Hawkish Fed Triggers Massive Short Squeeze?

Stocks climbed on Friday as the major averages notched their best week in more than a year.

The Dow Jones Industrial Average rose 274.17 points, or 0.8%, for the fifth day in a row to 34,754.93. The S&P 500 gained 1.1% to reach 4,463.12, and the Nasdaq Composite added 2.05%, ending at 13,893.84. Both indexes surged for a fourth consecutive day. All of the major averages finished their best week since November 2020.

Stocks are coming off a massive surge that resulted in the S&P 500 notching a 6.1% gain for the week. The Dow ended the week 5.5% higher, and the tech-heavy Nasdaq Composite advanced 8.1%.

Investors continued to digest news from the Federal Reserve earlier this week, as well as a rise in Covid cases in Europe stemming from an emerging subvariant and the ongoing war between Russia and Ukraine.

“The worst thing about any crisis is when it first hits out of left field, it creates nothing but uncertainty. You have no idea what it means or where it’s going to go, and you react violently as an investor to get out of the way,” Jim Paulsen, chief investment strategist for The Leuthold Group, told CNBC’s “Closing Bell.” “But after you’ve had some time to vet it [you see] the market is suggesting that they’re starting to feel a little better, that there’s some direction of this thing... It does seem like the economic fallout will not be nearly as detrimental as it looked going in.”

President Joe Biden spoke with Chinese President Xi Jinping on Friday to discuss Russia’s invasion of Ukraine. Xi told Biden that the United States and China each had an obligation to promote peace. Russia has made requests for military or economic aid from China and the call was seen as a critical test of whether Biden can convince Beijing to stay on the sidelines of the conflict.

Several missiles hit an aircraft repair center on the outskirts Lviv in western Ukraine. A Ukrainian official also said one person was killed in an airstrike that hit Kyiv. (Click here for live updates.)

Russia on Thursday reportedly made a $117 million bond payment in dollars, thereby avoiding what would be a historic foreign currency debt default. Stocks extended their gains following the report. Bloomberg reported Friday that clearing houses in Europe and the U.S. have processed the payment.

Investors were also assessing their own risk appetite. The week’s big gains came with a side of volatility, which shows no signs of tempering anytime soon.

“For 2022, volatility is going to be the investor narrative,” Greg Bassuk, CEO of AXS Investments, told CNBC. “We would normally feel much more bullish around any single factor having a good ability to level the volatility, but given this unprecedented level of very significant factors that could drive the markets one way or another, we don’t see volatility normalizing over the next couple of months.”

On Friday tech stocks led the market higher. Salesforce and Apple were among the top gainers in the Dow, rising 3.9% and 2%, respectively. Nvidia climbed 6.8%. Meta Platforms gained 4.1%, and software stocks Paycom and Fortinet advanced 4.6% and 5.4%.

Shares of Moderna rose 6.3% as the company seeks FDA approval for a second Covid-19 booster shot for adults 18 years or older.

Boeing gained 1.3% after Reuters reported the company is in talks with Delta Air Lines for a landmark order of 737 MAX 10 jets.

Traders are also still digesting the latest Federal Reserve update from earlier this week. The central bank signaled it expects to raise rates at its remaining six meetings this year. The Fed also raised rates for the first time since 2018 on Wednesday.

On Friday, Fed Governor Christopher Waller told CNBC’s “Squawk Box” the central bank may need to enact at least one more interest rate hike this year of 50 basis points or more in order to tame “raging” inflation.

“Fortunately, investor expectations for inflation over the next five years was brought down quite a bit, which, if sustained, will continue [to] be helpful for the Fed and the markets despite somewhat higher interest rates,” said John Vail, chief global strategist at Nikko Asset Management.

Patti Domm of CNBC also reports investors come off a strong week looking for more gains now that they have some clarity from the Fed:

With the Federal Reserve’s first rate hike out of the way, market pros are now debating whether the market can continue the upswing it started in the past week.

A powerful rally in technology and growth stocks helped drive the stock market higher in its best week of the year. The S&P 500 was up about 6.2% for the week, ending at 4,463. The Nasdaq was up 8.2%, and the Dow gained 5.5%.

Consumer discretionary stocks gained more than 9% as the top performing sector, followed by technology, up about 7.8%. Energy was the only major sector to decline, falling 3.6%.

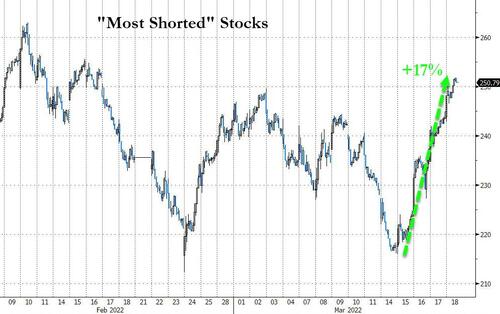

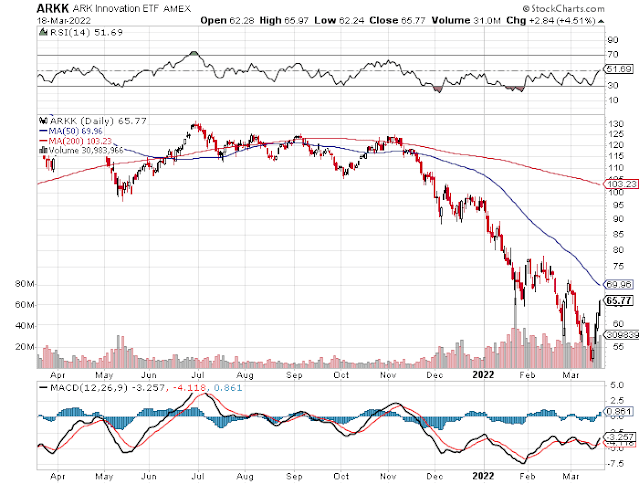

Some of the names that had been most punished like airlines, were among the biggest winners on the week. Airlines were up about 14.7% for the week. High growth names also bounced, with the ARK Innovation Fund, a poster child for growth, jumping about 17.4%. The fund is still down more than 46% over the last six months.

Ukraine will continue to be a focus, and headlines could continue to create volatility in the coming week. Investors are also watching the course of Covid, which is causing shutdowns of Chinese cities and is spreading again at a higher rate in Europe.

There are more than a dozen Fed speeches, including from Fed Chairman Jerome Powell who appears at an economics conference Monday and at an international banking conference Wednesday. The economic calendar is relatively light, with durable goods and both services and manufacturing PMI released Thursday.

“The anticipation of the first rate hike did more damage than the rate hike itself. We got ourselves twisted in a knot, starting in December, with the Fed pivot from transitory inflation to tapering” [bond purchases], said Art Hogan, chief market strategist at National Securities. “That’s kind of behind us now as a headwind. That diminishes the impact that any parade of Fed speakers will deliver.”

The market indeed ignored hawkish comments Friday from St. Louis Fed President James Bullard and Fed Governor Christopher Waller, who appeared on CNBC. Both said they want to raise rates faster than the median seven hikes the Fed expects this year.

The Fed released its interest rate forecast Wednesday, when it raised its fed funds target rate range by a quarter point to 0.25% to 0.50%, its first rate hike since 2018. The Fed also said it would look to start reducing its nearly $9 trillion balance sheet at an upcoming meeting.

Tech and growth did well in the past week, and they are the stock groups most hurt by higher interest rates. They typically command higher prices because investors buy them for their future earnings, and easy money makes them very attractive.

Strategists say tech can continue to gain in a rising rate environment, now that some of the excesses are wrung out of the group. But they may not be the leaders they once were.

Looking past the Fed

“I think the stage has been set by the Fed for investors to focus on earnings again,” said Julian Emanuel, head of equities, derivatives and quantitative strategy at Evercore ISI. “Bottom line...earnings estimates since the beginning of the year have risen.”

Emanuel said he expects the market could continue to rise in the near term, barring an escalation of geopolitical events. While it appears oil prices may have peaked, he said it is still not clear whether stocks put in the low for the year.

“Sentiment is absolutely horrendous...You put it all together, and we just think it’s a recipe for higher share prices looking out over the next month or two,” Emanuel said. He said investors are now able to discount the fact the Fed has begun its rate hiking cycle.

“We’re there. We know what’s going to happen. We know they’re going to do 0.25% in May. We know they’re going to start QT [quantitative tightening] some time at mid-year,” he said. “They’re not raising rates enough that it’s really going to hurt the market and investors can focus on earnings again.” He expects S&P 500 profits to be up 9.3% this year.

Hogan said the market is leaning towards a favorable outcome for Ukraine, such as a cease fire, although no developments suggest an end is now in sight.

“Everyone is leaning in this direction that this will come to an end in weeks rather than months,” he said. “If not, the market is going to have to recalibrate that.”

This is what the stock charts say

Scott Redler, partner with T3Live.com, focuses on the short-term technicals of the market, and he said after a strong run, the market could digest some of its gains early in the week.

“After an impressive week like this, most active traders are reducing risk into this [S&P 500] 4,400 level, not adding to it,” said Redler. “If we could digest a day or two after quadruple witching that might give us some signals that this could continue towards 4,600.” The quadruple expiration of options and futures was Friday.

Redler said Russia’s war in Ukraine and Fed policy tightening will continue to hang over the market, and that might keep the S&P 500 in a range. “I don’t think anyone is thinking the market goes right back to all-time highs anytime soon,” he said. “I think we’re smack in the middle of a range. This is a very neutral spot not to get short and not to add to longs. We’ll see how we digest this next week. For me, I think oil put the high in for the year, and that could be helpful.”

Oil briefly popped to $130.50 per barrel earlier this month, when investors feared sanctions on Russia would restrict its oil exports and create major shortages. Since then oil has fallen back, and West Texas Intermediate crude futures were trading just under $105 per barrel Friday.

Redler said an important test for the S&P 500 will be to see if it can hold the top third of its range and stay above 4,330. “It if can hold that, the next move could be higher,” he said. “That would show commitment to this week’s actions.”

Technology shares made a strong comeback, and Redler said he is watching to see if they continue to lead. “Tesla helped lead the way all week. A bunch of tech names did break their downtrends,” he said. “Tesla, NVIDIA and Amazon have been buyable on dips...NVIDIA gave clues that the bounce was as believable as it because it was one of the first stocks to cross its downtrend line.”

Apple and Microsoft, both higher on the week, could be important drivers of the market in the coming week.

“Apple and Microsoft haven’t been a headwind but they weren’t a tailwind. If they could outperform a little bit, they could help the broader indices,” Redler said. He said the two stocks, the biggest by market cap, were higher on the week, but they lagged the Nasdaq’s gains because they had they had large sell imbalances during the quadruple witching expiration.

“The stocks with the biggest buybacks have the biggest selling imbalances,” Redler said.

It was a big week in the stock market with monster moves all around led by technology shares.

Last week, I talked about how it feels gloomy like the 1970s and said:

Will the Fed say something dovish next week? I doubt it, it will however increase rates by only 25 basis points and will move gradually.

Fed Chairman Powell doesn't care if stocks sell off but he is petrified of a credit event seizing credit markets.

A lot of this is already priced in the market, so don't be surprised if stocks have a relief rally next week once the Fed announces.

Well, we got a relief rally this week which Martin Roberge of Canaccord Genuity attributes to these factors:

The catalysts for the rally include: 1) a sharp drop in oil prices, 2) China signaling supports to their economy, real estate sector and financial markets, and 3) Fed Chair Powell removing much uncertainty on forward rate hikes by telegraphing a rate increase at each of the next six meetings. By doing this, the Fed also removes any ambiguity/bias when comes the mid-term elections in November. If there is one caveat behind this week’s rally is that small caps have lagged. The opposite is usually required to confirm a positive shift in risk appetite. Otherwise, US 10-year bond yields jumped to the top of our projected 2.0-2.25% range for 2022 but have since backed down. With our economic reflation indicator pointing to a sharp downturn in April, our hunch is that we may have seen the peak in Treasury yields for the year.

If indeed we have seen the peak in bond yields, then you'd expect technology stocks to rip higher, which they did, and a lot of stocks that were heavily shorted to rip higher:

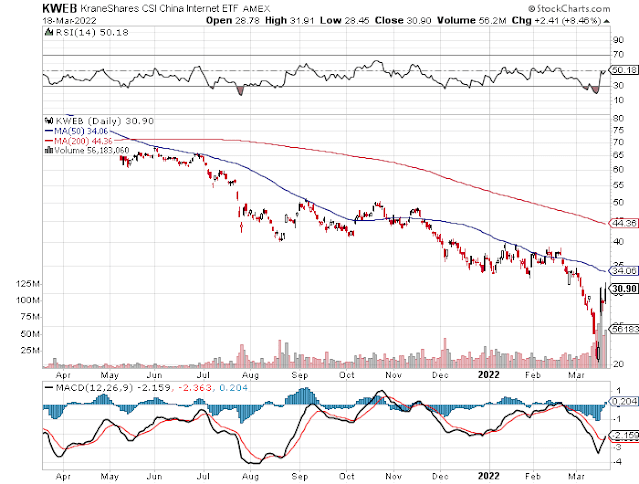

Not surprisingly, the biggest moves up this week came in the Ark Innovation ETF (ARKK) and the Chinese Internet ETF (KWEB):

A lot of this is just good old fashion short covering, shorts got squeezed hard this week and it was a perfect week to squeeze them.

Stock Traders Endure a $3.5 Trillion Triple Witching Event https://t.co/YC23TvwPll via @Yahoo

— Leo Kolivakis (@PensionPulse) March 18, 2022

But have a look at the 5-year weekly chart of the Nasdaq, it still remains very weak even after this week's monster rally:

If inflation pressures persist and rates keep going higher, the downtrend will reassert itself.

And long bond prices keep dropping as yields climb and traders don't buy the Fed is on top of inflation:

Another sign that bond traders don't believe that the Fed will go through with aggressive rate hikes: inflation expectations over the next five years have risen to new post-2002 highs, despite a more aggressive stance from Powell this week. Here are 5-year breakeven rates: pic.twitter.com/SOm9IEaWp4

— Lisa Abramowicz (@lisaabramowicz1) March 18, 2022

Meanwhile, the US economy keeps slowing:

ECRI's U.S. Weekly Leading Index growth rate falls to a fresh 82-week low. pic.twitter.com/WGPPzYzmSM

— Lakshman Achuthan (@businesscycle) March 18, 2022

And you have some Fed presidents calling for 50 basis points rate hikes to squelch "raging inflation":

Fed Governor Waller says half-point rate hikes could be needed as 'inflation is raging' https://t.co/e8QP8FdUqF

— Leo Kolivakis (@PensionPulse) March 18, 2022

The Fed Isn’t Doing Enough to Fight Inflation, Fed President Says. Why It May Not Matter Anyway. https://t.co/cBwczYUTHp via @BarronsOnline

— Leo Kolivakis (@PensionPulse) March 18, 2022

Of course, the Fed Chairman has the final say but even he seems more hawkish:

Fed's Powell sees the light --- and turns far more hawkish than expected https://t.co/KCR4Npc2Qr

— Leo Kolivakis (@PensionPulse) March 18, 2022

What does all this tell me? We are in for a lot more volatility and it's way too early to conclude anything on stocks.

The bears got dinged this week, no doubt about it, but there still lurking and they'll be back.

As a follow-up to the last chart I posted, this is the close-up version.

— Mac10 (@SuburbanDrone) March 19, 2022

The Nasdaq is now two years overbought and has the same formation that preceded the January crash:#CheapTequilaOnLinoleum pic.twitter.com/2roPEUZBwr

Below, Jon Najarian, MarketRebellion.com co-founder joins 'Halftime Report' to discuss the outlook on ARKK ETF.

Second, Paul Hickey, co-founder of Bespoke Investment Group, joins 'The Exchange' to discuss the state of the markets and the tech sector.

Third, Greg Branch, Veritas Financial Group managing partner, joins 'Power Lunch' to discuss where further downside risk exists, and why he likes some of the big-tech blue chip companies and cyber security companies.

Lastly, Federal Reserve Chairman Jerome Powell holds a news conference following a closed two-day meeting of the Federal Open Market Committee and their latest interest rate decision.

Comments

Post a Comment