The Silence of the Bears?

The silence of the bears is deafening. And who can blame them? The last 2 years have been absolutely brutal for any fans of price discovery, volatility and anything analytical mattering. Nothing matters. Be it divergences, valuations, earnings misses, slowing data, yield curve, equal weight, internals, catastrophes in nature, slowing loan growth, slowing auto sales, slowing real estate, retail apocalypse, debt levels, etc…I can drone on. Nothing matters. Markets keep drifting higher despite it all.Sven Henrich of the Northman Trader sounds like a truly frustrated bear. You can track him on Twitter here and I highly recommend you read his team's market analysis regularly.

Price discovery as we used to know it, the back and forth of buyers and sellers engaging in the argument of forward valuations based on expected earnings growth, has ended with the disappearance of sellers as part of the normal market functioning:

Corrections as a means of price discovery don’t exist any more. Every day we don’t have a 3% correction is a new record in length of time without any such correction. And the chart above illustrates this adequately. It is a global phenomenon, it’s not only US based.

5% corrections, what also used to be regular part of markets and a bare minimum at that, have also disappeared:

Not quite at a record, yet the message is nevertheless clear: There’s not much happening in these markets on a day to day basis.

The abomination of what passes for intra-day trading ranges these days illustrates the point quite nicely:

Whatever downside does occur can’t sustain itself for more than minutes, a couple of hours at best. Case in point: The $DAX was only negative for 1 hour 16 minutes after the surprise collapse of German coalition talks on Monday. Nothing matters.

Hence it is no surprise sentiment is as bullish as it is. Recall allocations are all bullish, people, funds, even central banks all own the same shrinking universe of stocks.

Indeed there is not even a sense that anything could change this program:

This chart of the global Dow Jones, more than any other, shows how historically out of balance this rally has been. Red bars don’t exist and this is the steepest uninterrupted ascent ever accompanied by the steepest volatility compression ever.

In this context yesterday’s capitulation by Goldman Sachs was classic. They were the investment bank that kept citing valuations as a major concern and were the most bearish on 2017. Then they capitulated. Now their mid range target is 2850 for 2018. with little to no downside risk:

That’s if the exuberance stays rational they say, if it goes irrational they covered themselves with an irrational scenario of 5300.

As I said classic. It is notable how both Monday and Tuesday were suddenly flooded with bullish forecasts. I won’t bother to recite them all here, I gave you a glimpse yesterday.

I’m just highlighting this as a latest example of the complete lack of any divergent views remaining in the marketplace. Which is fine. It simply illustrates market sentiment, but also again underscores the extent of the bubble.

Bulls will counter that growth is solid. I’ve documented variant signs of a slowdown in the works (Caution: Slowdown). And I’m not the only one to notice:

Growth in Developed Economies Slowed in Third Quarter, OECD Says

And yet while bulls cite supposed great growth figures the ECB keeps printing like we’re in the middle of the financial crisis:

The numbers behind the chart via Holger Zschaepitz: “#ECB ramps up balance sheet expansion despite booming#Eurozone economy. Total assets rose by another €24.1bn to a fresh life-time high of €4,411.9bn on QE program, equals to 40.9% of Eurozone GDP.”

Now that’s just intellectually insulting. If things are so great we wouldn’t need this level of intervention or any intervention.

But this is what they are doing. Every day. I keep asking: What is the organic market price balance without intervention? The answer remains the same: Nobody knows as we haven’t seen markets without intervention other than the brief moments were they produced full out panic. 2011 and early 2016 are examples coming to mind.

So I continue to view price extensions and disconnects to be a direct result of trillions of dollars in ongoing intervention and exacerbated by record ETF inflows.

Let’s be clear: I don’t know how or when it ends, but it will end. Our primary mission here is to figure out what we consider good risk/reward set-ups knowing that we are finding ourselves in the most one way focused and technically disconnected markets in decades:

But this is precisely the point in time when the Goldman Sachs capitulation takes place and all the bullish forecasts are coming out. And I understand why they are coming out. No corrections have taken place and we are in a bullish seasonal part of the year.

Now that we have entered the seasonally most bullish time of the year I can certainly understand the silence of the bears. What is there to say? No rationally reasoned argument has mattered, prices keep going up and there appears absolutely nothing on the horizon to stop this train.

Indeed, not only are bulls bullish, but some of the remaining bears I still see floating about have resigned themselves to talk blow-off top coming and are busily identifying higher upside targets from 2700-3000. Funny that. Bulls are bulls and bears are bulls.

But this is the lay of the land folks.

Add some oversold signal charts coinciding with new all time highs and I could easily argue 4 to 5 weeks of upside coming:

The message: Markets cannot possibly go down. There is no risk. Everybody is bullish, join the party.

Bottom line: Fading this action and sentiment is the most contrarian thing anyone can do here and for that reason it can also be the most dangerous. I have no illusions about that.

Folks are piling in long at the technically most disconnected market ever since the 2000 Nasdaq bubble. But that doesn’t mean it will stop here.

Are there any issues with the bull case here other than technical disconnects and divergences that don’t matter?

Well, here’s a few considerations I wanted to share:

This chart doesn’t tell us we can’t go higher. We can. But it suggests something disturbing and I’ve made reference to it in the past, but the overlay with the 10 year gives additional context: It could be argued that these waves of bullish action were driven by one primary factor: Cheap money. Artificial low rates and debt.

Furthermore it could be argued that the bearish break on the S&P 500 in 2008 was never technically repaired. Yes, massively higher prices as a result of over $20 trillion in central bank intervention, zero rates and a global explosion in debt levels to the tune of above $145 trillion in the non financial sector. All made possible by cheap money:

The lower the rates the higher the debt:

So the big question is simply this: What if that downtrend in the 10 year yield bursts above its trend line for the first time since 1987?

As you can see in the S&P 500 chart above we have never seen a break above trend to the upside. Yet the entire market advance has been dependent on its declining trend. All of it. To fix any downside in markets rates had to be lowered and lowered.

None of this tells us anything about this week or next, but it highlights perhaps the precarious nature of the construct.

While the ECB keeps printing $DAX remains at a critical long term juncture:

And the quarterly chart also raises red flags:

The ECB is scheduled to slow down their QE program in 2018, but not end it nor will they raise rates at any time during Mario Draghi’s reign. The ECB remains in full policy panic mode. Because that’s what NIRP is. Panic mode. And you know why they keep pressing? Because inherently they know prices could not sustain themselves. They have to keep rates low.

The yield curve keeps flattening, but it matters not, it is now at the flattest level since 2007:

We are told not to worry of course:

We can only go up and nothing matters.

The only thing that matters is that people keep piling long into these markets.

ETF inflows have now reached an all time history high of $400B of inflows just in 2017:

There’s a QE program right there.

I’ve been mentioning the weekly 5 EMA:

As you can see from the chart: No weekly close below the weekly 5EMA is permitted. Any break lower is saved by the end of the week.

This is what we need to see change before a change in trend can be considered.

For now, markets can only go up and growth is wonderful.

Now, who’s going to tell the bond market?

The screaming of the bears has ended. Their silence is deafening.

And perhaps that should worry bulls more than anything.

Another bearish blog I highly recommend you read is Edge and Odds, published here in Montreal from now-retired portfolio manager Denis Ouellet (great blog, subscribe to it).

A reader of my blog told me: "He uses the Rule of 20 to scale exposure, but supplements it with a rule of 120 which says that equity returns tend to be substandard with the 10 year/3 month spread is less than 120, as it is now."

Now, the silence of the bears is nothing new, it goes hand in hand with the silence of the VIX, which I covered in the summer.

In a nutshell, global central banks are heavily intervening in global equity, bond, and currency markets with one goal, namely, kill volatility and kill big hedge funds who are trying to short these markets.

Why are central banks intervening to the tune of trillions in markets? Because they are petrified of deflation and unfortunately no matter what they do, my forecast of deflation coming to the US will materialize, and this will most definitely bring about the worst bear market ever.

Those of you who don't understand the "baffling" mystery of inflation-deflation, including some members of the Fed concerned about low inflation, better wake up and smell the coffee or risk getting slaughtered.

Importantly, central banks cannot stop global deflation. There is no big reversal in inflation taking place. Global inflation is in freefall. Central banks can continue pumping trillions into markets but they will lose the war on deflation and if they're not careful and hike rates too aggressively, they will exacerbate global deflation.

Central banks also know markets are on the edge of a cliff and the bubble economy is set to burst, which is why they're desperately trying to reflate risk assets at all cost even if that means euphoria might creep into markets. Why do you think the Fed is openly talking about QE infinity?

So, while I still think it's as good as it gets for stocks, I'm back at trading shares full-time, carefully navigating through these prickly markets, using all information available to me, like what top funds bought and sold last quarter, but truth be told, these markets terrify me.

And they should terrify you too, especially if the quiet melt-up continues and you see a parade of bulls telling you to jump in, enjoy the party.

I keep coming back to this weekly chart of the S&P 500 (SPY) which every trader will tell you is bullish:

I want to see a meaningful correction right back down to its 200-week moving average. It is unlikely to happen at the end of this year but it has to happen because if it quietly keeps grinding higher, when the music stops, these markets are going to get destroyed, clobbering everyone, especially retail investors jumping in as bull stretches to new highs in a late-cycle rally.

Central banks are playing with fire here. They know it and I think the big canary in the coal mine remains credit markets where things look fine after a couple of shaky weeks:

Keep your eyes peeled on high yield (junk) bonds (HYG) because that's the first place trouble will show up and spill over to the stock market.

The stock market is just a show, real traders fear the bond market and the signals coming out of the bond market are what should concern all of you.

Importantly, while some think the collapse of the Treasury yield curve is due to coming changes of the US tax code and US corporate pensions, I think something far more ominous is in the works here.

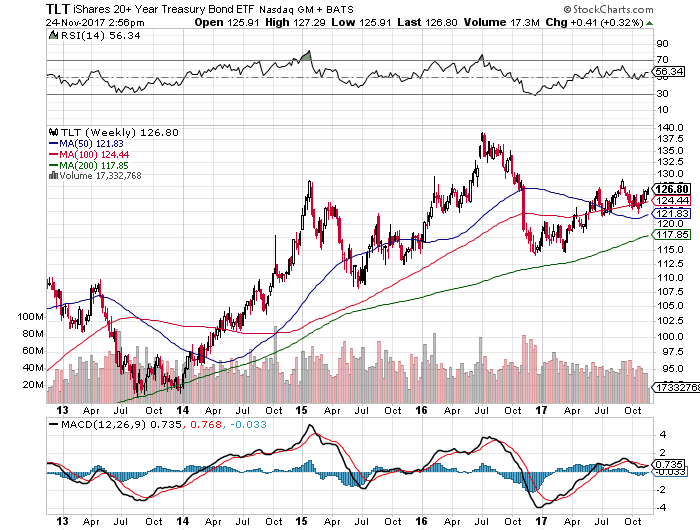

I personally think the bond market is equally worried of deflation headed to the US, which is why US long bond prices (TLT) keep rallying as yields tumble in the long end:

Remember, the Fed controls the short end of the curve but inflation expectations determine the long end of the curve, so right now, you have an interesting dynamic where the Fed is raising rates but the long end keeps rallying despite the selloff in the short end.

For me, this is normal. The Fed is trying to restore its ammunition by raising rates so it can cut them later on when the next crisis hits, but the bond market is worried it's going too fast and will kill the economy and exacerbate deflationary pressures.

Interestingly, the US dollar (UUP) is still in a downtrend as they're trying to raise inflation expectations through higher oil prices (OIL):

But a lower greenback puts pressure on Europe and Japan where deflation is alive and well (higher euro and yen mean lower import prices there, which they can't afford for long because it exacerbates deflation there). And as I stated previously, if oil rises too fast, it’s deflationary because it will impact aggregate demand in a debt-laden economy.

Then there is China which is set for a major economic contraction but you wouldn't know by looking at Chinese large cap shares (FXI):

Given my worries of global deflation, I’m short Chinese and emerging market equities (EEM) and bonds (EMB). Because of deflation, I'm also short oil (USO), energy (XLE), metals and mining (XME) and financials (XLF) and remain long and strong good old boring US bonds (TLT), the ultimate diversifier in these insane markets.

By the way, all these frustrated bears are funny, if you diligently read my blog on how GE botched it pension math, you would have been short and made some serious money:

I used to invest in L/S Equity hedge funds and laughed when they told me there are NO shorting opportunities (there are plenty, you need to do your homework!!).

So, while most bears are silent, some are laughing all the way to the bank, and those are the bears you need to invest with.

Below, an excellent interview from USAWatchdog with former Federal Reserve insider Danielle DiMartino Booth says the record high stock and bond prices make the Fed nervous because it’s fearful of popping this record high credit bubble.

Danielle is one sharp lady who authored a best selling book, Fed Up. I obviously don't agree with her on everything since I remain long US long bonds and believe deflation is headed our way, but listen to her comments carefully as she gives you a very sobering view of today's credit markets.

Hope you enjoyed this comment, please kindly remember to donate or subscribe to this blog via PayPal on the right-hand side under my picture and support my efforts in bringing you insightful daily comments on pensions and investments. I thank all of you show who have contributed and continue to contribute to this blog, it's truly appreciated.

And since it's Friday, let's have a quick glimpse into what's moving up on my watch list today:

Take care, I wish all Americans a Happy Thanksgiving weekend. Those of you who took a long weekend off, make sure you read my last comment on OTPP's Barbara Zvan on managing risk.

Comments

Post a Comment