CPP Investments Gains a Record 20.4% in Fiscal 2021

CPP Investments released its fiscal 2021 results, gaining a record net annual return of 20.4%:

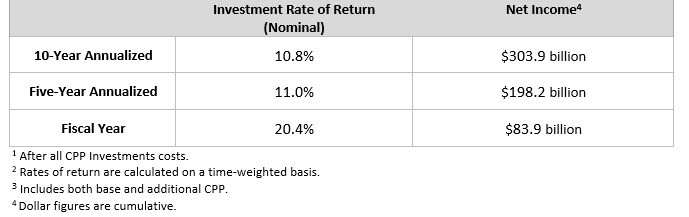

Canada Pension Plan Investment Board (CPP Investments) ended its fiscal year on March 31, 2021, with net assets of $497.2 billion, compared to $409.6 billion at the end of fiscal 2020. The $87.6 billion increase in net assets consisted of $83.9 billion in net income after all costs and $3.7 billion in net Canada Pension Plan (CPP) contributions.For the fiscal year, the Fund returned 20.4% net of all costs, the highest return since inception. The Fund, which includes the combination of the base CPP and additional CPP accounts, achieved 10-year and five-year annualized net nominal returns of 10.8% and 11.0%, respectively.

CPP Investments continues to build a portfolio designed to achieve a maximum rate of return without undue risk of loss, taking into account the factors that may affect the funding of the CPP and the CPP’s ability to meet its financial obligations. The CPP is designed to serve today’s contributors and beneficiaries while looking ahead to future decades and across multiple generations. Accordingly, long-term results are a more appropriate measure of CPP Investments performance compared to quarterly or annual cycles.

In the five-year period up to and including fiscal 2021, CPP Investments has contributed $198.2 billion in cumulative net income to the Fund after CPP Investments costs. Since its inception in 1999, CPP Investments has contributed $343.7 billion to the Fund on a net basis.

“The Fund performed exceptionally well in fiscal 2021, with all investment departments capitalizing on improving global equity markets following the steep declines observed at the end of fiscal 2020,” said John Graham, President & Chief Executive Officer, CPP Investments. “The fiscal year was bookended by extremes, with markets reaching new record highs following the significant lows just 12 months earlier. Our discipline ensures we keep the Fund on track, demonstrating resilience in a crisis and strong growth on the upside. With optimal diversification, including access to private assets, the Fund continues to perform as designed.”

CPP Investments established an ambitious business plan going into fiscal 2021, as the global pandemic arrived at our offices across five continents. Virtually all employees pivoted to remote work for their safety, and to help protect our communities. The circumstances affected regular business activities, including in-person engagement with partners and portfolio companies. Enterprise-wide teams quickly adapted to ensure full implementation of our business plan and regular operations, including managing existing assets and completing hundreds of new transactions while upholding high standards of risk management and compliance.

“The organization never paused despite the personal and professional challenges of operating during a global pandemic. Everyone leaned into their work, collaborating remotely to best serve CPP contributors and beneficiaries. Delivering strong results that contribute to the sustainability of the Fund helps remove at least one potential worry for millions of households – and there is no greater motivation for us in the full spirit of our purpose,” Mr. Graham added.

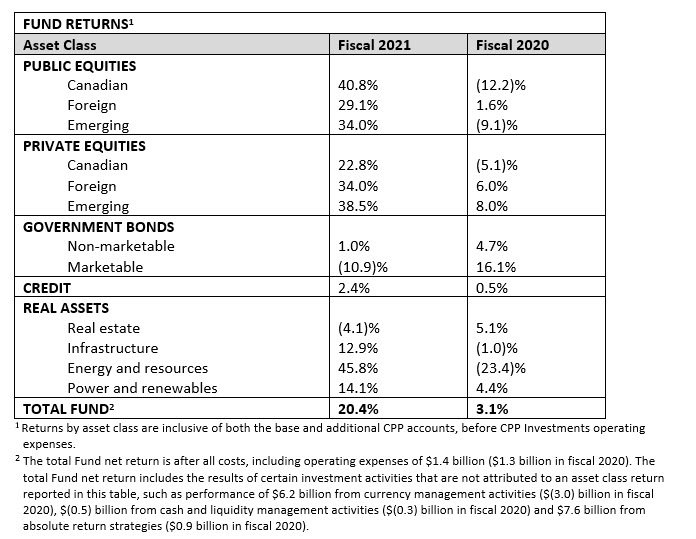

All six investment departments exhibited positive performance over the fiscal year. Global equities, across both emerging and developed markets, contributed to significant investment returns for the Fund. Amid these buoyant markets, foreign exchange losses of $35.5 billion curtailed the Fund’s gains due to a strengthening Canadian dollar against the U.S. dollar during the fiscal year.

“Diversification, prudent risk-taking in investment selection and high-caliber global teams propelled the Fund as we near the half-trillion-dollar milestone about seven years before it was projected at inception,” added Mr. Graham.

Fund 10- and Five-Year Returns1, 2, 3

(for the year ended March 31, 2021)

Performance of the Base and Additional CPP Accounts

The base CPP account ended the fiscal year on March 31, 2021, with net assets of $490.9 billion, compared to $407.3 billion at the end of fiscal 2020. The $83.6 billion increase in net assets consisted of $83.5 billion in net income after all costs and $0.1 billion in net base CPP contributions. The base CPP account achieved a 20.5% net return for the fiscal year.

The additional CPP account ended the fiscal year on March 31, 2021, with net assets of $6.3 billion, compared to $2.3 billion at the end of fiscal 2020. The $4.0 billion increase in net assets consisted of $0.4 billion in net income and $3.6 billion in net additional CPP contributions. The additional CPP account achieved an 11.6% net return for the fiscal year.

The additional CPP, that began in 2019, differs in contributions, investment profile and risk targets from the base CPP because of the way each part is designed and funded. As such, we expect the investment performance of each part to be different.

Long-Term Sustainability

Every three years, the Office of the Chief Actuary conducts an independent review of the sustainability of the base and additional CPP over the next 75 years. In the most recent triennial review, published in December 2019, the Chief Actuary reaffirmed that, as at December 31, 2018, both the base and additional CPP continue to be sustainable over the 75-year projection period at the legislated contribution rates.

The Chief Actuary’s projections are based on the assumption that, over the 75 years following 2018, the base CPP account will earn an average annual real rate of return of 3.95% above the rate of Canadian consumer price inflation, after all costs. The corresponding assumption is that the additional CPP account will earn an average annual real rate of return of 3.38%.

The Fund, combining both the base CPP and additional CPP accounts, achieved both 10-year and five-year annualized net real returns of 9.1%.

Relative Performance against the Reference Portfolios

CPP Investments has established benchmarks of passive, public market indexes called Reference Portfolios that reflect the targeted level of market risk that we believe is appropriate for each of the base CPP and additional CPP accounts, while also serving as a point of measurement when assessing the Fund’s performance over the long term. CPP Investments performance relative to the Reference Portfolios can be measured in dollar terms, or dollar value-added, after deducting all costs.

On a relative basis, the aggregated Reference Portfolios’ return of 30.4% exceeded the Fund’s net return of 20.4% by 10.0%. As a result, in fiscal 2021, net dollar value-added for the Fund was negative $35.3 billion.

The base CPP account earned a net return of 20.5%, which was less than its Reference Portfolio’s return of 30.5% by 10.0%. This equates to a single-year net dollar value-added of negative $35.2 billion, after deducting all costs. The additional CPP account earned a net return of 11.6%, which was below its Reference Portfolio’s return of 17.0% by 5.4%. This equates to a single-year net dollar value-added of negative $93.7 million, after deducting all costs.

In investing for the long term, the Fund grows not only through the value added in a single year, but also through the compounding effect of continuous reinvestment of gains (or losses). We calculate compounded dollar value-added as the total net dollars that CPP Investments has added to the Fund through all sources of active management, above the returns of the Reference Portfolios.

CPP Investments has generated $28.4 billion of compounded dollar value-added, after all costs, since the inception of active management at April 1, 2006.

While the Reference Portfolios provide a comparable measure of the level of risk required to fulfill the Fund’s long-horizon mandate, CPP Investments has deliberately and prudently constructed a portfolio that is significantly more diversified, including by asset type, region and sector, and includes considerable weightings in private equity and real assets. This is designed to minimize short-term volatility and generate more consistent returns compared with a portfolio that is mainly exposed to public equity markets. Our active management strategy has resulted in the Fund exceeding the return of the Reference Portfolios on a cumulative basis since inception, demonstrating lower volatility while serving as a safe harbour during periods of stress.

Managing CPP Investments Costs

CPP Investments is committed to maintaining cost discipline as we continue to build a globally competitive platform that will enhance our ability to invest over the long term. The Fund’s performance is reported net of costs, as is the net income generated by each investment department.

To generate $83.9 billion of net income, CPP Investments directly and indirectly incurred $1,417 million of operating expenses, $2,723 million in investment management fees paid to external managers and $291 million of transaction costs. Altogether, these costs totalled $4,431 million for fiscal 2021, compared to $3,452 million for the previous year.

Total operating expenses of $1,417 million represent 31.4 cents for every $100 of invested assets, compared to $1,254 million in fiscal 2020 or 30.6 cents. Operating expenses of 31.4 cents are in line with the five-year average of 31.5 cents, even as we continue to enhance our capabilities in technology and build our global talent. Investment management fees increased by $915 million in the fiscal year, driven by a greater volume of assets under the direction of external fund managers, growth of funds in emerging markets, and higher performance fees paid to fund managers in public market strategies and real estate. Performance fees are paid to external managers when higher than expected returns are earned for CPP Investments, which helps ensure an alignment of interests. Transaction costs decreased by $99 million compared to the prior year as we pursued fewer private market investments. Transaction costs vary from year to year as they are directly correlated with the number, size and complexity of our investing activities in any given period.

CPP Investments also incurred financing costs associated with its use of leverage. CPP Investments’ strong balance sheet, measured by a “AAA” credit rating, has increasingly provided access to a range of cost-effective financing options to make additional and more diversified investments while maintaining the Fund’s risk and liquidity targets. Financing costs include expenses from a variety of leverage generating strategies, ranging from debt issuances to derivative transactions. Financing costs were $1,217 million in fiscal 2021, a decrease of almost 50% compared to $2,429 million for the previous year. The decrease over the prior year of $1,212 million is attributable to lower effective market interest rates.

A breakdown of costs by base and additional CPP accounts is included in the CPP Investments Annual Report for fiscal 2021, which is available at www.cppinvestments.com.

Portfolio Performance by Asset Class

Fund returns by asset class are reported in the table below. A more detailed breakdown of performance by investment department is included in the CPP Investments Annual Report for fiscal 2021.

Diversified Asset Mix

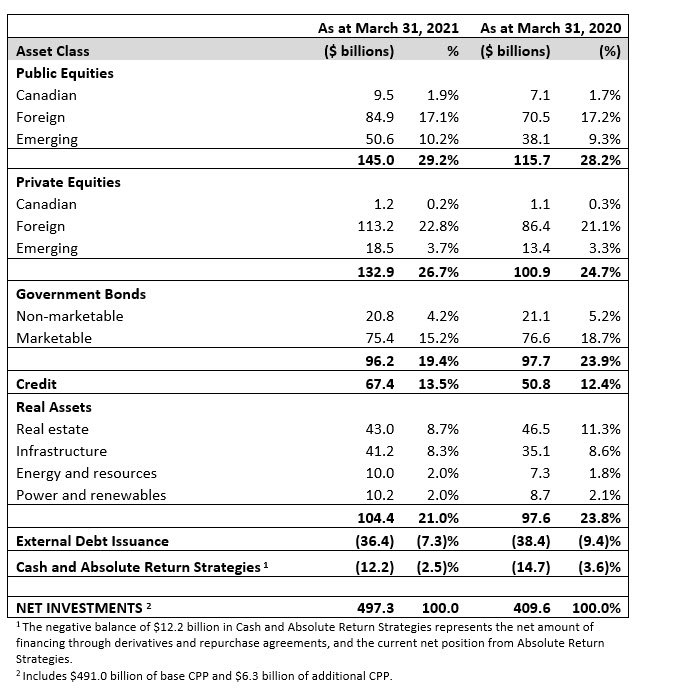

We continued to diversify the Fund by the return-risk characteristics of various assets and countries during fiscal 2021. Canadian assets represented 15.7% of the Fund, and totalled $78.3 billion. Assets outside of Canada represented a combined 84.3% of the Fund, and totalled $419.0 billion. The asset mix below is reported for the Fund.

Operational Highlights for the Year:

Executive announcements

- John Graham appointed as President & CEO in February 2021, succeeding Mark Machin. In this role, John is responsible for leading CPP Investments and its investment activities globally. John has been instrumental in shaping and executing CPP Investments’ strategy over the last decade. As a member of the Senior Management Team and throughout his career, he has had a highly successful track record of building and leading global investment businesses.

- Announced the following Senior Management Team appointments:

- Ed Cass as the first dedicated Chief Investment Officer and Head of Total Fund Management;

- Deborah Orida as Senior Managing Director & Global Head of Real Assets;

- Frank Ieraci as Senior Managing Director & Global Head of Active Equities; and

- Andrew Edgell as Senior Managing Director & Global Head of Credit Investments.

Board announcements

- The National Association of Corporate Directors (NACD) named the CPP Investments Board of Directors as a winner of the 2020 NACD NXT® award. NACD NXT showcases boards that are leveraging innovation and diversity to elevate company performance, and this is the first time the recognition has been awarded to a Canadian organization.

Corporate developments

- Thinking Ahead, an initiative to share CPP Investments insights, issued several reports in the year. For example: our 2021 Economic and Financial Outlook highlighted the continuing ripple effects of COVID-19 and considered possible long-term outcomes; Women, COVID-19 – and the threat to gender equity and diversity explored the potential for the pandemic to reverse the progress corporate Canada has made in diversity and inclusion, identifying seven steps companies and policy makers can take to protect the gains to date and assure future progress; and How COVID-19 is shaping the landscape for long-term investors, analyzed the breadth of change expected following the global pandemic and emerging opportunities.

- Hosted our public meetings, one for each of the nine provinces that participate in the CPP and one meeting for the three territories, to inform Canadians about the Fund’s financial performance and our investment strategy.

- Published an updated Policy on Sustainable Investing, reflecting our increased conviction in the importance of considering environmental, social and governance risks and opportunities amid an increasingly competitive corporate operating environment. The new Policy on Sustainable Investing specifically outlines CPP Investments’ support for companies aligning their reporting with the Sustainability Accounting Standards Board and the Task Force on Climate-Related Financial Disclosures.

Bond issuance

CPP Investments uses a conservative amount of short- and medium-term debt as one of several tools to manage our investment operations.

- In fiscal 2021, CPP Investments continued with its leadership role in the global transition to the new reference rates through its Sterling (GBP) issuance platform, with two benchmark issuances totalling £1.75 billion. In addition, CPP Investments issued its first SONIA-linked Floating Rate Note valued at £200 million, among other issuances. Debt issuance gives CPP Investments flexibility to fund investments that may not match our contribution cycle. Net proceeds from the issuances will be used by CPP Investments for general corporate purposes.

- With our continued commitment to sustainable investing, CPP Investments added a fourth currency for green bond issuance with an inaugural 20-year Australian-dollar green bond valued at A$150 million. The total issuance of green bonds since inception of the program is now C$5.5 billion. Green bonds enable CPP Investments to invest further in eligible assets such as renewables, water and green real estate projects, and to diversify the investor base.

Investment Highlights for the Year:

Active Equities

- Invested a total US$150 million in the Series B financing and as lead in the Series C financing for insitro, a biopharmaceuticals company that applies machine learning throughout the discovery and development process, and joined the Board of Directors upon closing.

- Invested US$150 million as a cornerstone investor in the IPO of Kuaishou Technology, a mobile short video sharing and live streaming platform in China.

- Invested C$1.2 billion in cornerstone financing to support Intact Financial Corporation (Intact) in its acquisition of the RSA Insurance Group plc. Canada and U.K. & International operations. Intact is the largest provider of property and casualty insurance in Canada.

- Closed a US$100 million investment in HUTCHMED through a private placement. HUTCHMED is an innovative biopharmaceutical company with a portfolio of nine cancer drug candidates currently in clinical studies or early stages of commercialization around the world.

- Invested an additional C$92 million in fiscal 2021 in Premium Brands Holdings Corporation, a Canadian specialty food manufacturing and differentiated food distribution business, through two private placements of common shares. Our ownership in the company is approximately 8.3%.

- Invested a combined €499 million in Sweden-listed Embracer Group, Europe’s largest developer and publisher in the global video game industry, for a 5.4% stake.

Credit Investments

- Established an investment vehicle with Angel Oak Capital to invest up to US$250 million in U.S. residential mortgage loan pools, with Angel Oak Capital managing the operations, asset management and financing.

- Committed up to US$125 million as a cornerstone investor to Baring Private Equity Asia’s India Credit Fund III, and up to US$125 million to a Credit Fund III overflow vehicle. The fund’s strategy is focused on Indian rupee-denominated secured lending to performing mid-market Indian companies.

- Invested US$175 million in the first lien term loan, senior secured notes and second lien term loans of LogMeIn, Inc., a provider of remote working, collaboration and customer engagement software-as-a-service.

- Committed to acquire US$1 billion of home improvement focused consumer loans from Service Finance Company, LLC, a sales finance business owned by ECN Capital Corp. Under the agreement, the purchases will be made through 2020 and 2021.

Private Equity

- Invested US$300 million in equity to acquire a 24.99% stake in Virtusa Corporation (Virtusa), alongside Baring Private Equity Asia. Virtusa is a global provider of a full spectrum of IT services.

- Increased our investment in Visma, a leading provider of business-critical software to enterprises in the Nordic, Benelux and Baltic regions in Europe, to an approximate 6% stake.

- Committed to invest approximately US$160 million in CITIC aiBank, an internet-based consumer finance bank in China, representing an approximate 8.3% equity stake in the company.

- Committed US$30 million to Y Combinator ES20 and YCC20, a pair of venture capital funds backing the global accelerator known for its early seed investments in technology companies such as Stripe, Dropbox, Doordash and Coinbase, among others.

- Committed US$750 million to Silver Lake Partners VI, targeting large scale, growth-oriented investments in the technology, media and telecommunications and technology-enabled sectors.

Real Assets

- Entered into a joint venture with Tricon Residential Inc. to invest in build-to-core multi-family rental projects in the Greater Toronto Area, with a C$350 million equity allocation for 70% ownership.

- Established a new joint venture to invest US$200 million to acquire and develop a portfolio of institutional-grade facilities in Indonesia with logistics real estate specialist LOGOS.

- Invested approximately US$624 million for a 15% interest in Transurban Chesapeake, a toll-road business comprising the 495, 95 and 395 Express Lanes located in the Greater Washington Area in the U.S., alongside other investors collectively acquiring a 50% interest.

- Established a new, U.K.-based platform, Renewable Power Capital (RPC) to invest in solar, onshore wind and battery storage, among other onshore renewable technologies, across Europe. The business is a majority-owned, but independently operated portfolio company. RPC announced its first investment in January 2021, for which we committed €245 million to support RPC’s acquisition of a portfolio of onshore wind projects in Finland. Subsequently, the company announced a joint venture in Spain to develop a portfolio of 3.4 GW of solar energy projects.

- Allocated an additional £300 million of equity to investment vehicles in the U.K. targeting the logistics sector, alongside Goodman Group and APG Asset Management N.V. The expansion follows the success of the Goodman UK Partnership established in 2015.

- Extended our partnership with GLP through the launch of the GLP Japan Income Fund (GLP JIF), the largest private open-ended logistics fund in Japan. The partnership with GLP was first established in 2011, and at the end of August 2020, CPP Investments successfully exited the investment in GLP JDV I, receiving approximately JPY 48 billion (C$590 million) of net proceeds. Following the disposition, CPP Investments recommitted JPY 25 billion (C$307 million) of the proceeds into the newly established GLP JIF. In December 2020, an additional JPY 8.2 billion (C$105 million) was committed to the fund in conjunction with further asset dispositions from GLP JDV II into GLP JIF.

Disposition Highlights for the Year:

- Agreed to sell our 45% interest in GlobalLogic Worldwide Holdings, Inc. (GlobalLogic), a leader in design-led digital engineering services that develops next-generation software platforms for enterprises worldwide, to Hitachi, Ltd. for an enterprise value of US$9.5 billion. Net proceeds from this transaction are expected to be approximately US$3.8 billion. Our ownership stake was initially acquired in 2017.

- Sold our 80% interest in a Distribution Centre in Lytton, Queensland, Australia, held through the Goodman Australia Development Partnership. Net proceeds from the sale are expected to be approximately A$138 million. Our interest was progressively funded between 2011-2012.

- Sold our 7.5% stake in Citycon, or half of our position, in the Nordic owner, manager and developer of mixed-use centres. Net proceeds from the sale were approximately C$147 million. Our ownership interest was initially acquired in 2014.

- Sold our ownership interest in Zoox, a U.S. technology company focused on developing a fully integrated autonomous vehicle mobility solution, as part of Amazon.com, Inc.’s acquisition of the company. Our ownership interest was initially acquired in 2018.

- Exited our 18% ownership stake in Advanced Disposal Services Inc., a solid waste services company in the U.S., through its acquisition by Waste Management Inc. Net proceeds from the sale were US$502 million. Our ownership stake was originally acquired in 2016.

- Sold our 50% interest in Nova, an office-led, mixed-use development in London Victoria, U.K. Net proceeds from the sale, which was completed through two separate transactions, were approximately C$725 million. Our ownership interest was initially acquired in 2012.

- Sold our 45% stakes in AMLI 900, AMLI Lofts, AMLI Campion Trail, and AMLI Arts Center, multifamily properties in the U.S. Combined net proceeds from the sales were approximately US$223 million. Our ownership interests were initially acquired in 2012 and 2013.

Transaction Highlights Following the Quarter:

- Acquired an additional 15.9% of the total units in IndInfravit Trust (IndInfravit) through two separate transactions for a combined investment amount of C$173 million, increasing our stake to 43.8%. IndInfravit is an infrastructure investment trust sponsored by L&T Infrastructure Development Projects Limited, which acquires and maintains stable brownfield road concessions in India and holds a portfolio of 13 operational assets.

- Committed €185 million to the new Commercial Real Estate Debt Opportunities partnership with Acofi Gestion. The partnership’s strategy is to invest in middle market real estate credit opportunities across France.

- Committed to an investment of up to R$1.7 billion (C$385 million) in Brazilian water and wastewater company Iguá Saneamento S.A., in which we hold a 46.7% aggregate equity stake, to support the privatization of water and sewage services from CEDAE in greater Rio de Janeiro.

- Invested US$70 million in a super priority term loan of David’s Bridal, a U.S.-based bridal and special-occasion apparel retailer.

- Invested US$150 million in the National Stock Exchange of India, the leading equity and derivatives exchange in India.

- Entered into a joint venture with RMZ Corp to develop and hold commercial office space in Chennai and Hyderabad, India, with an INR 15,000,000,000 (US$210 million) equity allocation for an 50% ownership.

About CPP Investments

Canada Pension Plan Investment Board (CPP Investments™) is a professional investment management organization that manages the Fund in the best interest of the more than 20 million contributors and beneficiaries of the Canada Pension Plan. In order to build diversified portfolios of assets, investments are made around the world in public equities, private equities, real estate, infrastructure and fixed income. Headquartered in Toronto, with offices in Hong Kong, London, Luxembourg, Mumbai, New York City, San Francisco, São Paulo and Sydney, CPP Investments is governed and managed independently of the Canada Pension Plan and at arm’s length from governments. At March 31, 2021, the Fund totalled $497.2 billion. For more information, please visit www.cppinvestments.com or follow us on LinkedIn, Facebook or Twitter.

Alright, it's time to cover the results of Canada's largest and best pension fund, CPP Investments.

Let me begin by thanking Michel Leduc, Senior Managing Director & Global Head of Public Affairs and Communications, for emailing me last night to give me a heads-up and for sending me a lot of material this morning to review and share on my blog comment.

I give CPP Investments an A+ on communications and I'm not just stating this to flatter Michel or John Graham, you will understand why after reading my comment below.

In fact, I spoke to John Graham earlier today going over the results and we talked about the importance of communication (see section below toward end of my comment).

Let me begin by stating I read the Annual Report 2021 for their fiscal year 2021 (ends March 31, 2021).

The annual report is where you will get all the relevant and necessary information and I urge you all to read it carefully.

Admittedly, it's not a quick and easy read but it's very well written and explains in detail all the operations at this mammoth pension fund.

Because I have a lot to cover, I will skim through the more important parts of the report, bringing to your attention what caught my eye.

First, I read the Chairperson's Report on page 2 where Dr. Heather Munroe-Blum went over the performance, risk management and notes this on succession planning:

Succession planning is an ongoing activity, not an event. Key members of the Senior Management Team (SMT) are identified and prepared for potential appointment as chief executive. This ongoing process enabled the Board of Directors’ clarity and conviction in appointing a new President & CEO, John Graham, when Mark Machin stepped down at the end of February.

Since joining CPP Investments in 2008, John has established a successful track record as an innovator and builder of leading global investment businesses. A highly regarded member of the SMT, John has been instrumental in helping shape and execute our organization’s strategy. John’s commitment to the organization, to his colleagues and to CPP Investments’ unique mandate is unequalled. The Board of Directors unanimously agreed that he is ideally suited to lead the organization forward.

I thank Mark Machin for his leadership and very significant contributions to the growth and success of CPP Investments during his tenure as CEO. My fellow Directors and I wish Mark the best in his future endeavours.

In writing this, Dr. Munroe-Blum lays to rest any speculation that the appointment of John Graham after Mark Machin's abrupt departure was done in a hasty manner.

Importantly, and I can't emphasize this enough, an organization like CPP Investments which is in charge of the pensions of over 20 million Canadians can't afford not to have ongoing succession planning no matter who is in charge because the role of President and CEO is critically important.

The fact that John Graham was appointed so quickly shows you how the Board takes succession planning very seriously and to be frank, it's also a testament to the organization's incredible bench strength at the senior level. Having had conversations with John Graham and Ed Cass, the CIO, I can attest to this and I'm sure other senior managers are just as highly qualified.

Moving on to the President's message on page 4 of the annual report, John Graham's first annual update, he discusses how the past year was characterized by "extreme conditions" but CPP investments stuck to its diversified investment strategy to deliver solid returns.

I urge you to read John's full message but here I will focus on his discussion on performance:

The challenges of the last year tested the Fund like never before. This experience strengthened our belief that working together across our distinct investment departments and across markets to act as one Fund will continue to allow us to surface compelling opportunities to grow and safeguard the Fund.

The Fund performed well in fiscal 2021 and these results indicate that our strategy is on track. We saw the Fund grow to $497.2 billion, based on $83.9 billion in net income and $3.7billion in net contributions received. The half-trillion-dollar mark is a significant milestone for the Fund and underscores the strength of our active management strategy. When CPP Investments was first created in 1999, it was estimated that we would not reach this point until 2028. Now, here we are, about seven years and $175 billion ahead of schedule, with a global footprint and diversified investment programs that could scarcely have been imagined back then.

To hold our strategy of active investment management accountable, we report a dollar value-added (DVA) comparison of our investment returns, after all costs, to our aggregated Reference Portfolio, which represents a passive portfolio of public-market stocks and bonds that the Fund might otherwise hold had CPP Investments not pursued active management.

The Reference Portfolio for the base CPP is made up of 85% global equities and the Reference Portfolio for the additional CPP is made up of 50% global equities. These Reference Portfolios outperformed this year after global equity markets soared amid fiscal stimulus flooding the market in response to COVID-19. Our Investment Portfolios’ growth was less dramatic, but well above the range required to maintain the Fund’s sustainability over the long term. Both the Reference Portfolios and the Fund ultimately behaved as we would expect them to this year, as they did at the end of our last fiscal year when our private market investments cushioned against a dramatically different falling market backdrop. Our DVA compared with our aggregated Reference Portfolio this fiscal year was negative $35.3billion, or negative 10.0%, and our Reference Portfolios returns for the base CPP and additional CPP were 30.5% and 17.0%, respectively.

This year’s return should be viewed in the context of our generational investment horizon. Short-term pressures can have a striking influence on yearly results but may be barely visible when viewed over the course of a generation. In fiscal 2015, for example, we achieved an annual net return of 18.2%, which was then our highest ever (until this year’s results). Yet, just six years earlier, in fiscal 2009, we suffered our largest loss of 18.6% as the world entered the global financial crisis. This stark contrast of yearly results is an expected part of the process for long-term, diversified investors. As I have assured my friends and neighbours, we are built to withstand these annual fluctuations. We continue to far exceed returns projected to be needed to sustain the CPP over the long term. Our five-year and 10-year net returns of 11.0% and 10.8%, respectively, begin to demonstrate the wisdom of this strategic approach.

And on why CPP Investments remains highly diversified in a COVID-19 world, John adds this:

While risks abound in the world today, our strategy of diversifying across currencies, countries and asset classes enables us to manage those risks. We seek to ensure that the Fund is appropriately rewarded for risks we take, including geopolitical, climate change and reputation-related considerations, which is a unique approach that helps set us apart when analyzing investments and executing our strategy. For example, we rely on our regional expertise to deeply understand the risk characteristics of an intensifying capital and technology race between the Eastern and Western Hemispheres – an ability few investors can claim. (For more on our approach to Risk Management see page 97.)

John also highlights three notable achievements over the past year:

First, we believe that the most rewarding investment opportunities in the global economy over the coming decades will be found among businesses that truly understand the risks, opportunities and impacts of climate change. Our investment strategy ensures we identify such businesses. Our Climate Change Program is more deeply embedded into our investment processes and operations, including tools for assessing the economic damage associated with different Energy Transition and Climate Change (ETCC) paths as we select securities and design our portfolio. By acting as a long-term and engaged capital partner, we expect to see continued reduction of the Fund’s exposure to greenhouse gas emissions over time.

Second, we continued to enhance our approach to risk management. This year, we built on our Integrated Risk Framework with a new and extended policy that provides the safeguards needed to manage a crisis while protecting the financial stability and operations of the Fund. Our approach worked as intended during the pandemic by prioritizing employee health and safety, the ability to meet our obligations to the CPP and other counterparties, and adherence to Board-approved investment and non-investment risk tolerances. We were able to act decisively this year because we had risk management mechanisms in place before COVID-19, including a structure to quickly gather and assess information in a crisis.

Third, we started to realize an increase in innovation across the Fund through a focused effort to harness the power of our San Francisco office’s proximity to cutting-edge technology. We now regularly expose our global colleagues to the expertise and relationships we’ve built in the Valley. For example, we hosted a private discussion for select portfolio-company Chief Financial Officers and organized an investment pitch event focused on solving complex societal problems. We have reimagined how collaboration can happen by acting as a convener between our investment professionals, external investment managers and Bay Area thought leaders and entrepreneurs.

Having now spent over a decade at CPP Investments, I’m convinced our organization has unparalleled potential. We operate at a rare nexus in the financial world and possess knowledge and perspective that is only attainable by managing a multi-asset class, global and diverse portfolio. This powerful combination makes us the sought-after capital partner we are today.

We plan to use this standing to bring increased rigour to how we integrate various elements of our portfolio and use new tools. Three elements of particular interest include: building our talent strategy to attract the highest performing individuals from a multitude of disciplines who want to work for a purpose-driven organization; identifying and removing unconscious biases from investment decisions by bringing to bear all the talents and wisdom of a diverse workplace; and continuing to seek rewarding investment opportunities among businesses that understand the risks, opportunities and impacts of climate change.

On the last point, I continue to believe CPP Investments represents all Canadians and as such it has to reflect the society it works for.

I also believe that CPP Investments should hire the best, most diversified talent across the country no matter where they are located and accommodate that talent to work at this purpose-driven organization.

Yes, the head office will remain in Toronto but CPP Investments now manages half a trillion in assets and has offices all over the world, surely it can open a few more offices across Canada or just hire talent that is already working from home in a post-pandemic world (hint: the name of the talent retention game is flexibility).

In short, while Toronto is the mecca for North American pensions, it doesn't hold a monopoly on pension talent in this vast country of ours.

Please note, these are my views, not John Graham's or anyone else's at CPP Investments, but I have strong views on our national pension fund and how it can attract more talent across the country.

Keep in mind, by 2050, the CPP Fund (base + additional) is projected to reach $3 trillion ($1.6 trillion when value is adjusted for expected inflation):

That's a lot of money to manage and it's going to happen over the next 29 years.

I believe it's critically important that CPP Investments stays the course, meaning it continues with its active strategy, diversifying across public and private markets all over the world, leveraging off its external partners where needed and managing the rest in-house.

Of course, the key to CPP Investments' long-term success remains its independent governance, it needs to remain independent, managing assets at arm's length from the federal and provincial governments.

Now, getting back to the results, they were obviously excellent but like John Graham states in his message: "this year’s return should be viewed in the context of our generational investment horizon."

Looking at the annual performance for each of the ten past years, you see that fiscal 2021 was indeed a record year:

It was a great year, no doubt about it, but you really need to focus on long-term results when looking at pensions because one year -- good or bad -- doesn't make or break a pension with long dated liabilities.

And on that front, CPP Investments is delivering solid long-term results, delivering 10-year and five-year annualized net nominal returns of 10.8% and 11.0%, respectively.:

Importantly, CPP Investments is designed in a way to capture global growth while demonstrating resilience during periods of market uncertainty. The Fund invests in 56 countries and has 292 world-class investment partners to build value in their existing assets:

But it's also important to note that there are six investment departments at CPP Investments, managing assets across public and private markets, and all of them performed well last year:

Now, I did note this in the press release above in terms of the relative performance relative to the Reference Portfolio:

On a relative basis, the aggregated Reference Portfolios’ return of 30.4% exceeded the Fund’s net return of 20.4% by 10.0%. As a result, in fiscal 2021, net dollar value-added for the Fund was negative $35.3 billion.

The base CPP account earned a net return of 20.5%, which was less than its Reference Portfolio’s return of 30.5% by 10.0%. This equates to a single-year net dollar value-added of negative $35.2 billion, after deducting all costs. The additional CPP account earned a net return of 11.6%, which was below its Reference Portfolio’s return of 17.0% by 5.4%. This equates to a single-year net dollar value-added of negative $93.7 million, after deducting all costs.

I have two comments to make:

- On any given year, CPP Investments can outperform or underperform its Reference Portfolio (benchmark) for base CPP which is made up of 85% global equity and 15% Canadian government bonds. For the additional CPP, CPP Investments has adopted a Reference Portfolio of 50% global equity/50% nominal bonds issued by Canadian governments (see details here).The Reference Portfolio for additional CPP takes less risk because unlike base CPP, it's not partially but fully funded. The bulk of the assets remain in base CPP, for now.

- Still, as experienced last fiscal year, when stocks are on a tear and performance is coming mainly from a handful of tech giants, both base CPP and additional CPP can underperform their respective Reference Portfolio.

Why are these points important? Because in order to really understand CPP Investments active management, you need to look at the cumulative performance over the Reference Portfolio since inception of the active management:

The first chart shows the excess return over the required minimum return for the plan's sustainability since implementing the active management back in fiscal 2006 (see details here).

The second chart shows the cumulative 10-year return of the CPP Fund relative to its Reference Portfolio, showing it added 60 basis points (10.8% vs 10.2%) or more importantly, $27.8 billion 10-year dollar value added.

That's $27.8 billion value added that wouldn't have existed if CPP Investments only invested passively in its Reference Portfolios.

What this tells you is CPP Investments' strategy works but in order to fully appreciate it, you need to stop looking at relative performance on any given year and look at it over a longer time horizon.

It's also worth noting that CPP Fund's framework changed in F2015 from 100% relative return to 50% relative/ 50% absolute return:

All this to say, it's not just about beating a benchmark, it's about delivering solid risk-adjusted returns over the long run to make sure the CPP remains sustainable over the long run no matter what economic conditions prevail.

So, yes, on any given year, CPP Investments can underperform its Reference Portfolio (see the Globe and Mail article which misses the point) which is made up mostly of global equities (85%) but it will not experience the volatility of this benchmark because it's highly diversified across public and private markets:

Now, CPP Investments did send me a chart on how its Reference Portfolio is the most competitive in the industry:

However, I took issue with this slide because base CPP is partially funded and its Reference Portfolio is heavily tilted towards equities, so in a raging bull market like we experienced over the past year, it will be the toughest benchmark to beat, but you're not comparing apples to apples.

John Graham actually agreed with me here and stated each pension has "its own objective function" to beat and it's not really fair comparing benchmarks for one fund to the other.

Discussion with John Graham

Alright, let me get to my discussion with John Graham, CPP Investments' President and CEO.

John began by telling me to go back a year, to April 2020, there was a lot of uncertainty and major dislocations in all markets.

He told their priority was on Fund liquidity and was very pleased on how everyone at CPP Investments performed operationally, not just the investment group, but "tax, legal, finance, HR, everyone pulled through."

Basically, the two top priorities were:

- Operational excellence throughout the organization

- Building out the organization by focusing on breadth in capital management, seizing on the right opportunities

By breadth, he means geographic and sector diversification and really looking at each deal bottom-up, company by company, deal by deal, and that includes leveraging off their global offices and the people working there.

John is a huge believer in diversification and he told me last year was odd in the sense that most of the gains in global markets came from a handful of stocks, tech giants (like Alphabet, Facebook, Amazon) and Tesla.

This "crowding effect" is another reason why CPP Investments can underperform its Reference Portfolio on any given year, especially when positioning is so extreme in a handful of tech names.

John told me markets have rallied back to their highs and now more than even, they need to be cognizant of risk-adjusted returns, making sure they get compensated for the risks they take.

We spoke about credit, the department he used to run, and he told me that Credit delivered 18.8% local currency in F2021, 6.8% in CAD.

He said it's his roots in credit which leads him to believe so much in diversification because it's a "heterogeneous asset class" where you need to diversify by geography and strategy (corporate, structured, direct lending, etc.).

He told me CPP Investments has built out a solid credit platform, doing a lot internally, using some funds for emerging markets, and still relying on Antares for its mid market direct lending in the US market.

Interestingly, he told me most of the best relative value they are seeing in credit is in the structured credit space where they are still active across the market.

He noted, however, while Credit Investments performed well, the CPP Investment returns were driven by strong results from across the entire organization, "it was really a team effort" (indeed, read performance by investment department starting on page 66 of the annual report).

On Real Estate, he told me Retail remains challenging and the pandemic accelerated trends that were already in place before, benefiting logistics properties which CPP Investments identified early on as a growth area.

He said in the Office space they're seeing "a flight to quality" where tier 1 buildings remain in high demand, tenants continue to pay their rent, but he admitted there is a lot of uncertainty as employers grapple with working from home versus working from office.

Interestingly, he said Multifamily has now become more popular than Office and that they see increased activity there, in logistics and data centers.

Still, he noted "there's a lot of dispersion in real estate."

On transportation infrastructure, I asked him about Highway 407 which remains CPP Investments most important asset.

John told me that the pandemic and lockdowns hit toll revenues but it remains a very valuable asset and given its long dated concession, "it's a very sought after asset".

Given where rates are, I believe him, this remains a jewel of an asset for CPP Investments.

Lastly, we talked about the importance of communication, both internal and external.

Internally, he told me he's holding more town hall meetings, one on ones with all employees, and even meetings with senior managers "where there's no agenda", just free flowing thoughts and discussions.

Externally, he told me he views CPP Investments 20 million+ contributors and beneficiaries as "clients" and that's why regional public meetings are important but above and beyond those, John wants to make sure the Fund treats all Canadians with respect and that they understand the strategy and "given the choice, they will always opt to stay invested with us."

He credits his wife for the focus on communications and praised Michel Leduc and his team as well.

I told him that he's the only Canadian pension CEO who took the time during the pandemic to do a video going over the results and that speaks volumes (never take your contributors and beneficiaries for granted even if they're captive clients).

Alright, I am going to end it there, I want to thank John Graham for taking the time to call me earlier, always enjoy our conversations.

Please take the time to read the Annual Report 2021 to go over their fiscal year 2021 in detail.

Also, as I customarily do when covering annual results, I end with a summary compensation table for senior managers:

As always, compensation is based primarily on long-terms results, and CPP Investments has delivered outstanding long-term results. Take the time to read compensation details beginning on page 119 of the annual report.

Below, CPP Investments' President and CEO, John Graham, goes over fiscal 2021 results, with input from others working at the Fund.

John also spoke to BNN Bloomberg earlier to break down the record results (watch here if it doesn't load below). Take the time to listen to him, he provides great insights here.

Comments

Post a Comment