The Absolutely Insane (AI) Market Reaches New Levels of Delusions

The frenzy surrounding artificial intelligence led another day of gains in the stock market as traders were also growing more confident a deal on the US debt limit will be reached.

The S&P 500 rose 1.1% and the tech-heavy Nasdaq 100 added 2.4% as Marvell Technology Inc. said 2024 revenue would “at least double” from a year ago on a surge in demand from AI, echoing sentiments from Nvidia Corp. earlier. Shares of the chipmaker surged 30%.

The gains came as US negotiators also appeared to be moving closer to an agreement to raise the US debt limit and cap federal spending for two years. A US default could result in catastrophic damage, putting markets on edge. However, House Speaker Kevin McCarthy said he believed progress had been made last night.

“Today we are getting a boost from debt ceiling headlines plus continued AI enthusiasm,” said John Kolovos, chief technical strategist at Macro Risk Advisors.

Investors were demanding less of a premium to hold US Treasury bills seen most at risk of nonpayment if a deal isn’t reached in time. Securities expiring in early June — when Treasury Secretary Janet Yellen warned the government could run out of money — are all yielding less than 6% on Friday.

Meanwhile, the rate-sensitive two-year Treasury drifted as traders considered how a debt deal could play into the Federal Reserve’s path forward on interest rates. The two-year yield hovered around 4.56% after a report on consumer spending showed the Fed still has more work to do to bring inflation back towards its target. The personal consumption expenditures price index, one of the Fed’s preferred inflation gauges, rose by a faster-than-expected 0.4% in April.

“While we believe that there are good chances for a [debt] resolution before the FOMC meeting, any deal would almost certainly include some fiscal tightening, which should reduce the need for the Fed to hike rates,” said Brian Rose, senior US economist at UBS Chief Investment Office. “Going past the debt ceiling deadline would have serious consequences, and in that event there is almost no chance that the Fed would hike.”

In other corporate news, retailer Gap Inc. rallied 14% after reporting better-than-expected results. Workday Inc. jumped 9.9% after results at the application software company pointed to stable demand. And Ford Motor Co. rose 7.0% after striking a deal with Tesla Inc. to give its electric vehicle customers access to the Tesla Supercharger network.

Elsewhere in Europe, the Stoxx 600 rose with chipmakers including ASML Holding NV advancing for a second day. Glencore Plc rose after a report that its Viterra unit is in talks to merge with Bunge Ltd., one of the world’s largest crop merchants. And in Asia, the benchmark CSI 300 index ended little changed, bringing the week’s losses to 2.4% amid growth concerns.

Josh Schafer of Yahoo Finance also reports stocks rise as investors await debt deal, AI hype lifts tech:

Stocks surged higher Friday afternoon as investors waited for developments from Washington, D.C. on the debt-ceiling deliberations and digested the latest corporate earnings as a new wave of AI optimism boosted tech stocks.

All three major indexes ended the trading day higher with the Nasdaq pacing gains.

The S&P 500 (^GSPC) closed 1.3% higher, the Dow Jones Industrial Average (^DJI) was up more than 300 points, or 1%, while the technology-heavy Nasdaq Composite (^IXIC) gained more than 2%.

The Nasdaq and S&P 500 both notched weekly gains with Friday's rally.

On Friday morning, Reuters reported that President Joe Biden and Speaker of the House Kevin McCarthy are "closing in on a deal" to extend the government's debt ceiling for two years.

"Negotiators appear to be closing in on an agreement," Goldman Sachs's economic research team led by Jan Hatzius wrote in a note to clients on Thursday night.

"While it is hard to predict when an announcement could come, we think the odds are highest that a deal is announced late Friday (May 26) or on Saturday (May 27). If so, this would likely allow a House vote late Tuesday (May 30) or Wednesday (May 31). The Senate also needs to pass the deal, though procedural obstacles there are unlikely to be what prevents timely enactment," they added.

The Nasdaq rallied to close 1.7% higher on Thursday as Nvidia's (NVDA) blowout quarter sent the chip giant's stock soaring more than 24%.

Earnings continued to move stocks on Friday morning as well.

Marvell Technology (MRVL) stock rose more than 30% on Friday as the chipmaker joined Nvidia in sharing positive artificial intelligence news. Marvell believes its revenue attributable to AI could double in the next year.

"AI has emerged as a key growth driver for Marvell," Marvell CEO Matt Murphy said in the company's earnings release. "While we are still in the early stages of our AI ramp, we are forecasting our AI revenue in fiscal 2024 to at least double from the prior year and continue to grow rapidly in the coming years."

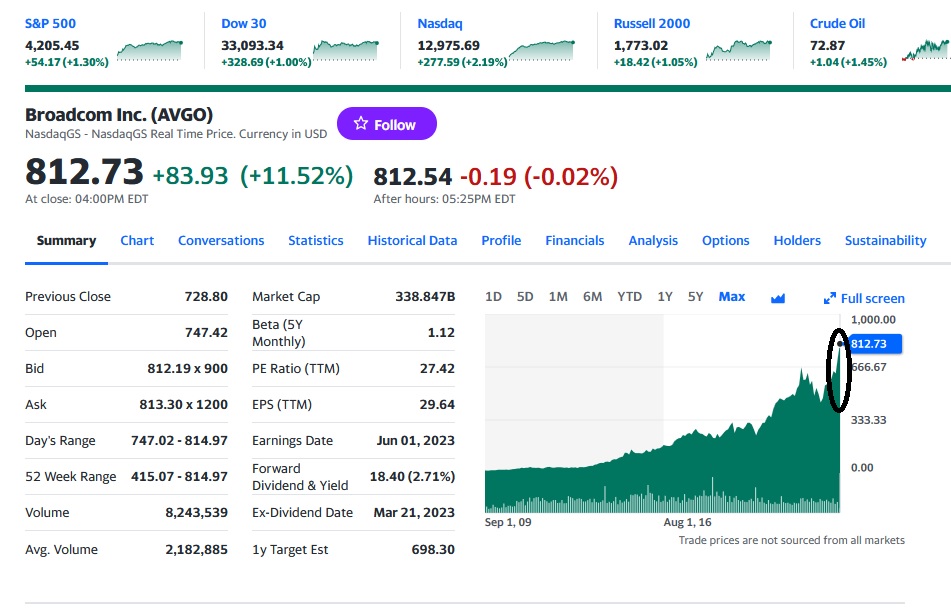

Chip names including Broadcom (AVGO), Ambarella (AMBA), Skyworks (SWKS), and Micron (MU) were all up more than 5% on Friday. The PHLX Semiconductor Index (^SOX) was also up more than 5%.

Elsewhere on the earnings front, Gap (GPS) stock rose more than 10% after the apparel retailer posted a surprise profit late Thursday. Meanwhile, shares of Ulta Beauty (ULTA) fell as much as 13% after the company warned of slowing growth trends, even though the beauty store chain beat Wall Street's revenue and earnings per share expectations for the first quarter.

"Category growth is healthy but moderating as we lap two years of unprecedented growth. And as category growth normalizes, promotional activity is increasing," Ulta CEO Dave Kimbell said on the company's earnings call.

On the economic data side, the PCE price index — the Federal Reserve's preferred inflation measure — came in hotter than expected and flipped market expectations for the central bank's next policy announcement on June 14.

Core PCE rose to 4.7% over last year in April, more than the 4.6% increase expected by economists and an acceleration from the 4.6% annual jump seen in March. Data from the CME Group as of Friday morning showed investors placing a 58% chance on the Fed raising rates by another 0.25% next month following this release.

"We will be sticking with the forecast for the Fed to keep rates unchanged through the remainder of this year," Ryan Sweet, chief US economist at Oxford Economics, wrote on Friday. "However, odds are rising that we will be altering the forecast for the fed funds rate in 2024, reducing the number of rate cuts."

Data on personal income and spending also showed consumers remained resilient in April with spending rising 0.8% last month, more than the 0.3% increase expected by economists. Durable goods orders also delivered a surprise with April's preliminary reading showing an increase of 1.1% last month; economists had expected this data to show a 1% drop.

Consumer sentiment data for May from the University of Michigan, however, showed the debt ceiling standoff has dampened the economic outlook for many Americans, with sentiment dropping 4 points from April.

"Consumer sentiment slid 7% amid worries about the path of the economy, erasing nearly half of the gains achieved after the all-time historic low from last June," said Joanne Hsu, director of the survey of consumers.

"This decline mirrors the 2011 debt ceiling crisis, during which sentiment also plunged. This month, sentiment fell severely for consumers in the West and those with middle incomes. The year-ahead economic outlook plummeted 17% from last month."

Alright, it's Memorial Day weekend in the US, most people are already in vacation mode so I'll try to keep this comment short and entertaining.

First, let's look at the top-performing large cap stocks over the past week:

As you can see above, a lot of the chip stocks were on fire this week, led by Marvell Technology (MRVL), Super Micro Computer (SMCI), Nvidia (NVDA), Broadcom (AVGO) and others.

Next, let me show you the frenzy in AI stocks in images:

I added Rambus and Lattice there too but there are plenty of other semi stocks (AMD and Micron) on fire this week.

These are the type of charts that remind me of 1999-2000 during the tech melt-up phase when hedge funds were partying like it's 1999.

In fact, in his weekly market wrap-up, "2000 Vibes," Martin Roberge of Canaccord Genuity writes:

Our focus this week had to be on NVDA and the ongoing AI mania. Many investors are asking how it compares to the dotcom bubble. Our Chart of the Week provides some insight as we compare Cisco Systems, the poster child of the 1999-2000 tech bubble, to NVDA. Our reference point is March 2000, which was the peak of the bubble. The good news for NVDA bulls is that the company accounts for ~2.7% of the S&P 500 market cap compared to ~4% for Cisco. If one assumes the S&P 500 remains flat, a 4% weight for NVDA would peg the stock price at ~$550-600. The bad news is that at ~$380, the stock trades at ~22x one-year forward sales estimates of $43.6B. This is only 1x point below Cisco’s peak at 23x. Bulls may argue that NVDA’s sales growth profile is superior to that of Cisco but as the third panel of our chart shows, analysts were also very upbeat about Cisco’s sales projecting ~40% annual growth for the bulk of calendar 2000 and 2001. This is exactly where we are today with NVDA following this week’s monster guidance (see the hockey stick?). For the record, despite steady increases in forward EPS and sales estimates from March 2001 to February 2001, Cisco’s shares dropped ~60% during this time interval. Back then, analysts missed on their TAM assumption for high-performance communication gears as global telecoms became debt trapped through the fiber optic rollout. For AI stocks, the TAM is huge but current valuations seem to discount an immaculate GPU transition among clients and no supply bottlenecks and/or manufacturing hiccups from chip suppliers.

Last week, I covered top funds Q1 activity and warned my readers not to follow Cohen, Druckenmiller, Tepper and other elite hedge fund managers into these AI names because they're extremely risky here.

And this week, they all digested a pack of Viagra and are literally bursting at the seams!

The amount of nonsense I've seen since the onset of the pandemic when central banks dropped rates to zero and engaged in massive QE is unprecedented.

And even after the Fed and other central banks have raised rates aggressively all year, there is still too much money sloshing around out there and the proof is we are witnessing one bubble after another.

The latest AI bubble is all hype, it's absolutely insane but if you sit down and tell people this, they look at you like you're from Mars.

Consider some tweets I've retweeted this week (there are plenty more here):

Last 10 Years

— Charlie Bilello (@charliebilello) May 25, 2023

Bitcoin $BTC: +19,968%

NVIDIA $NVDA: +11,145%

AMD $AMD: +2,896%

Tesla $TSLA: +2,884%

Apple $AAPL: +1,168%

Microsoft $MSFT: +1,047%

Netflix $NFLX: +1,013%

Facebook $META: 908%

Amazon $AMZN: +780%

Google $GOOGL: +459%

S&P 500 $SPY: +202%

Gold $GLD: +34%

US CPI: +31%

Forget 10-baggers, NVIDIA $NVDA is now a 100-bagger over the last 10 years. Up more than 11,000%. pic.twitter.com/hhEIwwv2yj

— Bespoke (@bespokeinvest) May 25, 2023

S&P 500 Performance Breadth (the % of outperforming stocks) has fallen to its lowest level in more than 2 decades pic.twitter.com/RrzxNGdcs7

— Barchart (@Barchart) May 25, 2023

Only 20% of S&P 500 companies are outperforming the overall index on a 3-month trailing basis which is the smallest % since the dot-com bubble burst in 2000 👀 pic.twitter.com/c4AflVfK5A

— Barchart (@Barchart) May 28, 2023

Nasdaq now outperforming the Dow Jones Industrials by more than 22 percentage points, the widest margin thus far in the year since the Nasdaq launched in 1971 pic.twitter.com/qg8an2uwpX

— Barchart (@Barchart) May 25, 2023

The S&P 493 is up 1% YTD pic.twitter.com/qZozY3k4pP

— Leo (@Growth_Value_) May 26, 2023

9 FANG+ have cumulatively returned +9.6% this year, making up 108% of the S&P 500’s YTD gain. - @LeutholdGroup pic.twitter.com/mUpLNzgl1C

— Eric Wallerstein (@ericwallerstein) May 26, 2023

1999, 2007, 2020, 2023 👇 What a pattern. (BBG) pic.twitter.com/a0yRcK1xc1

— Michael A. Arouet (@MichaelAArouet) May 27, 2023

Party like it's 2020 again with mega-cap growth. (Returns through Thursday, May 25) pic.twitter.com/vYbwItsH0M

— John Coumarianos (@JCoumarianos) May 27, 2023

God Candle from Nvidia $NVDA - Oh My!! pic.twitter.com/gG1DYRlikQ

— Barchart (@Barchart) May 24, 2023

Cathie Wood’s flagship exchange-traded fund closed out its Nvidia stake in early January. Then, came the artificial intelligence frenzy that sent the stock and its big tech peers on a tear https://t.co/DSs8AqHOow

— Bloomberg Markets (@markets) May 26, 2023

Cathie Wood defended her firm’s decision to bail on Nvidia before the chipmaker’s shares surged 160%, saying the computer-chip industry’s boom-bust cycle poses risks https://t.co/lPidpcUuYb

— Bloomberg Markets (@markets) May 26, 2023

Street upgrades to Nvidia's earnings forecasts were so substantial yesterday that the forward price to earnings actually FELL - making the stock look cheaper even with the 25% rally...! pic.twitter.com/An2P1QlJNN

— Valerie Tytel (@ValerieTytel) May 26, 2023

NVIDIA becomes first of “Super 7” to close its drawdown gap from prior peak … important to keep in mind that this group encompasses Tech, Consumer Discretionary, and Communication Services sectors; so, it’s not all a “tech” trade pic.twitter.com/MRDY7TYiZW

— Liz Ann Sonders (@LizAnnSonders) May 26, 2023

Short Sellers have lost a combined $8.1 billion betting against Nvidia $NVDA in 2023 pic.twitter.com/08It62uN75

— Barchart (@Barchart) May 25, 2023

"What's interesting about #Nvidia is this was not a widely shorted stock into the results. So that 30% rally was really the market recognizing they have to reprice the future cash flows. I think that's pretty true for most of the FAANG trade," says @fundstrat pic.twitter.com/X0BidNd2Wu

— CNBC's Closing Bell (@CNBCClosingBell) May 26, 2023

And my favorite one that made me laugh out loud:

Young people probably think that I don't understand artificial intelligence.

— Mac10 (@SuburbanDrone) May 25, 2023

They are right. pic.twitter.com/zH2O7gb2sL

Of course, the pain trade has been up, not down this year but debt deal or not, I know how this movie ends, in tears:

ALL of the Nasdaq selloffs came from this level overbought or lower.

— Mac10 (@SuburbanDrone) May 28, 2023

8:8 pic.twitter.com/zIaaEaZn4i

The Tech sector heads into the weekend trading 3.23 standard deviations above its 50-DMA, its most overbought reading since January 2004! https://t.co/q67x95hrcY pic.twitter.com/8UMWAhLVBk

— Bespoke (@bespokeinvest) May 26, 2023

The chart of the week.

— Mac10 (@SuburbanDrone) May 26, 2023

Choose carefully: pic.twitter.com/irXVDVnWEb

Disclaimer: I know nothing about Nvidia other than what I've read in the media. What I do know is its revenues have been cyclical for the last 20 years, and this, with the most aggressive Fed tightening cycle in generations. FOMO wins the day, but I suspect macro wins the cycle. pic.twitter.com/mJPEKJBkke

— Francois Trahan (@FrancoisTrahan) May 25, 2023

The 10 Most Overbought Stocks include $AMD, $NVDA, $META, and $GOOGL according to FactSet pic.twitter.com/yYnvFOrlBM

— Barchart (@Barchart) May 28, 2023

There may be some disappointments on the horizon 👇 But of course this time it’s different. Chart @RichardDias_CFA pic.twitter.com/RruflwD2IQ

— Michael A. Arouet (@MichaelAArouet) May 27, 2023

If there is a debt deal, rate hike odds will likely explode higher.

— Mac10 (@SuburbanDrone) May 26, 2023

Currently at 66%.

I'm not convinced a deal would pass Congress. If not, this casino is bidless.

Have a great weekend everyone! pic.twitter.com/IC0FIGuurK

The new "x date" for default is June 5th.

— Mac10 (@SuburbanDrone) May 27, 2023

Here's the 2011 scenario overlaid on today's chart. When the deal was reached, stocks sold off on the news.

Shorts covered ahead of the vote.

And then the market crashed when it passed.

If it doesn't pass, markets explode. pic.twitter.com/cwotFmjAiz

It's important to remember that none of today's bullish pundits saw the last market top either. pic.twitter.com/YWsJZRW7Co

— Mac10 (@SuburbanDrone) May 26, 2023

This is noteworthy.

— Otavio (Tavi) Costa (@TaviCosta) May 26, 2023

The only other times when the tech sector surged over 4% while overall stocks declined were at the onset and in the middle of the Tech Bust.

April 2000 and March 2001.

My 2 cents:

Watch for times when the generals lead but the soldiers don’t follow. pic.twitter.com/FsXJAlUSpA

And what will end this nonsense once and for all?

Well, it's time Jay Powell and company grow a pair and jack up rates to 9% or more!

Markets are now betting the Fed will raise rates next month https://t.co/IlUagGfeI0 via @YahooFinance

— Leo Kolivakis (@PensionPulse) May 26, 2023

Either way, with core inflation remaining sticky and wage inflation pressures picking up steam, don't be surprised if rates rise over the next six months.

Sure, I will admit the S&P 500 led by tech stocks looks bullish here:

And so does the Nasdaq but note here a double top is forming, it really needs to break above the 14,000 level for me to conclude this rally led by a few big names has legs:

Also note the rebound in the US dollar which signals risk aversion is picking up here:

Lastly, it's Memorial Day on Monday, markets will be closed and next Friday we get the US nonfarm payroll numbers for May. That will definitely ignite something.

The two weeks after Memorial Day were the worst two weeks of 2022 for Global markets.

— Mac10 (@SuburbanDrone) May 24, 2023

I don't recall a debt default mind you. pic.twitter.com/pdwtA7m7ix

And by the way, the trade of the week wasn't buying Nividia or Marvell before earnings -- although that paid off handsomely -- the trade of the week was buying shares of Annexon (ANNX) on Thursday when they plummeted more than 57% after the company reported mixed results for an eye disease therapy late Wednesday and selling them at the close today:

Alas, LTK Capital Management missed this one, maybe I need to grow a pair too! (or a brain!)

Alright, enjoy the long Memorial Day weekend, I'll be back next week.

Below, CNBC's Kayla Tausche joins 'The Exchange' to discuss the latest updates from the debt ceiling negotiations.

Next, Mohamed El-Erian, chief economic adviser at Allianz and Bloomberg Opinion columnist, says an "overly data dependent" Federal Reserve will raise its benchmark interest rate at the next policy meeting in June. He also talks about how the debt ceiling drama is hurting the economy. He speaks on "Bloomberg The Open."

Third, Carter Worth, Worth Charting, discusses Nvidia as the stock surged this week with CNBC's Melissa Lee and the Fast Money traders.

Fourth, Tom Lee, Fundstrat managing partner, joins ‘Closing Bell’ to discuss the tech industry's remarkable run in the market, the recent surge in Nvidia stock, and more.Watch full interview here.

Fifth, Ark Invest CEO Cathie Wood discusses why she is cautious on Nvidia and her approach to AI investing with Caroline Hyde on "Bloomberg Technology." Wood also comments on the US debt impasse and the outlook for inflation.

With all due respect to Ms. Wood, Tesla is still a big time short as far as I'm concerned:

Sixth, Lori Calvasina, RBC Capital Markets Head of US Equity Strategy & Gillian Tett, Financial Times Editor-at-Large question whether AI will enhance productivity and the impact it may have on tech. I agree that we are overestimating the productivity gains from AI.

Lastly,Morgan Stanley Chief US Equity Strategist Mike Wilson says his firm's bearish call for equity markets hasn't changed despite the recent runup in big technology stocks. "This is what bear markets do. They are designed to fool you, confuse you, make you do things you don't want to do," he says on "Bloomberg Surveillance."

Comments

Post a Comment