James Bradshaw of the Globe and Mail reports Ontario public sector pension plan IMCO posted 8.1% loss in 2022:

Investment

Management Corporation of Ontario reported an average loss of 8.1 per

cent on its investments in 2022 as the pension fund investor’s exposure

to plunging values in public stock and bond markets punched a hole in

its annual returns.

With

inflation running at its highest levels in decades, a combination of

steep losses on a broad array of public equities and fixed-income

investments – which suffered a rare simultaneous decline last year –

battered returns for core portfolios at many pension plans. That made

for “a challenging year to say the least,” said IMCO chief executive

officer Bert Clark.

Assets under management at IMCO fell to $73.3-billion as of Dec. 31, from $79-billion a year earlier.

IMCO,

which invests on behalf of a number of pension plans for public-sector

employees in Ontario, was more exposed to the public-market declines

than many of its large pension-plan peers in Canada. More than

two-thirds of IMCO’s investments are in publicly traded assets, with a

comparatively smaller allocation to private assets such as

infrastructure, real estate and private equity.

In

part, that is because IMCO is a relatively new investor: It was created

less than six years ago to consolidate investing for several

public-sector pension funds. As it reports its third set of annual

investment results, it is still reshaping some portfolios that it now

manages for those various clients.

“Unfortunately

when you have a mostly public portfolio, broad public market conditions

are kind of like gravity: You can’t really escape it,” Mr. Clark said

in an interview. “We’re disappointed by minus 8 [per cent returns] but

we weren’t entirely surprised.”

IMCO

is gradually shifting more of its clients’ assets to private markets,

seeking to take advantage of its long-term investing horizon to make

higher returns on illiquid assets. And it is “positioning portfolios” to

suit a shifting investing environment marked by high interest rates and

rising levels of global uncertainty, Mr. Clark said. With valuations

for private assets taking longer to adjust than public markets, he said

“there needs to be real caution” to avoid buying those assets at

outdated, elevated values.

Among

IMCO’s clients, which include the Workplace Safety and Insurance Board

and the Ontario Pension Board, returns ranged from a loss of 9.1 per

cent to a gain of 1.6 per cent, leading to a weighted average loss of

8.1 per cent for the year.

That

still beat IMCO’s internal benchmark return of minus 8.4 per cent. Over

three years, the annual return on its investments is 2 per cent, ahead

of a benchmark of 1.6 per cent. Over the long term, IMCO aims to boost

returns for clients by beating its annualized benchmark by 0.25 to 0.5

percentage points, “so we’re right on target,” Mr. Clark said. “But

there are things that are frankly working better than others.”

Last

year, IMCO’s investments in public equities and fixed income securities

both missed one-year benchmarks. Public stock investments lost 13.5 per

cent against a benchmark loss of 11.9 per cent, and are now worth

$18.6-billion. Fixed income missed an internal benchmark by 0.1

percentage points with a loss of 19.2 per cent, reducing the portfolio’s

value to $14.9-billion.

Returns

from the $10.7-billion real estate arm were also weak with a loss of

0.3 per cent. That fell far short of a 12 per cent gain for its

benchmark, though IMCO chief investment officer Rossitsa Stoyanova said

in an interview that “we are reviewing our real estate benchmark” as it

is not well matched to the plan’s portfolio.

By

contrast, gains on some private assets blew past benchmarks and helped

stem IMCO’s losses. Its $5.9-billion private equity portfolio gained 12

per cent, as IMCO closed 12 direct and co-investments. And its

$8.6-billion global infrastructure returned 7.4 per cent.

This

year, IMCO is “seeing a world of opportunities” in private credit as

some banks pull back on lending, and activity in private equity and real

estate has slowed, Ms. Stoyanova said. But in private assets, “you

can’t build a portfolio overnight.”

On Thursday, the Investment Management Corporation of Ontario (IMCO) issued a press release announcing it returned -8.1% in 2022 but beat its benchmark:

TORONTO (April 13, 2023) – The Investment

Management Corporation of Ontario (IMCO) today announced that the

weighted average net return of its clients' portfolios was -8.1% for the

year that ended December 31, 2022, compared to a consolidated benchmark

return of -8.4%. IMCO generated 0.3 percentage points of net value add

(NVA) in 2022. Since inception (or over the three years since assets

have been managed according to IMCO strategies) the annualized return

was 2%, compared to a consolidated benchmark return of 1.6%,

representing 0.4 percentage points in net value add. IMCO's assets under

management sat at $73.3 billion at the end of 2022.

IMCO's clients are public-sector entities, each with their own

unique investment horizon and tolerance for risk. Therefore, their

results are different both in absolute terms and NVA due to broad

differences in asset mix and maturity of their respective strategies.

The range of returns across IMCO's client portfolios was -9.1% to 1.6%

in 2022.

QUOTES

"Although 2022 was the most turbulent year for markets in

recent memory, we outperformed our benchmark and delivered added value

for the third straight year, reaffirming the effectiveness of our

long-term approach to helping clients build resilient portfolios," said Bert Clark, President and CEO of IMCO.

We witnessed an unusually large dispersion of returns across

pension funds and asset managers in 2022, where funds with higher

allocations to private assets typically posted higher returns," said Clark.

"We continue to help many of our clients increase their allocations to

private assets and to leverage their longer investment time horizon, as

well as our strategic relationships and direct investment capabilities."

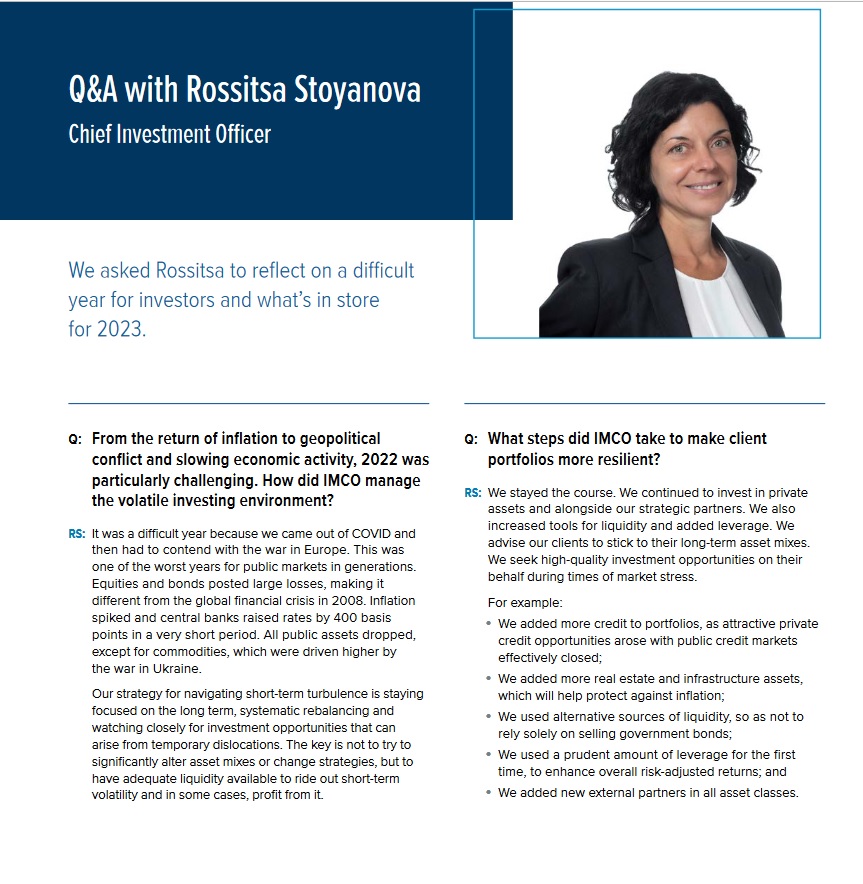

"2022 was a challenging year and we were certainly

disappointed in these returns. We remain focused on our strategy for

navigating short-term turbulence by maintaining discipline in executing

our long-term investment strategy, systematic rebalancing, and effective

liquidity management to capitalize on investment opportunities arising

from temporary dislocations," said Rossitsa Stoyanova, Chief Investment Officer of IMCO.

"We continue to increase our private market exposure alongside

our strategic partners, which was a huge returns' driver for us in

2022," said Stoyanova. "On the other hand, our absolute

returns' performance was driven mainly by losses in public equities and

fixed income, as both public markets and bonds took an unprecedented

hit."

As we move forward, responsible investing and ESG integration

will continue to play a growing role in our strategies. We believe that

companies that strategically manage material ESG risks and turn them

into opportunities will outperform their peers in the years to come and

understand the importance making this a priority for IMCO," added Stoyanova.

2022 HIGHLIGHTS

Generated 0.3 percentage points of value add for clients in 2022.

Over three years, achieved 0.4 percentage points of value add for clients.

Committed over $2 billion to new managers in our global credit portfolio, including new exposure to actively managed public credit.

Released Climate Action Plan, IMCO's road map to achieving Net Zero by 2050.

Published a comprehensive "World View," which detailed IMCO's perspectives on major global themes and their investment implications in the next five to 10 years.

123Dentist: Co-invested alongside

existing strategic partners, Peloton Capital and KKR, in a Canadian

dental support organization, as part of its merger with Altima Dental.

CDK Global Inc.: Invested with a new strategic

partner, Brookfield Capital Partners, in a leading software provider to

North American auto dealerships.

Trinity Life Sciences: Co-invested alongside

Kohlberg & Company in a company that helps bring new drugs to market

by providing consulting and analytics services.

Apax Global Impact Fund I: Committed $100

million to our first private equity investment in an impact fund that

focuses on themes that include environment and resources, health and

wellness, social and economic mobility, and technology businesses that

enable positive societal and environmental impact.

Infrastructure: Completed two direct investments, committed to two fund managers, and completed pooling.

DataBank:Invested US$450 million in a leading U.S. digital infrastructure operator, in partnership with global infrastructure investors.

Macquarie GIG Energy Transition Solutions Fund: Committed to invest $455 million to accelerate IMCO's investments in the global energy transition.

Antin Fund V: Committed to invest $552

million, which will target sectors in which Antin has established

operations and significant expertise, including transport, energy and

environment, telecom and social infrastructure.

Infrastructure Pool: IMCO completed its first

private market pool, which manages approximately $8.4 billion of client

assets, and enables clients to access this asset class efficiently.

Global Credit: Established

over $2 billion to new managers in 2022 and updated the credit strategy

to increase allocation to non-investment grade credit, private credit

and increased internalization.

Actively managed public credit: Invested US$1 billion

to two of the world's leading global credit managers, Loomis, Sayles

& Co. and Beach Point Capital Management. This provides IMCO clients

with access to investment grade debt, high-yield bonds, structured

credit and leveraged loans.

Carlyle Credit Opportunities Fund III:

Committed up to US$200 million to access special situations credit and

opportunities fueled by a rapidly shifting macroeconomic environment.

Blackstone Green Private Credit Fund III:

Committed up to US$300 million in a fund that will provide flexible

credit capital to companies and assets in renewable energy, the energy

transition, and climate change solutions.

Brookfield Infrastructure Debt Fund III:

Committed up to US$300 million in a fund that will add incremental yield

and diversification through exposure to hard assets with contracted

cash flows (utilities, renewable power, transportation, midstream

energy) outside North America.

Ares' Infrastructure Debt Fund V: Committed up

to US$300 million to help address the substantial gap between planned

and required investment to improve or replace aging infrastructure in

developed markets.

Real Estate: Diversified

the real estate portfolio and committed US$980 million to industrial,

life sciences, property technology and multi-residential investments,

alongside key strategic partners.

The Fifth Wall Climate Tech Fund:Committed to investing US$50 million in a fund that aims to decarbonize the real estate industry through new technologies developed by venture capitalist.

Tishman Speyer Separately Managed Account 2.0:

Committed an additional US$500 million to invest in strategic value-add

and build-to-core opportunities, as part of a portfolio of modern

assets in office, mixed-use and multi-residential sectors in major U.S.

markets.

Tishman Speyer Proptech Venture fund: US$30

million committed to a fund that invests in early-stage companies with

technologies intended to improve efficiencies in real estate and the

construction processes (not specific to climate).

WPT Industrial Joint Venture: Committed an

additional US$400 million to a portfolio of industrial properties in

strategic U.S. logistics markets through development, redevelopment, and

value-add strategies.

PORTFOLIO PERFORMANCE BY ASSET CLASS 2022 Net Investments and Rates of Return (As of Dec. 31, 2022)

Asset Class

Net Investments ($ billions)

1-Year Return

(Percentage)

3-Year Return

(Percentage)

Actual

Benchmark

NVA4

Actual

Benchmark

NVA4

Public Equities

$18.6

(13.5%)

(11.9%)

(1.6%)

3.6%

4.5%

(0.9%)

Fixed Income

$14.9

(19.2%)

(19.1%)

(0.1%)

(4.8%)

(4.8%)

0.0

Real Estate1

$10.7

(0.3%)

12.0%

(12.3%)

(0.3%)

2.6%

(3.0%)

Global Infrastructure

$8.6

7.4%

(3.7%)

11.1%

7.0%

1.7%

5.3%

Global Credit

$6.8

(7.7%)

(12.8%)

5.1%

1.8%

(2.1%)

3.9%

Public Market Alternatives

$4.9

1.9%

3.6%

(1.7%)

2.4%

1.8%

0.6%

Private Equity

$5.9

12.0%

(9.1%)

21.1%

21.4%

5.1%

16.3%

Money Market and Other2

$1.4

-

-

-

-

-

-

Leverage3

($2.7)

-

-

-

-

-

-

Total

$69.1

(8.1%)

(8.4%)

0.3%

2.0

1.6%

0.4%

1Real Estate is net of certain assets (mortgages) and investment-related liabilities (debentures).

2Money Market & Other also includes other

assets and strategies for portfolio rebalancing and asset allocation

purposes and are included in the total return.

3Leverage employed by IMCO's clients as part of

their strategic asset allocation is applied at the total portfolio

level rather than within a specific asset class.

4Net value add (NVA) is the difference between

investment returns of an asset class, net of all direct and indirect

costs, and its respective investment policy statement (IPS) benchmark.

Take the time to download and read IMCO's 2022 Annual Report which is available here.

I reached out to IMCO's CEO and CIO, Bert Clark and Rossitsa Stoyanova, to discuss these results.

Neil Murphy, Vice President Corporate Communications emailed me to say "unfortunately Bert and Rossitsa are not available for an interview."

That's alright, I cannot always please everyone all the time, nor is this my goal.

Importantly, I'm fair but ruthless, when Canada's large pension funds do a good job, I will praise them but when I smell something fishy or when they screw up, I will come after them hard even if this costs me access to senior managers.

Truth be told, I do not need access to CEOs or CIOs to cover results properly.

I knew IMCO's results were going to be negative because I understand their asset mix which is more weighted to public markets than that of its large Canadian peers.

And last year, both stocks and bonds got hit, so not too surprised that IMCO posted an 8.1% loss in 2022, faring a little but better than HOOPP which posted a. 8.6% loss last year.

Differences in asset mix help explain most of the variation in returns among Canada's top pensions.

More mature pension plans that have allocated 50% of their asset mix to private markets fared better last year than large Canadian pension funds which have allocated more to pubic markets (as both bonds and stocks got hit last year).

Will this be the case this year? I seriously doubt it as I see a deep and prolonged global recession headed our way, one which will impact public and private markets.

So, private markets will not "save" Canada's large pension funds in 2023 and public markets will once again drag down returns because the earnings recession is just getting underway.

Capiche? 2023 won't be any better than 2022, it will be far worse for all pension funds, including Canada's Maple Eight (Nine if you include IMCO).

***

Before I get to my analysis and comments, Bert Clark, President & CEO of IMCO posted a comment on LinkedIn on Taking the Long View:

2022 – A CHOPPY RIDE FOR INVESTORS

2022 was a

challenging year for most investors, with historically weak results

across many asset classes. The S&P 500 lost 18 per cent, U.S.

corporate bonds lost 15 per cent, ten-year U.S. Treasuries lost 12 per

cent, and the North American REIT index declined 28 per cent. Only a few

asset classes performed well: Cash was up two per cent, the U.S. dollar

rose seven per cent against the Canadian dollar, and commodities rose

by 16 per cent. Private assets were somewhat insulated from declines in

the public markets, as private valuations typically lag their public

market equivalents.

The combination of large and divergent

movements in asset classes resulted in a wide range of returns for

institutional investors in 2022 (see table below). Funds with long-term

strategic asset allocations that are heavily weighted to private assets,

shorter duration bonds, and with little or no U.S. dollar hedging

achieved stronger returns than funds holding more public assets, longer

duration bonds, and more hedged U.S. dollar exposure.

2022 Returns: Global Institutional Investors

Source: IMCO Research Team

2023 – STAYING THE COURSE IN TURBULENT TIMES

With

interest rates rising more than 400 basis points over the past 12

months, and the move toward “quantitative tightening”, or shrinking of

balance sheets by central banks, we are now seeing ripple effects

throughout the financial system. The $212 billion Silicon Valley Bank

was the first sizeable bank failure since the 2008 global financial

crisis and UBS had to take over the struggling Credit Suisse with the

support of the Swiss government. Investors are now closely watching

whether ongoing restrictive monetary policy will negatively impact

economic growth levels in 2023 by decreasing demand.

Challenging

environments like these can tempt some investors to try to temporarily

change their asset mix to avoid the short-term market risk. Temporarily

altering asset mix is exceedingly difficult to time right and the

consequences of mistiming can materially impact long-term returns. As a

result, we believe that our clients should hold firm on their long-term

strategies, including during periods of volatility.

One of the

most significant advantages that long-term investors can leverage is a

longer investment time horizon. This longer-term perspective combined

with proper liquidity management allows our clients to invest in asset

classes, such as equities, infrastructure, real estate, and credit,

which may be more volatile in the short term, but typically generate

higher returns over the long run. For example, $100 invested in the

S&P in 1928 would now be worth more than $624,000; while $100

invested in each of 10-year U.S. Treasuries and gold would be worth less

than $9,000. There have been periods when equities and other

growth-oriented assets have underperformed, but the long-term case for

growth-oriented assets is strong.

NAVIGATING THE CURRENT MARKET

Holding

firm to long-term strategies and maintaining a growth orientation does

not mean ignoring current market conditions. There are several

strategies we are employing on behalf of our clients to help them

navigate the current market. These include the following:

We

are carefully managing client liquidity, in order to navigate what we

believe will be more frequent, and longer, periods of market volatility

than in the recent past. Central banks cannot be relied on to quickly

address market downturns in an environment of potentially higher

inflation.

We are gradually re-orienting client bond exposures

to reflect a more balanced mix of inflation and nominal bonds to protect

from what we believe will be more frequent periods of higher inflation

than in the recent past. There are many global inflationary forces, such

as the energy transition and slowing globalization.

We are

investing in the energy transition, which will create significant

opportunities for investors with the right expertise and a pragmatic

approach.

We are closely monitoring the increased geopolitical

and ESG risk related to investing in China and we are avoiding

“overweights” to China and limiting investments there to liquid public

investments.

We ensure that new private market transactions are

done at valuations that are in line with their public market

equivalents, even though most private market book values still lag their

public market equivalents.

We are being careful about portfolio

rebalancing decisions that are driven by the denominator effect of

reduced assets under management when public markets have repriced more

than private markets. We don’t believe in selling private markets’

assets or slowing new investments to reduce allocations driven by lagged

valuations.

Finally, we continue to increase our clients’

allocations to private credit, where deal terms have significantly

improved, and deal volumes have not fallen off in the same way as other

private asset classes (like private equity, real estate and

infrastructure where owners have more flexibility than borrowers to

postpone transactions).

2022 was a challenging year for many investors and 2023 has already had its fair share of market volatility. However, we continue

to believe that for long-term investors the right course of action is

to stick to their long-term plans, maintain a growth asset orientation,

avoid the impulse to step out of the markets until things feel more

settled, and take steps to optimize portfolios within the current market

context.

Alright, some quick points on Bert's comment above:

No doubt, 2022 was choppy and turbulent with both stocks and bonds getting hit hard as inflation reached a 40-year high, prompting central banks led by the Fed to hike rates aggressively. We pay Canada's large pension fund managers big bucks to be able to foresee such "short-term trends" but the reality is many cannot escape the carnage because their investment policy is too geared toward public markets.

Second, while Canada's large pension funds can take advantage of their "long investment horizon" to capitalize on opportunities as they present themselves, this time is a bit different. What I mean by this is the depth and duration on the coming global recession will be unlike anything we have seen in decades, clobbering public and private markets and private credit!

Third, IMCO is reorienting its portfolio in bonds to reflect a higher inflationary environment and that rates will be higher for longer, but Bert states they do not attempt any tactical asset mix decisions. If you look at the two global pensions that produced the strongest returns in 2022 -- OMERS and OTPP -- yes they were more heavily weighted in private markets but they also did an amazing job shortening up their bond duration, adding significant value over their fixed income benchmarks. True, most pension funds are terrible at tactical asset allocation, and it isn't easy (CDPQ tried for years unsuccessfully), but they're not hiring the right talent to do TAA properly internally. The same goes for currency hedging and alpha, hire the right people to consistently add alpha in currencies.

No doubt, liquidity management is much more important than diversification, especially when the going gets rough (see my recent comment on OPTrust).

China is fraught with geopolitical risks, best ot take a much more cautious approach investing there.

Ensuring that new private market transactions are

done at valuations that are in line with their public market

equivalents is a way to ensure your private market assets are not way overvalued and I also agree that you cannot cut allocations to private markets because stocks and bonds got hit hard one year. That is just plain dumb.

Increasing allocations to private credit at a time when the global economy is on the cusp of a severe and long recession isn't the way to go, in my humble opinion.

The U.S. commercial credit market has grown significantly since the

global financial crisis (GFC), particularly in pockets outside of the

more heavily regulated U.S. banking sector, including the private credit

segment.

While the contagion risks and interconnectedness to the broader economy

are difficult to identify given a high degree of opacity in the non-bank

financial intermediation (NBFI) sector, Fitch Ratings believes a credit

cycle downturn in private credit will not have widescale financial

stability implications given the limited liquidity transformation risks,

since private credit is typically held in closed-end funds with

committed capital for extended periods.

Further, while growth in private credit has been strong, it still

represents a modest portion of the overall U.S. commercial credit market

at approximately 12%, and a small portion of the US economy, at just 3%

of GDP. That said, to the extent any recession is deeper and/or longer

than anticipated this would pressure market access, particularly for

weaker credits, at a time when financial market conditions are likely to

further tighten following several bank failures in the U.S. in

mid-March. While we believe the risks are sufficiently mitigated and

that any deterioration in the private credit sector will not in itself

cause systemic issues in the financial sector, the opacity in the

overall NBFI market make it more challenging to have a great deal of

visibility into expected outcomes.

I immediately called out this report on LinkedIn stating Fitch doesn't have a clue about what is going in private credit because by definition it's PRIVATE and NOT RATED:

For example, the report

doesn't mention how many of the newer closed end funds are peddling

their untitranche loans as senior debt when in reality they have 25-40%

junior debt in there.

Moreover, while banks aren't investing in

unitranche debt, they certainly have been very active originating and

selling them to clients and they're exposed to any serious crisis in

this unregulated area.

Experts I talk to tell me there's a lot more risk in private credit than what investors are aware of and it's a disaster waiting to explode.

All I know is big pension funds with a lot of private debt experience (CPP Investments) know what their loan exposures are and they're on top of the risks and underwriting standards.

We will not know who the amateurs are in private debt until the next crisis hits this asset class.

IMCO has experts in private debt who understand the risks of this asset class. Jennifer Hartviksen, Managing Director, Global Credit is an expert in her field but I did notice Christian Hensley, Senior Managing Director, Equities and Credit, is no longer at IMCO, raising more questions about what the hell is going on at this organization (Christian came from CPP Investments, he hired Jennifer and is a recognized expert in private debt).

[Note: A little word of advice to anyone looking to join IMCO, think long and hard before doing so and wait till there's a change in leadership and a cleanup at their Board before doing so. The place is a huge mess and it's not necessarily the fault of the investment or executive team.]

Below, I'll only reprint the bright spots in a challenging year:

Our net value add was good, with strong outperformance

by our private asset strategies. We delivered 0.3

percentage points of NVA, which shows the benefit of

active investment management. This result would have

been impossible for our clients with index investing.

We also finalized our five-year strategy and in it,

identified the priorities that will enable us to deliver

investment excellence.

We think that sharing strategic research insights with

clients and integrating them into portfolio decisions is part

of our role. That’s why we developed our comprehensive

World View which provides our perspectives on major

global themes and their investment implications in the

next five to 10 years.

We also completed planned initiatives that will reduce

costs for clients. For example, we launched our first

private asset pool, the Infrastructure Pool. In public

equities, we continue honing our roster of external

managers to reduce fees and are allocating more to

factor and index investing. We also participated in more

private co-investments with external partners. All of

these will deliver savings. Costs matter because they

directly affect net returns.

I actually read IMCO's Insights which are pretty good (some better than others but all worth reading).

Here are IMCO's major global trends and implications for clients:

Below, some highlights from 2022, IMCO's portfolio in brief and regional allocation:

And here are the asset class returns over the last year and three years:

Apart from Private Equity and Infrastructure, I can't say there was anything spectacular over the last three years and even those asset classes performed in line with their large peers.

This brings me to IMCO's executive compensation for 2022 (full discussion page 71 of Annual Report):

Wow! IMCO's CEO Bert Clark CIO Rossitsa Stoyananova both collected $3.3 million and their Chief Risk Officer Ben De Prisco collected $1.5 million.

Now, I'll spare Ben De Prisco even though I think his compensation is very generous for the job he's doing but paying Bert Clark and Rossitsa Stoyananova $3.3 million for a year where they were down 8% (the average Canadian DB plan was down 10%) is ridiculous.

Even if you look at three-year returns, they generated 40 basis points over their benchmark, hardly exceptional by any stretch and definitely not worth $3.3 million.

What is going on at Canada's large pension funds? Yes, we need to pay for talent but we need to keep it real and pay for stellar long-term performance!

When I see Ziad Hindo and Satish Rai pulling in $4 million last year, it doesn't exactly sit well with me but at least they generated the long-term performance to justify their (outrageous) compensation.

I cannot say the same for Bert & Rossitsa and while I like Rossitsa and think she's really good, I need to keep it real on compensation.

My neurosurgeon at the Montreal Neurological Institute, Dr. Benoit Goulet, is the Director of the Spine and Peripheral Nerve Program.

He works his tail off there, has huge responsibilities and he isn't pulling in anywhere close to $3-4 million a year and he's a top neurosurgeon.

Let this sink in as we pay Canada's public pension fund executives millions in compensation (and many, many managing directors are pulling over a million dollars a year and they're definitely not neurosurgeons).

These are people managing public pension funds, they have captive clients.

Yes, we have to pay for performance but let's take it down a notch, they're not neurosurgeons nor do they have the skill set and responsibilities of a neurosurgeon!!!

"Well Leo, the CEO of Royal Bank pulled in $15 million in total compensation last year. Also, if our public pension executives leave who will take over?"

In all honesty, I can easily provide you with a long list of exceptional individuals (men and women) who will take over for a lot less compensation a year (closer to a million a year).

And the CEO of Royal Bank, Dave McKay and his counterparts at other Canadian banks are grossly overpaid, it's a scandal (no CEO should make more than 30 times average salary of people working at their organization, especially at Canadian banks which are protected by the federal government from outside competition).

In contrast, LTK (Leo Thomas Kolivakis) Capital Management doesn't enjoy a huge salary, has NO defined benefit pension, and has to eat what he kills (this is called living real capitalism, not fake capitalism!).

On that note, it's a good reminder here that all you executives getting millions in compensation to pay up for the exceptional service I provide covering pensions and investments in detail.

There is no other financial blog in the world that covers pensions and investments like I do, none.

Wow, I'm totally flabbergasted and I'm questioning what IMCO's Board is thinking doling out this type of compensation.

Chair Brian Gibson is no fool, far from it, but I noticed that OTPP's inaugural CIO, Bob Bertram, has recently left IMCO's Board and this just confirms my worst fears, things are NOT going well at IMCO at all.

I would highly recommend their clients, existing and prospective, contact me directly at LKolivakis@gmail.com and I will gladly provide them a series of very tough questions to ask senior executives and board members.

On that note, it's Orthodox Christian Easter this Sunday, I want to wish Rossitsa and all Orthodox Christians celebrating the resurrection of Christ a Happy Easter (Chistos Anesti, it's going to be a beautiful weekend).

As far as markets, I remain more bearish than ever and will only leave you with two tweets:

Fed is going to have a hell of a time navigating a soft landing in second half of the year! pic.twitter.com/HQaVQ5ZBQO

Get the hell out of banks while you still can and all cyclicals and pretty much all stocks before the huge haircut comes.

Alright, one more chart to make you ponder about markets:

The VIX is being manipulated lower and lower to make it look like everything is just peachy, but it's far from peachy:

‘Other things will break.’ Legendary investor Jeremy Grantham warns of more financial chaos and wants to see Powell ‘channel a little bit of Volcker’ https://t.co/oi8lY32vIg via @YahooFinance

And a brutal earnings recession is just getting underway, more to come next week!

Below, Wharton Professor Jeremy Siegel joins 'Halftime Report' to discuss economic data, bank lending constraints suggesting further economic declines, and when the Fed will cut rates.

Siegel thinks stocks will struggle in the next six months and the Fed will cut rates this year lower than those futures

signal, once policymakers have seen a slowdown in inflation and economic

activity.

I think he's overly optimistic and the Fed will only cut if there's a financial crisis hitting markets, and that will not be good for stocks and other risk assets.

Also, Christopher Harvey, Wells Fargo Securities, joins 'Closing Bell' to discuss the revenue outcomes of business right-sizing, whether investors should sell before May, and the stimulus implications of a ruling on student loan forgiveness.

Third, former US Treasury Secretary Lawrence Summers comments on the current state of the US economy during an interview with David Westin on "Wall Street Week Daily."

Fourth, Larry Fink, BlackRock chairman and CEO, joins 'Squawk on the Street' to discuss money leaving the banking system in to the capital markets, changing payments with digitizing currency, and interest rates remaining higher for longer.

Fifth, the ‘Halftime Report’ investment committee, Josh Brown, Bill Baruch, Jason Snipe and Stephanie Link, discuss the latest inflation reports and expectations for the Fed. Link also thinks remains sticky and Fed will keep hiking rates.

Sixth, "I am terrified that if central banks don't own their mistakes...people are going to say 'You're not accountable enough,'" Mohamed El-Erian, a Bloomberg Opinion columnist, says during a panel discussion in Washington.

Seventh, Saira Malik, Nuveen CIO & Kristina Hooper, Invesco Chief Global Market Strategist discuss what a recovery could look like and the importance of investing in resilient companies.

Lastly, since it's Orthodox Easter this weekend something beautiful my mom sent me.

Comments

Post a Comment