Ron Mock Reflects on OTPP's Success

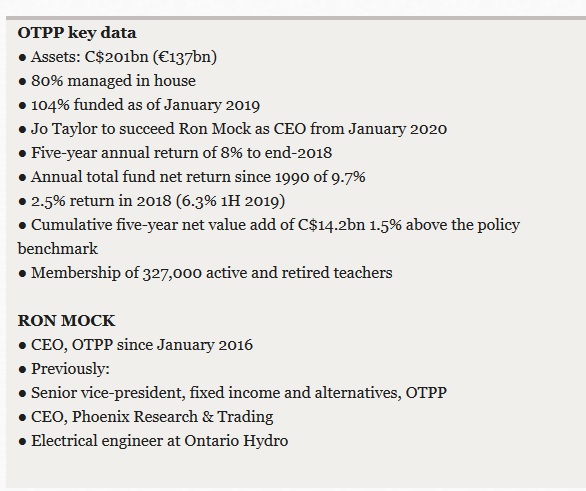

Lots of pension fund executives would like to be in the shoes of Ron Mock as he sits in the London offices of Ontario Teachers’ Pension Plan (OTPP), overlooking Portman Square. Ahead of his retirement as CEO at the end of the year, Mock oversees a fully funded pension plan with assets of over C$200bn (€137bn).I saw this interview earlier today and immediately reached out to OTPP's outgoing CEO, Ron Mock.

He has transitioned OTPP’s management to a new benchmark aligned to the funding of the scheme. OTPP is sought the world over for its advice on how to implement it. It is the embodiment of what has become known as the “Canadian model”.

“Pick 30 countries, the top 30 around the planet, and there isn’t a week or month that goes by where they’re not in our office asking us, ‘how can we do this?’.”

Yet Mock, modestly, describes himself as standing on the shoulders of giants. What is the Canadian pension fund model? Can it be emulated, and is it, indeed, a useful way of looking at the world?

It may be thought of as having a high exposure to real or private assets. It may also be seen in terms of the high levels of compensation broadly necessary to attract and retain the required investment talent.

Indeed, many European pension funds look enviously at the higher compensation budgets that allow OTPP and its Canadian peers to recruit private market specialists, on the basis that it is better to pay them to work for you directly. Some 80% of OTPP’s assets are managed in-house.

Yet for Keith Ambachtsheer, the renowned Canadian pension specialist and director emeritus of the Rotman International Centre for Pension Management, success drivers for OTPP have been “legal freedom for the organisation to succeed at its 1990 start, governance that is both representative and skilled, and entrepreneurial culture and management through 29 years”.

Ambachtsheer’s 1980s recommendation for autonomous-funded public pension institutions was taken up by the Ontario treasurer, Robert Nixon, in 1987 in his Task Force on the Investment of Public Sector Pension Funds. In Ambachtsheer’s words, Nixon’s report recommended that taxpayer-funded pension funds “should have a clear mission, have a strong independent governance function, and be able to attract and retain the requisite talent to be successful”.

The most tangible outcome of this recommendation was the transformation of the old Teachers’ Superannuation Fund – which invested entirely in non-marketable provincial bonds – into the OTPP of today.

Success was not predetermined: OTPP’s first private equity investment was a total write-off. Employer and union stakeholders have stayed true to the model recommended by Ambachtsheer and Nixon more than three decades ago.

Today, Mock is happy to emphasise the bond between members and OTPP through “vertical alignment” between members, stakeholders and management.

In his tenure as CEO, Mock has spearheaded the OneTeachers strategy, which recognises that total fund returns and risk reduction are as important for plan sustainability as value-add returns. Aimed at increasing this “vertical alignment” with stakeholders, it has effectively meant recalibrating the fund’s benchmark to orientate it to pension liabilities.

Effective from 2017, OneTeachers has also meant shifting pay structures “to better align compensation practices to this strategy’s key performance indicators”, according to the 2016 annual report. OneTeachers, which Mock describes as originating within management rather than from stakeholders, is currently in the final phase of implementation.

Mock describes the transition variously as difficult and time-consuming, but also exciting and important. “The new ideas, the new concepts, that started getting unleashed from this was one of the most rewarding things I got an opportunity to witness.”

Teachers’ in the news

OTPP regularly appears in financial news media globally as an acquirer of private market assets. Indeed, capturing long-term illiquidity premia is widely seen as a hallmark of the Canadian model; OTPP currently has 18% in non-publicly-traded equity, for instance, and 9% in infrastructure.

And as an investor in high-profile infrastructure assets globally – like Brussels or London City Airports, as an investor in projects such as Elon Musk’s SpaceX, or as owner of smaller private companies like Burtons Foods in the UK, the maker of the decidedly homely Jammie Dodgers and Maryland Cookies brands – OTPP has a wide economic footprint that encompasses a broader set of risks than the traditional financial risk-return set-up.

Direct ownership of real assets brings a level of tangibility and connection to the real economy - but potentially also heightened questions around social responsibility and reputational risk. By OTPP’s definition, stakeholder groups include both regional and national governments but also residents around airport holdings, for instance.

As Mock puts it: “You become very acutely aware that you are carrying a responsibility to interface with that group of stakeholders, because they have a voice. They have an interest. And if you’re not taking care of that group, the governments that are actually giving you the privilege of investing in such assets, are going to have something to say about that.”

OTPP’s investment in water and sanitation in Chile – it supplies 30% of the water in the capital Santiago, where civil unrest started in mid-October – is a case in point. A rise in metro fares was the widely reported cause for the ongoing rioting and Mock makes a direct link between underlying issues of income inequality and OTPP’s investments in emerging markets.

OTPP’s investment, the CEO claims, has fundamentally improved water supply in the Chilean capital since the investment was made in the summer of 2011. “One of the benefits is, infant mortality dropped from a level that was third world country-like, down to the equivalent of G7 levels, because we invested the capital to deal with this kind of issue properly, where the Chilean government was not in a position to do so.”

But 24-hour news media mean that such investments are under constant scrutiny. “Our teachers watch this very, very closely. And in one second, if they ever thought that we were putting returns over people’s wellbeing, my phone and my emails will light up in the middle of the night like nobody’s business.”

A large organisation like OTPP can bring economies of scale to bear, but also a network effect of what Mock calls “horizontal connectivity”, which broadly refers to alignment and value creation across the portfolio: “Probably 70% of the value we have as an organisation is our horizontal connectivity. Buying something, leveraging it up, and driving return on equity through excessive leverage, those days are long gone.”

Few, like OTPP, can afford to acquire a team focused on airports, for instance or, indeed, can claim, as Mock does, to have at least some degree of diversification within their portfolio of airports. And few rub shoulders with the likes of Temesek or Carlos Slim’s investment operations in international deals.

OTPP and its Canadian counterparts might even over-bid for key assets where other considerations are at play. London City Airport, acquired in early 2016 from Global Infrastructure Partners by a consortium that included OTPP, is often cited in this regard. Overbidding is a loaded term, of course. For OTPP, the ability to take a longer-term view to value creation than a traditional private-equity fund horizon is crucial to how it values prospective assets.

Capital is white paint

Mock says scale of capital is no great distinction for global investors today.

“I can identify 50, 60 massive pools of capital around the world. And so capital is no longer a differentiator. Quite frankly, if somebody’s looking for capital, $500m cheques can easily be found. It’s like selling white paint.

“You’d better start thinking about, how am I a little bit different? The quality of partnership, the integrity with which you are dealing with your partners, and going in knowing that as a long-term investor one of your goals is to grow and improve the business.”

A key challenge – and opportunity to add value – is to leverage sector knowledge and transmit it between portfolio companies. Mock is keen to talk about how OTPP has helped the UK childcare company Busy Bees to expand in Asia, for instance. There are numerous other examples.

An important part of this has been the creation of a global strategic relationships unit within OTPP, which Mock describes as connecting between regions, companies and investors. “Global Strategic Relationships have made it their business to know all of our partners, all of our bankers, in all of our countries around the planet, in all of the companies that we own, and connect the dots,” Mock explains.

“When we sit down with a company, we need to be able to bring not just a cheque. We need to be able to bring pretty leading-edge HR thinking.” Indeed, Mock estimates that “maybe 40 to 50% of what we acquire, is because we are selected, even in a bidding process.

“The management will often come and say ‘we want Teachers’; you’re long-term capital, patient capital’.”

OTPP has also partnered with BCG Digital Ventures, the technology arm of Boston Consulting, to create an AI incubator. Named Koru, its objective is to interface with companies, and create new product lines through the use of AI and digital technology, for instance by devising efficiencies to drive EBITDA growth.

As part of the effort to boost “connectivity”, conferences of senior management from OTPP portfolio companies take place regularly across the world, including one yearly three-day global conference with around 300 CEOs and other senior executives. “Whether it’s high speed trains, airports, childcare companies, Jammie Dodger companies or lottery companies, we bring it all together.

“This is what’s pretty unique about Teachers’. We have more of a direct investing model than almost anybody that I know in the pension industry. And that has worked very well for us, both in infrastructure, private equity and, frankly, in real estate.”

Teaching and learning is a key to understanding how OTPP sees itself. This applies to both the organisation itself and the portfolio companies, and Mock describes the “knowledge equity” built up over the 29 years of OTPP’s existence as a key resource.

“Think of a classroom, think of learning, think of teachers, and mostly about ongoing learning. When this plan was started, while there was brilliant governance and insight, defending the model and operationalising it, is something that has to be ongoing.

“You have to maintain the independence of governance around this. You have to run it like a business. You have to have the freedom to create compensation structures that will attract the type of talent that you will need to handle the complexity of a global platform, and the kinds of businesses we invest in and operate.”

Moats and models

Can others adopt OTPP’s model? Along with other proponents of the Canadian model, has OTPP effectively built up a ‘moat’ or sizeable barriers to entry, around its operation? After all, it has built investment scale in private markets that few can rival, and can bid more effectively through its network, gaining opportunities that many other institutions don’t see. “We are paid well to think in a very competitive context,” as Mock puts it.

Mock denies that OTPP has built a moat – “that would suggest a level of protection, or even arrogance” – and advocates others adopt the kind of pay structures that his fund offers, even if he understands that political pressures and public scrutiny may make this very hard.

But he also cautions against glib assumptions that effective private market operations can be established in a short amount of time. “Replication of the model takes time,” Mock explains. “And by that I mean, you can get a good part of the way there, but it’ll take you a decade.” Not for the first time in the conversation, he cites the need for the right governance structure and for management to have the freedom to execute investment decisions.

As an active pension plan with growing assets, OTPP will need to continue to build its international network of people to identify and maintain a cutting edge in identifying a continuing stream of investment opportunities. This is still a considerable challenge. “We have to continue to innovate our value proposition for the people with whom we’re investing and the companies we’re investing in and buying,” as Mock puts it.

Mock has no ambition to have seats on multiple boards in his retirement. Instead, he wants to teach business, in Italian, and spend more time at his home in the Swiss-Italian lakes. What of his legacy at OTPP?

“We’ve built an organisation that is a learning organisation, that’s intended to deliver value to our partnerships as we need to deliver value to our partnerships above and beyond cheque writing. That is critically important. So there’s a long list of that kind of stuff but to me it’s a point of differentiation. It has to be, going forward.”

Ron was kind enough to get back to me late this afternoon and we had a lot to chat about. I first congratulated him on a beautiful stint at the top job and wished him well as he gets set to retire and spend more time at his home in the Swiss-Italian lakes.

The last time I spoke with Ron, he introduced me to Jo Taylor, OTPP's incoming CEO. We chatted quite a bit and I wanted to gather my thoughts to share some key elements of our conversation:

- Ron told me he liked the article above but there was a mistake in that he started as President and CEO on January 1st, 2014. He spoke to this journalist a month ago and said he wanted to focus more on talent and technology, two critical elements we discussed at length.

- Ron told me that assets will necessarily shift to Asia over the coming decade as "that's where growth will be" and to stay ahead, "we need to make sure we are attracting the talent and have the requisite technology to make sure we remain ahead of the curve."

- He said they're opening some new offices and are doing a global push to hire the "right talent with the right culture and mindset." He added: "This is critical if we are to stay competitive over the next 5 to 10 years."

- Ron kept harping on two critical elements: technology and talent. "If you don't have the right technology, you won't attract the requisite talent. Our organization needs to be agile or else we risk becoming stale and will be left behind in a world which is changing fast." He added: "We need to invest in our business and IT is a critical part of that investment." In fact, he said IT is "very sizeable" at Teachers' and "extremely critical" in all aspects of the operations.

- But he kept stating "technology is critical because tech will leverage talent." He said he has seen amazingly brilliant young people come work at Teachers' and it's critical they offer them the right development opportunities and mentoring. "This is critical if we are to continue delivering on our mission, making sure we are maintaining a fully funded pension plan over the long run."

- He said "they dropped the contribution rates" over the last few years but added "thank god we have conditional inflation protection which along with the surplus offers an additional relief valve if we ever run into trouble." He added: "This allows us to run with a level of risk we are comfortable with to attain our 4.5% real target-rate-of-return."

- In terms of investing in Asia, I asked Ron how important it is to have local partners and he said "it's critical", especially in Asia and Latin America. "We are comfortable investing in North America, Europe and the UK but still have trusted partners there. In Asia and Latin America, we need to know our limitations, you need partners that operate with the same integrity level and are aligned in terms of making businesses better over the long run (realizing on the value creation plan)."

- He gave me examples of the concessions on the Eurotrain going from London to Paris, Brussels airport "which is carbon neutral" and Bristol airport which is headed that way too. he also gave the example he gave in the article above, with how the infant mortality dropped in Chile once they invested in improving the water supply.

- In terms of having deep expertise, he gave me the example of how they own five airports in Europe run by a team of ten out of London who "if tomorrow, the main airport in Mexico City was up for sale, we can send them to do a deep dive." He said these platforms are crucial to Teachers' success and said that is what they did in infrastructure and private equity. He also added that is what Olivia Steedman is doing with TIP, "starting small and building it out."

- We talked about HR issues and I mentioned that from the outside it seemed as if Bjarne Graven Larsen, the former CIO, had a tough time fitting in culturally. Ron told me for family reasons, "it became difficult for Bjarne" but he added that "Ziad Hindo is going to be a superb CIO and it proves that Teachers' has an excellent bench, just like Dale Burgess, Olivia Steedman and others have stepped up to the plate." He said this is why three years ago his focus was on developing talent "so they are prepared to step into key roles when needed." Ron said the "turnover rate at Teachers' is abnormally low" but conceded some key investment professionals have left and there will always be some talent that leaves to go work elsewhere. He gave the example of Erol Uzumeri at Searchlight Capital "who has built a great fund with his partners". Interestingly, Andrew Claerhout, OTPP's former head of infrastructure, just joined Searchlight to lead infrastructure investments at the firm (see details here). He mentioned how Teachers' had some great talent in the past and specifically mentioned Mark Wiseman who went on to lead CPPIB and Claude Lamoureux who was inducted into the Canadian Business Hall of Fame earlier this year.

- Ron also mentioned Rosemarie McClean who will soon be the head of the UN Pension Fund and said that sometimes you need to bring new talent into the organization and specifically referred to Jo Taylor, OTPP's incoming CEO and Beth Tyndall, OTPP's Chief People Officer.

- We then moved our discussion to his long tenure at Teachers' and his transition into the CEO role and what he learned. Ron said he was privileged to have worked with good and smart people, stating several times that "culture is everything". He said "if you have the right platform that fosters innovation, the right governance, you can attract the right people." He said he "got to see the world, meet great partners and groups, and work with the smartest people."

- But he emphasized the key to all this was "the clarity of mission" which allowed the executive team to delegate authority and let them innovate. "You need engaged, excited staff which delegate authority. You want to hire the right kind of people who truly want to test their limits and if you're investing a dollar to develop them, you want $1.50 or $2 payoff, not 50 cents back."

- I asked Ron if Teachers' is ready for the next crisis and he told me that following the 2008 crisis, they moved the focus on liquidity and managing counterparty risk. "We borrow on 3 or 5 year terms and in different currencies. So, liquidity fundamentals, conditional inflation protection and bolstering our repo operations through central clearing making it less bilateral than is was are all critical." He added: "we conduct fire drills and recently did one a month ago where we scenario tested what happens if the S&P goes down and stays down for a few years."

- We then talked about hedge funds and private equity. Ron is an expert in hedge funds and he told me "the big, liquid shops which have invested enormous amounts into IT and talent will be fine and continue to gather assets but the smaller ($500-$700 million Long/Short Equity funds) will find it hard to survive."

- In private equity, he said they monitor leverage levels and pricing and thinks investors "need to be very selective" here.

- Lastly, I asked Ron what's next and he told me he doesn't want to take part in any board committees (seen his fair share of committees) and wants to lecture at a university because "education is the foundation of our democracy" and it gives him great pleasure to share knowledge with others. I told him I remember the first time I met him in 2002, he was extremely passionate about his subject matter and was a great teacher (he has it in him).

- Ron also told me Jo Taylor is ready to assume the role of CEO. "Jo has an international focus, he is performance oriented, acts with integrity and is decisive. He will be a great CEO and the board made the right choice."

- He ended by saying I've done a great job with this blog, "a true testament of your perseverance, professionalism and passion." I said it's because of people like him, Jim Keohane, and others that have stepped up to the plate to help me deliver great content.

Below, Ron Mock, outgoing president and CEO of Ontario Teachers' Pension Plan, discusses the global growth drivers for markets now and over the next decade.

Update: On December 30th, Ron Mock wrote his reflections on preparing for the future:

From my first day at Ontario Teachers’, I have been driven by our mission – to provide outstanding service and retirement security to our members. This has challenged me, every single day, to do better.Well put, Ron, very well put. Have a Happy & Healthy New Year and all the best in your next phase of life.

When I became CEO in 2014, I set out to make that mission our operational focus at every level. We attracted new people and sharpened our skills. And our peripheral vision got better as we stepped further out onto the global stage.

A true measure of performance for our pension fund is financial returns over time. Our OneTeachers’ investment strategy was key to aligning our board and management team with paying pensions over the long term, not just beating benchmarks. This inspired new departments, services and strategies— like our Total Fund Management and Global Strategic Relationships teams, our entrance into debt markets, and the launch of Teachers’ Innovation Platform and Koru. And, we’ve seen results. Our annual total-fund net return was 10.1% over the last 10 years, and 9.7% since inception in 1990 and we’ve held a surplus for six years straight.

We expanded more fully into global markets to diversify our portfolio, gain access to new opportunities and decrease risk. The local knowledge and relationships we have built help us navigate complex markets. This approach also helps us source, develop and motivate talent – the engine of our organization.

I’m extremely proud of the people who work at Ontario Teachers’. They foster insights that shape and sharpen our thinking. They nurture the relationships that drive our success. And the incredible depth of knowledge within our organization elevates good talent to great heights. We have a history as leaders in the pension industry, but we are not content with yesterday’s performance.

All these efforts are inspired by our members – good teachers impart knowledge, challenge expectations and nurture the progress of the next generation. While today’s changing world presents a lot of uncertainty, I believe the organization is well placed to fulfill our mission well into the future.

To the teachers of Ontario, it has been an honour.

Comments

Post a Comment