William Watts of MarketWatch reports US stocks lose more ground after jobs data, extending steepest fall since 2020:

U.S. stocks traded lower Friday, as investors weigh April jobs data amid

heightened stagflation fears, after the biggest daily drop since 2020

on Thursday.

On Thursday,

the Dow industrials slumped 1,063.09 points, or 3.1%, its worst daily

percentage drop since Oct. 28, 2020, according to Dow Jones Market Data.

The S&P 500 fell 3.6%, while the Nasdaq Composite tumbled 5% for

its worst daily percentage fall since June 11, 2020.

What’s driving markets?

The U.S. economy added 428,000

new jobs in April, but an acute labor shortage showed little

improvement last month, which could underline worries about inflation

already running its hottest in 40 years. Economists polled by The Wall

Street Journal had forecast 400,000 new jobs.

The unemployment

rate was unchanged at 3.6%, the government said Friday, just above a

54-year low. Average hourly earnings cooled, rising 0.3% versus

expectations for a 0.4% increase.

The jobs report “has something

for everyone…steady job gains supporting economic growth with less wage

pressure, possibly easing inflation fears,” said John Lynch, chief

Investment officer for Comerica Wealth Management.

“Investors

need confidence that the Fed won’t raise too aggressively and topple the

economy into recession in their fight against inflation. Today’s report

is balanced and may prove to dampen the extreme volatility of recent

days,” he wrote.

Investors will also hear Friday from New York

Fed President John Williams, and after the market close, St. Louis Fed

President James Bullard and Fed Gov. Chris Waller. In between, consumer

credit data for March is ahead Friday.

Major indexes were set to

end the week with small losses, which belies volatile action seen in

recent days. Stocks surged Wednesday after the Federal Reserve delivered

a widely expected half percentage point interest rate increase, and

perceptions that the central bank may be less hawkish than perceived,

but those gains reversed, and then some on Thursday.

“As we

approach intraday lows for the year, keep plenty of powder dry and build

a list of quality company opportunities to add when the bottom comes,”

said Louis Navellier, founder of Navellier & Associates, in a Friday

note. “Companies with double-digit earnings growth remain the only way

to “beat” current inflation expectations, when to step in remains

uncertain.”

Some blamed Thursday’s sharp drop, in part, on a divided decision by the

Bank of England to hike interest rates to the highest level since 2013,

alongside a grim economic forecast, which was accompanied by a grim

economic forecast.

A sharp drop in first-quarter U.S. productivity data and a rise in

unit labor costs published Thursday were also cited as a factor,

underlining stagflation fears. That rubs against the assertion by Powell

and other senior Fed officials that they can achieve a so-called soft

landing — lowering inflation without bringing economic growth to a

grinding halt.

“What’s dangerous about yesterday’s huge market

slump is that there must be an element of doubting the ability of there

to be an effective ‘Fed Put’ in this cycle following a 30-40 year period

where the central bank has almost always been able to come to the

market’s rescue,” said a team of Deutsche Bank strategists led by Jim

Reid.

Yields on 10- and 30-year Treasury bonds hovered at levels last seen in 2018, which they reached Thursday as stocks plunged. The 10-year yield rose 1.2 basis points to 3.078%.

It's Friday and it was an extremely volatile week in markets.

In his press conference, Fed Chairman Powell stated the "FOMC isn't looking to raise rates by 75 basis points" and given the "excess demand for labor" he thinks a soft landing is still achievable (but he admitted it's not going to be easy).

That was enough to send stocks soaring late Wednesday afternoon but by Thursday, reality hit and selling accelerated as investors bet the Fed remains behind the inflation curve and will need to raise rates more aggressively.

Stocks sold off hard on Thursday and Friday morning until Minneapolis Fed President Neel Kashkari posted a comment stating the Fed wasn't as

far behind on the fight against inflation as many hawks have been

arguing:

An

important question for monetary policymakers is, What policy stance,

including the current setting of the federal funds rate, the current

size and composition of the Fed’s balance sheet, and the expected paths

of the funds rate and balance sheet, represents “neutral” — neither

stimulating nor restraining the economy?

In

our Summary of Economic Projections (SEP), the participants in the

Federal Open Market Committee (FOMC) estimate the longer-run level of

the federal funds rate — that is, the overnight nominal interest rate

that best represents neutral in the longer run, once the various shocks

that are hitting the economy have passed. We cannot observe the neutral

funds rate directly; we can only estimate it. My own estimate of the

nominal neutral funds rate is 2.0 percent, and the range of estimates in

the most recent SEP among FOMC participants is from 2.0 percent to 3.0

percent.

But

is the nominal federal funds rate what really drives economic activity,

and therefore, is comparing it to our estimate of its longer-run

neutral level the best assessment we can make of the current stance of

monetary policy?

Most

economists argue that it is not nominal rates that drive economic

activity, but real rates: nominal rates less inflation. And while the

FOMC has now raised the funds rate by 75 basis points over the past two

meetings (to 75 to 100 basis points), inflation has climbed rapidly over

the course of the past year (chart 1). Some observers argue the Fed is

way behind the curve because inflation has climbed faster than we have

raised rates. Therefore, monetary policy has not tightened but has

actually become more stimulative as inflation climbed. So we aren’t

simply behind the curve, they argue, we are falling even further behind.

Is this criticism right?

No.

While

I agree real rates are more important than nominal rates in driving

economic activity, I believe it is long-term real rates — say 5 years,

10 years or longer — rather than overnight rates that influence business

and consumer demand for credit. When businesses consider taking a loan

to build a new factory, they consider their cost of capital over the

life of the project to determine if the project is a good investment.

Similarly, when families consider taking out a mortgage to buy a home,

most are not thinking about overnight interest rates. They are

considering the interest rate they will have to pay for the mortgage

over the life of the loan, 10, 15 or even 30 years. Hence, in my view,

long real rates are far more important than short real rates in driving

economic activity, and we should look at long real rates to assess if

policy is stimulating or restraining the economy. So what has happened

to long real rates?

Since the FOMC began pivoting its policy stance last fall, there has been a dramatic increase in long-term real interest rates.

Chart

2 shows that long-term real rates have risen quickly in the past

several months. In fact, they have risen even faster than they fell in

the spring of 2020, when the FOMC cut the federal funds rate to

essentially zero and launched a massive quantitative easing program to

support the economy. How is that possible given that we have only raised

the funds rate by 75 basis points and haven’t actually begun shrinking

our balance sheet?

We

are seeing the power of forward guidance: the FOMC has signaled where

policy is headed in the future and markets have adjusted in anticipation

of those policy moves, including both expected increases in the funds

rate and decreases in the balance sheet. Because the FOMC has strong

credibility with market participants, they take our forward guidance

seriously, as they should.

Just

before the pandemic hit, the 10-year real rate was about 0 percent, and

today it has returned to about 0 percent after falling to -1 percent

during the pandemic at the height of the Fed’s monetary stimulus. So

where are we now relative to neutral?

As

I noted above, we can’t directly observe the neutral nominal funds

rate. The same is true for the neutral long-term real rate. We can only

try to estimate it. One approach is to look at “forward” real interest

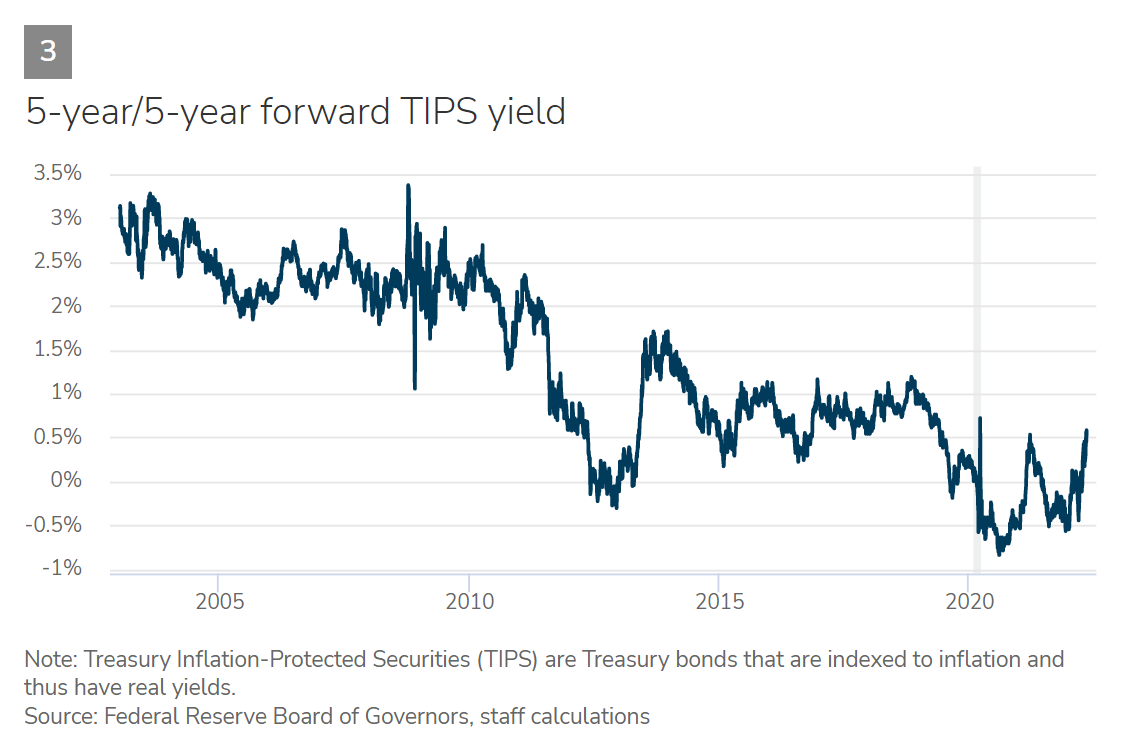

rates, which allow for the effects of shocks to have passed. The

following chart shows the 5-year real rate 5 years forward, which is one

such proxy. You can see it has been declining over the past 20 years

(chart 3).

We

do know that neutral rates have been falling in advanced economies

around the world due to factors outside the influence of monetary

policy, such as demographics, technology developments and trade. I

believe monetary policy was roughly at a neutral stance shortly before

the pandemic. Long-term real rates have now returned to roughly that

level.

So, if I think we are close to neutral now, what does that mean for monetary policy going forward?

First,

at a minimum, the FOMC must follow through on the forward guidance of

federal funds rate increases and balance sheet reduction that we have

already signaled in order to validate the repricing that has taken place

in financial markets.

Second,

we will need to see whether the supply issues that have contributed to

high inflation begin to unwind and/or if the economy is in a

higher-pressure equilibrium. I wrote about this possibility

seven weeks ago. Unfortunately, the news from the war in Ukraine and

the COVID lockdowns in China are likely delaying any normalizing of

supply chains. If supply constraints unwind quickly, we might only need

to take policy back to neutral or go modestly above it to bring

inflation back down. If they don’t unwind quickly or if the economy

really is in a higher-pressure equilibrium, then we will likely have to

push long-term real rates to a contractionary stance to bring supply and

demand into balance. The incoming data over the next several months

should provide some clarity on these questions.

Finally,

we will need to continue to assess where neutral is. If the economy is

in fact in a higher-pressure equilibrium, that might indicate the

neutral long-term real rate has increased, which would then require even

higher rates to reach a contractionary stance that would bring the

economy into balance.

So how do I put this all together?

The

FOMC has made a dramatic pivot in the overall stance of policy over the

past several months. Forward guidance and the committee’s strong

credibility with market participants have resulted in a withdrawal of

monetary stimulus even faster than we added it in the spring of 2020.

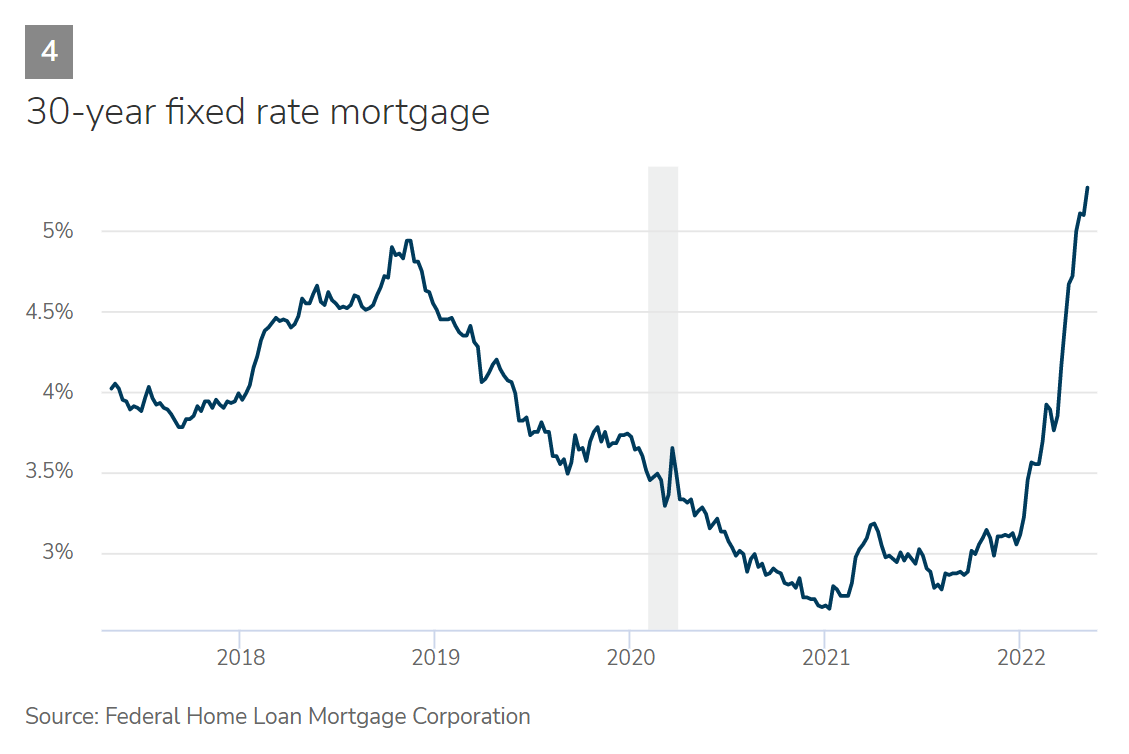

Look at how mortgage rates have sharply climbed as an indicator of how

rapidly monetary policy has tightened (chart 4).

We

now need to follow through on our forward guidance, and I am confident

we will. We will need to observe incoming data over the next several

months to determine if fulfilling current guidance is enough to bring

inflation back down or if we will need to do more. I am confident we

will do what we need to do to return inflation to our 2 percent target.

Whether or not you agree with Kashkari, he provides a lot of food for thought and I too question whether the neutral rate should be between 2.5% and 3% or 2% as he claims.

In reality, nobody knows because as he rightly notes, we can’t directly observe the neutral nominal funds

rate, we can only try to estimate it.

But Kashkari is clear that the FOMC may have to push long-term real rates into a contractionary stance in order to help bring inflation down:

"We will need to observe incoming data over the next several months

to determine if fulfilling current guidance is enough to bring inflation

back down or if we will need to do more," Kashkari said in an essay

posted on Medium, adding that the war in Ukraine and the COVID lockdowns

in China will likely delay any normalizing of supply chains.

"If

they don’t unwind quickly or if the economy really is in a

higher-pressure equilibrium, then we will likely have to push long-term

real rates to a contractionary stance to bring supply and demand into

balance," he said.

That's the big risk, if inflation pressures don't unwind quickly or if the economy is in a higher inflation-pressure equilibrium, then the Fed will need to push long-term rates to a contractionary stance to bring "supply and demand into balance."

And if that happens, the risks of a policy error and hard landing skyrocket.

That's what makes investors so nervous and that is why stocks sold off hard after the knee-jerk reaction following Powell's press conference on Wednesday.

Now, are stocks oversold? You bet, on a short term basis, they are, especially the tech heavy Nasdaq which reached a low of 11,990 this morning before bouncing up (it's still down):

The Nasdaq is way below its 50-day moving average and due for a relief rally:

But if a relief rally doesn't take it back to its 50-day moving average, the risk is selling will accelerate, taking the Nasdaq below its 200-week exponential moving average:

Notice in late 2018 and March 2020, when that happened, the Nasdaq rallied sharply, but the inflation environment was much more benign back then, allowing the Fed to step in.

This time around, the inflation environment isn't Fed friendly, which is why global investors are worried.

On Thursday, Senator Clément Gignac who still tracks markets very closely, shared his views with me:

Today, big institutional investors are packing up because they find the Fed is not credible and serious with its gradual approach in breaking inflationary expectations.

This is the reason I was of the opinion that a 75 bps hike would have been better to fight inflation expectations!

When Greenspan made the 75 bps hike in Fall 1994, bond and stock markets started to rally, being convinced that dentist chair period will finish sooner rather than later!

I would add that the Fed's prediction about the course of inflation has been wrong for the last 12 months. By mentioning that a jumbo hike of 75 bps is off the table, it suggests the Fed will remain behind the curve and be reactive rather than being preemptive.

Maestro Greenspan worked differently and he was successful in engineering a soft landing in 1994-95 despite a 300 bps rate increase in 12 months! Which US economist or Wall Street guru predicted or recommended such medicine a year ago? Nobody! If Chairman Powell had the guts to act earlier, he would have been proven right to act in a preemptive manner as a leader, not a follower.

Clément also posted this on LinkedIn earlier today which I agree with:

Anyway, it remains to be seen how credible the Fed will be in breaking inflation expectations.

If it's too credible, it risks breaking a lot more than inflation expectations, it risks a very hard landing.

Some final food for thought. Keep your eyes peeled on credit markets. As rates rise and junk bond spreads widen, it doesn't portend well for the economy or markets:

If we get a full-blown credit crisis, the Fed will be forced to act swiftly to avoid deflation, not stagflation!

Anyway, try to relax this weekend, I have a feeling there will be some relief rally next week.

If not, God help us!

Below, Steve Weiss, Short Hills Capital Partners' managing partner, joins the

'Halftime Report' to discuss inflation and the Fed hikes with Scott

Wapner, Jenny Harrington, Kevin O’Leary and Jon Najarian.

I also embedded Fed Chairman Powell's press conference which transpired on Wednesday afternoon. Take the time to watch it.

Lastly, Mike Wilson, Morgan Stanley's chief US equity strategist, joins

'Closing Bell: Overtime' to discuss the reaction to the Fed's efforts to

tighten monetary policy to tame inflation.

Update: Nasdaq records first five-week losing streak since 2012. See the details here and here. Also read this Bloomberg article on how the brutal stock selloff is a multitude of bear cases coming true.

Comments

Post a Comment