The Next Retirement Crisis?

The coronavirus crisis has punished the blameless across the world this year. That includes investors who did the supposed “right thing,” by keeping a balanced portfolio to fund long-term gains, just as the experts advise.It remains to be seen if the market "retests" its low from last Monday or slices right below it.

As the stock-market cascaded to its recent lows this month, the traditional portfolio of 60% stocks and 40% bonds suffered a greater than 20% decline from its peak value, for only the fourth time since World War II.

At last Monday’s low, this standard retirement allocation, as represented by the Vanguard Balanced Index Fund, was 22% off its peak Feb. 19 value – driven mostly of course by the 30% tumble in equity indexes that bonds only partially buffered. In fact, near the worst of the stock sell-off bonds were not offsetting the losses by rallying, as everything but cash was liquidated.

Upon request, Ritholtz Wealth Management research director Michael Batnick went back in history to track each time the 60/40 portfolio had taken at least a 20% hit. Such a decline struck initially at only the following points since 1945 (using month-end data for 60% S&P 500 and 40% five-year Treasuries): August 1974, September 2002 and January 2009.

The fact that the 60/40 autopilot approach has only retreated by 20% on a monthly basis four times in 75 years is itself a testament to the smoothing effects of offsetting equity-fixed income interplay.

What happened next after the prior 20% setbacks? Those months were all within months of the trough of major bear markets, though in each case the ultimate low for the stock indexes was still to come.

Batnick calculates that in those three instances in 1974, 2002 and 2009, it took between 10 and 20 months for this portfolio to recover back to its peak level.

An investor who kept to the disciplined approach and rebalanced holdings back to the 60/40 asset split at the end of the month when a 20% decline was first registered would have been positioned for attractive returns in subsequent years.

In those three instances, the average annual total return from the 60/40 portfolio was close to 12% over the following five years. That’s a healthy advantage over the very long-term average yearly return of around 9% for this asset allocation.

This is perhaps comforting, if not terribly surprising. Any investment discipline that triggers a move to take advantage of steep underperformance in one asset classes tends to be rewarded over time. And rebalancing after big declines in a blended-asset portfolio has generally been about buying nasty breaks in stock indexes.

Is 60/40 stance broken?

On a more opportunistic, shorter-term basis, strategist Terry Gardner of C.J. Lawrence last week noted that simply buying the S&P 500 the last three times it’s dropped 25% from a peak (1987, 2001 and 2008), as it did this month, has always led to positive returns over the next year – even though in none of those instances did the minus-25% level represent the ultimate low for stocks. Those returns one year out were 20% after 1987, 2.5% after 2001 and 18% after 2008.

Are there reasons to be skeptical that holding fast to the 60/40 stance this time will not fare as well as in past decades? Some investment professionals have discussed for some time that the essential premise of the 60/40 mix has been challenged due to extremely low bond yields that leave far less room for bonds to appreciate in an economic slowdown or crisis, mitigating their value as ballast to stocks.

Goldman Sachs strategists last week sounded a cautious note on this front last week with regard to the present market skid. “In addition to the sharper-than-normal equity correction, diversification in 60/40 portfolios has been less good,” the firm said. “With bond yields at all-time lows now and close to the effective lower bound, there is little space for most [developed-market] bonds to buffer equity drawdowns.”

Stretching deeper into history, skeptics might note the 60/40 portfolio carried a 20% loss for longer stretches in the 1930s, when stocks stayed deep underwater during the entire Great Depression.

So perhaps the traditional asset mix will get less help over time from bond yields squeezing lower in tough times (barring a move to negative yields, which would create a whole other set of issues). Still, bonds can still serve the role as cushion against equity losses.

Rebalancing aided the bounce?

The entire issue of rebalancing is hardly just an academic issue. The impulse from pension funds and automated asset-allocation vehicles to shift hundreds of billions in assets from fixed-income to stocks was detailed by strategists across Wall Street and was at least one significant driver of the surge in the S&P 500 into Thursday’s close.

The S&P 500 at its low point last week was underperforming the Barclays Aggregate Bond Index by some 30 percentage points year to date. Bespoke Investment Group notes that this effectively turned a 60/40 portfolio into a 55/45 mix, requiring one of the bigger rebalancing moves in years.

Of course, to the extent that this mechanical reallocation is timed to the quarter’s end, it means one short-term tailwind for the rebound rally has just about abated, as the market bounce leaves the indexes less stretched and investors have celebrated fresh trillions of dollars in support from the Federal Reserve and Congress.

Strategist Tony Dwyer of Canaccord Genuity, who’s been waiting for a retest of last week’s low to get more aggressively positioned, noted Friday, “Over coming days, the market will not be as oversold, the pension rebalancing will be done, and the bulk of monetary and fiscal stimulus will have been announced.”

While those factors could present a test of the immediate resilience of the market’s attempted comeback, they don’t much alter the case for long-term investors to take what the market has served up with its swift retrenchment this month.

As of Monday afternoon, stock market indexes are all up led by tech stocks (XLK) and I think investors are taking comfort in the fact the Fed wants everyone to know "the Fed put" is alive and well even if rates are at zero:

What it would take for the Fed to start buying stocks during coronavirus crisis https://t.co/XKeNzAF4Gg— Leo Kolivakis (@PensionPulse) March 30, 2020

“One of the questions asked most frequently is, isn’t the Fed out of ammunition? No, they still have plenty of tricks in their bag. Moving into further purchases of risk assets is one of the things they could do,” said Lauren Goodwin, economist and multi-asset portfolio strategist at New York Life Investments.But the Fed needs to be careful here because sometimes it makes a situation far worse, like in the mortgage market where bankers warn Fed mortgage purchases unbalanced the market, forcing margin calls:

Mortgage bankers warn Fed purchases of mortgages unbalanced market, forcing margin calls https://t.co/RBlcnqNz1e— Leo Kolivakis (@PensionPulse) March 30, 2020

In its letter to regulators, the MBA said: “The dramatic price volatility in the market for agency mortgage-backed securities [MBS] over the past week is leading to broker-dealer margin calls on mortgage lenders’ hedge positions that are unsustainable for many such lenders.”Anyway, back to the article on top, it got me thinking of the next major retirement crisis.

The letter went on to say, “Margin calls on mortgage lenders reached staggering and unprecedented levels by the end of the week. For a significant number of lenders, many of which are well-capitalized, these margin calls are eroding their working capital and threatening their ability to continue to operate.”

'The Government has helped everyone – apart from us pensioners' https://t.co/AiZ4ZOI7oa— Leo Kolivakis (@PensionPulse) March 30, 2020

One former senior pension fund manager shared this with me:

That article was cherry-picking the peak to trough move, which always makes things seem more extreme.The last email he is referring to came after he read my comment on whether Canada's top ten pensions are in trouble, sharing this:

I find it surprising that markets are not down more. A 60/40 portfolio would be up over 5% from Jan 1, 2019, despite the fact that we are now in something between a recession and depression.

As I said in my email last week, I think there is a lot more downside and that the world in the future will look very different and will certainly be less profitable and less about maximizing shareholder returns. So I don't see how markets will go back to a 20+ multiple.

I think that the big Canadian pension plans will be fine, they are well managed and came into this situation in very good financial shape. However this is going to be a disaster for US states and municipal plans. It was just a matter of time for many of them as their pension plans were so poorly funded, even when using completely unrealistic return expectation.This person is extremely knowledgeable, has tremendous experience and he is providing my readers with excellent food for thought.

Now these governments are having to pile on debt to bail out their economies. This may give them political cover to break their pension promises.

One thing that could hurt Canadian pension plans is longer term effects of the coronavirus on the assets they own. Two things come to mind - real estate and some types of infrastructure. This crisis may just hasten the demise of the retail sector and commercial office space. For example, OTPP owns about 17% of Macerich which is a publicly traded US REIT. It is down 92% from the end of 2015. The office sector has been booming in some parts of Canada but that may change if companies decide to take less space in the future as they find that employees can work efficiently from home.

Airports and toll roads are taking a HUGE hit in the short term. Will traffic volumes come all the way back? Did anyone do a worst case scenario for Hwy 407 that saw traffic down 90% for a month or more? These assets may need equity injections to stay viable, and their long term valuations may shrink as globablization reverses and the flight volumes at airports decreases.

I also think that long term equity markets will do less well due to (1) lower long term earnings, and (2) lower P/E multiples. Taxes are going to have to go up to pay for these bailouts and that will have to come from somewhere. Companies, and society, will now focus more on resiliency than efficiency which will hurt profits. Will the Eurozone survive this crisis? And this crisis is showing us that there are a lot of unseen risks in the world and you can't be pricing markets for perfection at a 20 P/E multiple. That just won't work over the long run.

The other risk that I am worried about in the long term is inflation. How are governments going to pay back all of the debt being issued? Do they inflate their way out of this problem?

I have more questions than answers but I think the future will look very different than the last 25 years, and I think we are going back to valuation ratios that we saw from 1880-1995 rather than what we have seen for the last 25 years. And note that we are STILL at high ratios in the US - to get to a P/E10 ratio of 10 markets have to fall by another 50%+. I don't think that will happen but I don't think we are going to see a snap back to an S&P500 of 3300 any time soon.

If you haven't already heard this I suggest you listen to this Recode/Decode podcast featuring Chamath Palihapitiya from last week (click here or here to listen to it).

We do not know the long-term effects of coronavirus and if we get into a serious recession or worse, depression, you'd better believe markets are going to feel the pain, even if the Fed goes all BoJ and starts buying up ETFs like the S&P 500 ETF (SPY).

A buddy of mine texted me earlier telling me he loves Microsoft (MSFT) BCE Inc (BCE) and Mastercard (MA), they are "saving his portfolio". I said I love these companies too but also told him to temper his enthusiasm.

Everybody is telling me this stock market crash feels like 1987, the ferocity of the selloff feels a lot like that year.

Then you have all the gurus (Bill Ackman, David Tepper, Paul Tudor Jones) telling us this is the time to get greedy.

Really? Do they have a crystal ball? Are they willing to forego all their massive fees if they're wrong and give money back to their investors?

‘Don’t be a hero’: Why some market watchers are reluctant to call a bottom despite big rally for stocks | Financial Post https://t.co/nOkWiy2yCe— Leo Kolivakis (@PensionPulse) March 29, 2020

When I look at the traditional portfolio of 60% stocks/ 40% bonds (VBINX), I see a lot of pain out there:

And unlike Canada's large well governed DB pensions, these retail investors can't pool investment or longevity risk, so if they are retiring soon, they're in big trouble.

What else? Unlike Canada's large well governed DB pensions, retail investors can only invest in stocks and bonds, not private equity, infrastructure, unlisted real estate, private debt, commodities, etc.

They also can't invest in top hedge funds getting bailed out by the Fed and commodity hedge funds crushing it as oil prices sink to new lows:

The Hedge Fund Bailout Worked: Citadel, Millennium And Point72 Recover Most Of Their March Losses | Zero Hedge https://t.co/XptVkGnUsz— Leo Kolivakis (@PensionPulse) March 30, 2020

Hedge Fund News: Pierre Andurand Oil Fund Surges 57.5% in March - Bloomberg https://t.co/56xDTnO8iJ— Leo Kolivakis (@PensionPulse) March 30, 2020

By the way, Pierre Andurand didn't just call the plunge in oil prices right, he also called the entire coronavirus crisis right and early on, he saw what I saw, namely, a disaster in the making as asymptomatic people spread the virus to everyone.

Anyway, I am worried about two things right now:

- Chronically underfunded US state and municipal pensions which are on the brink of collapse

- And a generation of people retiring who are condemned to pension poverty

It's the pensions which came into this crisis in bad shape with a terrible funded status as well as people with no pensions at all who just saw their retirement accounts get creamed and probably sold at the wrong time.

The next retirement crisis is already upon us. Anyone who thinks otherwise is delusional.

Sure, there's unprecedented fiscal and monetary policies all over the world but that’s a symptom of the crisis at hand.

I might be wrong, markets might continue surprising everyone, climbing the wall of worry, but I think it's highly unlikely, especially since the economic fallout will likely linger for some time.

Who knows? Maybe the market is anticipating a major breakthrough, peak deaths, or whatever, but if you've been listening to Dr. Fauci very closely, you'd better brace for more bad news ahead:

Dr Fauci warns up to 200,000 Americans could die from coronavirus https://t.co/M7frSqiqqc— The Independent (@Independent) March 29, 2020

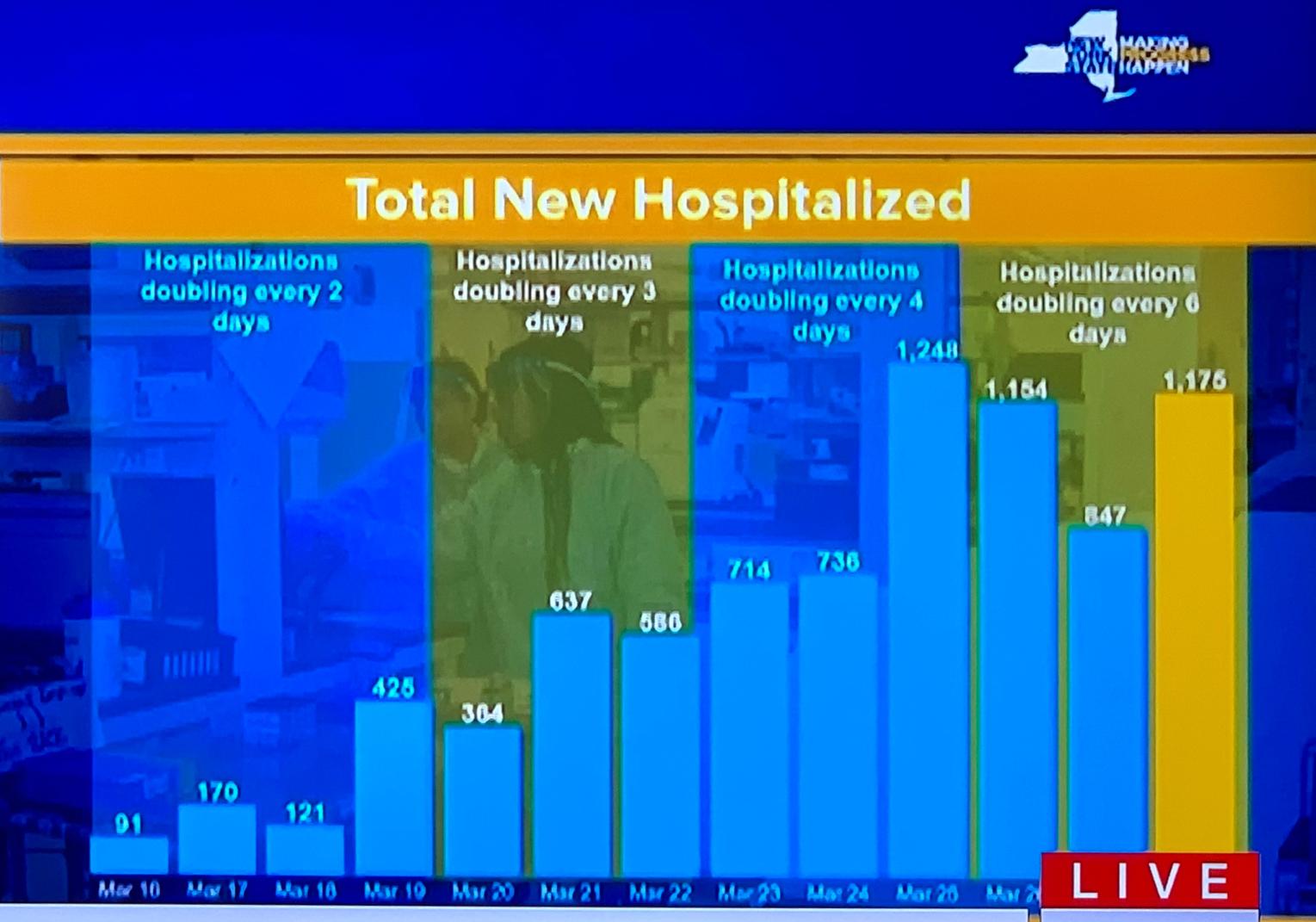

By the way, Evangelos Momios, Senior Director and Financials Sector Head at PSP Investments, posted three hopeful charts on LinkedIn yesterday from New York Governor Cuomo's press conference:

I thought these were excellent charts and I shared them with some friends.

A friend of mine in New York said this: "Unfortunately I think this is only noise. Deaths peak about three weeks after the beginning of a lockdown so for NYC that would be the end of next week ... it will be ten times that I fear.”

Another close friend of mine, a top physician in the US, shared this with me:

Go here and enter state of New York at the top and you can see they predict peak count of daily deaths in ~9 days. You can compare to other states which are mostly 3-4 weeks away for peak daily deaths. New York is woefully short of beds in the hospitals and ICU…..the worst shortage numbers I have seen for any state at this site. They are and will continue to be triaging ventilators - that means if you need one at the same time as someone else, there will be rationing based on chances of survival (so older subjects with co-morbidities will be let go). New England is generally in a lot of trouble because density of population and lack of beds/ventilators. Florida is OK…... California needs some ventilators, not beds. In general, densely populated states are in worse shape than less densely populated states.I trust my friend, he's not only a top physician, he's a top epidemiologist who understands the numbers better than anyone else.

[Update: My friend shared an update with me stating this: "Florida is now in trouble based on these models due to recent trends while California is in better shape with no ICU bed shortage projected...I am hopeful that we are starting to see dividends from the early institution of social distancing. Our county (Santa Clara) was the first in the nation to implement."]

I also believe China is blatantly lying about its coronavirus figures. So is Iran and so are others. The only data I trust is from developed countries and even there, it varies between countries and even states/ provinces (some are way ahead of others in terms of testing and tracking).

Lastly, everone is talking about this op-ed on how if everyone wore some sort of mask (not just an N95 mask), it could help flatten the curve.

Simple DIY masks could help flatten the curve. We should all wear them in public. https://t.co/8AoLZYsA7f— Leo Kolivakis (@PensionPulse) March 30, 2020

It makes perfect sense, there's also a video circulating on YouTube on how we all need masks, but I warn you, if you can't make or get masks, it's much more sensible to stay home, stay healthy, and if you venture out, avoid crowds, and wash your hands thoroughly the minute you get back home.

It's annoying, it's painful but next time you whine about it, think about the hell those frontline healthcare workers at our hospitals are witnessing and just stay home, you will potentially be saving lives, including your own.

Remember, even if it's benign for most people, it's deadly to others, and you simply don't know who it will impact and how hard it will impact them. You also don't know if you're carrying it and are asymptomatic and spreading it which is why you need to practice physical distancing and just stay home as much as possible.

This morning, my friend in New York texted me telling his friend was rushed to the hospital and is now on a ventilator in the ICU of the hospital. This is a healthy 48-year old male, a father and husband of a healthcare worker who had high fever that wasn't breaking so his wife rushed him to the hospital.

I just pray they will be able to treat him successfully but I'm sharing this because people need to understand, this virus isn't something to fool around with and everyone needs to their part so we can get past this nightmare, and that's what this is, a total nightmare and some have it a lot worse than others, so please stay home, stay safe and stay healthy!!

Below, Guggenheim Global CIO Scott Minerd joins 'Fast Money' to discuss his recent paper and where he thinks the economy could he headed if the coronavirus pandemic continues.

And Dr. Anthony Fauci, Director of the National Institute of Allergy and Infectious Diseases, explains the latest timeline and expectations around COVID-19 in the US as well as Trump’s change of course.

Comments

Post a Comment