John Gittelsohn of Bloomberg reports that US office buildings are facing a $1.1 trillion obsolescence hurdle:

One of the tallest office towers in St. Louis lost 96% of its appraised

value. Denver’s former World Trade Center complex faces foreclosure. An

oil company’s vacant Houston workplace sold this year at a $67.4 million

loss to lenders.

Those properties are among the 30% of U.S. office buildings -- worth

an estimated $1.1 trillion -- that are at high risk of becoming obsolete

as tenants’ tastes change in the hybrid-work era, according to Randall

Zisler, an independent consultant and former head of real estate

research at Goldman Sachs Group Inc.

Some

companies are scaling back their space. Others are gravitating to newly

developed or recently overhauled offices that are environmentally

friendly, with plenty of fresh air and natural light, fitness rooms and

food courts. Left behind are older buildings that would be expensive to

renovate to today’s standards.As values for those properties slide,

some landlords are walking away.

“We’re not saying bulldozers are

arriving en masse,” Zisler said. “But you’re going to see a repricing

and, in some cases, reuse of these buildings.”

Average U.S. office

values remain 4% below their pre-pandemic levels, the worst performance

of any type of commercial real estate, Green Street data through

February show. A deeper look shows a divided market: While prices for

newer, amenity-filled offices have gained about 15%, they’re down 20%

for smaller, older properties, Zisler said.

In addition to $1.1 trillion of endangered buildings, another $1.1

trillion make up a “mediocre middle” with limited upside because of

uncertainty about long-term demand and potential renovation costs,

Zisler estimated. Top-tier buildings, worth about $3.2 trillion, are

likely to gain value as tenants move up in quality.

Buildings that

opened since 2015 recorded more than 51 million square feet (4.7

million square meters) of occupancy gains since Covid hit, while

vacancies swelled elsewhere, according to Jones Lang LaSalle Inc. The

divide is most pronounced in big-city markets where more than 70% of

office stock is at least three decades old, such as New York, San

Francisco, Los Angeles, Boston, Chicago and Philadelphia, the brokerage

reported.

Workers

have been slow to return to offices two years after pandemic lockdowns

sent them home. With many people vowing never to go back to their old

commutes, companies are reconsidering their real estate needs, with some

downsizing or listing space for sublease. Demand for in-person space

may fall 15% from pre-Covid levels over the next five years as remote or

hybrid schedules become more common, according to Green Street.

To

entice balky workers back to their desks, employers are looking for

spiffed-up offices with some of the perks of home. Many top-paying

tenants, such as tech companies, only want buildings with low carbon

footprints, while regulations such as New York’s Local Law 97 may

require heavy investment to meet energy goals.

Giving Up

Renovations

don’t guarantee success for buildings in weak locations. Empire State

Realty Trust Inc. added a gym and dining facility in 2019 to a Norwalk,

Connecticut, building that was only 46% occupied as of December. The

company stopped paying a $30 million mortgage rather than spend more

money to lease up space, Chief Financial Officer Christina Chiu said on a

conference call last month.

“The math favored handing the keys

back to the lender,” said Danny Ismail, a senior analyst at Green

Street. “Increasingly, that’s a risk going forward.”

Some lenders

are giving up. MUFG Union Bank is selling a $190.8 million mortgage on a

Chicago complex with its biggest tenant, BMO Harris Bank, moving to a

new riverfront tower this year. The debt matures March 31, positioning

the note buyer to assume ownership on an “attractive basis relative to

new construction,” according to a marketing memo from JLL.

A MUFG

Union Bank spokesperson declined to comment. Downtown Chicago’s office

vacancy rate hovered around 18.5% at the end of 2021, JLL data show.

‘Alarm Bells’

The

mortgage delinquency rate for offices remains far lower than for hotels

and retail properties because of long-term leases and contract

obligations to pay even if tenants aren’t using the space. In a sign of

growing caution, some new mortgages include “cash trap” clauses

diverting tenant rent payments straight to lenders rather than landlords

when offices stay dark for lengthy periods, said Elizabeth Murphy, a

real estate finance attorney with Alston & Bird LLP.

“That sets off alarm bells,” Murphy said in an interview from Charlotte, North Carolina.

Values

plunge after delinquencies. Reappraisals in the past two years of 60

office buildings with distressed commercial mortgage-backed securities

fell by an average 67%, erasing more than $1.2 billion in collateral,

according to data compiled by Bloomberg.

Biggest Losers

The

biggest wipeout of that group was 909 Chestnut in St. Louis, which was

appraised in August at $9.2 million, down from $207.3 million in 2014.

Built in 1986 as the world headquarters for Southwestern Bell Corp., the

building’s 1.2 million square feet are available for lease, according

to a broker presentation.

The property is under contract and the

sale is expected to close this year, loan documents show. The broker,

Tony Kennedy at Colliers, declined to comment.

Houston’s vacancy

rate reached 28% in December, JLL reported, aggravated by years of the

U.S. oil industry’s contraction. Three Westlake Park, an empty former BP

Plc and ConocoPhillips office, sold in January for about $21 million,

resulting in a $67.4 million loss for lenders, according to Kroll Bond

Rating Agency LLC. The new owners plan to convert the offices to

apartments.

In Denver, where downtown offices are 24% vacant, one

loser is the former World Trade Center I & II towers, built in 1979

and appraised at $176 million in 2013. The owners failed to find a buyer

who would cover the $132 million mortgage and agreed to surrender the

property, now called Denver Energy Center. A foreclosure is expected

this month, according to loan data compiled by Bloomberg. A spokeswoman

for the owner, Los Angeles-based Gemini Rosemont, didn’t reply to

requests for comment.

More losses loom for landlords across the country.

“We’re

going to see a substantial decline in prices in buildings that are

obsolete,” Zisler said. “You’ll see it over the next four years, maybe

even sooner.”

This is an important article worth examining further.

Real estate is an important asset class for all pensions so you really need to understand what is going on in these portfolios as they typically make up 12-15% of total assets.

Admittedly, offices are an important sub-sector of a real estate portfolio. Some pensions have more exposure, some less, but we know what happened to offices and retail assets during the pandemic, they got hit hard because of legislative closures.

Things are slowly coming back but important questions remain and experts I talk to see a hybrid future where workers are not called into the office every day of the week.

This article, however, discusses another major risk offices and maybe even other sectors of real estate face, the risk of becoming obsolete.

"Real estate (and other private assets) is where the revolution lies,

this is where disruption will take place. For me, it's not going to be

like this building will be discounted a little bit, at one point, it

will be zero or one. Liquidity is the main risk in our industry,

when you can't find a buyer, there's no value. At a point electricity

came into buildings, now you can’t buy a building without electricity.

At a point ESG standards will be the same, nobody is going to buy a

building where you cannot guarantee the quality of the air, especially

after the pandemic,all these factors will be the new normal."

This is the head of an organization managing C$60,4 billion in global real estate assets telling you they take the risks of obsolescence very seriously.

And they should. As Nathalie told me, "consumers are demanding change, businesses are demanding change, if you're not proactive, you'll be left behind."

Yesterday, I had a conversation with HOOPP's CEO Jeff Wendling going over their 2021 results, and he told me they're committed to achieving net zero by 2050 and their real estate team has been a leader in sustainable investing:

"If you look at our three biggest holdings in office real estate, the

building we are in right now, it was the most efficient LEED certified

building in Canada when it was built. We have another great building

down the street and another energy efficient building in London. We have

good product and environmentally high quality product as well."

Every large Canadian pension with billions invested in real estate is thinking the same way, buying high-quality assets that appeal to potential tenants, especially large corporations looking to reduce their carbon footprint.

As you can read above, buildings that are not meeting these standards tenants demand quickly become obsolete and their appraisal values decline dramatically.

In some cases lenders are walking away, creating opportunities for vulture funds to swoop in and buy these assets at deep discounts.

But renovating old office buildings is expensive and repositioning them to convert to multifamily could be even more expensive depending on permits and a whole host of other factors.

Notice the article talks about office buildings but what about the multifamily sector?

There too, there is growing demand for LEED certified properties:

The multifamily sector has experienced significant growth

in the past year, as constant demand for space pushed new supply. The

health crisis reinforced the need for clean air within both apartments

and communal areas within multifamily properties, while the prevalence

of remote work made residents more mindful of their energy consumption.

Sustainable multifamily communities are treated more and more as a

requirement rather than an exception.

Earlier this week, I spoke with OTPP's CEO and CIO, Jo Taylor and Ziad Hindo, going over their 2021 results, and they told me they're looking to reposition some of their retail assets to transform them into mixed-use.

This is a smart strategy and they're not the only ones doing this as demand for housing soars in Canada and the US.

The one big advantage of developing new properties is you can work with developers to adopt the highest energy efficiency standards.

But the most important thing I want my readers to get from this post is there are significant risks in real estate portfolios and they're not just related to the pandemic and working from home.

Another bigger issue is whether your assets are up to snuff when it comes to energy efficiency standards consumers, businesses and governments are increasingly demanding and if not, this represents a material risk when appraisers cut the valuations by half or more.

One last thing that crossed my mind.

On Wednesday, I discussed CPP Investments' comment from its CEO, John Graham, on why massive disruption requires collective efforts.

He states: "Decarbonizing essential sectors: Power, real estate

and agriculture are core to our economy, but they can also generate high

emissions."

He also talks about investing in new technologies that will accelerate this decarbonization.

New technology in real estate can come in many different forms but there will be opportunities here to invest in them.

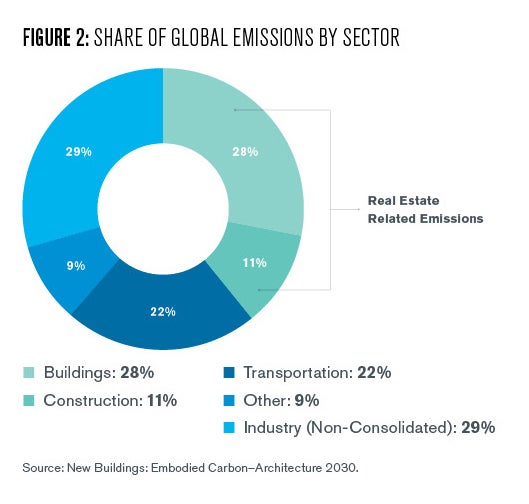

In fact, real estate is the largest contributor to climate change at 40% of global emissions and climate tech for real estate remains the elephant in the room:

It is not an

exaggeration to suggest that eliminating real estate’s 40% share (EIA

Outlook 2017) of global emissions will spawn the most significant

technological shift in the history of modern buildings. And yet, this

fact is gravely underappreciated by both traditional real estate

investors as well as prop-tech investors, the two pools of financial

capital that not only have the greatest power to directly catalyze the

inevitable transition to net zero buildings, but also to most directly

profit from its realization.

And it is not

just the investment community that is under-indexing climate tech for

buildings in their portfolio of investments or priorities. PWC recently

listed the top 13 disrupters to the real estate industry in its annual 2021 Disrupters for Real Estate

report. Climate tech for real estate was nowhere on the list (PWC

2021), a tremendous oversight if we consider how rapidly the building

decarbonization policy landscape is evolving, how costly it will be to

building owners, and how much new venture funding is being raised to

hasten the decarbonization transition.

In Q4 2020, the

European Union passed its “Renovation Wave” regulations—requiring a 60%

reduction of carbon emissions in buildings over the next decade, along

with an 18% reduction in heating and cooling demand. Building owners

that do not comply will pay substantial fines.

Bloomberg New

Energy Finance estimates that in Europe alone, this will cost more than

$3 trillion (Coker & Champion 2021). The European Renovation Wave,

which followed policy precedents from Los Angeles’s 2019 Green New Deal

and New York’s Local Law 97, pulled the real estate community into the

the epicenter of the climate change conversation.

This digest

analyzes why the real estate community should consider investing more

capital into the Climate Tech for Real Estate ecosystem, and where

current policy may be falling short in promoting this capital influx.

Furthermore, we will map out the eight largest categories emerging in

the Climate Tech for Real Estate subsector, and develop a framework for

assessing how participants across the real estate ecosystem could profit

from this once in a generation wealth creation opportunity.

You should read more about this from the Kleinman Center for Energy Policy here.

Clearly climate tech for real estate is a huge potential disrupter which investors need to be aware of.

Alright, let me wrap it up there.

I hope I provided you some food for thought in this comment and welcome feedback from real estate and other experts who are far more knowledgeable than I am concerning these issues.

Below, Stephane Theuriau, head of real estate at London-based private equity

firm BC Partners, discusses the future of post-pandemic commercial real

estate post-pandemic. "Some office space is going to get closer to where

people live," he said on Bloomberg Television. "The office has

been looked at as a cost center for too long. Now it's become a

competitive tool."

Second, last September, the Global Energy Center hosted a virtual discussion on how the real estate investors, innovators, owners, and operators can lead on carbon emissions reduction in the built environment.

Next, watch the GRESB Real Estate results for Americas from last November and last week, GRESB released the TCFD Alignment Report demo. You can watch this discussion below.

Lastly, a webinar launched on September 10, 2019, raising awareness about the Zero Carbon Buildings for All Initiative, proposed for the 2019 UN Secretary-General’s Climate Action Summit in New York.

Comments

Post a Comment