Investing Under Trump?

- Chen Zhao, the now retired former Co-Director of Global Macro Research at Brandywine

- Pablo Calderini, the President and Chief Investment Officer of Graham Capital Management

- Marko Papic, Chief Strategist, Geopolitics at BCA Research

- Yanick Desnoyers, Deputy Chief Economist of the Caisse de dépôt et placement du Québec

Before I begin, let me thank Claude Perron of Crystalline Management for inviting me to this event which he helped organize. For those of you who don't know, Crystalline is run by Marc Amirault and is Quebec's oldest hedge fund and among the first hedge funds established in Canada.

I posted a picture above with Claude, Mario, the panelists (on Mario's left) and the event organizers and sponsors to Claude's right (Stephane Amara, Sophie Palmer and Frederick Chenel).

Anyway, the event began with a presentation from Marko Papic discussing the geopolitical landscape. Marko was kind enough to send me his presentation and he wanted me to stress this point: "Fade Fed dovishness and fade ECB hawkishness."

It was the second time I saw Marko this month. The first time was at the International Pension Conference of Montreal which I covered here.

Marko started off with the way he sees the world over the next 24 months:

- U.S.: Trumps populist agenda - Tax cuts! - will pass

- Europe: Euro area collapse is overstated, but Italy is understated

- China: Beware of Beijing doing the "right thing"

According to Marko, passing these reforms is bad news for bonds and bullish for the US dollar.

As far as Europe, he stated that Le Pen never stood a chance and that Germany is turning radically Europhile (click on image):

Interestingly, he said that Europe has experience with populism which is why they implemented the social welfare state a long time ago. He said that populism is more rampant in the US and UK where there are free markets and less rampant in countries where the social welfare system is better (click on image).

Marko is bullish on Europe, stating Macron will be able to introduce major reforms in France and influence Germany to build a better Eurozone.

Equally interesting, he sees inflation pressures picking up in Europe, based on reforms and better growth prospects ahead due to monetary and fiscal policy.

He singled out Italy as a potential problem as the percentage of Italians who think they will be better off out of the Eurozone is climbing, but he didn't sound the alarm on 'Italexit'.

Also interesting, he sees Europe moving more to the right and the US moving more toward the left, stating: "If Trump fails his reforms, watch out in 2020, we might see someone in office who makes Bernie Sanders look like a free market candidate."

As far as China, he sees major structural reforms ahead which will be painful and have ripple effects across the world (click on images):

As I've stated previously, the biggest risk Marko sees ahead is in Asia (not the Middle East) where the Sino-American symbiosis is over and East Asia is the 21st century's powder keg (click on images):

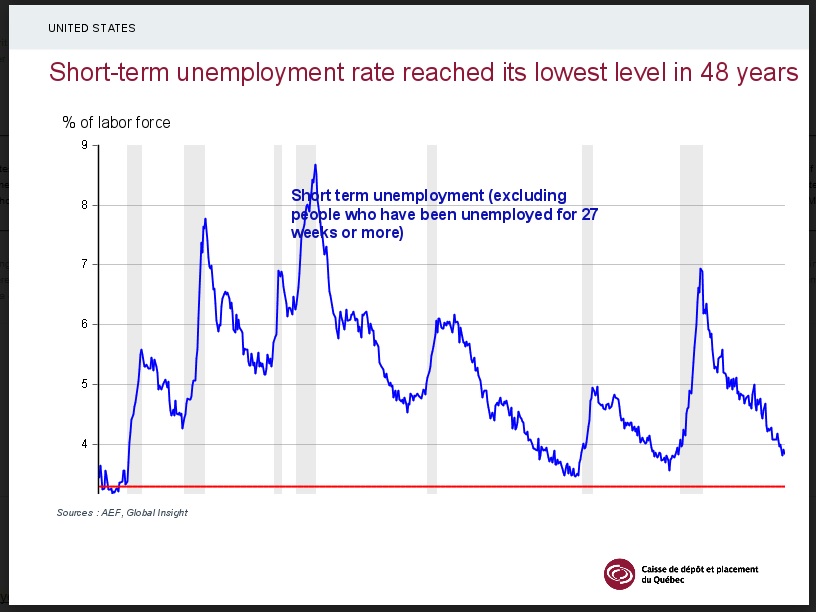

After Marko, Yanick Desnoyers, Deputy Chief Economist of the Caisse de dépôt et placement du Québec, gave an excellent economic overview of the US economy.

Yanick was also kind enough to give me a copy of his presentation. The big picture points are as follows (click on image):

As you can read, Yanick states the current US recovery is slower because of an ageing population and sluggish productivity growth (click on image).

However, he also states the US economy is in excess demand territory and it will be a challenge for the Fed to normalize rates with GDP growth so low (click on images):

But the chart that really caught my eye is the one below on signs of rising wage pressures (click on image):

I've never heard of the Atlanta Fed's Wage Growth Tracker:

The Atlanta Fed's Wage Growth Tracker is a measure of the nominal wage growth of individuals. It is constructed using microdata from the Current Population Survey (CPS), and is the median percent change in the hourly wage of individuals observed 12 months apart. Our measure is based on methodology developed by colleagues at the San Francisco Fed.Yanick told the audience this is a better measure than average hourly earnings. According to this Bloomberg article:

The Atlanta Fed's wage metric tracks the incomes of individual workers over time, and as such is not prone to the composition effects — like the exit of higher-paid baby boomers from the labor force — that have weighed on the usual measure of average hourly earnings this cycle.Moreover, according to Yanick, the Phillips Curve is alive and well (click on image):

"Average hourly earnings are more susceptible to compositional and demographic changes in the labor force, while the tracker is comparing the wages of the same individuals over time, providing a unique insight into wage growth," said Bespoke Investment Group Macro Strategist George Pearkes. "That growth has been strong and accelerating recently despite very modest inflation and some remaining underemployment."

Lastly, Yanick warned us that the Fed will have a hard time bringing the economy back to equilibrium (click on image):

Following these two excellent presentations, Mario Therrien moderated a panel discussion. Pablo Calderini discussed the dismal environment for hedge funds noting how a portfolio of stocks and bonds (50/50 or 60/40) had a higher Sharpe ratio than most hedge funds since the crisis because central banks have been backstopping markets.

However, he also warned that the normalization of rates and winding down of balance sheets will present excellent opportunities for top hedge funds, especially top global macro funds (like his).

Chen Zhao was the old Chen I knew from my BCA Research days stating "the consensus view is to be cautious on US stocks, bearish on bonds, bullish on the US dollar and negative on EM and commodities. And we all know the consensus is always wrong."

Non-consensus Chen was kind enough to share his thoughts with me via LinkedIn:

"My view is that while most analysts are trying to figure out where the next recession is, we might have already gone through "nominal recession" in 2015/16 when nominal growth around the world fell to usual recession levels. If so we may be at the start of a new cycle. This would suggest that stocks have further to rise, the USD might have topped out and the Fed would soon stop tightening. Commodities might have already reached the bottom early last year. That being said, I am not bearish on US bonds and 10 year yields could fall further."I pressed Chen to explain why he's not bearish on US long bonds if he feels we may be at the start of a new cycle:

"Last decade we had booms In American consumption and Chinese investment. This decade, desired investment in China has fallen dramatically and the US consumers spend at less than half of the speed. Nonetheless, China's saving rate has stayed at 50% and the US saving rate is a lot higher than last decade. In absolute terms, we are talking about $10 trillion in net new savings for the US and China alone. How much desired investment there is? Not much. This does not mention that governments are also trying to spend less and saving more (balance the budget). How is it possible for interest rates go up in this environment? I look for zero rates in the US when next recession hits. This is something different from past cycles."On China, there was divergent viewpoints between Marko and Pablo who were more cautious due to China's dangerous debt levels and Chen who is more bullish. "Nobody can figure China out because they don't really understand the economy," he said.

Chen made a good point that a large population of Chinese were still agrarian and that industrialization will move millions into the cities.

I asked Yanick a question on inflation, noting that inflation expectations are dropping despite the uptick in the Atlanta Fed's Wage Tracker. I covered my thoughts on inflation in my recent comments on Ken Griffin, the Fed making a huge mistake, and on the Bezos and Buffett effect.

Again, I'm in the deflation camp so when I see inflationistas warning of inflation, I tend to dismiss them as does the bond market. But Yanick is a top economist who worked at the National Bank prior to joining the Caisse so I pay attention to his views because he knows what he's talking about.

He told me that any notion that the Phillips Curve is dead is silly and that inflation pressures are building. Again, if this is the case, why are inflation expectations so low and why aren't bond yields surging?

I don't know folks, I'm still a deflationista and have strong doubts there is any significant wage inflation in the US (or elsewhere in the world) to worry about.

My macro thoughts remain the same:

- Long US stocks, especially biotech (XBI) and technology (XLK), but be ready for a major pullback in Q4 or Q1 of next year (hedge your portfolio with US long bonds).

- Long the USD (UUP). The US economy leads the global economy by six to nine months so get ready to see weakness in Europe and Japan in the last quarter and early next year (short the euro and yen relative to the USD)

- Long US long bonds (TLT). Stimulus or no stimulus, the US economy is slowing, inflation expectations are dropping, and long bonds will rally, especially if we get another crisis (flight to safety will support bonds and the greenback).

- Short Emerging Markets (EEM), commodities, energy, commodity currencies and commodity-weighted stock indices (Australia and Canada).

As always, please remember to contribute to this blog and support my efforts in bringing you some unique insights on pensions and investments. I thank all of you who take the time to contribute, it's greatly appreciated.

Below, a couple of clips where Marko Papic, Chief Geopolitical Strategist at BCA Research talks to Money Talk's Kim Parlee about how markets are understating risks in 2018 and why Italy is Europe's biggest threat (see the entire interview here where it is easier to watch).

Comments

Post a Comment