Three Bearish Billionaires And A Glimmer of Hope

For much of this year, the Fed has held steadfast to its goal of a “soft landing” for inflation, the idea of vanquishing inflation without a dramatic economic downturn.

But despite several interest rate hikes, inflation is still running hot, and business leaders are saying that it’s not a matter of if a recession will happen, but when.

On Wednesday, after another rate hike, and a promise from Fed chairman Jerome Powell to stay the course until inflation comes down, Bridgewater founder Ray Dalio said that the Federal Reserve will probably keep tightening its monetary policy until high prices come down, no matter the consequences. As a result, a recession is likely within the next year.

“You’re starting to see all the classic early signs,” he said during an interview with MarketWatch editor-in-chief Mark DeCambre during the outlet’s inaugural Best New Ideas in Money festival. Those signs, he said, are contraction in the housing and auto sectors, which are the first to be impacted by the Fed’s higher interest rates.

It’s not the first time Dalio has sounded the alarm on imminent economic trouble. In June, he was already arguing on LinkedIn that a soft landing was out of the Fed’s reach, even as Bridgewater beat the bear market in the first half of this year, delivering a 32% return to investors as other firms struggled.

Dalio’s comments followed the Fed’s decision this week to institute its third consecutive 75-basis-point rate hike this year. Prior to June, the last time the bank had made such a big rate hike was in 1994.

Those hikes have already slowed down economic growth significantly in the U.S., according to Dalio.

“We are right now very close to a 0% growth year,” he said. “I think it’s going to get worse into 2023 and then 2024, which has implications for elections.”

After the Fed’s rate hike on Wednesday, the S&P 500 fell 1.7% to a two-month low. Dalio joined other billionaire investors like Carl Icahn and said that the stock market will sink further this year as the Fed continues its hikes, adding that the bond market will be hit particularly hard.

“Who is going to buy those bonds?” Dalio asked, noting that there’s been a multi-decade “bull market” in bonds marked by elevated prices. “Now you have negative real returns in the bonds…and you got them going down.”

Last month, Federal Reserve Chair Jerome Powell said that the central bank will stop at nothing until inflation is under control, even if it means “some pain to households and businesses.”

This week, he was even more clear about the cost: “We have got to get inflation behind us. I wish there were a painless way to do that. There isn’t.”

That pain, said Dalio, will be very sorely felt over the next few years. “The Fed always has a tradeoff,” he said, between economic strength and inflation. With inflation now the bank’s target, it will chart a course until “economic pain” is deemed more severe than inflation.

At that point, the bank will begin to pare back on its rate hikes. “Now we play the game of, what level will that be?” said Dalio.

Ray Dalio isn’t the only billionaire sounding the alarm on stocks.

Will Daniel of Fortune reports Carl Icahn warns ‘the worst is yet to come’ for investors and compares US inflation to the fall of the Roman empire:

Throughout 2022, Wall Street has repeatedly warned investors that a recession could be on its way.

From JPMorgan Chase CEO Jamie Dimon to former Federal Reserve officials, the world’s top economic minds have pointed, practically in unison, to the storm of headwinds facing the global economy and expressed fears about the potential for a serious downturn.

In the U.S., consumers are grappling with near 40-year-high inflation and rising interest rates, all while the world struggles to cope with the war in Ukraine, the European energy crisis, China’s COVID-zero policies, and more.

And even after a more than 21% drop in the S&P 500 this year, Wall Street’s best minds still think stocks have further to fall.

“The worst is yet to come,” Carl Icahn, who serves as the chairman of Icahn Enterprises and boasts a net worth of $23 billion, told MarketWatch at the Best New Ideas in Money Festival on Wednesday.

Icahn made his name as a corporate raider on Wall Street in the 1980s, buying up unloved companies and aggressively advocating for change to improve shareholder value by appointing board members, selling assets, or firing employees.

Even at 86, Icahn remains one of Wall Street’s most respected minds, and this year he has repeatedly warned the U.S. economy and stock market are in trouble.

The investor argues the Federal Reserve boosted asset prices to unsustainable levels amid the pandemic using near-zero interest rates and quantitative easing—a policy where central banks buy mortgage backed securities and government bonds in hopes of spurring lending and investment.

“We printed up too much money, and just thought the party would never end,” he said, adding that with the Fed switching stances and raising rates to fight inflation, he now believes “the party’s over.”

The hangover from the Fed’s loose monetary policies, according to Icahn, is sky-high inflation, which rose 8.3% from a year ago in August.

“Inflation is a terrible thing. You can’t cure it,” Icahn said, noting that rising inflation was one of the key factors that brought down the Roman Empire.

Rome famously experienced hyperinflation after a series of emperors lowered the silver content of their currency, the denarius. The situation then dramatically deteriorated after Emperor Diocletian instituted price controls and a new coin called the argenteus, which was equal in value to 50 denarii.

The result of Roman emperors’ unsustainable policies was an inflation rate of 15,000% between A.D. 200 and 300, according to estimates by some historians.

Icahn said that inflation like this worries him so much that he would have liked to see the Federal Reserve raise interest rates by a full 1% on Wednesday, instead of the 75-basis-point hike that Chair Powell announced, to ensure price increases won’t stick around.

But despite Icahn’s inflation fears, the billionaire investor said he has managed to outperform his peers by hedging his portfolio—a strategy that uses derivatives to limit market risk and increase profits—during the market downturn.

Icahn Enterprises' net asset value jumped 30% or $1.5 billion in the first six months of 2022.

On Wednesday, Icahn argued that there are still stocks that look appealing on the market today, but he cautioned investors not to get greedy too soon.

“I think a lot of things are cheap, and they’re going to get cheaper,” Icahn said, arguing that companies in the oil-refining and fertilizer businesses should outperform the overall market moving forward.

Wednesday’s warning for investors wasn’t the first from Icahn this year.

The billionaire warned back in September that a recession or “even worse” was likely on the way for the U.S. economy and compared today’s high inflation with that of the 1970s, arguing the Fed will struggle to control rising consumer prices.

“You can’t get that genie back in the bottle too easily,” he said.

Last week, it was Stanley Druckenmiller who warned there is a ‘high probability’ the stock market will be ‘flat’ for an entire decade:

After a hotter-than-expected inflation reading spooked investors on Tuesday, the Dow Jones industrial average sank over 1,200 points in the stock market’s worst showing since June 2020.

That same day, Stanley Druckenmiller, one of Wall Street’s most respected minds, argued that the pain won’t be temporary—and that stocks face an entire decade of sideways trading as the global economy goes through a tectonic shift.

“There’s a high probability in my mind that the market, at best, is going to be kind of flat for 10 years, sort of like this ’66 to ’82 time period,” he said in an interview with Alex Karp, CEO of software and A.I. firm Palantir.

Druckenmiller added that with inflation raging, central banks raising rates, deglobalization taking hold, and the war in Ukraine dragging on, he believes the odds of a global recession are now the highest in decades.

And given Druckenmiller’s track record, investors would be wise to heed his warnings.

The legendary investor founded his hedge fund, Duquesne Capital, in 1981, and routinely outperformed the majority of his peers on Wall Street over the coming decades, delivering an annual average return of 30% from 1986 to 2010, according to Yahoo Finance.

But Druckenmiller really made his name when he led George Soros’s bet against the British pound in 1992, helping the billionaire pocket a cool $1.5 billion profit in a single month.

Druckenmiller eventually shut down his hedge fund in 2010 and converted it into a family office—a type of private firm established by wealthy families to manage their money—as many hedge funders typically do when they unofficially retire. But the leading investor’s views are still widely followed on Wall Street.

Reformed smokers

Druckenmiller’s argument for why the stock market is facing a decade of “flat” trading is based on the idea that central banks’ policies are shifting around the world from a supportive to a restrictive stance.

This shift is a result of the globalization that characterized the past few decades fading amid the war in Ukraine and U.S.-China tensions. Druckenmiller points out that globalization has a deflationary effect because it increases worker productivity and speeds up technological advancement, but now that’s gone.

“When I look back at the bull market that we’ve had in financial assets really starting in 1982…all the factors that created that not only have stopped, they’ve reversed,” he said, referencing current de-globalization trends like the rift between the U.S. and China, along with a move toward increased government spending and more regulation since the 1980s.

Druckenmiller went on to explain how central banks responded to the disinflation caused by globalization since the 1980s—and particularly after the 2008 Great Financial Crisis—with unsustainable policies that now have to be reworked.

“The response after the global financial crisis to disinflation was zero rates, and a lot of money printing, quantitative easing. That created an asset bubble in everything,” he said.

Central bank officials around the world are now moving away from the near-zero interest rates and quantitative easing—a policy of buying mortgage-backed securities and government bonds in hopes of spurring lending and investment—that have bolstered financial assets over the past few decades.

“They’re like reformed smokers,” Druckenmiller said. “They’ve gone from printing a bunch of money, like driving a Porsche at 200 miles an hour, to not only taking the foot off the gas, but just slamming the brakes on.”

To his point, the U.S. Federal Reserve has raised rates four times this year to combat inflation, and it’s not the only central bank attempting to bring down consumer prices with tighter monetary policy. From the U.K. to Australia, central bankers around the world are shifting to a more conservative approach and raising interest rates.

While that means financial assets, including stocks, will likely underperform over the next decade in Druckenmiller’s view, there is some positive news.

“The nice thing is, there were companies that did very, very well in that environment back then,” Druckenmiller said, referencing the stock market’s flat trading seen between ’66 and ’82. “That’s when Apple Computer was founded, Home Depot was founded.”

Druckenmiller also gave a caveat for investors when it comes to his pessimistic outlook, saying that this is the most difficult time in history to make economic forecasts and that he has a history of a “bearish bias” that he has had to work around his whole career.

“I like darkness,” he said.

It seems like a lot of billionaires like darkness these days as rates shoot up all over the world.

The common refrain is we are in for a whole lot of pain over the next couple of years and maybe longer as the era of ultra low rates is over, reversing into an era of high inflation, low growth and higher rates.

Central banks are way behind the inflation curve and now they are racing to put the genie back in the bottle.

They will eventually succeed, no doubt, but at a painful cost to the economy.

The magnitude and speed of rate increases are already hurting interest sensitive sectors and they will be felt throughout the economy over the next 18 months.

There will be no soft landing, that is impossible given what is happening and what central banks are trying to do.

I agree with those who see a hard landing ahead as recession odds skyrocket.

The big problem right now is whether central banks are making a policy mistake and risk tightening well into a recession.

It remains to be seen where the Fed's terminal rate will be but if core inflation remains sticky, it might be 5% or more and more quantitative tightening might be required (so far QT is negligible).

What does all this mean for stocks and bonds?

It means investors have to reprice risk and that process is still underway.

It means the old 60/40 portfolio will not generate anywhere close to the returns of the past 20 or 10 years and alternatives will need to kick in to make incremental gains.

Large, well capitalized institutional investors with a diverse portfolio across public and private markets all over the world -- like Canada's large public pension investment managers -- will be able to weather the storm as they have a long investment horizon and the right active management approach but even they will be hit if the recession is severe and drags on for a lot longer than usual.

But they have been bracing for tough times and will pounce on opportunities and deliver great returns over the long run.

It will be a lot tougher for individual investors to navigate this environment.

Over to the stock market, how low will it go is anyone's guess.

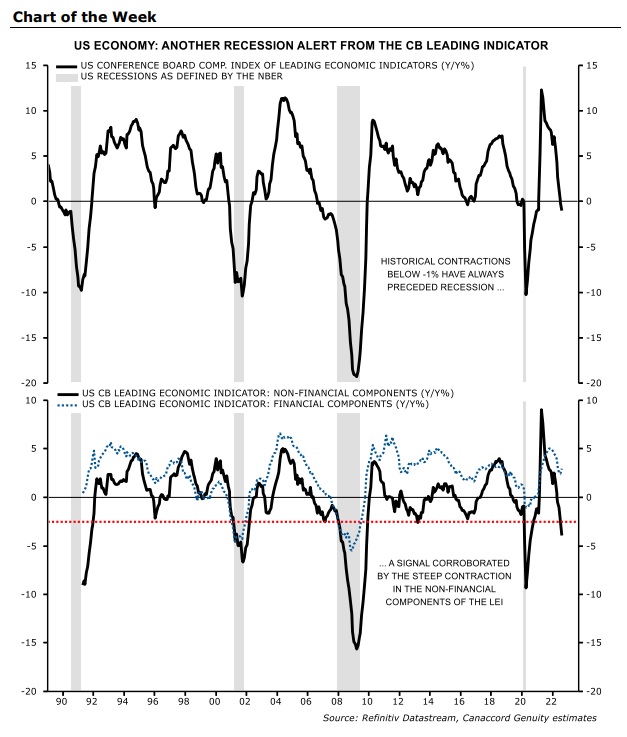

In his latest weekly market wrap-up, "R.I.P. Soft Landing," Martin Roberge of Canaccord Genuity writes:

So far this year, our investment strategy has been predicated upon three major assumptions: 1) inflation will remain sticky, preventing the Fed from doing an early pivot, 2) the economy will enter into recession in 2023, and 3) the stock market will need to find its own equilibrium, that is, without the helping hand of central banks. Recent inflation data are such that our first assumption does not need to be debated anymore. Inflation could come down in 2023 but likely not fast enough for the Fed’s taste. As for our recession call, our Chart of the Week shows that annual change in the CB leading indicator reported Thursday. History shows that annual contractions below -1% have led to US economic recessions, a signal corroborated by the steep contraction in the non-financial variables (-3.9% YoY) below the -2.5% boom-bust line. Then, if we think the stock market will need to find its own equilibrium and become cheap enough to buy before a Fed pivot, where is this valuation equilibrium? We believe the starting point is a >3% ERP which is ~SPX 3,600 and below current bond yield levels. However, a valuation reset is needed to incorporate an earnings recession and complete downward adjustments to 2023 EPS. This is ~SPX ~3,360. Last, we must account for our worst-case scenario which is paying 15-17x trough multiples on forward EPS declining 5-20% from peak earnings. This is ~SPX 3,100. Thus, our strategy remains to re-risk again and buying in 1/3 increments at SPX 3,600, 3,360, and 3,100.

In his weekly comment, Francois Trahan of Trahan Macro Research was surprisingly somewhat optimistic, stating he sees a Q4 rally but he also clearly states we are in the early innings of a bear market and stocks have not bottomed yet:

Francois will hold a conference call on Wednesday morning to go over his call for a Q4 market rally and I would encourage you to contact them at research@trahanmacroresearch.com to receive their research notes, they are excellent.

In an interview with The Market, Chen Zhao, Founding Partner and Chief Strategist of Alpine Macro says the Fed will overdo it but he remains bullish on US equities and long bonds:

Yes, I’m bullish on US equities and bullish on US Treasuries on a six month time horizon. I think long-term bond yields have peaked out – although, mind you, I said that a while ago and was wrong. But unless my logic about the path of inflation and the weakening economy is completely wrong, I think the equilibrium bond yield level in the US is about 2.5%. So today, duration represents a lot of value. I don’t think you want to be overweight anything else right now, because every world region has particular problems that are more severe than the US. But sometime in the later part of this year or early part of 2023, the dollar will probably start to soften. Because the forex market will sniff out a Fed pivot and move first.

It's a great interview worth reading it all here.

Anyway, I am just providing you with some market comments, the truth is this is a tough environment, the yield curve remains inverted and a recession is headed our way.

Stocks can easily bounce from these depressed levels because retail and institutional investors remain pessimistic.

Or something can go horribly wrong and we can see a panic selloff.

Nobody really knows what will happen in the short term but I am keeping my eye on high yield bonds (HYG) to gauge whether they are bottoming here (they typically lead stocks):

As always, wish you a great weekend and I only covered a small fraction of what’s behind this selloff in financial markets.

The world is a scary place, we are in for a very long hangover so be prepared for a lot tougher times ahead. If you have never experienced a rough bear market, you will see what it's all about (it sucks!).

Below, Stanley Druckenmiller and Palantir CEO Alex Karp discuss the rapidly changing geopolitical and economic climate. Fast forward to minute 27 to hear Druckenmiller discuss his macro views.

Comments

Post a Comment