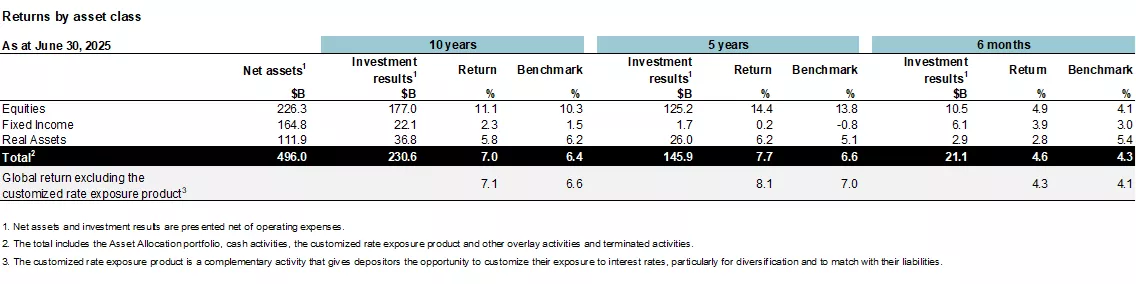

Earlier today, La Caisse released its mid-year results stating it posted a return of 4.6% over the first six months of the year and 7.7% over five years:

Five-year return beats benchmark portfolio and exceeds depositors’ needs

Ten-year return of 7.0% also higher than the benchmark portfolio

Depositor plans in excellent financial health, reflecting their assets’ good performance

La Caisse today presented an update of its results as

at June 30, 2025. Over six months, the weighted average return on its

depositors’ funds was 4.6%, above its benchmark portfolio’s 4.3%. Over

five years, the average annualized return was 7.7%, also outpacing the

benchmark portfolio’s 6.6%. Over ten years, the average annualized

return was 7.0%, also higher than its benchmark portfolio, which stood

at 6.4%. As at June 30, 2025, La Caisse’s net assets were $496 billion,

up $23 billion over six months.

“In

the first half of the year, tariff issues related to U.S. policy were a

major concern. Financial markets were highly volatile, with a

correction in April followed by a robust rebound. Despite this overall

performance, we must remain vigilant as we have yet to see the full

effects of the U.S. administration’s measures,” said CharlesEmond, President and Chief Executive Officer of LaCaisse.

“Against significant rate increases, stock market concentration and

challenges in real estate over the past five years, our portfolio held

strong and outperformed its benchmark portfolio. Our depositors’ plans,

and therefore Quebecers’ pensions, are in excellent financial health.”

Return highlights

Equities

Equity Markets: Performance powered by Europe, Canada and emerging markets

In

the first half of the year, global stock markets responded to the

back-and-forth on tariffs with volatility, yet recorded gains. The MSCI

ACWI Index, which includes both developed and emerging markets, posted

a 4.4% return, hampered by the U.S. market, which suffered from

uncertainty around the country’s economic policy. Indexes from several

major regions, including the eurozone, Canada and emerging markets,

delivered excellent performance. In this context, the Equity Markets

portfolio recorded a 6.0% return, outperforming its benchmark

portfolio’s 5.5% return. This result was due to all management mandates,

with a significant contribution from Canadian and emerging market

stocks, as well as timely risk-taking during the slide in early April.

Over

five years, the annualized return was 13.3%, compared with 12.9% for

the index. Drivers of this performance include the increase in exposure

to major technology stocks and the contribution of Canadian portfolio

companies over the period.

Private Equity: Portfolio companies continue to grow despite the market slowdown

Over

six months, the portfolio turned in a 3.4% return, above its benchmark

index, which posted a 2.0% return. The performance is explained by

growth in the profitability of portfolio companies, both in Québec and

internationally, but that was more moderate in a slowing environment.

During the six-month period, the teams pursued their disposition

strategy and completed just over $8 billion in materializations, while

making new investments of $4 billion.

Over five years, the

portfolio’s annualized return was 16.7%, compared with 15.4% for the

benchmark index. Exposure to the technology, finance and industrial

sectors was particularly beneficial over the period.

Fixed Income: Strong current yield due to high rate environment and credit Premiums

The

first half of the year was characterized by escalating trade tensions

and the risk of economic recession in the United States, as well as U.S.

yields diverging from the rest of the world. In this context, the Fixed

Income asset class generated a 3.9% six-month return, above its

benchmark index’s 3.0%. The performance is due to a strong current yield

of 2.8% and positive execution in government debt, corporate credit and

capital solutions activities.

Over five years, the asset class

posted an annualized return of 0.2%, still largely affected by 2022’s

major market correction, compared to the index’s -0.8%. The quality of

all credit activities explains the difference with the index.

Real Assets

Infrastructure: Constant return in an unstable geopolitical context

Over

six months, the Infrastructure portfolio continued to be a pillar of

stability for the overall portfolio. The return was 4.5%, buoyed

primarily by transportation assets. Its benchmark index was 8.1%,

boosted by the public stocks that compose it, which continue to be

stimulated by the energy demand driven by artificial intelligence. In an

environment that remains competitive due to the asset class’s

particularly attractive profile, the teams were proactive. They

completed nearly $4 billion of acquisitions, primarily abroad, in

sectors such as telecommunications, data centres and power transmission.

They also made targeted strategic sales to materialize gains and ensure

portfolio turnover.

Over five years, the annualized return

was 11.2%, compared with 9.0% for the index. The portfolio once again

benefited from sound asset diversification and its favourable

positioning in promising sectors, including renewable and transition

energy, ports, highways and telecommunications.

Real Estate: Overall stabilization of the portfolio

In

the first half of the year, the portfolio earned a 0.1% return,

compared with the 1.2% return of its benchmark. The vast majority of

sectors that make up the portfolio saw their values stabilize during the

six‑month period. Shopping centres and offices posted good current

yields after the pandemic shock. However, performance was limited by the

impact of the higher-rate environment.

Over five years, the

annualized return on the portfolio stands at 0.3%, in line with its

index at 0.4%, reflecting the cyclical and structural challenges

affecting the entire industry in recent years. The difference with the

index is mainly due to the portfolio’s longstanding concentration in the

U.S. office sector, which experienced difficulties over the period. It

should be noted that the sectoral repositioning of the real estate

portfolio toward sectors of the future, such as logistics, since 2020

was favourable over five years.

Impact of currencies on returns

In

the first half of the year, the portfolio’s exposure to foreign

currencies adversely impacted overall performance, mainly due to the

sharp depreciation of the U.S. dollar. The partial hedging of this

currency implemented by the teams, however, offered significant

protection, offsetting nearly half of the negative impact. Over five

years, foreign currency exposure contributed positively to overall

performance, mainly due to the strength of the U.S. dollar over the

period and the portfolio’s large exposure to it.

Québec: Support for local companies and structuring projects as the global economy redefines itself

The

beginning of the year helped consolidate the positions of some Québec

leaders in strategic industries, in addition to continuing to advance

structuring projects. Highlights included:

Support to grow companies

Innergex: Announcement of the acquisition of this renewable energy leader, bringing the enterprise value to $10 billion

Norda Stelo:$28 million

for an equity stake in this impact engineering leader, following two

years as a lender, thereby reinforcing our partnership focused on

sustainable innovation

Germain Hotels: Leading a financing round for a total of $160 million to accelerate its expansion, and support for the company’s succession

Synex Business Performance:

Equity stake as a minority shareholder and support in the form of debt

for this growing company in the Canadian insurance brokerage sector

Structuring projects

REM:

Migration of all operations to Brossard and start of the test period on

two new branches (Deux-Montagnes and Anse-à-l’Orme) before the dry run

stage at the end of the summer

Québec-Toronto high-speed train:

The Government of Canada selected the Cadence team, led by CDPQ Infra,

as a private partner of Alto, the federal Crown corporation responsible

for carrying out this major project for Canadian mobility

TramCité:

Announcement of consortia qualified for two major contracts as part of

requests for expressions of interest led by CDPQ Infra; ultimately, this

new 19-km modern tramway network will become the backbone of mobility

in the Québec City region

Financial reporting

Cost

management remains a priority for the organization. As such, the

integration of the real estate subsidiaries, Ivanhoé Cambridge and Otéra

Capital, into La Caisse, continued to benefit from the full potential

of a simplified organization and to generate efficiency gains. Note that

this integration, which began last year, will conclude in 2026. The

synergies achieved already represent annual savings beyond the initial

target of $100 million. Information on internal and external investment

management costs as at December 31 will be presented in the

annual disclosure.

The credit rating agencies reaffirmed

La Caisse’s investment-grade ratings with a stable outlook, namely AAA

(DBRS), AAA (S&P), Aaa (Moody’s) and AAA (Fitch Ratings).

ABOUT LA CAISSE

At La Caisse, formerly CDPQ, we have invested for 60 years with a

dual mandate: generate optimal long-term returns for our 48 depositors,

who represent over 6 million Quebecers, and contribute to Québec’s

economic development.

As a global investment group, we are active

in the major financial markets, private equity, infrastructure, real

estate and private debt. As at June 30, 2025, La Caisse’s net assets

totalled CAD 496 billion. For more information, visit lacaisse.com or consult our LinkedIn or Instagram pages.

Earlier today, I had a chance to catch up with Vincent Delisle, Executive Vice President and Head of Liquid Markets to go over mid-year results.

I want to begin by thanking him for taking some time to share his insights and also thank Marjaurie Côté-Boileau for setting up the Teams meeting and graciously allowing me an extra five minutes to talk to Vincent (I need a minimum of 20 minutes to cover these results properly, maximum of 30).

Vincent began by giving me an overview of the results:

I'll start it off with our overall performance numbers, 4.6% in terms of returns, ahead of our index which stands at 4.3%. The 5-year numbers are attractive, 7.7% versus 6.6%, ahead of the benchmark. And over a 10-year window, we're at 7% versus 6.4%.

So quite happy with the results. Aside from real estate which had flat numbers, we're getting contribution from the other asset classes which is welcome news in this environment which as you know is very much public equity driven, very concentrated still albeit less concentrated in the first half and we are getting contribution from all our portfolios.

I asked him for his insights in public markets including fixed income:

I'll start off with public equities. Amidst all the negotiations on tariffs and all the uncertainty, public equity markets are doing quite well year-to-date mainly driven by Canada and emerging markets which are two big weights in our portfolio.

We came in at 6%, the Public Equity portfolio, our benchmark is 5.5%. I think the Equity is at 4.4%, so we executed well versus our benchmark and we beat the Equity portfolio so the strategic decisions paid off (he clarified, the strategic decision was being underweight USequities versus the Equity index).

5-year numbers look good, 13.3%, ahead of the benchmark at 12.9%. We are quite happy with this because markets have been complicated. It's been almost non-stop Risk On over the last five years, very concentrated.

When I joined in 2020, similar to when Charles became CEO, that's when we implemented many strategic initiatives in public equities: we increased the beta, we added more growth exposure, and we went quant. All that has paid off, we are back to a 5-year window of outperformance in that portfolio.

I interjected to ask him about the quant vs value strategies as I'm sure quant strategies got whipsawed around Liberation Day and then came back when markets starting trending back up again (they're mostly trend followers and don't do well in a highly volatile environment).

Vincent replied:

Yes, and you and I have had this discussion almost every six months, quant portfolios, both internal and external had a more volatile swing in March and April but they quickly came back, and I'm impressed with how quickly performance came back with these quantitative strategies.

One thing I'll point out, the old fashion way of managing money -- fundamental equities -- it is still a tough environment. Very tough environment because if you look at what has been driving equities over the last few months, meme stocks have come back, crypstos have been rallying as has non-profitable growth. So quants style still performing very well this year. The fundamental toolkit is still having a tough time because quality is getting smoked out there.

I told him he's right, the Goldman Sachs Non-Profitable Tech Index surged higher after hitting a low in April and I'm seeing A LOT of silliness trading these markets. The same for meme stocks and crypto related equities, etc. I told him "all this garbage is rallying because that's where the quant funds love to execute their strategy, squeezing short sellers."

I added if I look at US indices, valuations are at extremes whether it's historical or forward price to earnings or price-to-sales and I asked him if that gives him cause for concern.

Vincent replied:

One thing I'll point out here, I don't think you can blame quant strategies for the market's lack of rationality. I would look at another direction, namely, S&P ETF retail money that has been dominating trading.

When you look at systematic trading strategies but especially retail ETF coming in, the market has been driven by retail flows, almost double the flows over the last five years versus the 2010-2020 time frames. So the fundamental toolkit used by pension funds and institutional money is not having fun right now in this market.

Is the US market expensive? Absolutely. Are we concerned about this? Absolutely.

Over the last 5 years, we increased our US equity exposure from 40sh% to 50% of the Public Equity portfolio. We are going to stop at 50%. This is as high as we want to go. I don't want to do anything drastic because it's probably too soon to call the end to US equity outperformance but we want to be more diversified in looking for pockets of opportunities in Europe and in Asia.

I told Vincent he just made two good points. First, according to professor Campbell (Cam) Harvey, retail investor trading combined with the increasing dominance of passive investing works against market efficiency (see this LinkedIn post and clip below). Basically, Cam demonstrates how passive indices routinely invest in expensive, slow growth stocks, which creates a sizeable performance drag (see this more recent LinkedIn post).

The second thing Vincent mentioned was they capped their US equity exposure to 50% and I asked him whether US stocks dominated by Big Tech names make up 40% or 50% of MSCI World Equity Index?

He replied: "It's close to 60%, I can get a specific number for you later but it's above 60%."

I interjected, even if MSCI World is above 60% US equity exposure, La Caisse is still not going to exceed 50% in US public equity exposure.

He replied:

Yes, we stop at 50. This is where you're probably the only one who will understand my answer.

Our reference portfolio has 20% Canada and 12.5% emerging markets.

So when I refer to our US exposure on a relative basis, it's based on our reference portfolio, we are neutral US public equities versus our reference portfolio.If you compare us to the average Joe out there or the MSCI World, we are underweight US public equities because we are overweight Canada.

[Note: I guess I'm the average Joe because for the last 15 years, I only trade US stocks :) ].

We moved on to Fixed Income where Vincent shared this with me on that portfolio's performance in the first half of this year:

Fixed income, we're quite happy with the numbers. 3.9% performance in the first half versus 3% (for the benchmark).

We benefited from two things that we have not seen in a while. First thing is the yield on the fixed income portfolio was 2.8%, we clipped the coupon and we are exposed to US duration. US 10-year Treasury yields went down so that also helped.

We had a combination we had not seen in a few years. First half, yields had great movements that helped us. We had some strong numbers from our credit portfolio, especially in emerging market debt where we are exposed to Latin America, Brazil and Mexico. Yields went down there and currencies appreciated. It was a pretty nice semester for our emerging markets business. Pretty much every cylinder in our credit portfolio performed well.

Obviously, the divergence in yields favoured us because we have US duration exposure. The divergence with US 10-year yields going down and yields going up in Canada, Europe, Japan and the UK was also an interesting development alongside with the weaker US dollar.

So whether it's for our public equity strategy or fixed income strategy, we are very much in tune with these developing trends.

I think the currency is telling you US exceptionalism is in jeopardy. If the DXY comes back down and resumes its downtrend, it will have an impact on where flows will be heading and it's certainly something we are looking at whether it's on the fixed income or equity side.

We had successful strategies in steepening. Our steepening call helped us both in asset mix and in fixed income.

Time was running out so we shifted focus to private markets. I told him I spoke yesterday to Jo Taylor, Gillian Brown and Stephen McLennan on OTPP's mid-year results and we discussed how illiquid alternatives are experiencing a period of adjustment whereas liquid alternatives (ie hedge funds) are performing well.

I told him I saw the Private Equity numbers and they looked decent and asked him to give me some colour on private markets.

Vincent shared this:

I'll cover Private Equity, Infra and Real Estate, the key highlights.

Private Equity performance is 3.4% which is ahead of the benchmark at 2%. We're quite happy to see that the profitability of our investments, our companies in the portfolio, continues to grow. We are invested in the right companies. High interest rates are still hampering M&A activity and that's one of the highlights in this asset class.

The numbers for Private Equity on a 5-year basis are quite attractive as well, 16.7% versus a benchmark performance of 15%.

Obviously when you have public equities indices rallying like this, it is a more challenging environment for privates. We're seeing it in Private Equity but it's also having an impact in our Infra portfolio.

Infrastructure is very stable, delivering semester in, semester out, a performance of 4.5%. Our Infra portfolio has been punching in numbers of 9-10% almost constantly on a yearly basis. The yield is attractive, we are invested in sectors that are performing well such as transports.

Underperforming the benchmark in Infra mainly because the public equity index for Infra is loaded up in AI and energy related names.

But Infra in the alternatives and privates is certainly an area where we have been increasing or exposure, we continue to like the asset class.

I told Vincent I noticed the Private Credit portfolio at La Caisse now falls under the jurisdiction of Private Equity and he responded:

Private Credit and Private Equity are under the same leadership, Martin Longchamps who I think you probably knew at PSP (don't recall ever meeting him).

Private Credit is in the Fixed Income portfolio. I oversee the Credit portfolio and Martin Longchamps oversees the Private Credit aspect of it. The Credit portfolio has a lot of public credit in there and a lot of public emerging market debt as well.

He then went on to discuss trends in La Caisse's real estate portfolio:

Real Estate continues to be challenging. Although it's only a six month window, we are quite happy with some encouraging signs we are seeing in the office market. The back to the office we are seeing in Toronto, New York and other North American cities, so it seems to be stabilizing there.

Performance was 0.1% in Real Estate, the index is at 1.2%.

The high yield environment continues to be a struggle for the asset class but we are repositioning. We have a new team leader, Rana Ghorayeb who took over and she's working on stabilizing that portfolio.

I noted it's the same situation pretty much everywhere with real estate, challenges persist in offices, logistics and multifamily continue to perform well but higher rates are a challenge.

I asked Vincent one last question on the uncertainty in markets focusing on inflation versus growth and what they see on the macro front.

He responded:

We are very cautious. Although everyone has been talking about tariff risks for the last 4,5, 6 months, we now have much more tariff clarity, meaning we know the numbers that will be paid out by the US trading partners.

Year-to-date the US economy has shown some resilience but there are some pockets of weakness that we witnessed recently like in employment and domestic demand.

When you separate the US economic outlook excluding all the AI capex related spending, business spending has been quite weak.

We are expecting in the next few months the inflation numbers will not be as friendly as what we've seen recently so there's a risk that long bond yields could move higher. The US economy could face a real threat over the next few months. We are not negative, we are not bearish but after such a phenomenal rebound from the Liberation Day lows, it's show me time for the US economy and we're much more cautious for the remainder of the year.

Did you get that last point, more US inflation, higher yields? Start trimming your Mag 7 exposure (Meta shares just shy of $800!!) and hang on to your hats as we hit September to December, will be a bumpy ride (maybe, who knows, stocks can continue melting up despite higher yields but I doubt it).

Alright, it's really late, let me wrap it up there.

Below, as I promised Vincent, professor Campbell Harvey argues that the surge in retail investor trading combined with the increasing dominance of passive investing works against market efficiency.

Cam, who I met at La Caisse over 20 years ago, demonstrates that passive indices routinely invest in expensive, slow growth stocks, which creates a sizeable performance drag and he quantifies the scale of that underperformance and offers solutions (see second and third clip).

Fourth, Rick Rieder, BlackRock global fixed income CIO, joins 'Closing Bell' to discuss Rieder's thoughts on the current investing environment, if the Fed will cut rates in September and risks to equity markets.

Lastly, Warren Pies, 3Fourteen Research co-founder, joins 'Closing Bell' to discuss their decision to downgrade equities in July, why there's so much cash on the sidelines and much more.

Comments

Post a Comment