However, it recorded weaker performance in private equity, following

double-digit returns over the past few years, while its office real

estate holdings were affected by a structural transformation, including a

significant shift to mobile work, offset by investments in the

logistics segment of commercial real estate.

The Caisse’s net assets rose to $424 billion as of June 30, 2023, up from $402 billion a year earlier.

“Over

the last three years, we’ve adjusted our portfolio to reinforce our

capacity to withstand market volatility,” chief executive Charles Emond

said in a news release, adding that market conditions reinforce the

Caisse’s strategy of diversification and taking a long-term approach.

“The

many contradictory signals confronting investors — the direction of

inflation, rates, employment and markets — make the environment

challenging.”

Caisse executives said the pension has so

far been able to weather trends including tightening credit conditions

in the United States and the shift to remote work.

Vincent

Delisle, head of liquid markets at the Caisse, said there is still

uncertainty when it comes to what central banks will do in terms of

setting interest rates, the fund’s large fixed-income portfolio

positions the pension manager well.

“Today, with

interest rates that are higher than four per cent, (and) credit returns

that are 7.5 per cent, for us, that is very attractive when we look at

the next five to 10 years,” he said during a media conference on Aug.

16. “And … it’s a portfolio that represents $130 billion out of $424

(billion).”

Emond said that while the first half of the year went well, “it’s a

bit too soon to cry victory” over the impact of rising rates on the

economy.

However, when it comes to the reckoning in

commercial real estate, he said the pension manager was prescient in

anticipating trends such as the shift to remote work and reluctance to

commute that only accelerated during the COVID-19 pandemic. This, he

said, is why the Caisse portfolio responded better to current conditions

than its benchmark.

“Structurally speaking, we have

anticipated quite a bit, we have sold a lot … so I think the bets that

we have made were the right ones,” he said. “On some assets, we’ve

already reduced the value significantly over the past few years (such as

shopping centres and offices), so I believe most of the depreciation

linked to structural changes is behind us.”

The

Caisse’s fixed-income portfolio posted a 3.9 per cent return in the

first six months of 2023, outpacing the benchmark of 3.2 per cent, with

the help of recovering bond markets as interest rates rose and additional contributions from corporate credit and emerging country sovereign debt.

In the real assets portfolio, infrastructure proved to be a solid

contributor during a period of high inflation, the Caisse said, noting

its 4.7 per cent return in the first six months of the year compared to

the benchmark of -2.1 per cent.

“The

renewable energy, telecommunications and transportation sectors, to

which (the Caisse) has been exposed for many years, are significant

vectors of performance,” the pension fund said.“Over five years, the annualized return was 9.6 per cent, driven by the same sectors as in the first six months.”

Over

the five-year period ending June 30, 2023, the Caisse’s average

annualized return was six per cent, above a benchmark portfolio that

returned five per cent, which reflected more than $18 billion in added

value. Over 10 years, the average annualized return was 7.9 per cent,

also exceeding the benchmark portfolio’s seven per cent, representing

nearly $30 billion in added value.

In the first half of 2023, higher financing costs hurt the Caisse’s

private-equity portfolio, which posted a return of 1.4 per cent, far

below its benchmark of 7.2 per cent.

“In

the short term, the portfolio was constrained by higher financing

costs, which influenced the performance of certain private companies,”

the pension fund said.

However, with a focus on sectors

including technology, health care and insurance and a five-year return

of 15.4 per cent, the portfolio still significantly outperformed the

index’s 11.9 per cent return.

Jason Magder of The Montreal Gazette also reports Caisse's Emond 'extremely proud' of REM's early success:

The Réseau express métropolitain officially went into service for paying customers on July 31, and broke down

for roughly 90 minutes during its first morning rush hour.

Nevertheless, the Montreal region’s newest transit agency has surpassed

the expectations of its owner.

Speaking to reporters during an update of the Caisse de dépôt et

placement du Québec’s financial results Wednesday, CEO Charles Emond

revealed the electric driverless light-rail system has achieved a 99 per

cent on-time rate so far, ferrying an average of 25,000 riders per day

between Brossard and downtown Montreal. The Caisse is the principal

owner and operator of the REM through its subsidiary CDPQ Infra.

Later, Marc-André Tremblay, a spokesperson for CDPQ Infra, said

forecasts call for roughly 30,000 passengers per day on the REM when

everyone has returned to work and school after the vacation period, so

registering 25,000 per day during the construction holiday is a good

sign.

“My expectations are naturally always high, but I

would say that I’m very proud of 99 per cent,” Emond said. “We’re still

in this training period, working extremely hard to make sure this train,

which is a computer, reacts perfectly and gets there on time.”

He

said the 99 per cent punctuality rate is impressive, considering that

is the rate expected for transit systems after many years of operations.

“I’m

not saying there won’t be any more incidents, but the reality is I’m

extremely proud, because there is a sense of urgency,” Emond said.

“We’re learning from every incident that happens, and the operator makes

corrective measures. So far, so good. I’m delighted with the outcome.”

The

REM is now operational in five stations over 17 kilometres, but the

project is slated to eventually span over 68 kilometres and serve 26

stations across the Montreal region.

Emond said the next two branches, to Ste-Anne-de-Bellevue and

Deux-Montagnes, are projected to enter service by the end of next year —

a “very aggressive timeline.”

Work on the REM began in

2018, and any construction delays should be compared with the timelines

of other major transit networks, Emond said. Delivering a completed

project in less than 10 years is impressive, he said, given that a

high-speed rail link in California is expected to take 13 years to

build, and one in Hawaii, which just began construction, and is expected

to take 12 years.

“The speed at which the REM was built is nothing short of remarkable,” Emond said.

The

Canada Line in Vancouver, which was financed in part by the Caisse, was

completed in four years, in time for the 2010 Winter Olympics.

With the REM, work in the Mount Royal Tunnel was delayed by an explosion. The pandemic and global supply chain issues also hampered the project.

The

most recent projection has raised the expected cost of the completed

REM to around $7 billion, but Emond has said he expects the projected

price tag to increase again.

The Caisse expects to unveil an update on the cost of the overall project in the first two weeks of September.

Yesterday, CDPQ put out a press release stating as at June 30, 2023, it posted an average return of 4.2% over six months and 6.0% over five years:

Net assets rose to $424 billion from $402 billion as at December 31, 2022

Sustained level of activities in Québec

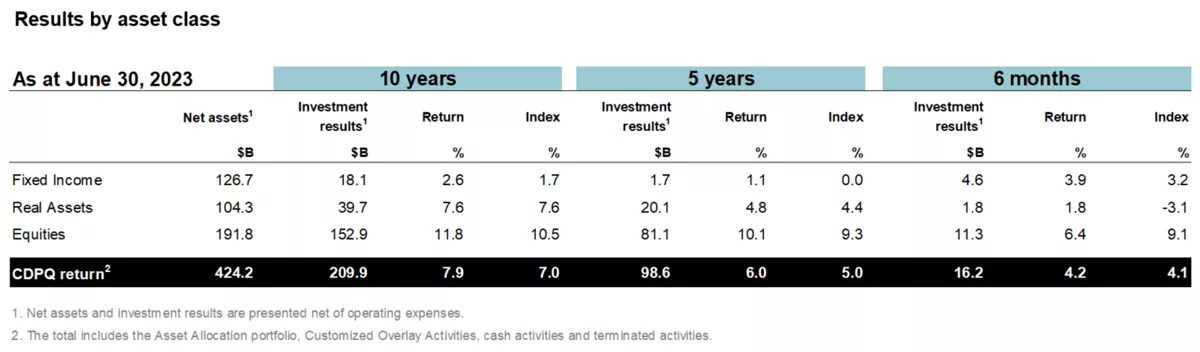

CDPQ today presented an update of its results as at June 30, 2023. Over six months, CDPQ generated an average return of 4.2%, in line with that of its benchmark portfolio’s 4.1%. Over five years, the average annualized return was 6.0%, above the benchmark portfolio’s 5.0%, which represents over $18 billion in value added for its depositors. Over ten years, the average annualized return was 7.9%, also higher than its benchmark portfolio’s 7.0%, producing nearly $30 billion in value added.

CDPQ manages the funds of 48 depositors and adapts

investment strategies to meet their objectives, taking into account

their different risk tolerances and investment policies. The total

portfolio’s six-month, five-year and ten-year returns represent the

weighted average of these funds. As at June 30, 2023, the returns of CDPQ’s eight largest depositors ranged from 3.8% to 5.2% for six months. Their annualized returns ranged from 4.4% to 6.8% over five years and 6.5% to 8.9% over ten years.

“Over the last three years, we’ve adjusted our portfolio to reinforce

our capacity to withstand market volatility. This enabled us to

generate returns that ensure the financial strength of our depositors’

plans,” said Charles Emond, President and Chief Executive Officer of CDPQ.

“The many contradictory signals confronting investors—the direction

of inflation, rates, employment and markets—make the environment

challenging. This invites us to remain vigilant and emphasizes the

importance of diversification and adopting a long-term approach,” concluded Charles Emond.

Return highlights

Fixed Income: Performance stimulated by higher rates

Benefiting from interest rates that are now higher than in past

years, bond markets recovered in the first six months from their

counter-performance during 2022, in the wake of recent historic rate hikes. CDPQ posted a 3.9% six-month return, outpacing the 3.2%

of its benchmark index with a performance stimulated by credit

activities, notably the performance of corporate credit and emerging

country sovereign debt.

Over five years, the asset class recorded an annualized 1.1% return

due to central banks’ efforts to significantly tighten monetary

conditions to control soaring inflation. This result is higher than its

benchmark index’s 0% return, due to all five segments in credit.

Real Assets

Infrastructure: Continued performance in an inflationary context

In the first six months, the portfolio once again demonstrated its

ability to perform in a context of high inflation. During this period,

it posted a 4.7% return, higher than its benchmark index’s -2.1%.

The renewable energy, telecommunications and transportation sectors, to

which CDPQ has been exposed for many years, are significant vectors of performance.

Over five years, the annualized return was 9.6%, driven by the same sectors as in the first six months. This performance is well above the index’s 5.7% return.

Real Estate: Repositioning in real estate mitigates the effect of rising rates

Over six months, the portfolio’s return was -1.5%, compared with -4.3%

for its benchmark index. The rapid and significant rise in interest

rates affected the entire market and its sectors, as reflected by the

benchmark. However, the portfolio’s shift toward the logistics segment

offset the more mitigated performance of the office sector, which is

undergoing a structural transformation in light of new work habits.

Over five years, the annualized return was 1.0%, below the index’s 3.1%,

attributable to the weak performance of the Canadian shopping centre

sector, in which Ivanhoé Cambridge, CDPQ’s real estate subsidiary, was

historically overweighted. Note that since the portfolio’s repositioning

over the last three years, the performance has greatly improved.

Equities

Equity Markets: High, more diversified return in historically concentrated markets

Over six months, the portfolio recorded a 10.6% return, in line with its benchmark index’s 10.7%, despite the markets’ historical overconcentration in seven major high-growth tech stocks, which for example represented 80% of the S&P 500’s gains in the first half of the year. The portfolio’s performance proved comparable, but more diversified than that of the markets.

Over five years, the annualized return was 7.1%, below the index’s 7.5% return.

This difference, which is explained by the portfolio’s more limited

exposure to major tech stocks at the beginning of the five-year period,

has progressively diminished during the last three years following the

portfolio’s strategic evolution. This repositioning allows the portfolio

to benefit from the potential of these stocks, while avoiding an

exacerbated overconcentration as seen in the markets.

Private Equity: Higher financing costs felt after several years of strong returns

In the first six months, the portfolio’s return was 1.4%, below its benchmark’s 7.2%,

following the exceptional results of recent years. In the short term,

the portfolio was constrained by higher financing costs, which

influenced the performance of certain private companies.

Over five years, the portfolio posted a 15.4% return, outperforming its index’s 11.9%. The judicious choice of sectors, including technology, health care and insurance, explains these results for the period.

Québec: Large-scale projects and local company growth

In Québec, CDPQ maintained a good level of activity despite a

particularly low volume of transactions observed worldwide. Following

are some recent achievements of note by CDPQ’s teams, which leverage a

wide range of tools to contribute to Québec’s economic development:

Major real estate and infrastructure projects

Achievement of a milestone in delivering the REM with the

commissioning of the South Shore Branch between Gare Centrale Station

and Brossard on July 31, 2023. Once completed, the 67-km project will represent the longest automated light metro line in the world.

Mandate awarded to Ivanhoé Cambridge by CDPQ, following the

conclusion of an agreement in principle with the Government of Québec,

to conduct a feasibility study on converting part of the old Royal

Victoria Hospital site into a world-class university campus.

A $355-million investment to acquire 50% of the A25 Concession, a 7.2‑km network comprised of a toll road and bridge on the A25 in Montréal from Transurban, an Australian company.

Participation in financing the new Île-aux-Tourtes bridge by underwriting $75 million of Groupe Nouveau Pont Île-aux-Tourtes’ bond issue.

A $145-million loan by subsidiary Otéra Capital for a multi-residential project located in the heart of Montréal’s Golden Square Mile.

Support for growing Québec’s companies and expertise

Participation in Previan’s acquisition of Sensor Networks, an American supplier of sensing tools and technologies.

A $125-million investment to accelerate the growth of Workleap

(previously GSoft), which offers software that improves the employee

experience of 16,000 companies located in over 100 countries.

Renewal of the collaboration with the Quebec Emerging Manager

Program to accelerate the development of emerging managers, bringing

CDPQ’s commitment to $250 million, or $50 million per year for five years.

Expertise and leadership recognized globally

In the first six months of the year, CDPQ received various

distinctions that illustrate the quality of its work and the

accomplishments of its teams:

In sustainability, CDPQ ranked first in the world, alongside three

other international investors, in the Global SWF’s 2023 Governance,

Sustainability and Resilience ranking, a benchmark that assesses the

governance, sustainability and resilience practices of 200 sovereign wealth and pension funds worldwide.

In real estate, Ivanhoé Cambridge received nine awards at the IPE

Real Assets Global Awards, which recognize global leaders in the

industry, including Investor of the Year, as well as ESG and

Environmental Sustainability.

In infrastructure, CDPQ ranked first in the Global Investor 50

list, a showcase of the world’s largest institutional investors in

infrastructure based on the size of their assets, compiled by Infrastructure Investor magazine.

Financial reporting

As at June 30, 2023, the annualized costs incurred for CDPQ’s

activities, which include internal operating expenses, external

management fees and transaction costs, were estimated at 55 cents per $100 of net average assets, compared with 48 cents as at December 31, 2022. The difference with 2022 is primarily explained by the increase in external performance fees related to increased returns. CDPQ’s cost ratio compares favourably with that of the industry.

In addition, CDPQ is rated investment-grade with a stable outlook by the credit rating agencies, namely AAA (DBRS), AAA (S&P), Aaa (Moody’s) and AAA (Fitch).

ABOUT CDPQ

At CDPQ, we invest constructively to generate sustainable returns

over the long term. As a global investment group managing funds for

public pension and insurance plans, we work alongside our partners to

build enterprises that drive performance and progress. We are active in

the major financial markets, private equity, infrastructure, real estate

and private debt. As at June 30, 2023, CDPQ’s net assets totalled CAD 424 billion. For more information, visit cdpq.com, consult our LinkedIn or Instagram pages, or follow us on X.

CDPQ is a registered trademark owned by Caisse de dépôt et placement du Québec and licensed for use by its subsidiaries.

Before I get to me comment, a quick word on the REM.

When I initially covered the inauguration of the REM, I mistakenly said Macky Tall, he former head of liquid markets, wasn't present.

Well, my bad, he was there and even took a photo with CDPQ Infra's CEO, Jean-Marc Arbaud:

I corrected that in my previous comment and remain very positive on the REM which I consider an engineering marvel and something all Quebecers should be proud of.

Unfortunately, I'm not very proud of some of the articles I'm reading lately in the French media and publicly stated my opinion on Twitter:

The Regional Metropolitan Transport Authority (ARTM) plans to abandon the automation of trains recommended by CDPQ Infra to reduce the imposing bill of 36 billion for the most recent version of the REM de l'Est, renamed Projet structurant de l'Est (PSE) since the withdrawal of the Caisse de dépôt subsidiary.

Can you imagine how idiotic these people at the ARTM are?

As a friend stated: "Driverless trains actually bring down the cost such that you can actually earn a return on investment so that you can actually pay for the assets."

DUH!!

Anyways, the REM is an incredible asset and CDPQ is the only pension fund in the world that can boast of delivering a greenfield project of this scale on time and on budget (for the most part, some minor delays and cost overruns).

Alright, let me get back on track and focus on CDPQ's mid-year results.

Yesterday, I had a chance to talk with Vincent Delisle, Executive Vice-President and Head of Liquid Markets at CDPQ (since August 2020) and went over the results with him.

I want thank Vincent for taking the time to talk to me and also thank Kate Monfette for setting up this discussion.

Since Vincent is Head of Liquid Markets (ie. Public Markets and Private Credit), our discussion focused more on that area of the portfolio but we did end with a discussion on Private Markets.

I began by stating from my understanding, CDPQ is still underweight tech stocks and the way Charles Emond explained it to me last time, is they prefer taking more technology risk in private markets. I said that if you weren't overweight technology, it was hard to beat your index in the first half of the year because of the concentration risk from the so-called Magnificent Seven (Apple, Microsoft, Amazon, Google, Nvidia, Meta and Tesla).

Vincent responded:

It's a fair assessment and to be honest, technology is so broad, we need to dig a bit deeper in terms of what we own in technology.

We increased our technology/ growth exposure in the last three years.

What it meant this year is even though we have technology, we are not overweight the top US technology names. When you have the Magnificent Seven dominating as they have in the first semester, it's tougher to track the index.

We've actually managed to keep up with our benchmark with the help of other strategies, other mandates if you will. But when it comes to the top mega cap tech names, we've adapted but we are underweight that group.

I asked him if this boom (more like bubble) in mega cap tech shares will continue or is it just a call on where long-term bond yields are heading, meaning if higher for longer persists, they're in trouble but if ultra low rates come back and persist, mega cap tech should continue to do well. I also told him in the pension world, you want to be more diversified into value plays, not be overweight growth.

He replied:

Obviously, we all would like to call the top on this concentration bubble and that predates me arriving in 2020. We've made some adjustments in how we want to be more agile, how we want a broader exposure in our Pubic Equity portfolio but what we haven't changed is we have a preference for quality, less volatile industries and stocks. From that standpoint, we are not going to chase anything because it's rebounding or because it's leading.

Next three years, rates are higher, what does it mean? Bonds are attractive, some pocket of equities like long duration/ non profitable tech certainly at risk of disappointing.

But if you look at the dominating forces in the market in the first half of the year, you have to treat so many things differently even within the bellwethers, whether it's Microsoft, Google or Meta versus Tesla and Nvidia.

So, I don't want to say this is a long-term call on rates but too much volatility, cyclicality and certainly non-profitable areas is something we try to be more careful of.

On the Private Equity side -- and that's probably the line Charles shared with you -- is where we do have technology/ growth exposure so we don't feel we have to overly compensate on the Public Equity side.

I asked Vincent if there was a change in strategy since he took over Liquid Markets, in particular focusing more on quantitative strategies:

Not on the Fixed Income side. When I joined in 2020, the Fixed Income strategy we have in Private Credit was launched in 2017. It's been a great performer for CDPQ. We've made some minor adjustments but it's a vehicle that has provided a very positive contribution so I haven't been very active on that side.

In Public Equities, we have made small adjustments. A lot of things were working but in some aspects, the portfolio was a bit too concentrated in some defensive mandates. So in terms of diversification, we diversified through broader exposure to styles, and that included buying some technology names.

Just to give you a sense of proportion, in 2020, we had 3.7% of the portfolio exposed to large cap technology versus today, we are closer to the 10%. So we are still underweight but we have introduced more exposure to large cap tech.

Alpha generation was mainly through fundamental stock picking strategies, both internal and external. They still dominate the portfolio but we have introduced quantitative portfolios as well whether it's internal or external.

We currently manage north of $25 billion in internal quant strategies that are doing very well. It's algorithmic, simple processes, math driven, that I'm happy we introduced as they complement what we were already doing very well with the fundamental equities bottom up teams.

I told him, the problem with the bottom up fundamental approach is you can be right but you might have to sit on your hands for a very long time before being proven right.

Vincent responded:

That's where my background came into play. If we were blessed with stable, buy and hold type markets, then I think the fundamental approach provides more in that type of environment.

Let's be honest, if you look at 2021, 2022 and 2023 where we go from one extreme to the other, some of these quantitative approaches had an easier time at adapting exposures. For example, our internal quant growth portfolio is beating its growth benchmark this year and I repeat, we are NOT overweight the Magnificent Seven.

That's very impressive and I told him it makes a huge difference.

In fact, I was looking at Norway's Government Pension Fund results, they posted a 10% gain for the first half of the year but when you look at Table 6 of their public report, they're heavily exposed to the Magnificent Seven:

Again, it's a different Fund with different objectives but it shows you how missing out on those dominant mega cap tech names can make a huge difference, so in this regard, what the internal quant growth teams did at CDPQ is very impressive (as they remain underweight the Mag 7).

To be fair, I did mention CDPQ's peer group in Canada also have a value/ quality tilt in Public Equities because they don't want the volatility that comes with being overweight large cap tech names (again, Norway's large sovereign wealth fund doesn't care as much about that, they're not matching assets and liabilities).

I then shifted my attention to Private Debt and Fixed Income, noting this is where the large peers have all shifted their attention and more importantly, this is where performance has come from in Fixed Income. I asked Vincent if he's concerned about a bubble in Private Debt and how do they underwrite their loans to make sure there's not a bunch of junior debt in there.

He replied:

Fair point. Our Credit operation is tilted toward investment grade. The bulk of what we own is single A or triple B. Our IG (investment grade) exposure is roughly 55% and 45% is in high yield debt.

In terms of Credit, most is in private markets (Private Credit/ Debt) where we have much better influence on the covenants and what gets written in the contract.

In private Credit, the premium we get is approximately 150 basis points. Obviously if there's a credit cycle, the portfolio will be impacted but we feel that the 150 bps over Treasuries warrants the exposure to this asset class.

The current yield in our Credit portfolio is north of 7.5%. Our depositors are looking for north or 6-7% long term. This asset class was attractive but it's gotten even more attractive.

So, more investment grade, more Private Credit where we have more influence in terms of how we underwrite loans and we stick to less cyclical areas like property & casualty, software, data centers, that's where the bulk of the exposure has been.

He added: "On the whole, we are very confident with this asset class."

I then quickly asked him about external mandates and specifically external hedge funds as I used to invest in them 20 years ago when I was at the Caisse:

It's a lower percentage than what you would find at our peers. It's mainly global macro funds and some small exposure to Long/Short Equity funds. It was a very good contributor last year. Certainly when you look at the volatility the last few months, when interest rates aren't going the way people expect and volatility is high, that's an area we're happy to be in.

I completely agree and that led me to talking about Bonds and rising interest rates.

I remember, luckily the article you're referring to was from last September, so I wasn't too far from 4% (as he chuckled).

I told him "I'm very bearish and do not believe in soft landing fairy tales" but admitted the last bit of rate hikes are tough to gauge and I see wage inflation creeping in the US (UPS drivers and others signing big raises), that part of the puzzle unnerves me because if wage inflation becomes entrenched, inflation will come back strong and rates will head even higher.

That's longer term, short term, I see bonds attractive as we head into Jackson Hole summit next week where Fed officials will share more of their thinking with us.

Vincent responded:

When you look at the decline in US inflation from 9% annualized CPI a year ago to 3% today, that was the easy adjustment. Getting from 3% to 2% where we think the Fed wants it will take more softness from US consumer and employment.

We talk about scenarios. The most likely scenario for us is a shallow recession and we feel it's too soon to celebrate this soft landing unicorn type of environment

It takes 18 months plus for rate hikes to filter into the economy and the first Fed rate hike was in March 2022. We expect to see signs where bank lending in the US impacts job growth and consumer spending.

Where the long end eventually peaks? Between 4% and 4.5% is where we continue to like our bond exposure here.

Once we do hit that air pocket in the US economy, the question for us is how much help do we get from the Fed and our answer is would be quite modest, quite minimal. So, let's say there's a landing or recession over the next 12 months, what kind of ammunition does the Fed have to take rates down from 5%? 4% to 3%, yes, but more than that is where we expect the market to be disappointed.

So, tactically, we think we're near the peak on the long end of the curve. On a 3 to 5-year basis, I don't see much coming from declining interest rates in terms of helping multiples in other asset classes.

He added this:

I spoke about Private Debt in our Fixed Income portfolio but we also have emerging market debt in that portfolio mainly in Latin America. So we've actually been very long duration in parts of the world where rates are starting to come down. I'm pointing that out because I feel all we talk about in the industry is US 10-year Treasury yield and yes yields have gone up and that's where our focus is but it's more in Brazil and other areas where we've seen rates cuts and that's been a decent performer for us in our Fixed Income portfolio.

We ended our discussion on a quick recap on Private Markets which isn't the area he covers but he's obviously well informed about their activities.

I said Infrastructure remains solid as renewable energy and transportation assets delivered solid gains, Real Estate and Private Equity seem to be getting hit more as rates rise and so do financing costs.

I did mention the Real Estate portfolio is being repositioned into logistics/ industrials and residential/ multifamily and this is ongoing and valuations in Private Equity remain healthy.

Vincent replied:

Infrastructure for us is a portfolio that continues to deliver in absolute and relative terms. That strategy continues to be a strong contributor. If inflation continues to climb in a resilient economy, it's a gift for the infrastructure portfolio.

Real Estate, the asset class is having challenges because of cap rates going up but we are very happy with the shift.

There are two portfolios that had a shift in terms of strategy since 2020 -- Public Equities which I alluded to earlier where we are more exposed to growth, more proactive and more quantitative and in Nathalie's portfolio in Real Estate moving out of Retail and Offices and more into Logistics and Multifamily and that is paying off.

Private Equity, I hear you on valuations and everyone is waiting for a valuation gauntlet to hit the asset class but when you look at the operations in our portfolio but even as a whole, corporate profits have been quite resilient across the world.

I think that's one reason why it hasn't been a severe bear market in Public Equity and I think you're seeing the same resilience in operations in Private Equity.

Obviously underperforming the index which is made up of 50% PE and 50% Public Indexes, that explains the lag versus the index.

I mentioned Martin Longchamps, the new Head of Private Equity since November 2022, will be busy and his experience at PSP will prove very useful.

Alright, let me wrap it up there and thank Vincent Delisle once again for a very insightful discussion.

I will just end this discussion with a French interview with CDPQ's CEO Charles Emond going over mid-year results.

Charles got some flack on Twitter from people who aren't impressed with the results but these people do not understand the mandate of large Canadian pension funds isn't to outperform the S&P500 or Nasdaq but to deliver steady long-term returns over the long run and make sure they have more than enough assets to meet future liabilities.

Lastly, don't be surprised if CDPQ is a big investor in a battery plant in Quebec or if it teams up with Hydro-Quebec to build a new nuclear power plant (Michael Sabia knows if Quebec is to decarbonize and be carbon neutral by 2050, they need more nuclear energy).

Comments

Post a Comment