CPPIB Up 10.1% in FY 2013

.bmp)

The Canada Pension Plan fund rode a wave of strong gains in foreign stock markets to push its investments up by 10.1 per cent last year and boost its assets to $183-billion.CPPIB put out a press release going over their fiscal 2013 results, providing fiscal year highlights of investment activity in public and private markets. You should also take the time to carefully read the Annual Report 2013 as it contains a lot more details.

While bonds and Canadian equity holdings posted slower growth in the year ended March 31, the Canada Pension Plan Investment Board, which manages the CPP’s assets, said its $64-billion portfolio of foreign equities had a stellar year.

Private equity holdings in foreign countries earned 17 per cent for the year, while publicly traded stocks in foreign countries posted 13-per-cent growth.

“That strength in global equity markets was the primary factor driving our solid returns for the year,” said Eric Wetlaufer, CPPIB’s head of public market investments.

The CPPIB’s overall returns were typical for a Canadian pension plan last year. A survey by RBC Investors Services Ltd. found that pension plans earned an average of 9.4 per cent on their investments in 2012, with the giant Caisse de dépôt et placement du Québec earning 9.6 per cent for the year ended Dec. 31, and the Ontario Municipal Employees Retirement System earning 10 per cent.

Over the past year, CPPIB has been threatening the Caisse’s long-held title as Canada’s largest investment fund. It has been difficult to directly compare the two fund managers, however, because they have different year ends, with the Caisse reporting assets of $176-billion as of Dec. 31, and CPPIB disclosing its assets hit $183-billion as of March 31, up from $162-billion a year earlier.

CPPIB said $5.5-billion of its asset growth in the past year came from net CPP contributions by employers and plan members, while $16.2-billion came from investment gains.

Chief executive officer Mark Wiseman told reporters Thursday the fund had “an excellent” year, but said his focus is not on annual returns but on an extremely long-term investment strategy to cover CPPIB’s long funding obligations.

Mr. Wiseman said CPPIB plans to become a public advocate for long-term investing around the globe, saying funds like CPPIB with a “natural multi-generational nature” don’t get enough credit for their beneficial impact on the economies.

By investing in companies for decades and funding innovation and growth, long-term investment funds spur long-term economic development, he said. Pension funds also act as a “shock absorber” during times of down markets when they become big buyers of stocks to maintain their investment weightings, he argued.

“You’re going to see us becoming increasingly vocal in encouraging market participants to adopt a more long-term lens, actually looking at value of stocks and not just looking at a stock as something that goes up and down on an individual day,” he said.

Mr. Wiseman said his proudest achievement in his first year as CEO of the fund is the 87 deals in 11 countries that CPPIB completed last year, including 36 that were worth more than $200-million each.

But André Bourbonnais, head of private investments, said deals appear poised to taper off this year as many more competitors are looking for bargains with plenty of available cash and cheap credit to fund their investments.

“If the environment remains as it is today, we’re going to be very selective,” he said.

The chief actuary of Canada has affirmed that the CPP is sustainable over the next 75 years if it earns an average of 4 per cent real annual returns after inflation. CPPIB said Thursday its 10-year real rate of return after inflation is 5.5 per cent, while it’s five-year rate of return is just 2.4 per cent, due mostly to large losses in fiscal 2009 when financial markets collapsed and CPPIB posted a 19-per-cent loss for the year.

The portfolio returns by asset class are available below (click on image):

.bmp)

The returns of every investment portfolio were positive. The big returns came from foreign public and private equities, up 13.2% and 16.8% respectively, but real estate and infrastructure also delivered solid results, up 9.2% and 8.8% respectively. Other debt, which I think is private debt, was up 15.1%.

The total Fund return in fiscal 2013 includes a loss of $348 million from currency hedging activities and a $1,414 million gain from absolute return strategies, which are not attributed to an asset class.

During fiscal 2013, CPPIB completed 87 deals in 11 countries that CPPIB, including 36 that were worth more than $200-million each. This alone blew me away. The due diligence on these huge deals and presenting them to investment committees and the Board for approval takes an enormous amount of work. These deals are complex, costly and have to be analyzed in detail to understand all the risks involved.

CPPIB's turnaround time to complete these deals is incredible, proving to me they run a very tight operation and are properly staffed to keep up such a breakneck pace. However, André Bourbonnais, head of private investments is right, if the environment remains as it is today, they will have to be a lot more selective.

One thing I know is that CPPIB has relationships with the very best private and public funds throughout the world and it has opened up offices in Asia and South America to capitalize on new opportunities.

As far as Mark Wiseman, CPPIB's President and CEO, he is right to extol the benefits of the long-term view:

Whether they like it or not, investors and company boards globally are going to hear a lot more from Canada’s biggest pension fund on the benefits of long-term thinking.Mark is right, companies need to think long-term and pension funds have a much longer investment horizon. Their results can't solely be judged on any given year.

CPP Investment Board has a mandate to identify investments that earn returns over many years to help cover the future retirement benefits of Canadians, so the fact that it takes a long-term investment view isn’t surprising. But Mark Wiseman, chief executive of the 183.3 billion Canadian dollar ($180.2 billion) fund, had a broader message Thursday for corporate boards and investors–that a pervasive focus on short-term returns could jeopardize the global economic outlook.

Mr. Wiseman likely isn’t about to become Canada’s version of Bill Ackman, the brash U.S. activist investor who last year successfully agitated to replace much of Canadian Pacific Railway Ltd.'s board and install a new chief executive. But he’s speaking out publicly about the merits of a long-term investment horizon.

Currently, “you will see” companies decide against an investment despite its merits to ensure they meet quarterly profit numbers, Mr. Wiseman told Canada Real Time.

But that can be a “terrible decision for shareholders and a terrible decision for the overall economy,” if jobs that could have been created are not, he said.

Last month, CPPIB was part of a group of big institutional investors that opposed a $17 million pay package for Barrick Gold Corp.'s new co-chairman, John Thornton. Shareholders ultimately voted against the miner’s executive-compensation proposals, but that vote was non-binding.

Next week, Mr. Wiseman will speak to Canada’s Institute of Corporate Directors and he said he plans to discuss the importance of long-term thinking for boards.

The executive believes CPPIB and other multigenerational pension funds can make a particular difference beyond their own returns, through investments in infrastructure, private equity and real estate.

These types of investments over time help generate jobs, innovation and overall growth, Mr. Wiseman said. But many investors don’t have the capital that these asset classes often require, or are unwilling to risk an investment that can’t quickly be sold if necessary. In addition, the complexity of arranging and financing these projects is often a deterrent.

CPPIB’s large size, significant resources and long-term investment horizon allow it to overcome these hurdles. And those same qualities allow CPPIB, and funds like it, to act as “shock absorber(s)” for the global economy, Mr. Wiseman said. That was the case during the global credit crisis, when they were able to buy assets other investors were forced to sell, he said.

Why is it important to understand the long-term view, especially when it comes to large pension funds investing in public and private markets? Look at CPPIB's performance against public market benchmarks in the press release:

CPPIB measures its performance against a market-based benchmark, the CPP Reference Portfolio, representing a passive portfolio of public market investments that can reasonably be expected to generate the long-term returns needed to help sustain the CPP at the current contribution rate.Again, 87 deals in 11 countries, including 36 that were worth more than $200-million costs a lot of money to set up in the short-run, but once these deals start realizing significant gains over the long-run, these costs will be recuperated and the CPP Fund will benefit from these transactions. That is why you can't just look at the negative $286 million in dollar value-added for fiscal year 2013 and jump to any conclusions.

In fiscal 2013, total portfolio returns closely corresponded to the CPP Reference Portfolio with $204 million in gross dollar value-added. Net of all operating costs, the investment portfolio returned negative $286 million in dollar value-added.

“We have strong conviction that our private market assets will outperform the public markets equivalents of the CPP Reference Portfolio over the long term,” said Mr. Wiseman.“ This result will, however, not necessarily be demonstrated in the short term. Particularly when public markets have rapid moves up or down, our active private market strategies may show short-term underperformance or overperformance vis-à-vis the CPP Reference Portfolio, which does not accurately reflect our long-term value-add expectations for these strategies.”

Given our long-term view, we track cumulative dollar value-added performance since the inception of our active management strategy in fiscal 2007. The cumulative outperformance added $3.1 billion to the CPP Fund net of all operating costs.

More importantly, as stated in the press release, public markets ran up in the first quarter of 2013, so the CPP Reference Portfolio took off in Q1 while private markets which make up roughly 38% of the Fund are appraised at the beginning of the calendar year. This was the primary reason behind the negative value-added over CPPIB's fiscal year which ended on March 31st. If public equities tanked in Q1, they would have showed considerable added-value over the CPP Reference Portfolio but again, this is meaningless on any given fiscal year. That is why compensation is based on four-year rolling returns and why it's best to look at cumulative dollar value-added performance net of all operating costs since inception of the active management strategy and forget yearly fluctuations in value-added.

Ultimately, the only thing that counts is the cumulative dollar value-added performance since inception of active management, net of all operating costs, and that is how you should properly judge any pension fund. The short-term comparisons to benchmarks are detrimental and just silly for these large pension funds, and I must confess, I've fallen into this trap in the past listening to my buddies in public markets. When you have significant investments in private markets, you need to look well past a year or two of value added.

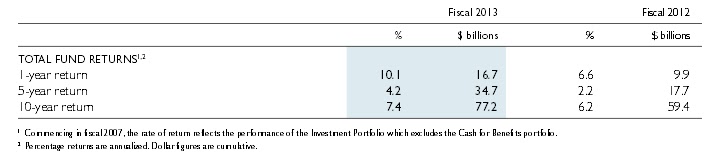

Below, you can view the long-term results of the CPP Fund (click on image):

A 7.4% return over the last ten years is solidly above their actuarial target. And if Mark Wiseman and senior managers at CPPIB are right in their conviction that private market assets will outperform public market equivalents of their CPP Reference Portfolio, they will add a lot of value over their benchmark, significantly bolstering the Canada Pension Plan.

Let me end by congratulating Mark Wiseman, the senior managers, and all the employees at CPPIB for their outstanding work and delivering another year of solid results. When you hear about reasons to go slow on expanding C/QPP or how C/QPP expansion is bad news for Canada, you should be very weary and concerned. If we want to improve our retirement system, we need to realize the enormous benefits these large public pension funds have over mutual funds and get on to expanding the CPP and QPP.

Below, Mark Wiseman speaks with Reuters' Chrystia Freeland from the World Economic Forum in Davos, January 24, 2013. He discusses CPPIB's long-term view, the shift into private market assets, the geographical diversification into Asia and South America, and the introduction of new groups looking into drug royalties and timberland.

Just like Ron Mock, his former colleague who was just named OTPP's next leader, Mark is brilliant and genuinely nice. Canadians are very lucky to have him at the helm of the CPP Fund and I share his conviction that the Fund will realize material gains in private market assets around the world over the long-run.