Naeem Aslam of Forbes reports that Warren Buffett dumps US bank stocks and buys a gold mining stock and that hedge funds dump tech shares:

On August 14th, we had a 13F filing update in the U.S., which gives more insight about the smart money and

how it is deploying its capital. Investors are always keen to know and

relate this information to their trading strategy. For retail traders,

this information can be seen as confirmation of whether their investment

strategy is correct and how they can fine-tune it.

Buffett Buys Barrick Gold

The most significant headline of the 13F filing was about Berkshire Hathaway’activity. It has purchased stock in Barrick Gold, a Canada-based mining company. Its position in Barrick Gold (GOLD) is worth nearly $565 million.

Buffett Dumps Goldman Sach, Still Owns Bank Of America

The Oracle of Omaha, Warren Buffett, reduced Berkshire Hathaway's positions in U.S. banks: JPMorgan (JPM), Wells Fargo (WFC) and PNC. It is critical to mention that Buffett still holds some U.S. banks, and Bank of America (BAC) is one of them.

Overall, it may not be a stretch statement to say Warren Buffett's

fund was more busy selling its positions— the fund sold its airline

stocks—than buying stocks during the coronavirus pandemic.

Saudi Sovereign Wealth Fund Sells Disney, Facebook, BP

The Saudi Sovereign Wealth Fund exited its positions in Disney (DIS), Facebook (FB), Boeing (BA)

and BP. Disney stock is mainly beaten down due to coronavirus, as the

Disney theme parks are still under the influence of Covid-19. Apart from

that, Disney is the stock among its peers that can see massive upside

in the coming quarters because of its new initiatives such as Disney+

streaming and also Disney premiering its new movies online—a new

territory.

The BP stock is very much an energy story. BP is making efforts in

the renewable sector; these bets can pay off in the long term.

Facebook is the giant in the social media space, and with the

introduction of Instagram Reels, it is ready to take on its competition,

TikTok. As for the Boeing stock, yes, the company is under pressure as

the entire airline sector is suffering massively. However, most of the

airlines are selling their old planes, and when the traffic does return,

we will likely see a surge.

Pershing Square Dumps Berkshire Hathaway

Pershing Square, which acts as more of an event-driven fund, has

exited its position in Berkshire Hathaway (BRK.B) and Blackstone (BX). The fund has

increased its exposure in the restaurant industry, as the coronavirus

has adversely influenced the sector. There are several bargains here,

such as Chipotle (CMG).

Aparna Narayanan of Investor's Business Daily also reports that Tesla and Apple are among the ten hottest stocks hedge funds bought in Q2:

Tesla stock saw strong interest from top hedge funds' in the second

quarter, with companies gaining from pandemic trends such as online work

and play generally in favor, the latest quarterly 13F filings with the

SEC show.

Here are the 10 stocks that were most popular among 150 winning hedge funds last quarter, as per new 13F filings tracked by Whalewisdom.com. The website uses a proprietary calculation to rank the stocks.

Individual investors use the regulatory data to assess where the

"smart money" is placing its bets. The 13F filings reflect hedge funds'

stock portfolio holdings at the end of each calendar quarter.

Workday (WDAY)

MercadoLibre (MELI)

Zoom Video Communications (ZM)

Apple (AAPL)

Tesla (TSLA)

Shopify (SHOP)

Coupa Software (COUP)

Zillow (Z)

Nvidia (NVDA)

Pinduoduo (PDD)

While hedge funds were generally hot on Tesla stock in Q2, the

Scottish fund manager Baillie Gifford, its largest institutional

shareholder, trimmed its stake by 2%. Tesla stock remains No. 1 in

Baillie Gifford's portfolio, at 10% of assets.

Apple kept its place as the No. 1 stock in Berkshire Hathaway's

portfolio in Q2. Berkshire Hathaway CEO Warren Buffett began gathering

Apple shares in Q1 2016 and is now one of the iPhone maker's three

biggest institutional shareholders. Apple stock accounts for more than

44% of Berkshire's portfolio.

Meanwhile, Zillow stock was recently featured in an IBD Stock of the Day column, which highlights stocks worth watching as they make notable moves on their charts.

Hedge Funds' Stock Buys And Sells

Among other notable hedge fund moves in Q2, activist investor Dan Loeb of Third Point reduced its Raytheon Technologies (RTX)

stake by 17%. Loeb had opposed the merger of United Technologies and

defense contractor Raytheon Company, which produced Raytheon

Technologies.

Third Point also added more than 4 million shares of Disney (DIS) to his portfolio. Disney stock now the biggest stock in Third Point's portfolio at 8.4% of assets.

David Tepper's Appaloosa Management boosted its Alibaba (BABA) stake by 49%, pared Amazon (AMZN) by 10%, and bought 5 million more shares of T-Mobile (TMUS). Those are now the top three stocks in its portfolio, accounting for roughly a third of Appaloosa's portfolio combined.

Hedge fund filings confirmed that Bill Ackman's Pershing Square fully

exited its large stake in Berkshire Hathaway last quarter, dumping

nearly 5.5 million shares. The sale was first reported in May, with

Ackman calling Berkshire Hathaway stock a "strong investment" but

suggesting he wished to act on new growth opportunities in the

pandemic-hit market.

Zero Hedge also posted a summary of what the most prominent hedge funds did in the second quarter, courtesy of Bloomberg:

ADAGE CAPITAL PARTNERS

Top new buys: RPRX, ABBV, W, HZNP, FIVE, ST, CCK, TRV, USB, JCI

It's that time of the year again, we get a sneak peek into the portfolios of top funds, with the customary 45-day lag.

Before I get into my thoughts on what top funds bought and sold in Q2, a little detour to bring you more up-to-date information on markets.

Earlier this week, Lu Wang of Bloomberg News reported the stock market is at a record forcing everyone to become a believer:

From professional investors to market handicappers, it’s becoming

next to impossible to stay bearish in the face of the rally in equities.

Fund

managers who went to cash when the pandemic broke out have been forced

back in to stocks, pushing measures of positioning toward historical

highs. Wall Street forecasters, some of whom threw up their hands in surrender

four months ago, are pushing up targets each day. Even Goldman Sachs

Group Inc., which once warned that bad loans and falling dividends could

drive a second leg of the bear market, now sees another 6% of upside in

the S&P 500.

While testament to the career pressure missing a $12 trillion rally

creates, the unanimity has become one of the biggest risk factors in

markets right now, with positions getting crowded as everyone is forced

to buy. A custom gauge of sentiment compiled by Citigroup Inc. showed

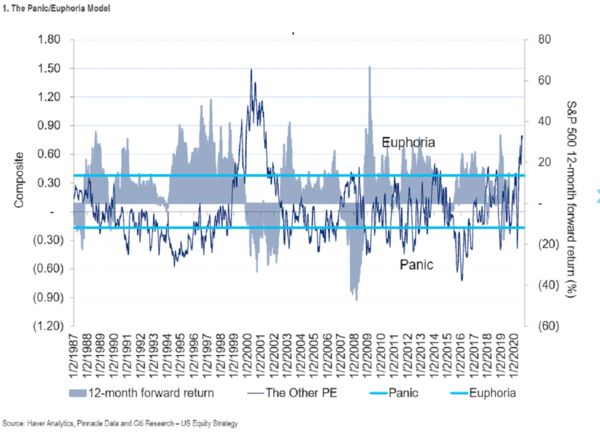

“euphoria” just hit the highest level since the dot-com era.

“While a new all-time closing high would certainly be

encouraging, it’s not always the pedal to the metal trade that it would

seem,” said Jonathan Krinsky, chief market technician at Bay Crest

Partners. “There is lot of optimism out there, which often makes

breakouts harder to sustain.”

Fear

of missing out gave birth to the rally and now it’s downright rampant

after stocks staged a powerful rebound from the fastest bear market

ever. Up more than 50% in less six months, the S&P 500 is poised for

the quickest recovery on record. The index rose to as high as 3,395.06

Tuesday, surpassing its prior intraday record reached in February,

before trading little changed on the day.

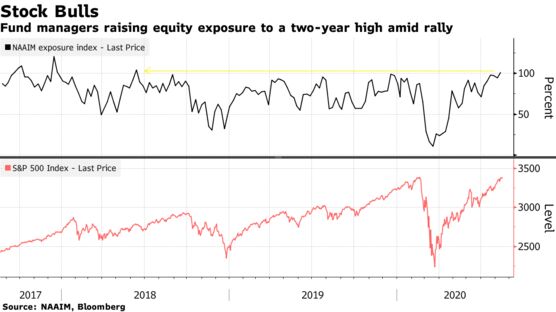

Money

managers are embracing the equity rally after cutting their exposure to

historically low levels during the downdraft, according to a survey by

the National Association of Active Investment Managers. The group’s

exposure index, tracking investment advisers from 200 firms overseeing

more than $30 billion, has risen to a two-year high. Even the most

bearish respondents are 50% long equities, something not seen since late

2017.

“Takeaways

from discussions with institutional investors indicate significant

comfort with central banks’ willingness to keep rates low for an

extended period,” Tobias Levkovich, chief U.S. equity strategist at

Citigroup, wrote in a note last week. “This is a marked shift from

commentary heard a month or two ago and reflects both

complacent/ebullient investor sentiment and a sense of rationalization

for the relentless bull run.”

Wall Street strategists, who rushed to cut price targets for

the S&P 500 during the March selloff, are now trying to catch up

with a rally that has defied most of their predictions. More than half

of the strategists tracked by Bloomberg have raised their projections

since June, when their projections were way below the market.

The latest skeptic giving in is Goldman’s David Kostin, who boosted his 2020 target by 20% to 3,600, the most bullish among peers. The call ended his months of skepticism over the market’s resilience, including a warning in May

that the S&P 500 would probably drop to 2,400 over the next three

months. Like the others, Kostin’s bullish case is centered around near

record-low interest rates.

“Share prices reflect not just the

expected future stream of earnings but also the rate at which the

profits are discounted to present value,” Kostin wrote in a note. “A

plunging risk-free rate partially explains why equities have performed

so well despite downward revisions to expected earnings.”

As stocks keep rising and turbulence subsides, demand from computer-driven

investors who buy and sell stocks on momentum or volatility signals, is

also returning. At Deutsche Bank AG, strategists including Binky Chadha

aggregated positioning among stock pickers and quant funds, and found

their overall exposure has increased to a one-year high.

Fund

positioning tends to show an inverse relationship with future market

returns, Deutsche Bank study shows. That is, the more bullish fund

managers are, the poorer the market performs in coming coming months.

While the current reading still signals positive market returns, with

gains averaging 1% over the next month, it also points to one third of

chances to go negative.

So much faith is put in the Federal

Reserve that investors are willing to pay up for earnings that’s

estimated to drop 20% this year. At 26 times forecast profits, the

S&P 500 was traded at the most expensive level in two decades. To

Peter Cecchini, founder of AlphaOmega Advisors LLC, all the index’s gains above 3,000 are unjustified.

“The

equity markets are now like an old elevator way over capacity,” said

Cecchini. “It’s just a matter of time before the cable snaps and its

passengers end up in the basement. That’s where the Fed will be

waiting.”

Speculators which include top hedge funds and bank prop trading desks used all that excess liquidity to buy risk assets, everything from junk bonds to tech stocks, to highly speculative vaccine stocks, some of which ran up as much as 3,000 or 4,000 percent year-to-date (before cooling off recently).

This is entirely rational behavior but make no mistake, we are in the midst of a massive liquidity bubble and even George Soros has publicly warned it's a liquidity bubble.

Anyone who thinks stocks would be up more than 50% since March lows and making new record highs without such massive Fed intervention is either a fool or completely delusional.

It's the Fed, stupid. The Fed took out the big bazooka and prayed it would work. It did, asset prices are all up all over the world, including in emerging markets, but the problem is the Fed has sown the seeds of the next crisis.

Why? Because a handflul of mega cap tech names -- Apple, Amazon, Microsoft, Google, Facebook, Netflix, NVIDIA, Tesla -- are melting up to bubble territory while the rest of the market is still depressed. This concentration risk is unprecedented as a handful of stocks represent almost 40% of the S&P 500.

Top hedge funds knew all this, they used the "Ackman bottom" when Bill Ackman went on CNBC in late March to scare the living daylights out of investors, to front-run the Fed and take super concentrated positions in a few tech names.

But most investors got caught flat footed, sold out of the market and didn't participate in this parabolic liquidity bubble over the last six months. Value investors, in particular, are underperforming once again relative to growth investors and some of them are jumping into this market to try to make some gains going into year-end for fear of missing out (FOMO).

On top of this, you have commodity trading advisors (CTAs) with trillions under management buying every breakout on the S&P and Nasdaq because that's what their systematic models tell them to do, driving stocks even higher.

Moreover, you have the passive investor craze where everyone is giving BlackRock, Vanguard, Fidelity and State Street money to invest in passive indexes which also exacerbates concentration risk and forces a handful of mega cap tech shares to fly to the stratosphere.

Of course, you also have the dumb day traders like Dave Portnoy who used this liquidity bubble to speculate on stocks, delusionally proclaiming "it's the easiest game ever".

And now, the final clincher, Wall Street strategists throwing in the towel, toppling over each other to raise their S&P 500 targets for the year based on the fact that record low rates warrant these forecast adjustments because there is no alternative (TINA).

It's enough to make any investor shake their head in disbelief.

I'm not a conspiracy theorist but given the vast fortunes Wall Street and a handful of tech gurus made since the pandemic erupted while many people have permanently lost their job, it makes you wonder.

Importantly, once again, the Fed has bailed out Wall Street and extremely high net worth individuals who invest in stocks and left everyone else to collect the crumbs Uncle Sam is sending them every month.

This is what capitalism has been reduced to, a charade that keeps benefiting the power elite and being a student of C. Wright Mills, I should have seen it all coming.

The late comic genius and social commentator George Carlin was dead right: "It's called the American Dream because you have to be asleep to believe it."

In his book, The Myth of Capitalism, Jonathan Tepper argues persuasively that regulators and competition bureaus are to blame, effectively killing competition to ensure monopsonies thrive.

He has many good points but the truth is capitalism is a system which thrives on massive inequality, that's its endemic engine and its ultimate demise because when this massive inequality becomes unsustainable, it will implode the system (we are seeing it every year with rising social tensions).

Why am I sharing all this with you? Because you have to think a lot bigger when looking at the stock market and ask yourself who is benefiting the most from this pandemic and what are the long-term consequences.

Top hedge funds invest on behalf of endowments, large global pensions and sovereign wealth funds but they also invest on behalf of ultra high net worth clients at Blackstone, Goldman, UBS Asset Management, and other big banks and their wealth management divisions.

The Fed has bailed them all out, at least so far, but when the next major crisis hits, even the Bezos and Gates of this world will get hit and hit hard.

Now, let me get back to top funds' activity. Have a look at these charts:

Everyone knows tech shares have outperformed the entire market but two stocks -- Apple and Microsoft -- make up almost 44% of the S&P Technology ETF (XLK) and ten companies which include names like Visa, Mastercard, NVIDIA, PayPal, Adobe and Salesforce, make up 70% of the holdings of this ETF (they've all done well except for Cisco).

This brings me to my next point: who cares what top funds are buying and selling, most of them are buying concentrated positions in the XLK and they're severely underperforming this ETF on an absolute and risk-adjusted basis over the last six months.

Yes, this can and will change when these high-flying mega cap tech shares get clobbered but why pay hedge funds 2&20 when the XLK only charges 13 basis points (0.13%)?

I'm being facetious, of course, but very serious investors have implemented a portable alpha strategy to invest in hedge funds where they swap into a stock or bond index and invest in non directional hedge funds which add pure alpha over a cash benchmark (typically T-bills + 500 basis points or 5%).

Paying fees to a hedge fund for beta bets is a losing strategy in these markets. Even the great Warren Buffett has a portfolio that looks awfully similar to the XLK but not quite which is why he's underperforming again this year.

Still, Buffett isn't stupid, he's raising billions in cash, and for good reason:

Other top hedge funds are undoubtedly doing the same thing and many of them are likely worried we might get a repeat of last September's Quant Quacke 2.0.

Can Apple and NVIDIA shares go to $600? Amazon and Tesla shares to $4,000? Sure, anything is possible in this Fed induced liquidity madness but be very careful chasing all these high-flyers because when the top hedge and quant funds pull the plug and decide to sell, it will be a bloodbath.

But what about the Fed? What about it? The tweet below summarizes everything you need to know:

"Mr. Powell I saw an overlay of the fed balance sheet against stonks, I mean stocks, and the balance sheet has plateaued and doesn't that imply tha- "

Notice, in the first table there's a bunch of speculative vaccine stocks and in the second, you have Apple, Google but also other names like Fedex, Chipotle, Domino's Pizza and Lululemon.

I was talking to a trader I know earlier today and told him Target (TGT) popped this week and it seems like all the quant funds are just going long anything making a new 52-week high (classic momentum trade).

He told me he sees a market of stocks and too many people are focusing just on mega cap tech names.

It's kind of hard not to when they're measuring their performance relative to the S&P 500.

By the way, maybe all these large powerful hedge funds should measure their performance relative to the S&P Tech ETF (XLK) but that will just decimate them.

Anyway, I've rambled on long enough, wanted to give you a lot of food for thought here.

Have fun looking at the latest quarterly activity of top funds listed below.

The links take you straight to their top holdings and then click on

the column head "Change (%)" to see where they increased and decreased

their holdings (you have to click once or twice to see).

These funds are run almost exclusively by men but one of the most impressive ones, ARK, is run by a lady called Cathie Wood, the best investor you never heard of (she's a Tesla bull and upped her stake in Q2).

Top multi-strategy and event driven hedge funds

As the name implies, these hedge funds invest across a wide variety of

hedge fund strategies like L/S Equity, L/S credit, global macro,

convertible arbitrage, risk arbitrage, volatility arbitrage, merger

arbitrage, distressed debt and statistical pair trading. Below are links

to the holdings of some top multi-strategy hedge funds I track

closely:

These hedge funds gained notoriety because of George Soros, arguably the

best and most famous hedge fund manager. Global macros typically

invest across fixed income, currency, commodity and equity markets.

George Soros, Carl Icahn, Stanley Druckenmiller, Julian Robertson have

converted their hedge funds into family offices to manage their own

money.

These funds use sophisticated mathematical algorithms to make their

returns, typically using high-frequency models so they churn their

portfolios often. A few of them have outstanding long-term track records

and many believe quants are taking over the world.

They typically only hire PhDs in mathematics, physics and computer

science to develop their algorithms. Market neutral funds will

engage in pair trading to remove market beta. Some are large asset

managers that specialize in factor investing.

Top Deep Value, Activist, Event Driven and Distressed Debt Funds

These are among the top long-only funds that everyone tracks. They

include funds run by legendary investors like Warren Buffet, Seth

Klarman, Ron Baron and Ken Fisher. Activist investors like to make

investments in companies where management lacks the proper incentives to

maximize shareholder value. They differ from traditional L/S hedge

funds by having a more concentrated portfolio. Distressed debt funds

typically invest in debt of a company but sometimes take equity

positions.

These hedge funds go long shares they think will rise in value and short

those they think will fall. Along with global macro funds, they

command the bulk of hedge fund assets. There are many L/S funds but

here is a small sample of some well-known funds.

I like tracking activity funds that specialize in real estate, biotech,

healthcare, retail and other sectors like mid, small and micro caps.

Here are some funds worth tracking closely.

Mutual funds and large asset managers are not hedge funds but their

sheer size makes them important players. Some asset managers have

excellent track records. Below, are a few funds investors track closely.

Pension Funds, Endowment Funds, and Sovereign Wealth Funds

Last but not least, I the track activity of some pension funds,

endowment and sovereign wealth funds. I like to focus on funds that

invest in top hedge funds and have internal alpha managers. Below, a

sample of pension and endowment funds I track closely:

Below, CNBC's Dominic Chu joins "Closing Bell" to discuss financials in the Berkshire Hathaway 13F filing. Is there a reason why Buffett dumoed so many US banks?I think he sees low growth and low rates are here to stay and hedged this deflation call with a stake in Barrick Gold.

More importantly, Howard Marks, co-founder and co-chairman at Oaktree Capital, the largest investor in distressed securities worldwide, warns the Federal Reserve and US Treasury can't keep stimulating the economy forever. He speaks with Bloomberg's Erik Schatzker on "Bloomberg Markets."

Comments

Post a Comment