Palash Gosh of Pension & Investments reports CDPQ posts 7.2% return in 2023:

Caisse de Depot et

Placement du Quebec, Montreal, delivered a net return of 7.2% in

calendar year 2023, slightly below the benchmark return of 7.3%.

For the five-year period, CDPQ

returned an annualized 6.4%, above the 5.9% of the benchmark, said a

Feb. 22 release. Over the 10-year period, the annualized return was

7.4%, compared with 6.5% for the benchmark.

As of Dec. 31, CDPQ's net assets totaled C$434 billion ($327.4 billion), up from C$402 billion at the end of 2022.

In 2022, CDPQ returned a net -5.6%, above the benchmark return of -8.3%.

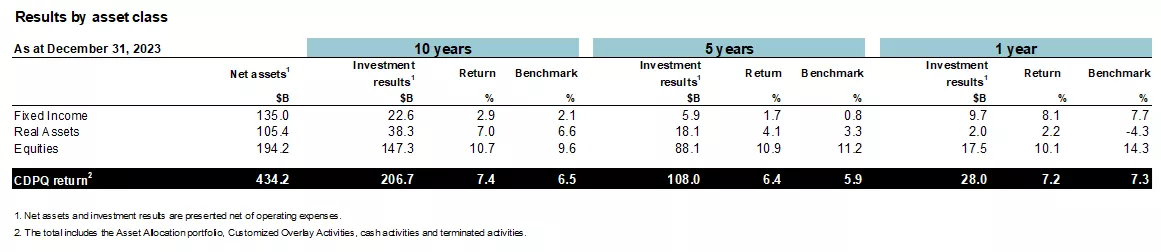

For 2023, by asset class, equities,

which comprises equity markets and private equity, returned a net 10.1%,

below its benchmark of 14.3%.

For the five-year and 10-year periods,

equities returned a net 10.9% and 10.7%, respectively, compared with

benchmarks of 11.2% and 9.6%.

With respect to public equities, CDPQ

noted that since 2020, a "few large public U.S. tech companies have

dominated the performance of the main stock indexes, creating a

phenomenon of historically concentrated gains," CDPQ said in the

release. CDPQ's own public equities portfolio saw its performance

"driven by growth stocks, as well as by large positions in Quebec

companies, which performed well."

The private equity

portfolio was affected by interest rate hikes as well as by an increase

in financing costs, which affected certain private companies.

"This slowdown was expected after the

portfolio produced considerable returns in recent years," CDPQ noted.

"Some sectors were hit harder, including healthcare as it returned to

normal activities following years of high volumes related to the

pandemic. In contrast, private investments in Quebec generated good

returns."

Fixed income returned a net 8.1%, above its benchmark of 7.7%, in 2023.

For the five-year and 10-year

periods, fixed income returned a net 1.7% and 2.9%, respectively,

compared with benchmarks of 0.8% and 2.1%.

Regarding the pension

fund's bond assets, CDPQ said the fixed income market was characterized

by higher yields and the narrowing of corporate credit spreads.

"Volatility remained a highlight

during the year: 10‑year bond yields fluctuated between 3.3% and 5.0%,

finishing the year stable in the U.S. and down 0.2% in Canada," CDPQ

added.

CDPQ partly attributed the one-year

outperformance of fixed income to the portfolio's "positioning in

government debt, which benefited from lower rates in certain emerging

countries, good execution in corporate credit and premiums on private

debt that foster a high current return."

Real assets (which comprise the real

estate and infrastructure portfolios) returned a net 2.2%, but that

still beat its benchmark of -4.3%.

For the five-year and 10-year

periods, real assets returned a net 4.1% and 7%, respectively, compared

with benchmarks of 3.3% and 6.6%.

Concerning its real assets portfolio,

CDPQ noted that the real estate sector had to contend with structural

trends in its industry, while the infrastructure portfolio "sustained

its momentum of recent years by continuing to provide a good combination

of protection against inflation and attractive current returns."

Within infrastructure, assets in

essential sectors such as transportation and renewable energy were among

the performance drivers in 2023.

Mathieu Dion of Bloomberg reports Quebec pension hit with real estate loss as 'hostile' market persists:

Quebec’s public pension manager reported a

7.2 per cent return in 2023, as losses in real estate detracted from big

gains in its credit and stock portfolios.

Caisse de Depot et Placement du Quebec has restructured its real

estate business, shifting capital to apartments and industrial

properties, but it wasn’t enough to offset problems in the office

sector. The fund manager posted a 6.2 per cent loss on its $46 billion

property portfolio — the only asset class for which it had a negative

return last year.

Nathalie Palladitcheff, the head of Ivanhoe Cambridge, CDPQ’s real

estate arm, described last year’s environment as “hostile.” High

interest rates and low occupancy have created a difficult outlook for

office owners and their lenders, with more than $1 trillion in

commercial real estate loans set to mature by the end of next year.

“The increase in rates impacts both the valuation and the cost of

debt, and this resulted in a very significant drop in transactional

volumes on a global scale,” Palladitcheff said, referring to the broader

real estate market. “They have been halved in Europe, halved in the

United States, even an 80 per cent drop in transactions in Germany, for

example.”

In equity markets, Canada’s second-largest pension fund benefited

from its high exposure to the technology sector with a 17.7 per cent

gain.But CDPQ’s private equity portfolio recorded just a 1 per cent

increase, as rising financing costs impacted private companies.

The fund’s net assets grew by $32 billion to end last year at $434

billion. It’s a shift from 2022’s results, when the firm posted its

worst annual return since the global financial crisis.

CDPQ’s assets under management have grown by almost $100 billion since the beginning of 2020.

“We may reach a crossroads in the year ahead, with many central banks

likely to pivot, but the scope and sequence remain unknown,” CDPQ Chief

Executive Officer Charles Emond said in a statement. “With a backdrop

of downward but persistent inflationary pressure combined with lingering

volatility, our portfolio remains well-positioned to keep delivering

the long-term returns our depositors need.”

Earlier today, CDPQ issued a press release stating it posted a 7.2% one-year return and net assets reached $434 billion, up $32 billion:

CDPQ today presented its financial results for the year

ended December 31, 2023. The weighted average return on its depositors’

funds was 7.2% in 2023, in line with its benchmark portfolio’s

7.3% return. Over five years, the annualized return was 6.4%, outpacing

the 5.9% of the benchmark portfolio, which represents close to

$12 billion in value added. Over ten years, the annualized return

was 7.4%, also higher than its benchmark portfolio which stood at 6.5%,

producing over $28 billion in value added. As at December 31, 2023,

CDPQ’s net assets totalled $434 billion.

“The

year 2023 was marked by highly volatile bond markets and a historic

concentration of gains from a handful of U.S. tech stocks that drove the

main stock indexes. Faced with this context, our portfolio performed

well, and our depositors’ plans continue to be in excellent financial

health,” said CharlesEmond, President and Chief Executive Officer ofCDPQ.

“Since

2020, investors have had to weather market conditions that ranged from

one extreme to the other. In such environments, our portfolio has grown

by nearly $100 billion over the period. We may reach a crossroads in the

year ahead, with many central banks likely to pivot, but the scope and

sequence remain unknown. With a backdrop of downward but persistent

inflationary pressure combined with lingering volatility, our portfolio

remains well positioned to keep delivering the long-term returns our

depositors need,” concluded CharlesEmond.

Return highlights

In

the past few years, there has been a more pronounced variation in

returns, year over year, in most asset classes. This is particularly the

case for stock and bond markets, which, following a severe and

simultaneous correction in 2022, bolstered CDPQ’s performance in 2023.

Following a period of considerable returns, private equity was affected

by the sharp rise in rates and the economic slowdown. Impacted by the

same economic factors, the Real Estate portfolio—which posted the best

return in 2022—also had to contend with structural trends in its

industry. The Infrastructure portfolio sustained its momentum of recent

years by continuing to provide a good combination of protection against

inflation and attractive current returns.

CDPQ manages the funds

of 48 depositors and adapts investment strategies to meet their

objectives, taking into account their different risk tolerances and

investment policies. The portfolio’s one-year, five-year and ten-year

returns represent the weighted average of these funds. In 2023, the

spread in the returns for CDPQ’s eight main depositors was fairly wide,

ranging from 6.3% to 9.3% for one year. Over longer periods, the

annualized return on their funds varied between 4.9% and 7.3% over

five years, and between 6.2% and 8.3% over ten years.

CDPQ’s investment results totalled $28 billion for one year, $108 billion over five years and $207 billion over ten years.

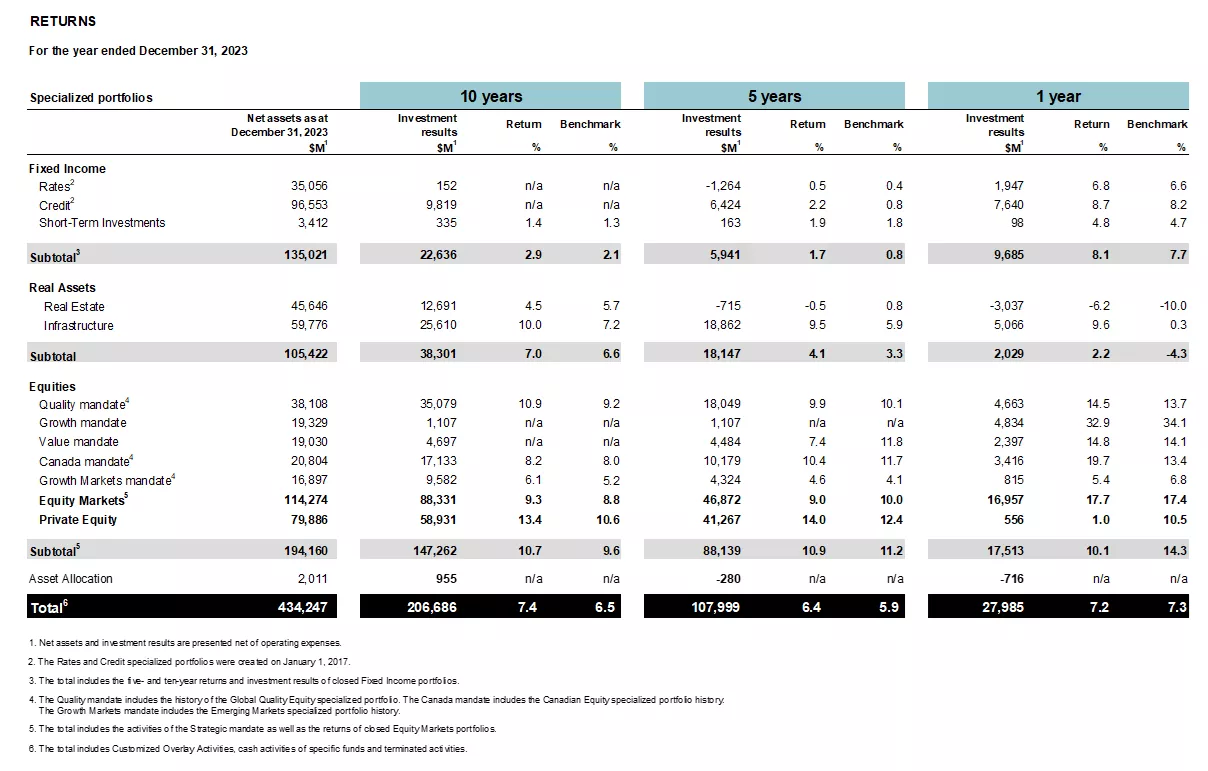

Fixed Income: Bonds lifted by higher yields, outpace their index

The

2023 bond market was characterized by higher yields and the narrowing

of corporate credit spreads. Volatility remained a highlight during the

year: 10‑year bond yields fluctuated between 3.3% and 5.0%, finishing

the year stable in the United States and down 0.2% in Canada. For

one year, the asset class posted an 8.1% return, compared with 7.7% for

its benchmark index. This return is in part attributable to the

portfolio’s positioning in government debt, which benefited from lower

rates in certain emerging countries, good execution in corporate credit

and premiums on private debt that foster a high current return.

Over

five years, the asset class posted a 1.7% annualized return, which was

limited by the weaker performance in 2022 in the wake of historic rate

hikes, but remains above its index’s 0.8% return. Over the period, it

benefited from private credit activities, an important driver of

performance, thanks in part to the high current return on this kind of

debt and the favourable execution of all mandates.

Real Assets

Real

Assets is a class composed of the Real Estate and Infrastructure

portfolios, which have quite different industry challenges.

Infrastructure: Assets that continue to perform well against inflationary pressure

In

2023, the portfolio continued its good performance of recent years,

generating a 9.6% return against an index at 0.3%. Assets in essential

sectors such as transportation and renewable energy were among the

performance drivers, as was the current return. With slower transaction

activity in 2023, the team remained disciplined in managing its

portfolio, both in selecting acquisitions and in sales and syndication

activities.

Over five years, the annualized return was 9.5%, above

its index’s 5.9%, primarily due to investments in renewable and

transition energy and in port and telecommunications assets.

Real Estate: Lower performance, but above the index in a transforming industry

The

market was difficult for real estate in 2023, which is reflected by the

benchmark index’s -10.0% one-year return. Despite economic challenges

and structural issues in some sectors such as offices, the Real Estate

portfolio demonstrated more resilience, and the repositioning toward

promising sectors such as logistics that began in 2020 mitigated the

decrease in value. As such, the portfolio recorded a -6.2% return for

one year, above its index. In 2023, teams remained selective in the

slowest transactional market in 15 years, with acquisitions in promising

sectors of the future aligned with the portfolio’s evolution, as well

as disciplined dispositions.

Over five years, the annualized

return was -0.5%, compared with 0.8% for the index, notably due to the

portfolio’s overweighting in Canadian shopping centres at the beginning

of the period. The strategic repositioning over the last few years,

which represented around 300 transactions totalling over $50 billion, is

nevertheless bearing fruit: since the pivot, $5.5 billion in value

added has been generated compared with the benchmark index.

Equities

The

Equities asset class is composed of Equity Markets and Private Equity,

which have seen vastly different market conditions in recent years.

Equity Markets: High return, above the index in a hyper-concentrated market

Since

2020, a few large public U.S. tech companies have dominated the

performance of the main stock indexes, creating a phenomenon of

historically concentrated gains. For example, this handful of stocks

represented 63% of the S&P 500’s performance in 2023.In this

context, the Equity Markets portfolio, which is more diversified in its

allocation to different sectors, outperformed its index’s 17.4% with a

return of 17.7% for one year. The results were driven by growth stocks,

as well as by large positions in Québec companies, which performed well.

Over

five years, the portfolio recorded an annualized return of 9.0%, below

its index’s 10.0%, due to lower exposure to large U.S. growth and tech

stocks at the beginning of the period. The current exposure enables

leveraging the potential of these stocks, while avoiding an

overconcentration as evidenced in the markets.

Private Equity: Following a period of strong returns, rate hikes affect theportfolio

For

one year, the portfolio posted 1.0%, below the 10.5% of its index,

which partially reflects public stock indexes. The increase in financing

costs, which affected certain private companies, impacted this return.

This slowdown was expected after the portfolio produced considerable

returns in recent years. Some sectors were hit harder, including health

care as it returned to normal activities following years of high volumes

related to the pandemic. In contrast, private investments in Québec

generated good returns. The Private Equity team rigorously pursued the

plan to monetize certain assets, with strategic sales achieved during

the year.

Over five years, the annualized return was 14.0%, above

its index’s 12.4%, due to the careful selection of direct portfolio

investments in the technology, financial and consumer goods sectors.

All teams rallied to fully play our role in Québec’s economic development

In

2023, CDPQ’s assets in Québec rose significantly toward its ambition

of $100 billion in 2026, with an increase of $10 billion in one year,

bringing the total to $88 billion.

“In

2023, our investments in Québec made a solid contribution to our

results. I’m especially proud of our teams’ work across all asset

classes, who, together, leveraged their expertise and networks to meet

the growth and international expansion objectives of Québec companies.

They also took part in different major structuring projects and

supported the climate transition, which are central to Québec’s economic

development,” noted CharlesEmond.

Some achievements during the year:

Support for growing Québec’s companies and expertise

An investment in Cogeco Communications,

a Québec leader that ranks among the top 10 cable companies in North

America, following the purchase of a block of shares held by Rogers

Communications Inc. Already a partner in Cogeco’s expansion over the

last few years, CDPQ now holds $350 million in the company’s capital and

will continue to support its North American growth.

An investment in Solotech,

a global leader in audiovisual and entertainment technology, to

facilitate its international expansion. This is the largest financial

investment in the company in 10 years, and a return by CDPQ as

a shareholder.

An investment in Vooban, a

rapidly growing Québec company in applied artificial intelligence

services, to support its growth and expansion ambitions, particularly in

Ontario and the United States.

Most recently, support for Metro Supply Chain’s acquisition of SCI Group Inc., representing the group’s 10th acquisition since partnering with CDPQ in 2018.

Major real estate and infrastructure projects

Achievement of a milestone in delivering the REM

with the commissioning of the South Shore Branch between Gare Centrale

Station and Brossard on July 31, 2023. Once completed, the 67-km project

will represent the longest automated light metro line in the world.

Conclusion

of an agreement in principle with the Government of Québec for Ivanhoé

Cambridge to conduct a feasibility study on converting part of the old

Royal Victoria Hospital site into a world-class university campus.

A $355-million investment to acquire 50% of the A25 Concession, a 7.2-km network comprised of a toll road and bridge on the A25 in Montréal from Transurban, an Australian company.

Mandate awarded to CDPQ Infra to recommend one or more solutions for a structuring transportation project for the Communauté métropolitaine deQuébec.

Cadence, a consortium that includes CDPQ Infra, qualified alongside two others for the procurement process of the High Frequency Rail (HFR) project between Québec City andToronto.

Investments in support of a more sustainable economy

In the promising battery sector, financing of around $200 million (USD 150 million) in convertible debt in Northvolt AB

to contribute to completing the Northvolt Six project, a fully

integrated battery plant in Saint‑Basile‑le‑Grand and McMasterville

in Québec.

An additional investment in Boralex, a renewable energy leader specialized in wind, solar, hydroelectricity and storage, bringing CDPQ’s stake to 15%.

Also of note is the ambition to more than double the size of amounts entrusted to external Québec managers, to reach $8 billion by 2028, and thereby promote the growth of the asset management industry in its local market.

Strong and internationally recognized leadership in sustainable investing

In

2023, through its initiatives and international recognition, CDPQ

continued to exercise strong leadership in sustainable investing. For

example, Ivanhoé Cambridge became the first real estate investor to

issue a senior unsecured sustainability bond obligation in Canada in the

amount of $300 million.

In addition, CDPQ ranked first in the

world, alongside three other international investors, in the Global

SWF’s 2023 GSR ranking, a benchmark in assessing the governance,

sustainability and resilience practices of 200 sovereign wealth and

pension funds worldwide. CDPQ was also the first Canadian pension fund

to receive the Terra Carta Seal from the Sustainable Markets Initiative

in recognition of its leadership on sustainability.

More details

on CDPQ’s sustainable investing strategy, including its progress on

climate targets, the advancement of its commitments and initiatives in

terms of diversity, equity and inclusion, as well as governance, will be

presented in the Sustainable Investing Report published in the spring.

Integration of the real estate subsidiaries

In

January 2024, CDPQ announced the integration of the activities of its

real estate subsidiaries—Ivanhoé Cambridge and Otéra Capital—to enable

greater focus on investment expertise and generate agility and

efficiency gains. As such, the subsidiaries’ investment teams will

become investment groups within CDPQ on April 29, 2024, and will

continue to conduct their activities in the market under their

respective brands, Ivanhoé Cambridge and Otéra Capital. In addition, the

corporate services teams already report to their counterparts at CDPQ.

At the conclusion of the integration, CDPQ expects to generate annual

savings of around $100 million through the synergies achieved in its

processes, resources and systems. The integration will conclude

within 18 to 24 months.

Financial reporting

CDPQ incurs

costs to conduct its activities, including operating expenses, external

management fees and transaction costs. As at December 31, 2023, the

total cost for internal and external investment management was 59 cents

per $100 of average net assets, compared with 48 cents per $100 of

average net assets in 2022. This total is up from the prior year due to

fees associated with higher asset performance. Operating expenses

remained stable at 22 cents per $100 of average net assets. CDPQ’s cost

ratio compares favourably with that of its peers.

The credit

rating agencies reaffirmed CDPQ’s investment-grade ratings with a stable

outlook, namely AAA (DBRS), AAA (S&P), Aaa (Moody’s) and AAA

(Fitch Ratings).

ABOUT CDPQ

At CDPQ, we invest constructively to generate sustainable returns

over the long term. As a global investment group managing funds for

public pension and insurance plans, we work alongside our partners to

build enterprises that drive performance and progress. We are active in

the major financial markets, private equity, infrastructure, real estate

and private debt. As at December 31, 2023, CDPQ’s net assets totalled

CAD 434 billion. For more information, visit cdpq.com, consult our LinkedIn or Instagram pages, or follow us on X.

Let me begin by apologizing to Charles Emond as I didn't reach out to him today for extra comments because I'm preparing for my second back surgery tomorrow and was on the phone with the hospital and preparing for that surgery.

Dr. Aoude did wonders back in April of last year as decompression surgery worked perfectly on my right side but the left side was a problem because it's foraminal lumbar stenosis and decompression doesn't work when that's the case as the nerve is difficult to reach without removing disc. Only fusion of my L3-L4 disc which Dr. Jarzem will perform tomorrow can help but there are risks as in any back surgery.

Nonetheless, the pain is agonizing and I was suppose to do this surgery before Christmas but the Quebec healthcare system is in far worse shape than Quebec's pension fund and when you're sick here, patience and luck are what you need (I'd love to have a coffee with Christian Dubé and Eric Girard who I knew back at National Bank and give them an earful of things they need to do, pronto. I also want to talk to Eric about Quebecers with disabilities and explain why they are right to fight 'unfair' pension penalties).

At least Dr. Jarzem made me laugh yesterday as he reviewed my case with Dr. Aoude to see if he can take me to OR on Friday and saw I was in distressing pain on my left side. I told him: "Dr. Aoude did wonders on my right side, no more pain there but the left side is crippling me."

Dr. Jarzem replied: "He's the right side specialist, I'm the left side one so you're getting two for the price of one," which made Dr. Aoude and me chuckle.

Alright, enough on my health issues, hopefully my back surgery goes well and I will recover and be able to walk, stand, sit and sleep again without any intense nerve pain on my left hip, buttock and thigh.

CDPQ's 2023 results were solid and in line with what I was expecting.

Let's begin with Real Estate since that is where everyone seems to be focusing on as there are issues there.

From the Bloomberg article:

Nathalie Palladitcheff, the head of Ivanhoe Cambridge, CDPQ’s real

estate arm, described last year’s environment as “hostile.” High

interest rates and low occupancy have created a difficult outlook for

office owners and their lenders, with more than $1 trillion in

commercial real estate loans set to mature by the end of next year.

“The increase in rates impacts both the valuation and the cost of

debt, and this resulted in a very significant drop in transactional

volumes on a global scale,” Palladitcheff said, referring to the broader

real estate market. “They have been halved in Europe, halved in the

United States, even an 80 per cent drop in transactions in Germany, for

example.”

Ms. Palladitcheff has done wonders repositioning that portfolio, diversifying out of retail into logistics and multifamily but offices remain a problem.

Also, as she correctly points out, the increase in rates impacts both the valuation and the cost of

debt, and this resulted in a very significant drop in transactional

volumes on a global scale.

Given the global backdrop in real estate and the lagged performance relative to publicly-traded REITs, I wasn't surprised Real Estate recorded a -6.2% return for

one year, above its index (-10%).

This has nothing to do with Nathalie Palladitcheff and her team at Ivanhoe Cambridge, all of Canada's major pension funds are going to post losses in their respective real estate portfolios in 2023 and I'll be calling out anyone who doesn't mark down assets.

The good news, or somewhat good news, it wasn't as bad as I feared.

Total real estate investments returned -2.0 percent for the first half and amounted to 3.9 percent of the fund at the end of the period. Unlisted and listed real estate investments are managed under a combined strategy for real estate.

Unlisted

real estate investments made up 58.4 percent of the overall real estate

portfolio and returned -4.6 percent, while investments in listed real

estate returned 1.7 percent.

The main driver behind the

negative return on unlisted real estate was the office sector, with US

investments in particular falling sharply in value during the period.

This was due mainly to increased vacancy, which means reduced income

for investors. The return on the listed portfolio was also affected by

the negative performance in the US office sector.

Why is this important?

Because as at the end of June, unlisted real estate was down 2% and at year-end, it was down 12%.

That

tells me the Fund's appraisers significantly marked down unlisted real

estate assets in the second half of the year as it became evident office

vacancies weren't getting better and other sectors also faced

challenges as rates hit financing (multifamily).

Importantly,

if Norway's Fund is posting -12% in unlisted real estate, it doesn't

portend well for the unlisted real estate portfolio at Canada's large

pension funds (to be fair, I suspect Norway's Fund has a bit more

exposure to offices but can't confirm this).

There were dramatic markdowns of unlisted real estate assets in the second half of the year and this is worth noting as Canada's large pension funds prepare to report their results.

I've already told people last week when I covered why CDPQ is integrating its real estate subsidiaries

that I expect a challenging time in real estate as assets were marked

down to reflect the clobbering publicly traded REITs took in 2022.

Why was Norway's unlisted real estate portfolio down 12% whereas CDPQ's real estate portfolio was down half that amount last year?

The answer is simple, Norway's unlisted real estate portfolio is made up almost exclusively of office properties which got hit hard last year (they are diversifying their unlisted real estate portfolio by sector and geography but given their enormous size, it takes time).

So, this just proves the repositioning that Nathalie Palladitcheff and her team have accomplished at Ivanhoe Cambridge is working and that's why they're beating their benchmark, adding $5.5 billion in value

added over their benchmark.

As far as CDPQ integrating its real estate subsidiaries, I posted a comprehensive post with my thoughts here.

Next, let's move on to Private Equity as high financing costs hit that portfolio too.

Again, nothing shocking to me, I'm expecting this at all of Canada's large pension funds but some may have fared better than others if their direct investments and distributions (selling assets) kicked in.

I noted in the press release that some sectors were hit harder, including health care as it returned to normal

activities following years of high volumes related to the pandemic.

CDPQ's new head of Private Equity Martin Longchamps has excellent experience coming over from PSP Investments and he and his team will maintain the focus on the long run where that portfolio continues to outperform its benchmark nicely.

Over five years, the annualized return in PE was 14.0%, above its

index’s 12.4%, due to the careful selection of direct portfolio

investments in the technology, financial and consumer goods sectors.

The Infrastructure portfolio had another solid year, generating a 9.6% return against an index at 0.3%.

From the press release:

Assets in essential

sectors such as transportation and renewable energy were among the

performance drivers, as was the current return. With slower transaction

activity in 2023, the team remained disciplined in managing its

portfolio, both in selecting acquisitions and in sales and syndication

activities.

Over five years, the annualized return was 9.5%, above its index’s 5.9%,

primarily due to investments in renewable and transition energy and in

port and telecommunications assets.

So far, so good, the insane concentration risk in a few megacap tech stocks hasn't collapsed but I would heed Stanley Druckenmiller's warning prior to the 1987 crash very seriously if this AI mania continues

As far as CDPQ's public markets, I would refer to my conversation with CDPQ's Head of Liquid Markets Vincent Delisle when I covered mid-year results back in August here.

Importantly, he explained the change in their quantitative strategy:

Not on the Fixed Income side. When I joined in 2020, the

Fixed Income strategy we have in Private Credit was launched in 2017.

It's been a great performer for CDPQ. We've made some minor adjustments

but it's a vehicle that has provided a very positive contribution so I

haven't been very active on that side.

In Public Equities, we have

made small adjustments. A lot of things were working but in some

aspects, the portfolio was a bit too concentrated in some defensive

mandates. So in terms of diversification, we diversified through broader

exposure to styles, and that included buying some technology names.

Just

to give you a sense of proportion, in 2020, we had 3.7% of the

portfolio exposed to large cap technology versus today, we are closer to

the 10%. So we are still underweight but we have introduced more

exposure to large cap tech.

Alpha generation was mainly

through fundamental stock picking strategies, both internal and

external. They still dominate the portfolio but we have introduced

quantitative portfolios as well whether it's internal or external.

We

currently manage north of $25 billion in internal quant strategies that

are doing very well. It's algorithmic, simple processes, math driven,

that I'm happy we introduced as they complement what we were already

doing very well with the fundamental equities bottom up teams.

The addition of more tech exposure obviously helped equities but knowing Vincent, he's looking intensely at the macro backdrop to see where the risks

He also spoke to me about emerging markets debt and how they played the long end well there and also explained why private credit remains a solid outperformer, helping the Fixed Income teams deliver solid returns last year (along with EM debt).

Also worth noting the Quebec portfolio rose significantly toward its ambition of $100 billion in 2026, with an

increase of $10 billion in one year, bringing the total to $88 billion.

I commend Kim Thomassin and her team for doing extraordinary work there, adding significant value to the fund and to the overall Quebec economy.

I'm not a huge fan of pension funds having dual mandates as I worry about governance issues but CDPQ seems to be doing it right.

All this to say that it was another solid year for CDPQ despite some challenges in the real estate and private equity portfolios which are affecting all funds.

Lastly, it is worth noting that Charles Emond’s mandate as President and Chief Executive Officer of CDPQ was renewed recently:

Caisse de dépôt et placement du Québec (CDPQ) today

announced that Charles Emond’s mandate has been renewed for a five-year

period concluding on February 6, 2029. This appointment by the CDPQ

Board of Directors was approved today by the Government of Québec

pursuant to the organization’s incorporating act.

“Over

the past four years, under Charles Emond’s leadership, CDPQ has

delivered solid results in an atypical environment marked by unusual

market conditions. In this context, and supported by his team, he

introduced key strategic changes to the CDPQ portfolio to generate

results that meet depositors’ needs and create value added. At the same

time, CDPQ significantly grew its assets in Québec and mobilized its

teams around several structuring projects in real estate and

infrastructure,” said Jean St-Gelais, Chairman of CDPQ’s Board of Directors.

“CDPQ will have to continue to navigate a complex context as it

executes its mission in the coming years. As such, and in light of

Charles Emond’s remarkable performance in recent years, the Board of

Directors has decided to renew his mandate now,” headded.

“We’re

facing tremendous challenges. The global environment has been volatile

and uncertain since 2020—and that will continue. To achieve our

ambitious objectives and keep striving to serve our depositors better in

these back-to-back extremes, we must continue to evolve as an

organization,” stated Charles Emond, President and Chief Executive Officer of CDPQ.

“We’re privileged to work for an institution whose unique

signature—constructive capital—is a great calling card that opens doors

to the best partners and best opportunities around the world. CDPQ is

also the pension fund most present in its local economy globally. I

would like to thank the Board for their trust and I’m extremely proud to

start this new chapter with the Executive Committee and all our teams.”

Mr. Emond’s second mandate is effective today.

As I stated in another post where I mentioned this,

I would have been shocked if Charles's mandate wasn't renewed

over the next five years because he's doing a great job at the helm of

this organization and it's not an easy job (probably one of the most

stressful jobs among Maple Eight CEOs because CDPQ has a dual mandate

and is always under the microscope).

One last note, it's not fair comparing Norway's 16% return last year to that of any Canadian pension fund simply because the asset mix there is heavily tilted toward public market beta and they have a much higher exposure to the Magnificent Seven stocks that significantly outperformed last year.

Canada's pension funds are a lot more diversified across public and private markets, they're not looking to shoot the lights out, they are looking to deliver consistent returns to meet their long-dated liabilities.

Alright, let me end it there, eat something light and go to sleep early to prepare for my surgery tomorrow (have to fast as it's general anesthesia).

Below, an older interview with CEO Charles Emond where he discusses the organization's unique "double mandate" - providing long-term financial returns for depositors and providing constructive capital to Quebec's economy.

Next, I added tonight's interview on Zone Economie (in French) where Charles goes over the results and more.

Lastly, Dr. Tony Mork talks about the problems of lumbar foraminal stenosis and how it can be treated in this 2 part series (he's talking up his book in treatments, so take that with grain of salt and listen to your specialist).

Comments

Post a Comment