CPPIB's Assets Top $400 Billion in Fiscal Q1

Highlights:I've covered many of these deals and typically don't cover CPPIB's quarterly results, just like I didn't cover the Caisse's mid-year results which were solid as it returned 6.1% as at the end of June:

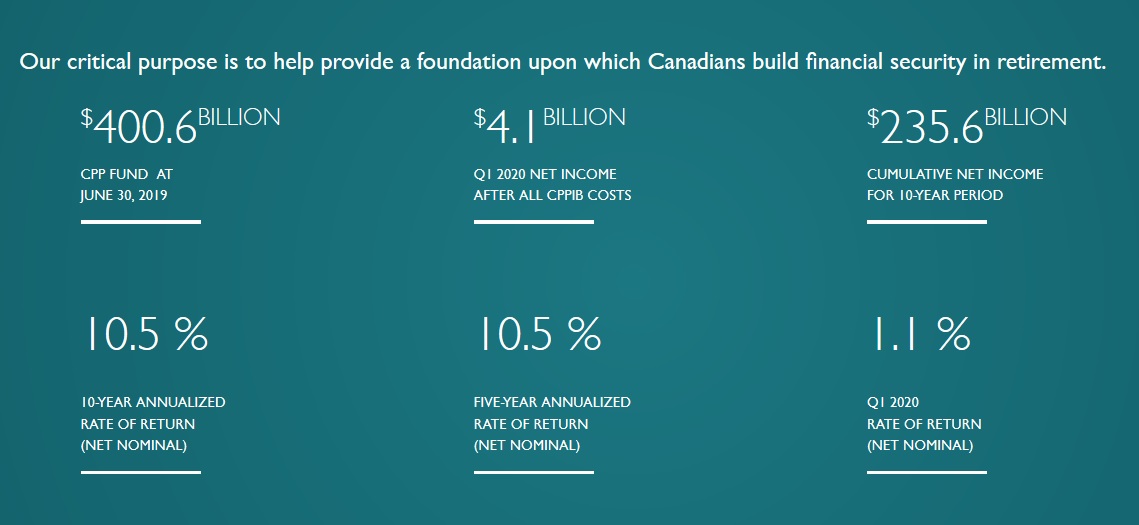

The $8.6 billion increase in assets for the quarter consisted of $4.1 billion in net income after all CPPIB costs and $4.5 billion in net Canada Pension Plan (CPP) contributions.

- Net assets surpass $400 billion

- 10-year and five-year returns of 10.5% each

- $4.1 billion in net income generated for the Fund this quarter

The Fund, which includes the combination of both the base CPP and additional CPP accounts, achieved 10-year and five-year annualized net nominal returns of 10.5% each. For the quarter, the Fund returned 1.1% net of all CPPIB costs.

“CPPIB’s investment programs performed well in the first quarter, achieving solid net income in local-dollar terms,” says Mark Machin, President & Chief Executive Officer, CPPIB. “At the same time, the strengthening of the Canadian dollar against all major currencies in June dampened our returns overall, as the market responded to lower interest rate expectations in the U.S. and Europe.”

The Total Portfolio Management department was the top contributor, in part due to gains in fixed income investments. Both the Private Equity and Active Equities departments also delivered positive results, supported by the improved sentiment in global equity markets.

CPPIB continues to build a portfolio designed to achieve a maximum rate of return without undue risk of loss, taking into account the factors that may affect the funding of the CPP and the CPP’s ability to meet its financial obligations. The CPP is designed to serve today’s contributors and beneficiaries while looking ahead to future decades and across multiple generations. As a comparative advantage, an extended investment horizon helps to define CPPIB’s strategy and risk appetite. Accordingly, long-term results are a more appropriate measure of CPPIB’s investment performance compared to quarterly or annual cycles.

Performance of the Base and Additional CPP Accounts

The base CPP account ended its first quarter of fiscal 2020 on June 30, 2019 with net assets of $399.7 billion, compared to $391.6 billion at the end of fiscal 2019. The $8.1 billion increase in assets consisted of $4.1 billion in net income after all costs and $4.0 billion in net base CPP contributions. The base CPP account achieved a 1.1% net return for the quarter.

The additional CPP account ended its first quarter of fiscal 2020 on June 30, 2019 with net assets of $0.9 billion, compared to $0.4 billion at the end of fiscal 2019. The $0.5 billion increase in assets consisted of $0.01 billion in net income and $0.5 billion in net additional CPP contributions. The additional CPP account achieved a 1.5% net return for the quarter.

Long-Term Sustainability

Every three years, the Office of the Chief Actuary of Canada conducts an independent review of the sustainability of the CPP over the next 75 years. In the most recent triennial review, the Chief Actuary of Canada reaffirmed that, as at December 31, 2015, the base CPP remains sustainable at the current contribution rate of 9.9% throughout the forward-looking 75-year period covered by the actuarial report.

The Chief Actuary’s projections are based on the assumption that, over the 75 years from 2015, the base CPP investments will earn an average annual rate of return of 3.9% above the rate of Canadian consumer price inflation, after all investment costs and CPPIB operating expenses. The corresponding assumption is that the additional CPP investments will earn an average annual real rate of return of 3.55%.

The Fund, combining both the base CPP and additional CPP accounts, achieved 10-year and five-year annualized net real returns of 8.6% and 8.8%, respectively.

Operational Highlights:

Q1 Investment Highlights:

- In June 2019, we opened a workspace in San Francisco to better access investment opportunities and deepen relationships within the technology ecosystem. Professionals from investment departments such as Private Equity and Active Equities will be represented in this location. This office becomes the ninth global location for CPPIB and our second U.S. location after New York, which opened in 2014.

- We built upon the enhanced Integrated Risk Framework introduced in fiscal 2019 to implement an additional set of risk limits that cover both financial and non-financial risks. The Integrated Risk Framework together with the related new risk limits provide a fuller representation and enhanced governance over the different dimensions of the various risks that we are managing. The new risk limits do not materially change the level of risk the Fund is exposed to.

Private Equity

Real Assets

- As part of a consortium, agreed to terms of a recommended offer to purchase Merlin Entertainments plc at a price of 455 pence per share in cash for the entire issued, and to be issued, share capital of Merlin, other than shares already owned by consortium partner KIRKBI. Merlin is a global leader in location-based family entertainment.

- Closed a transaction to invest an incremental £95 million in Visma, a leading provider of business management software and services in the Nordic and Benelux regions, increasing total investment to £200 million, and ownership to 4.7%.

Credit Investments

- Established Maple Power, a 50/50 Joint Venture with Enbridge, to invest in offshore wind projects in Europe at various stages of development following an initial transaction to purchase renewable power assets from Enbridge in 2018.

- Signed a Memorandum of Understanding with Piramal Enterprises to co-sponsor a Renewables InvIT that will acquire operating renewable assets in India. We will hold a majority stake, with an initial target investment of approximately $300 million, with Piramal and other long-term investors holding the remaining interest.

Active Equities

- Acquired a portion of LifeArc’s royalty interests on worldwide sales of Keytruda® (pembrolizumab) for approximately US$1.3 billion. Keytruda is an anti-PD-1 therapy developed and commercialized by Merck (known as MSD outside the U.S. and Canada).

Asset Dispositions

- Invested $200 million in Premium Brands Holdings, for an ownership stake of approximately 7.1%. Premium Brands is a leading producer, marketer and distributor of specialty food products in Canada and the U.S.

Transaction highlights following the quarter end include:

- Agreed to sell Acelity Inc. for a total value of approximately US$6.725 billion alongside our consortium of Apax Partners and the Public Sector Pension Investment Board. Acelity is a leader in negative pressure wound therapy, specialty surgical and advanced wound dressing products.

- Agreed to vote in favour of the acquisition of Advanced Disposal Services, in which we have a 19% stake, by Waste Management. The transaction is subject to customary closing conditions, and net proceeds are expected to be US$549 million. Advanced Disposal provides waste collection, disposal and recycling services in the United States.

About Canada Pension Plan Investment Board

- As part of a consortium, announced our agreement to merge the Refinitiv business, one of the world’s largest providers of financial markets data and infrastructure, with the London Stock Exchange Group plc in an all-share transaction for a total enterprise value of approximately US$27 billion.

- Agreed to acquire a stake in Waystar, a leading cloud-based provider of revenue cycle technology, alongside the EQT VIII Fund, which values the business at US$2.7 billion. The seller, Bain Capital, will retain a minority stake in the company.

- Agreed to invest A$136 million, as part of the Dexus Office Trust Australia (DOTA) partnership, to acquire office buildings in Sydney, Australia including 3 Spring Street and a portion of 58 Pitt Street.

- Completed the sale of our 40% stake in Solveig Gas HoldCo A/S, a company that held a 25.6% stake in Gassled, a natural gas transport network in Norway.

- Announced plans to sell Liberty Living, a wholly-owned student accommodation business, to the Unite Group plc for cash proceeds of approximately $1.3 billion, retaining a 20% share in the combined group.

- IndInfravit Trust, in which CPPIB is a founding investor, has agreed to purchase the entire equity shareholding in nine Indian operational road projects from Sadbhav Infrastructure Project Ltd. The transaction values 100% of the portfolio at an enterprise value of approximately INR 66,100 million. IndInfravit Trust is an infrastructure investment trust based in India.

Canada Pension Plan Investment Board (CPPIB) is a professional investment management organization that invests the funds not needed by the Canada Pension Plan (CPP) to pay current benefits in the best interest of 20 million contributors and beneficiaries. In order to build diversified portfolios of assets, CPPIB invests in public equities, private equities, real estate, infrastructure and fixed income instruments. Headquartered in Toronto, with offices in Hong Kong, London, Luxembourg, Mumbai, New York City, San Francisco, São Paulo and Sydney. CPPIB is governed and managed independently of the Canada Pension Plan and at arm's length from governments. At June 30, 2019, the CPP Fund totalled $400.6 billion. For more information about CPPIB, please visit www.cppib.com or follow us on LinkedIn, Facebook or Twitter.

The reason why I don't cover these mid-year and quarterly results is because these are large pension funds and what ultimately counts is annual and more importantly, long-term results (5,10,15 and 20 year performance).

CPPIB's assets topped $400 billion in its fiscal Q1 but as global equities get roiled in fiscal Q2, its assets will suffer too but not as much as people think because of its strategy to be well-diversified across public and private markets throughout the world.

If we go into a prolonged bear market, I expect CPPIB and other Canadian pensions will get hit but not as much as if they were only invested in stocks and bonds. This is why the focus has been on real assets, private credit and private equity.

CPPIB's long-term results are excellent, well-above its actuarial target rate-of-return, and that it is what ultimately counts the most, the long-term sustainability of the Canada Pension Plan (base and enhanced).

In related news, CPPIB just announced it is increasing its stake in Highway 407 International:

A company controlled by Canada Pension Plan Investment Board (CPPIB) has acquired a 10.01% equity stake of 407 International Inc. (407 International), which holds a concession over the 407 Express Toll Route (407 ETR), from SNC-Lavalin Group Inc. (SNC-Lavalin). Under the terms of the agreement, CPPIB agreed to pay $3.0 billion to SNC-Lavalin on closing, with an additional $250 million set to be paid over 10 years, conditional on achieving certain financial targets related to the performance of the toll highway.I wrote about OMERS, CPPIB and Highway 407 back in May and stated: "I'm not sure if CPPIB or Ferrovial will exercise the right of first refusal over any proposed sale of SNC-Lavalin's stake but given the sums involved, I wouldn't be surprised if either of them do."

CPPIB has been an investor in 407 International since 2010, when it acquired control of a 40% holding in the business through two separate transactions. Located in Ontario, Canada, 407 ETR is the world’s first all-electronic, barrier-free toll highway, stretching 108 km and serving more than 400,000 drivers each weekday.

“CPPIB invests in global infrastructure assets that offer predictable, resilient income streams in attractive locations. Toll roads provide CPPIB the opportunity to benefit from urbanization trends and invest in assets that benefit from the growth of a region,” said Scott Lawrence, Managing Director, Head of Infrastructure, CPPIB. “The 407 ETR continues to be an attractive infrastructure investment for all these reasons, and remains a good strategic fit with CPPIB’s portfolio and exceptionally long investment horizon. We are pleased to increase our investment in a company with great management, dedicated to delivering a valuable service to so many.”

CPPIB has a diversified, global portfolio of infrastructure assets and makes direct investments through many of its nine offices worldwide. CPPIB’s Infrastructure group is focused on investing in quality, large-scale core opportunities with dependable, like-minded partners.

Upon completion of the transaction, CPPIB controls a 50.01% stake in 407 International.

Well, CPPIB did exercise its right of first refusal and won a court case against Ferrovial, the other majority owner of the 407 ETR.

A research analyst from BNN Bloomberg recently contacted me to ask me if "CPPIB, being the majority shareholder now of the 407, could raise tolls as they please or would they have to go through a certain process?"

Someone from CPPIB shared this with me:

The immediate answer to the question is a categorical and absolute “no”.I agree, however, another expert told me "even though CPPIB and Ferrovial don't make the final decision on tolls, they have a seat on the board of the 407 ETR and definitely have a say on tolls."

A toll road (and we have significant investments in this type of infrastructure all over the world including roads in Chile, USA, India and Australia) for an institutional investor like CPPIB is not any different from the thousands of assets we seek to hold according to desired risk-adjusted returns. We seek long-dated, predictable returns to support the sustainability of the overall global portfolio. Whether it is a textile manufacturer, pharmaceuticals, film distribution, a shopping centre, river cruise line, we are always an investor and NEVER the operators or managers. We manage financial spreadsheets not companies and we especially don’t have the expertise to influence pricing at any company including something like the 407.

He also shared this with me:

"The Government of Ontario did a 100-year concession deal on the 407, it was a terrible deal for the government and consumers because they are allowed to raise rates as long as a minimum level of traffic is maintained, which is has consistently been maintained and surpassed. Typically, other toll road concessions are 40 or 50 years and are only allowed to raise rates by CPI (inflation)."In any case, it's fair to say the 407 ETR has been a great investment for CPPIB and Ferrovial, and that's why SNC-Lavalin held on to its stake for as long as possible and why OMERS desperately wanted a piece of that pie.

This toll road remains one of the best investments in CPPIB's portfolio and it was absolutely right to exercise its right of first refusal.

Below, a clip going over how CPPIB performed for the first quarter of its fiscal year, and what this means for its contributors and beneficiaries.

And Mark Machin, President and CEO of CPPIB, went over its long-term strategy when he spoke with BNN Bloomberg's Amanda Lang back in May. Great interview, he covered all the important points. For more details, read my comment going over CPPIB's fiscal 2019 results.

Comments

Post a Comment