global investor and the importance of CPP Investments to be a global investor, including building out the capabilities in emerging markets. Having the ability to tap into sources of global growth, tap into increased diversification, and just the opportunity to find alpha in emerging markets. That's important. That's why we've been focused on building out our capabilities investing in China, India and Latin America. The other pillar of the 2025 strategy, I call it the digital transformation of the organization to modernize the organization. And modernize not only the infrastructure, migrating to cloud and using modern technology, but actually challenging ourselves the investment side to use advanced analytics, AI and alternative data as a way of making better decisions. We have been proactively partnering up with people on the advanced analytics and data side."

They are already looking beyond the 2025 strategy:

On sustainable investments, he told me he was proud of their initiatives and under the leadership of Deborah Orida, Senior Managing Director, Global Head of Real Assets & Chief Sustainability Officer, they are well on their way to achieving carbon neutrality for their internal operations by the end of fiscal 2023 and delivering on their net zero commitment by 2050 or earlier.

I then asked him about whether CPP Investments is willing to take on more greenfield risk in infrastructure:

"We have done greenfield, for sure. We invest in portfolio companies that invest in both greenfield and brownfield infrastructure. We have an investment in our energy group which is a renewables company that develops projects in the US, Japan and elsewhere and sometimes we monetize these projects. We have an investment in an Indian company which is also involved in greenfield infrastructure projects. In toll roads and other places, we've been involved in greenfield. We would just view these projects from an investment lens, meaning is this a good investment and are we getting paid enough to take that greenfield risk? If you think about it, being a long-term investor, we don't need that near term yield, we can invest in a project and take the capital appreciation."

We talked a bit about currency risk and he confirmed they don't generally hedge currency risk because it's not optimal over the long run:

He also said that during times of uncertainty and volatility, investors typically flock to the USD and this is what we have seen recently (flight to safety in Risk Off markets):

"If you think about it from an asset-liability perspective, it makes sense for us to be unhedged. That being said, over the long run, we don't have a positive or negative expectation on currency return, so incurring costs with no expected long-term benefit doesn’t add value (over the long run).”

I did note that Canadian assets make up 16% of the total portfolio, which is a lot more than I thought, but critics still want more.

He

told me the 16% includes bonds.

But he said this:

"When you take our liabilities and mandate into account, we need to pursue our global growth and diversification strategy or else we run the risk of not delivering on our mandate . All the contributions come from Canadians so it makes sense to diversify assets globally. That diversification away from Canada on asset side actually helps the sustainability of the Fund, it's beneficial to diversify those assets globally so the 16% in Canada is actually quite a bit."

He said they own great assets like Highway 407 and invest in Alberta’s oil and gas sector, including pipelines.

We then talked about base and additional CPP:

"The CPP was meant to be one of a three-legged stool in people's retirement, in addition to workplace pensions and personal savings. If you look at what is happening, the workplace DB pension is largely gone, people are struggling to save, so if you're 20-years-old and forecast out 40 years, the CPP is going to be a big part of people's retirement thanks to the additional CPP."

Lastly, we talked about CPP Investments' commitment to equity, diversity & inclusion.

I'm a stickler for diversity & inclusion and told him I'd like to see more people with disabilities hired at CPP Investments and other large organizations:Rise in remote jobs could be a sea change for job seekers with disabilities https://t.co/H2YuuEVcTS via @Yahoo

— Leo Kolivakis (@PensionPulse) May 17, 2022

John told me:

"We are making sure our organization moves from diversity 1.0 to 2.0. What we did put in our annual report is female new hires, female senior leaders, LBGTQ+ and minorities in senior roles but we also do have a goal for people with disabilities. Our goal is 4% and we are at 3.7%. One thing we have been doing is having discussions with our colleagues with disabilities to ensure our cultural practices are supportive of people with disabilities. So it's an area we are focused on and we partnered with a recruiting firm to hire more people with disabilities. We also have conducted accessibility audits in our Toronto and Hong Kong offices and soon at our London office."

I was very pleased to learn this given that more than 6 million Canadians aged 15 and over (22% of the population) identify as having a disability, and it is expected actual numbers are likely higher.

He confirmed they take diversity & inclusion very seriously and will continue delivering on this front, investing in its people and purpose-driven culture:

There is also no question they are doing more to promote gender diversity within and outside their organization and should be commended for this.

If you look at their senior management team, you'll see many sharp and dedicated men and women:

We also briefly talked about the critics who love taking shots on compensation but if you look at the complexity and global reach of this organization, and the long-term performance, you can't argue with its success and that compensation is earned.

He told me they are "fully transparent" and they are, with detailed discussions throughout the annual report on compensation and how it is determined.

I'm mystified at critics who keep harping on "out of control pay" without fully understanding the sheer size, scale, scope and complexity of all their operations.

This isn't your grandfather or grandmother's CPP Fund, this is a much larger and far more sophisticated Fund requiring highly specialized talent:

The same goes for all of Canada's large pensions.

I thank John Graham for another enlightening conversation and look forward to speaking with him again.

Below, the CPP Fund surpassed half a trillion dollars, ending the fiscal year at $539 billion in net assets. CEO John Graham discusses the results and more and why the CPP Fund is strong, resilient and always focused on its long-term strategy. He also discusses the Fund's commitment to sustainable investing.

Comments

Post a Comment