The Fourth Inning Of Cyclical Leadership?

Hall of Fame analyst François Trahan is at it again.

After going underground for the last six months, Trahan, who turns 52 Sunday, on Friday announced the launch of Trahan Macro Research. In other words, he’s back in the macro strategy game full force.

Trahan was elevated to the All-America Research Team Hall of Fame in 2016 after winning the No.1 position for portfolio strategy in 10 out of the previous 11 years. Late of UBS, where he made a career pit stop as managing director of U.S. portfolio strategy from 2019 to 2020, Trahan was the co-founder of International Strategy & Investment Group spinoff Cornerstone Macro, co-founder of Wolfe Trahan, and executive managing director, chief investment strategist, and head of quantitative research at ISI.

His new boutique research firm at present has six employees and is in full hiring mode, according to Trahan, who said he is planning to scale up fast in the next few months.

“We are here to help investors navigate a profitable path forward in these turbulent times,” Trahan said in an interview. “Our collective talent and experience at combining macro and micro together will give a new and broad context to our work.”

He cited prioritization of in-depth research and meaningful exchanges with clients as the firm’s signature path forward. For now, the plan is to offer open research access to all.

Trahan, who hails from Montreal, began his career at BCA Research. He is a longtime acolyte of Evercore ISI chairman (and fellow Hall of Famer) Ed Hyman, to whom Trahan has previously credited his success and his reductionist philosophy of streamlining complex macro concepts to the simplest, easiest form possible — an approach he said he will continue to adhere to in this latest endeavor.

It's Friday, time to focus my attention on markets and what a crazy week it's been.

This week, I will start with great insights from François Trahan, one of the very best strategists/ analysts out there.

Full disclosure, François is a friend so I'm openly biased and shamelessly plugging his new research outfit which has Katherine Krantz as its CEO, another former BCAer and super smart lady.

Before I begin, please enter your email at Trahan Macro Research here and start receiving their research which is free for now.

Also, on the website, you will read this:

We are thrilled to announce the launch of Trahan Macro Research. After six months of hard work setting up the new firm, Francois and his team are back and focused on the macro backdrop once again.

The events of 2020 have left us with a macro puzzle that will take time to solve. Truth be told, the broader context for stock picking probably matters more today than ever before.

As a boutique firm, we choose to prioritize in-depth research and meaningful exchanges with clients and sincerely hope to help investors navigate the most profitable path forward. Our plan for now is to open research access to everyone. Simply fill out the form on this page to receive our work regularly.

Francois & Team

What I like about François is he understands macro extremely well and uses his understanding to then delve deeper into recommending sectors and industries.

He's not a trader, he's a top ranked analyst/ strategist and economist who makes great top down sector/ industry calls based on proprietary and readily available economic/ market indicators.

His research is read by the very best institutional funds in the world, and that includes elite hedge funds, so consider yourself lucky he has decided to give everyone access to it for now.

Anyway, you can read the latest research comment on why we are in the fourth inning of a cyclical leadership by clicking here.

He begins by stating this:

So, the Fed and the federal government have pumped an "insane" amount of monetary and fiscal stimulus into the pipeline and the economy is still in the early stages of benefiting from this.

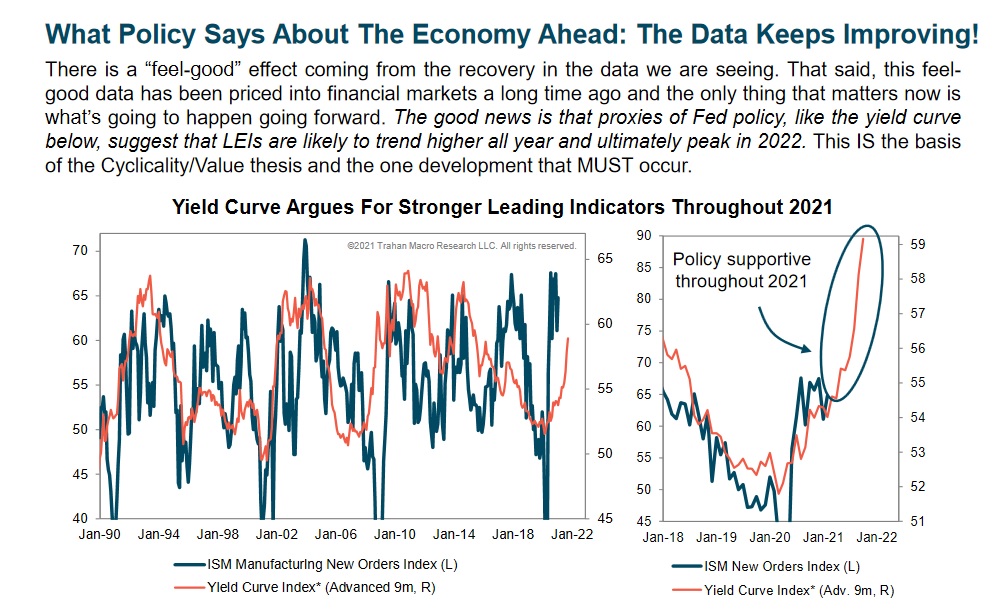

According to François, the yield curve is the best Anticipatory Economic Indicator (AEI) for timing the peak in the Leading Economic Indicators (LEI) and it suggests that this peak is unlikely to materialize until 2022.

And policy remains supportive of further growth:

Interestingly, he notes the last time investors faced a similar set of interest rates/ PMI conditions was in March 2017.

Just like today, back in March of 2017, consensus was very concerned about inflation and he states inflationary pressures only intensified over the course of the year as PMIs continued to trend higher.

What I find interesting is right above that chart, François Trahan states: "We believe that today investors should fear an easing cycle, not a tightening cycle, at least not in the near-term."

Wow! It seems like the world is scared of a tightening cycle or that the Fed is "behind the inflation curve” but right in that paragraph, Trahan is telling you to worry about another easing cycle.

This is something I wish he had expanded on but he didn't, maybe in a future comment he will.

Anyway, in terms of sectors and industries, Cyclicals (Risk-On segments) led and continued to lead thereafter, outperforming Defensives (Risk-Aversion trade) and while Risk-Off (Growth) basically performed in line with the S&P 500:

And most of the strong performance back in March 2017 was concentrated in Banks, Semiconductors and Transportation and these sectors continued to outperform through the end of the year.

The main lesson from March 2017 is stick with your winners this year as they're likely to outperform going into year-end as economic data improves:

Once again, please take the time to read the entire research comment here because I am covering the main points, you will learn a lot more reading the entire comment thoroughly.

Also, enter your email at Trahan Macro Research here and start receiving their research which is free for now.

So, are we going to see a redux of March 2017? Are cyclicals going to continue leading the rally going into year-end?

That's what it looks like but let me caution my readers some big cyclical stocks look quite extended here and others don't so you need to be careful with some winners and expect a nice pullback here, especially if the backup in yields subsides or even stalls.

For example, Financials (XLF), especially banks (KBE) and regional banks (KRE) bounced big on Thursday after the Fed meeting as the 10-year hit 1.74% and the curve steepened but gave up their gains from the highs and they seem very extended here:

I can say the same thing about Industrials (XLI) and Materials (XME), both on fire over the past year:

And then there's Energy (XLE) which has performed very well since the start of Q4 but seems to be stalling here:

Clearly, some cyclicals look better than others but there are some macro factors in the background that can play on cyclicals here:

- Have long bond yields peaked here? They seem to have overshot in the near term if you ask me but yes, the yield on the US 10-year Treasury note will likely rise up to 2% at the end of the year as the US economy continues to recover.

- On that point, I see the US economy gaining over Europe and other regions mostly because the vaccine rollout is going very well down south with 30% of the population now vaccinated (still not herd immunity but a lot better than many OECD countries).

- I see the US dollar coming back here and surprising a lot of people. I also expect all those shorting bonds now betting on inflation are going to be very surprised next year when it subsides.

Have a look at the TLT and UUP here:

The rout in long bonds is a bit overdone now and the US dollar has bottomed and is coming back lately.

Investors are all thinking the same thing: should we take profits on some of these cyclicals now that they rallied so much?

Put another way, do you buy shares of Goldman Sachs (GS), Caterpillar (CAT) and Deere (DE) here after a spectacular run-up, and there are plenty more that have had huge gains over the past year.

Maybe you stick with some winners but take some profits on others and wait for a nice pullback or look elsewhere.

Anyway, I can't get into all my thinking here but unlike François, I feel like the rally in some cyclicals is already in the eight or ninth inning and it will be very bumpy going forward.

Still, there's no doubt the US economy is recovering nicely and they will likely end the year up, outperforming other sectors, but what happens in the rest of the three quarters will be critical because I suspect a lot of trading/ rebalancing and rotation will be going on at the end of each quarter.

And if yields do decline or just stop rising precipitously, I expect Tech (XLK) will come back but the way the Nasdaq, Apple and many other shares that I track are trading, it looks very muted here and it remains to be seen if tech stocks can break from their current slump (they look toppish but if bond yield backup is done, they will rally here):

All this to say, while it looks a lot like March 2017, these markets are a lot more fickle and volatile and you need to be prepared for big corrections in all sectors.

But so far, it looks like François is right, stick with the winners, just don't be surprised if there will be a few major corrections along the way.

Alright, I am tired, spent a week glued on markets, absolutely insane action in some stocks this week, I need a break.

I wish you all a great weekend, stop fretting over inflation, the bond market, the Fed and yield curve control (YCC). A lot of what you saw this week is a total overreaction, much ado about nothing.

Below, CNBC's Bob Pisani takes a look at the market right after the open today and how markets performed this week. Listen carefully to his comments, I agree with him, as more and more retails and institutional traders dominate these markets, change is happening really fast.

Comments

Post a Comment