Will The Fed Keep At It Until the Job is Done?

Stocks rallied Friday as traders cheered comments from Federal Reserve Chairman Jerome Powell at the annual central bank conference in Jackson Hole, Wyoming, that point to stronger-than-expected economic growth.

The Dow Jones Industrial Average closed up 247.48 points, or 0.7% at 34,346.90, after being up more than 300 points at session highs. The S&P 500 gained about 0.7% to close at 4,405.71, while the tech-heavy Nasdaq Composite advanced 0.9% to 13,590.65, which was enough to help both indexes snap a three-week losing streak. However, the Dow logged a second-straight week of losses.

The S&P 500 energy and consumer discretionary sectors both rose at least 1% on Friday. Petroleum company Valero Energy and toymaker Hasbro were among the day’s biggest gainers, advancing 2.8% and 5.7%, respectively.

Optimism was fueled, in part, by Powell’s confidence in continued economic growth in the U.S., as he cited “especially robust” consumer spending and early signs of a recovery in the housing market. He reiterated the central bank’s commitment to pull inflation back down to its 2% goal.

“The economy may not be cooling as expected. So far this year, GDP (gross domestic product) growth has come in above expectations and above its longer-run trend, and recent readings on consumer spending have been especially robust,” Powell said. “In addition, after decelerating sharply over the past 18 months, the housing sector is showing signs of picking back up.”

Given that Powell gave no clear indication of which way he sees interest rates heading, however, LPL Financial chief global strategist Quincy Krosby said the trajectory of rising Treasury yields will be a key underpinning of market direction.

“Regardless of the reason that yields move higher, what they do is that they tighten financial conditions by themselves because the cost of capital goes up,” Krosby said. The yield on the benchmark 10-year Treasury note ended Friday lower at 4.233%, after hitting highs earlier in the week.

Some investors expressed optimism that the Fed is nearing the end of its rate-hiking cycle.

“Maybe there are one or two left,” said Alex Petrone, director of fixed income for Rockefeller Asset Management, referring to increases in the Fed’ benchmark lending rate.

Similarly, Timothy Chubb, CIO of Girard, sees Friday’s comments from Fed officials beginning to give the market confidence that future rate hikes may not be necessary.

“We’re getting the data that we need to see as inflation moves from those 9% levels down to 3%. And I think at this point, the question really just revolves around how much pain is the Fed willing to further inflict on the economy to get inflation from 3% to 2%,” he said.

Jeff Cox of CNBC also reports Fed Chair Powell calls inflation ‘too high’ and warns that ‘we are prepared to raise rates further’:

Federal Reserve Chair Jerome Powell on Friday called for more vigilance in the fight against inflation, warning that additional interest rate increases could be yet to come.

While acknowledging that progress has been made and saying the Fed will be careful in where it goes from here, the central bank leader said inflation is still above where policymakers feel comfortable. He noted that the Fed will remain flexible as it contemplates further moves, but gave little indication that it’s ready to start easing anytime soon.

“Although inflation has moved down from its peak — a welcome development — it remains too high,” Powell said in prepared remarks for his keynote address at the Kansas City Fed’s annual retreat in Jackson Hole, Wyoming. “We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.”

The speech resembled remarks Powell made last year at Jackson Hole, during which he warned that “some pain” was likely as the Fed continues its efforts to pull runaway inflation back down to its 2% goal.

But inflation was running well ahead of its current pace back then. Regardless, Powell indicated it’s too soon to declare victory, even with data this summer running largely in the Fed’s favor. June and July both saw easing in the pace of price increases, with core inflation up 0.2% for each month, according to the Bureau of Labor Statistics.

“The lower monthly readings for core inflation in June and July were welcome, but two months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal,” he said.

Powell acknowledged that risks are two-sided, with dangers of doing both too much and too little.

“Doing too little could allow above-target inflation to become entrenched and ultimately require monetary policy to wring more persistent inflation from the economy at a high cost to employment,” he said. “Doing too much could also do unnecessary harm to the economy.”

“As is often the case, we are navigating by the stars under cloudy skies,” he added.

Markets were volatile after the speech, but stocks powered higher later in the day and Treasury yields were mostly up. In 2022, stocks plunged following Powell’s Jackson Hole speech.

“Was he hawkish? Yes. But given the jump in yields lately, he wasn’t as hawkish as some had feared,” said Ryan Detrick, chief market strategist at the Carson Group. “Remember, last year he took out the bazooka and was way more hawkish than anyone expected, which saw heavy selling into October. This time he hit it more down the middle, with no major changes in future hikes a welcome sign.”

A need to ‘proceed carefully’

Powell’s remarks follow a series of 11 interest rate hikes that have pushed the Fed’s key interest rate to a target range of 5.25%-5.5%, the highest level in more than 22 years. In addition, the Fed has reduced its balance sheet to its lowest level in more than two years, a process which was seen about $960 billion worth of bonds roll off since June 2022.

Markets of late have been pricing in little chance of another hike at the September meeting of the Federal Open Market Committee, but are pointing to about a 50-50 chance of a final increase at the November session. Projections released in June showed that almost all FOMC officials saw another hike likely this year.

Powell provided no clear indication of which way he sees the decision going.

“Given how far we have come, at upcoming meetings we are in a position to proceed carefully as we assess the incoming data and the evolving outlook and risks,” he said.

However, he gave no sign that he’s even considering a rate cut.

“At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks,” Powell said. “Based on this assessment, we will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data.”

The chair added that economic growth may have to slow before the Fed can change course.

Gross domestic product has increased steadily since the rate hikes began, and the third quarter of 2023 is tracking at a 5.9% growth pace, according to the Atlanta Fed. Employment also has stayed strong, with the jobless rate hovering around lows last seen in the late 1960s.

“The basic thought that they’re close to done, they think they probably have a little bit more to do ... that is the story they’ve been telling for a little while. And that was the heart of what he said today,” said Bill English, a former Fed official and now a Yale finance professor.

“I don’t think this is about sending a signal. I think this is really where they think they are,” he added. “The economy has slowed some but not enough yet to make them confident inflation is going to come down.”

Indeed, Powell noted the risk of strong economic growth in the face of widespread recession expectations and how that could make the Fed hold rates higher for longer.

“It was a balanced but not trend-changing speech, even if the Fed kept the ‘mission accomplished’ banner in the closet,” said Jack McIntyre, portfolio manager at Brandywine Global. “It leaves the Fed with needed optionality to either tighten more or keep rates on hold.”

Getting into details

While last year’s speech was unusually brief, this time around Powell provided a little more detail into the factors that will go into policymaking.

Specifically, he broke inflation into three key metrics and said the Fed is most focused on core inflation, which excludes volatile food and energy prices. He also reiterated that the Fed most closely follows the personal consumption expenditures price index, a Commerce Department measure, rather than the Labor Department’s consumer price index.

The three “broad components” of which he spoke entail goods, housing services such as rental costs and nonhousing services. He noted progress on all three, but said nonhousing is the most difficult to gauge as it is the least sensitive to interest rate adjustments. That category includes such things as health care, food services and transportation.

“Twelve-month inflation in this sector has moved sideways since liftoff. Inflation measured over the past three and six months has declined, however, which is encouraging,” Powell said. “Given the size of this sector, some further progress here will be essential to restoring price stability.”

No change to inflation goal

In addition to the broader policy outlook, Powell honed in some areas that are key both to market and political considerations.

Some legislators, particularly on the Democratic side, have suggested the Fed raise its 2% inflation target, a move that would give it more policy flexibility and might deter further rate hikes. But Powell rejected that idea, as he has done in the past.

“Two percent is and will remain our inflation target,” he said.

That portion of the speech brought some criticism from Harvard economist Jason Furman.

“Jay Powell said all the right things about near-term monetary policy, continuing to hope for the best while planning for the worst. He was appropriately cautious on inflation progress & asymmetric about the policy stance,” Furman, who was chair of the Council of Economic Advisers under former President Barack Obama, posted on X, the social media site formerly known as Twitter. “But wish he had not ruled out shifting the target.”

On another issue, Powell chose largely to stay away from the debate over what is the longer-run, or natural, rate of interest that is neither restrictive nor stimulative – the “r-star” rate of which he spoke at Jackson Hole in 2018.

“We see the current stance of policy as restrictive, putting downward pressure on economic activity, hiring, and inflation,” he said. “But we cannot identify with certainty the neutral rate of interest, and thus there is always uncertainty about the precise level of monetary policy restraint.”

Powell also noted that the previous tightening moves likely haven’t made their way through the system yet, providing further caution for the future of policy.

You can read Fed Chair Jay Powell's Jackson Hole speech here and below (emphasis is mine):

Good morning. At last year's Jackson Hole symposium, I delivered a brief, direct message. My remarks this year will be a bit longer, but the message is the same: It is the Fed's job to bring inflation down to our 2 percent goal, and we will do so. We have tightened policy significantly over the past year. Although inflation has moved down from its peak—a welcome development—it remains too high. We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.

Today I will review our progress so far and discuss the outlook and the uncertainties we face as we pursue our dual mandate goals. I will conclude with a summary of what this means for policy. Given how far we have come, at upcoming meetings we are in a position to proceed carefully as we assess the incoming data and the evolving outlook and risks.

The Decline in Inflation So Far

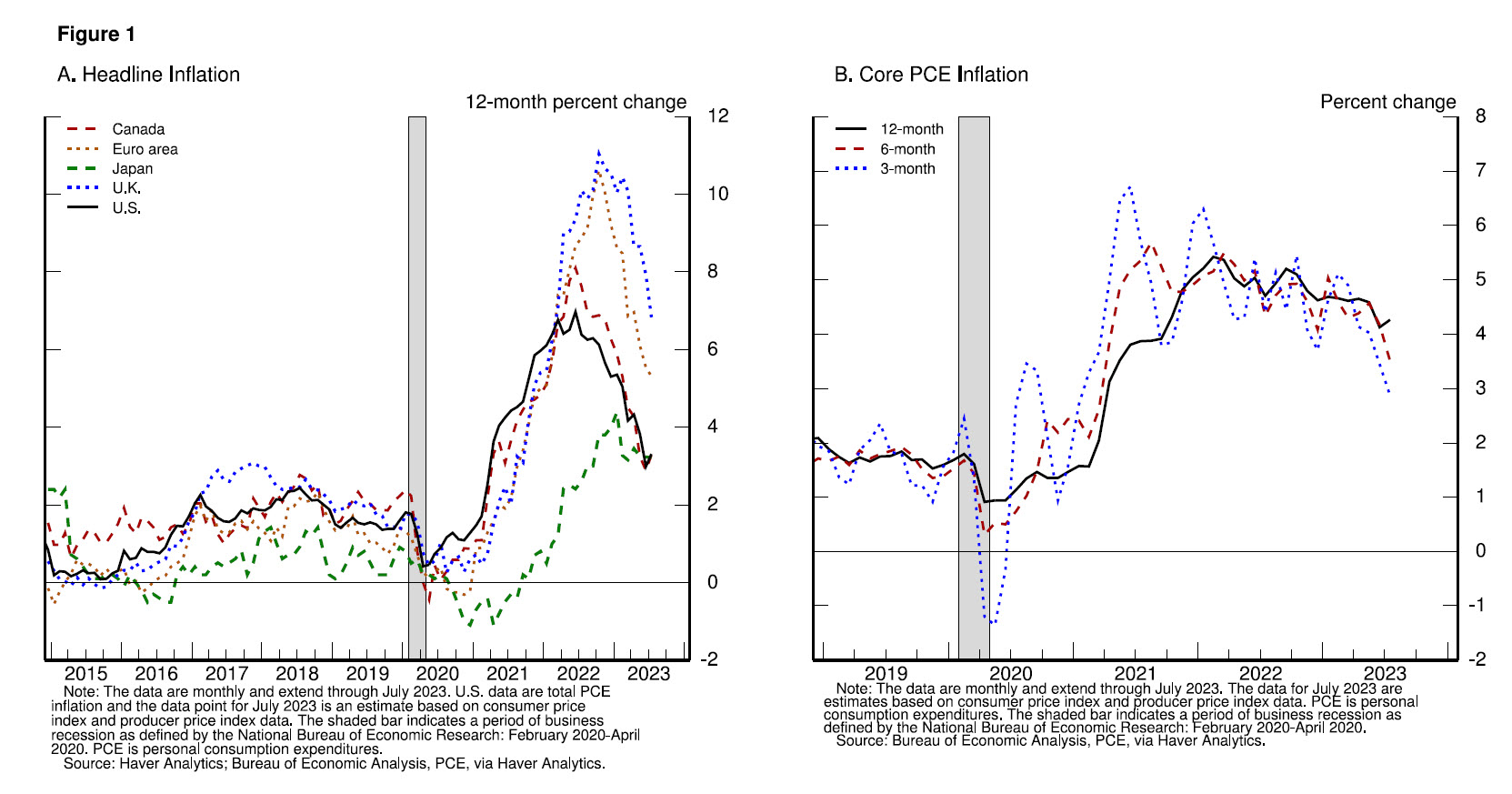

The ongoing episode of high inflation initially emerged from a collision between very strong demand and pandemic-constrained supply. By the time the Federal Open Market Committee raised the policy rate in March 2022, it was clear that bringing down inflation would depend on both the unwinding of the unprecedented pandemic-related demand and supply distortions and on our tightening of monetary policy, which would slow the growth of aggregate demand, allowing supply time to catch up. While these two forces are now working together to bring down inflation, the process still has a long way to go, even with the more favorable recent readings.On a 12-month basis, U.S. total, or "headline," PCE (personal consumption expenditures) inflation peaked at 7 percent in June 2022 and declined to 3.3 percent as of July, following a trajectory roughly in line with global trends (figure 1, panel A).1 The effects of Russia's war against Ukraine have been a primary driver of the changes in headline inflation around the world since early 2022. Headline inflation is what households and businesses experience most directly, so this decline is very good news. But food and energy prices are influenced by global factors that remain volatile, and can provide a misleading signal of where inflation is headed. In my remaining comments, I will focus on core PCE inflation, which omits the food and energy components.

On a 12-month basis, core PCE inflation peaked at 5.4 percent in February 2022 and declined gradually to 4.3 percent in July (figure 1, panel B). The lower monthly readings for core inflation in June and July were welcome, but two months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal. We can't yet know the extent to which these lower readings will continue or where underlying inflation will settle over coming quarters. Twelve-month core inflation is still elevated, and there is substantial further ground to cover to get back to price stability.

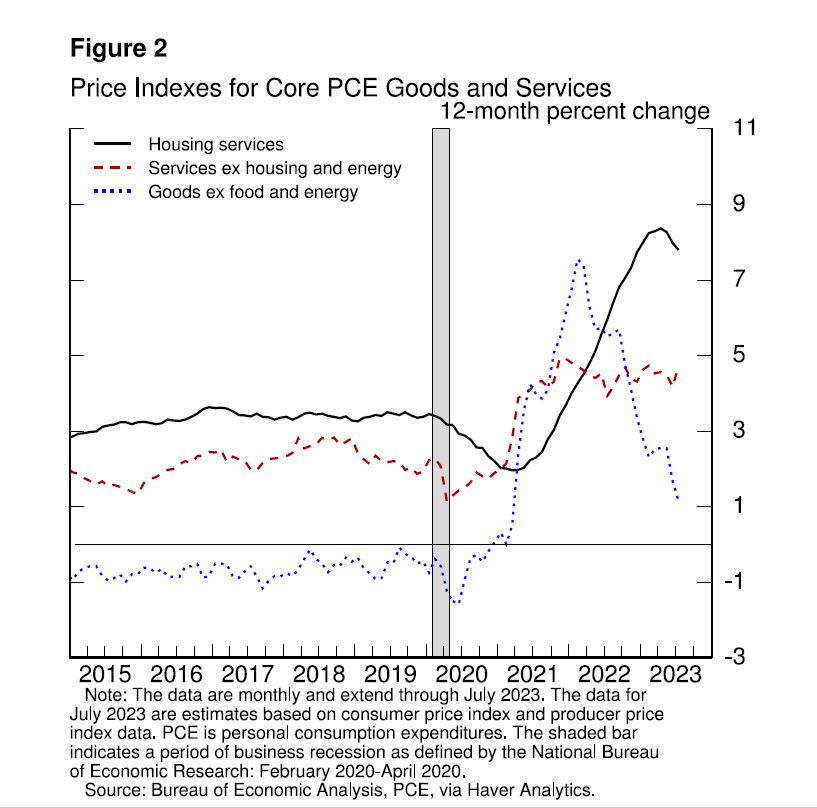

To understand the factors that will likely drive further progress, it is useful to separately examine the three broad components of core PCE inflation—inflation for goods, for housing services, and for all other services, sometimes referred to as nonhousing services (figure 2).

Core goods inflation has fallen sharply, particularly for durable goods, as both tighter monetary policy and the slow unwinding of supply and demand dislocations are bringing it down. The motor vehicle sector provides a good illustration. Earlier in the pandemic, demand for vehicles rose sharply, supported by low interest rates, fiscal transfers, curtailed spending on in-person services, and shifts in preference away from using public transportation and from living in cities. But because of a shortage of semiconductors, vehicle supply actually fell. Vehicle prices spiked, and a large pool of pent-up demand emerged. As the pandemic and its effects have waned, production and inventories have grown, and supply has improved. At the same time, higher interest rates have weighed on demand. Interest rates on auto loans have nearly doubled since early last year, and customers report feeling the effect of higher rates on affordability.2 On net, motor vehicle inflation has declined sharply because of the combined effects of these supply and demand factors.

Similar dynamics are playing out for core goods inflation overall. As they do, the effects of monetary restraint should show through more fully over time. Core goods prices fell the past two months, but on a 12-month basis, core goods inflation remains well above its pre-pandemic level. Sustained progress is needed, and restrictive monetary policy is called for to achieve that progress.

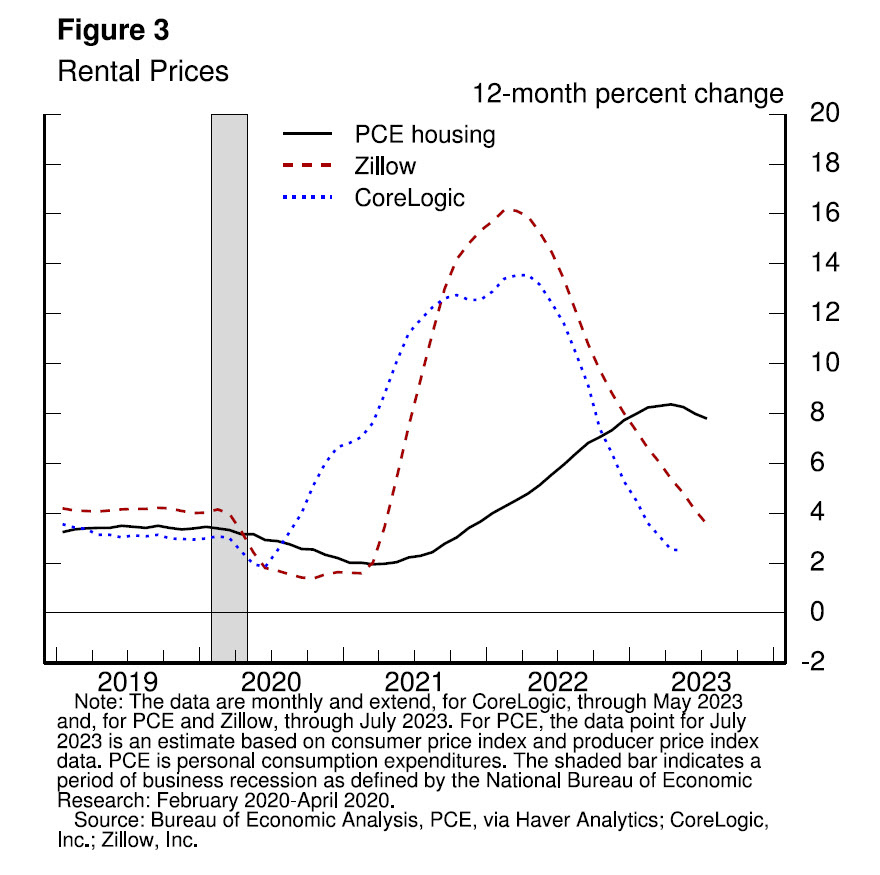

In the highly interest-sensitive housing sector, the effects of monetary policy became apparent soon after liftoff. Mortgage rates doubled over the course of 2022, causing housing starts and sales to fall and house price growth to plummet. Growth in market rents soon peaked and then steadily declined (figure 3).3

Measured housing services inflation lagged these changes, as is typical, but has recently begun to fall. This inflation metric reflects rents paid by all tenants, as well as estimates of the equivalent rents that could be earned from homes that are owner occupied.4 Because leases turn over slowly, it takes time for a decline in market rent growth to work its way into the overall inflation measure. The market rent slowdown has only recently begun to show through to that measure. The slowing growth in rents for new leases over roughly the past year can be thought of as "in the pipeline" and will affect measured housing services inflation over the coming year. Going forward, if market rent growth settles near pre-pandemic levels, housing services inflation should decline toward its pre-pandemic level as well. We will continue to watch the market rent data closely for a signal of the upside and downside risks to housing services inflation.

The final category, nonhousing services, accounts for over half of the core PCE index and includes a broad range of services, such as health care, food services, transportation, and accommodations. Twelve-month inflation in this sector has moved sideways since liftoff. Inflation measured over the past three and six months has declined, however, which is encouraging. Part of the reason for the modest decline of nonhousing services inflation so far is that many of these services were less affected by global supply chain bottlenecks and are generally thought to be less interest sensitive than other sectors such as housing or durable goods. Production of these services is also relatively labor intensive, and the labor market remains tight. Given the size of this sector, some further progress here will be essential to restoring price stability. Over time, restrictive monetary policy will help bring aggregate supply and demand back into better balance, reducing inflationary pressures in this key sector.

The Outlook

Turning to the outlook, although further unwinding of pandemic-related distortions should continue to put some downward pressure on inflation, restrictive monetary policy will likely play an increasingly important role. Getting inflation sustainably back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.Economic growth

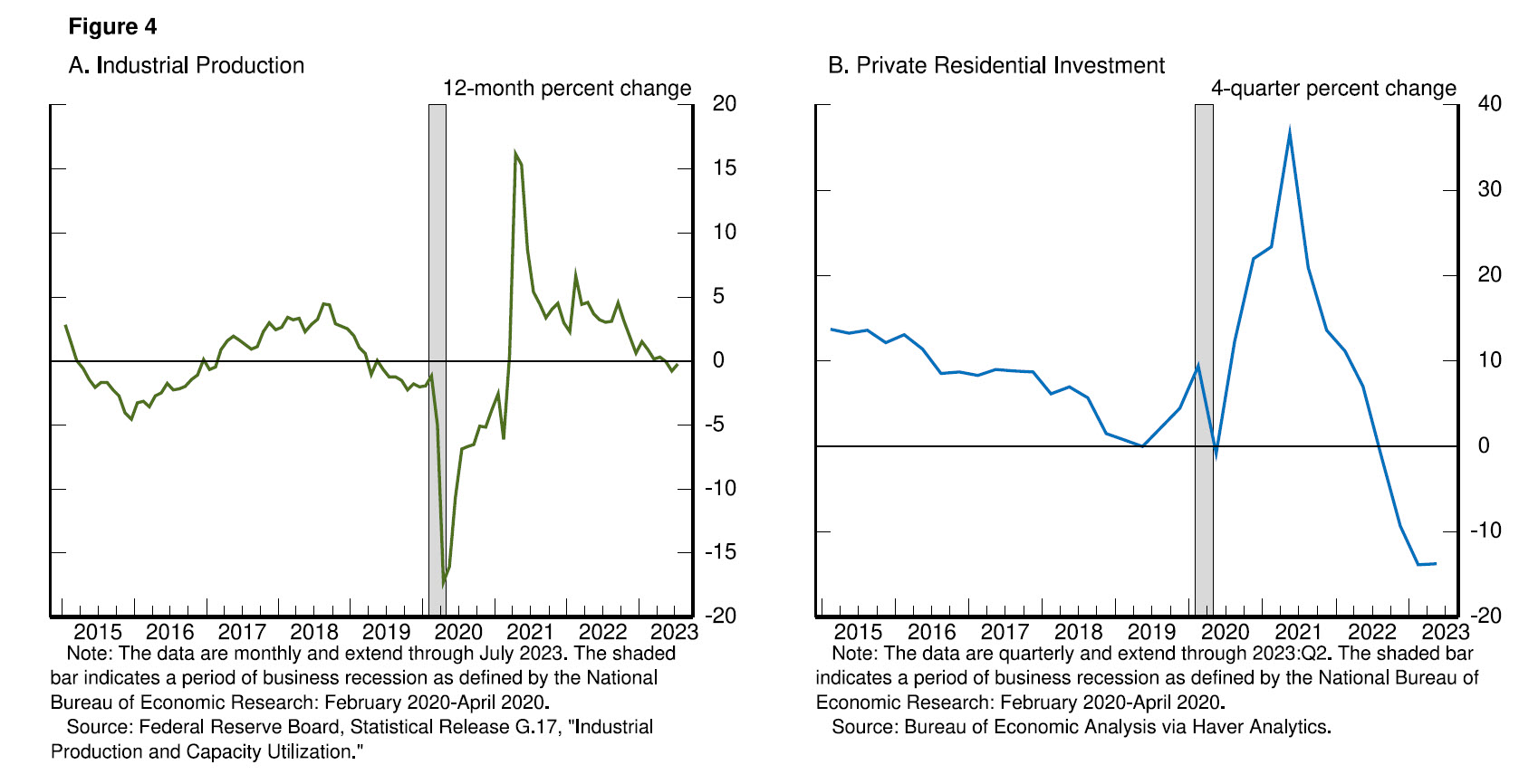

Restrictive monetary policy has tightened financial conditions, supporting the expectation of below-trend growth.5 Since last year's symposium, the two-year real yield is up about 250 basis points, and longer-term real yields are higher as well—by nearly 150 basis points.6 Beyond changes in interest rates, bank lending standards have tightened, and loan growth has slowed sharply.7 Such a tightening of broad financial conditions typically contributes to a slowing in the growth of economic activity, and there is evidence of that in this cycle as well. For example, growth in industrial production has slowed, and the amount spent on residential investment has declined in each of the past five quarters (figure 4).But we are attentive to signs that the economy may not be cooling as expected. So far this year, GDP (gross domestic product) growth has come in above expectations and above its longer-run trend, and recent readings on consumer spending have been especially robust. In addition, after decelerating sharply over the past 18 months, the housing sector is showing signs of picking back up. Additional evidence of persistently above-trend growth could put further progress on inflation at risk and could warrant further tightening of monetary policy.

The labor market

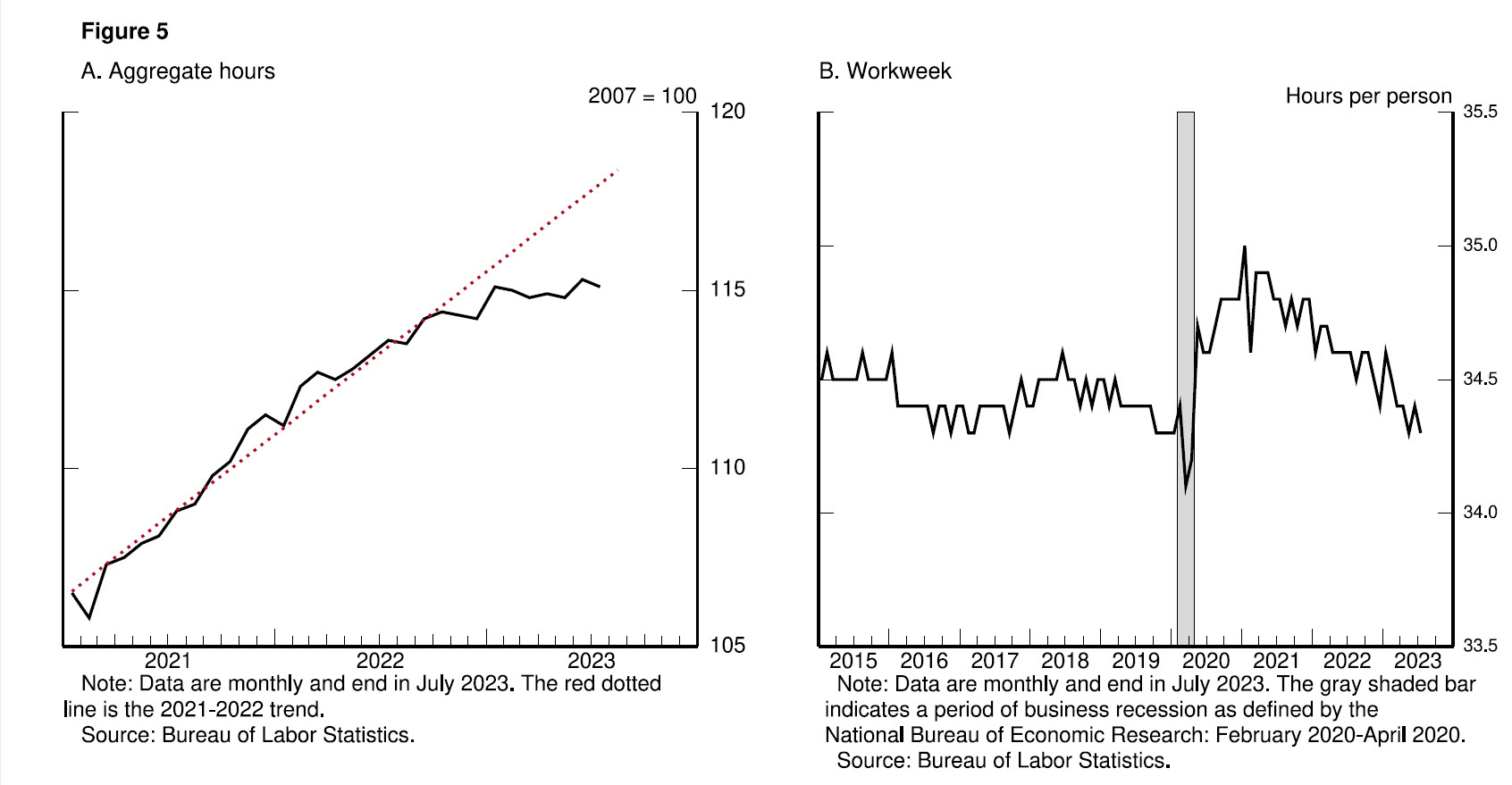

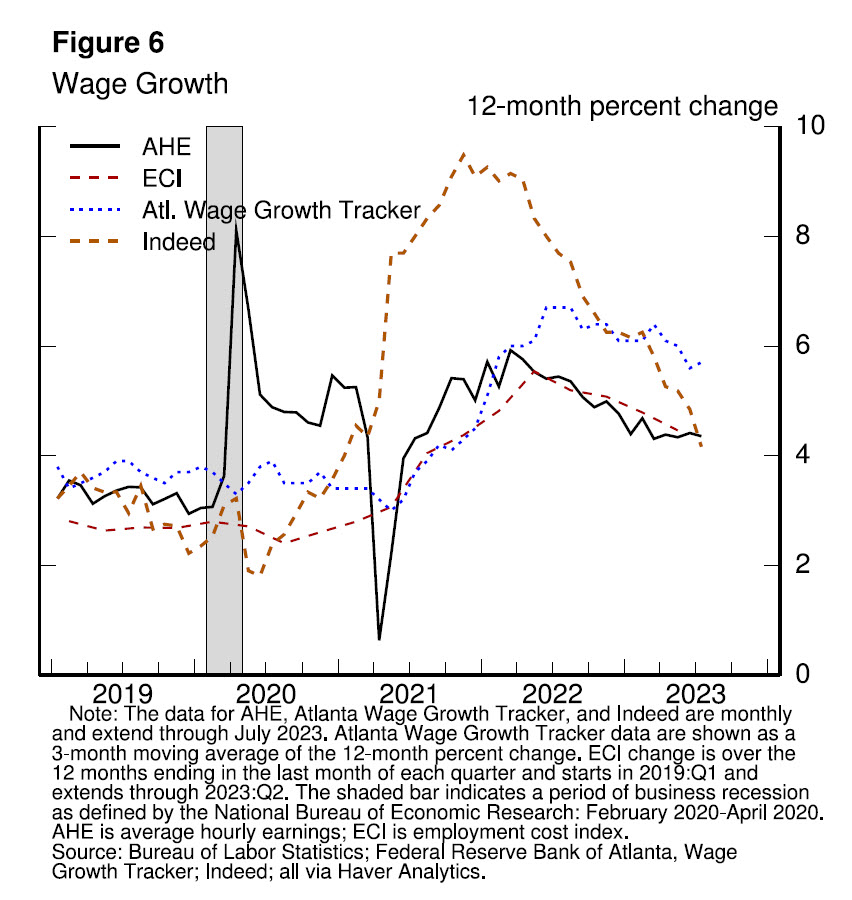

The rebalancing of the labor market has continued over the past year but remains incomplete. Labor supply has improved, driven by stronger participation among workers aged 25 to 54 and by an increase in immigration back toward pre-pandemic levels. Indeed, the labor force participation rate of women in their prime working years reached an all-time high in June. Demand for labor has moderated as well. Job openings remain high but are trending lower. Payroll job growth has slowed significantly. Total hours worked has been flat over the past six months, and the average workweek has declined to the lower end of its pre-pandemic range, reflecting a gradual normalization in labor market conditions (figure 5).This rebalancing has eased wage pressures. Wage growth across a range of measures continues to slow, albeit gradually (figure 6). While nominal wage growth must ultimately slow to a rate that is consistent with 2 percent inflation, what matters for households is real wage growth. Even as nominal wage growth has slowed, real wage growth has been increasing as inflation has fallen.

We expect this labor market rebalancing to continue. Evidence that the tightness in the labor market is no longer easing could also call for a monetary policy response.

Uncertainty and Risk Management along the Path Forward

Two percent is and will remain our inflation target. We are committed to achieving and sustaining a stance of monetary policy that is sufficiently restrictive to bring inflation down to that level over time. It is challenging, of course, to know in real time when such a stance has been achieved. There are some challenges that are common to all tightening cycles. For example, real interest rates are now positive and well above mainstream estimates of the neutral policy rate. We see the current stance of policy as restrictive, putting downward pressure on economic activity, hiring, and inflation. But we cannot identify with certainty the neutral rate of interest, and thus there is always uncertainty about the precise level of monetary policy restraint.That assessment is further complicated by uncertainty about the duration of the lags with which monetary tightening affects economic activity and especially inflation. Since the symposium a year ago, the Committee has raised the policy rate by 300 basis points, including 100 basis points over the past seven months. And we have substantially reduced the size of our securities holdings. The wide range of estimates of these lags suggests that there may be significant further drag in the pipeline.

Beyond these traditional sources of policy uncertainty, the supply and demand dislocations unique to this cycle raise further complications through their effects on inflation and labor market dynamics. For example, so far, job openings have declined substantially without increasing unemployment—a highly welcome but historically unusual result that appears to reflect large excess demand for labor. In addition, there is evidence that inflation has become more responsive to labor market tightness than was the case in recent decades.8 These changing dynamics may or may not persist, and this uncertainty underscores the need for agile policymaking.

These uncertainties, both old and new, complicate our task of balancing the risk of tightening monetary policy too much against the risk of tightening too little. Doing too little could allow above-target inflation to become entrenched and ultimately require monetary policy to wring more persistent inflation from the economy at a high cost to employment. Doing too much could also do unnecessary harm to the economy.

Conclusion

As is often the case, we are navigating by the stars under cloudy skies. In such circumstances, risk-management considerations are critical. At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks. Based on this assessment, we will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data. Restoring price stability is essential to achieving both sides of our dual mandate. We will need price stability to achieve a sustained period of strong labor market conditions that benefit all.We will keep at it until the job is done.

1. Descriptions of PCE inflation include Board staff estimates of the July 2023 values based on available information, including the July 2023 consumer price index and producer price index data. The July 2023 PCE inflation data will be published by the Bureau of Economic Analysis on August 31, 2023. Return to text

2. For example, 25 percent of respondents to the most recent University of Michigan Surveys of Consumers reported that it is currently a bad time to buy a new vehicle because of higher interest rates and tighter credit conditions, up from only 4 percent of respondents in 2021. For more information, see the preliminary results of the August 2023 survey, available on the University of Michigan's website at http://www.sca.isr.umich.edu. Return to text

3. This slowing in rent growth has likely occurred for a combination of reasons. Some of it likely reflects higher interest rates and the softening in real household income growth over the past couple of years. But the normalization of dislocations due to the pandemic is likely playing a role here as well. For example, the shifts in housing preferences related to working from home likely contributed to the increase in housing demand reflected in the sizable earlier increases in rents. As the price effects of that demand shift played out, the growth rate of rents would naturally decline toward its earlier trend. Finally, multifamily construction is quite high by historical standards, and that supply coming on line has likely also taken some pressure off market rents. Return to text

4. PCE prices for housing services include both the rents paid by tenants and an imputed rental value for owner-occupied dwellings (measured as the income the homeowner could have received if the house had been rented to a tenant). For additional details, see Bureau of Economic Analysis (2022), "Rental Income of Persons (PDF)," in NIPA Handbook: Concepts and Methods of the U.S. National Income and Product Accounts (Washington: BEA, December), pp. 12-1–12-15. Return to text

5. For an example of how tighter financial conditions affect economic activity, see the Federal Reserve Board staff's new index measuring U.S. financial conditions through their effect on the outlook for growth; the index is discussed in Andrea Ajello, Michele Cavallo, Giovanni Favara, William B. Peterman, John W. Schindler IV, and Nitish R. Sinha (2023), "A New Index to Measure U.S. Financial Conditions," FEDS Notes (Washington: Board of Governors of the Federal Reserve System, June 30). Return to text

6. Changes in real yields cited in this sentence refer to changes in yields on 2- and 10-year Treasury Inflation-Protected Securities. Return to text

7. In addition, as the policy rate increased, nonbanking lending conditions changed as well. For example, beginning in 2022 and continuing into the first half of this year, net issuance of riskier debt—such as leveraged loans and speculative-grade and unrated corporate bonds—in public credit markets declined. Return to text

8. The relationship between labor market slack and inflation, often called the Phillips curve relationship, is likely nonlinear, steepening in a tight labor market. If the Phillips curve has steepened in this way, a small change in labor market tightness could result in a more substantial change in inflation. It is difficult to know with precision how steep that relationship is in real time or how it might evolve as labor market tightness changes. For more information on nonlinearities in this relationship, see Christoph E. Boehm and Nitya Pandalai-Nayar (2022), "Convex Supply Curves," American Economic Review, vol. 112 (December), pp. 3941–69; Pierpaolo Benigno and Gauti B. Eggertsson (2023), "It's Baaack: The Surge in Inflation in the 2020s and the Return of the Non-Linear Phillips Curve (PDF)," NBER Working Paper Series 31197 (Cambridge, Mass.: National Bureau of Economic Research, April); and Nicolas Petrosky-Nadeau, Lu Zhang, and Lars-Alexander Kuehn (2018), "Endogenous Disasters," American Economic Review, vol. 108 (August), pp. 2212–45. Return to text

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Reading Powell's speech you might conclude there's not much there that is different from previous speeches.

The Fed remains committed to achieving 2% inflation and will do what is necessary to get the job done, but he did concede that monetary policy is restrictive and there is uncertainty as to when lags kick in.

I personally believe the Fed will wait to see next Friday's employment report to see if those lags are kicking in and I'm not convinced they will hike again at the next meeting.

Even if they do, it will be the last one and then a long pause will ensue where the Fed will pray wage inflation pressures don't pick up.

If they do, we can have a repeat of the 1970s, something Lawrence Summers hinted at this week:

This picture should be sobering to anyone convinced that we have reattained price stability. pic.twitter.com/pSbs7uZnOq

— Lawrence H. Summers (@LHSummers) August 24, 2023

Summers received criticism for posting this chart but he makes a good point, price stability can only be measured over a longer period here and it's way too soon to declare victory.

Anyway, here are some of the reactions from the Fed's Jackson Hole speech:

Powell definitely sounded more like Volcker today than he did Greenspan. Last line said it all: “We will keep at it until the job is done”. By the time the job is done, the economy will be knee-deep in recession.

— David Rosenberg (@EconguyRosie) August 25, 2023

"Higher for longer" is the somewhat muted message I got from Jackson Hole.

— Bill Gross (@real_bill_gross) August 25, 2023

The curve needs to disinvert but the likely future is for 10 year Treasuries to rise to 4.50 and short rates to remain relatively stable.

As expected, Powell rejects any idea that the inflation target would change in his Jackson Hole speech: "Two percent is and will remain our inflation target."

— Nick Timiraos (@NickTimiraos) August 25, 2023

I think it's really important to remember the full effects of restrictive monetary policy have yet to be felt and that is why smart macro managers are warning to forget about the soft or no landing scenario:

Repeat after me, we have not seen the whole impact of rate hikes yet pic.twitter.com/B4QzlXhZ3e

— Michael A. Arouet (@MichaelAArouet) August 25, 2023

The finance world is *all in* on the soft-landing or no landing outcome.

— Bob Elliott (@BobEUnlimited) August 25, 2023

Promoting GDPNow at 6%. '24 Earnings growth expected to be 12%. And this: 75% think either soft-landing or no-landing. Expectations of a good economic outcome this cycle have become extreme. pic.twitter.com/49TiFI4Nt8

Anyway, the market odds of another rate hike went up following Powell's speech but I would take this with a grain of salt:

BREAKING: Odds of a 25 basis point rate hike in September more than double, to 21.5%, after Powell speech.

— The Kobeissi Letter (@KobeissiLetter) August 25, 2023

Odds of an additional rate hike this year just hit a 2-month high of 52.1%.

Rate CUTS are now NOT expected to begin until JUNE 2024.

The Fed wants 2% inflation and will… pic.twitter.com/9i3EWbBpnO

The other thing I would take with a grain of salt is any talk of a robust consumer:

*GOOLSBEE: HAVEN'T SEEN CONSUMER SPENDING DETERIORATE - Bloomberg pic.twitter.com/o5htqKwaXF

— Lawrence McDonald (@Convertbond) August 25, 2023

US credit card debt has officially surpassed $1 trillion

— Game of Trades (@GameofTrades_) August 24, 2023

This is not sustainable with credit card rates above 20% pic.twitter.com/eRXKVIptCi

Disney $DIS closed back below its COVID Crash low from March 2020 yesterday.

— Bespoke (@bespokeinvest) August 25, 2023

COVID Crash low on 3/23/20: $85.76

Close on 8/24/23: $82.47

Change: -3.8% pic.twitter.com/hV8pdrrTom

And look at shares of Nike and Foot Locker as they provide a good indication of how robust retail sales will be in the future:

I think this nonsense of the "resilient US consumer" will soon come to an abrupt end.

As far as the stock market, the big news this week was Nvidia's stellar earnings.

Its share hit another all-time high on Wednesday after the close but sold off since as traders sold the news to pocket their gains:

It's all about valuations, elite hedge funds pumped this stock to the moon and now they're pulling the rug underneath retail investors.

You can trade it but don't be surprised if the selling picks up steam over the next couple of months.

I can say the same about the entire tech sector, especially if rates keep creeping up:

B of A: “.. best correlation past 15 years is central bank liquidity (insane surge from $5tn to $25tn) & tech stocks .. central bank balance sheets down $3tn yet Nasdaq wants new highs .. we say tech = H2 trouble rather than era of new AI rules ..” [Hartnett] pic.twitter.com/OCtVv9bIYx

— Carl Quintanilla (@carlquintanilla) August 25, 2023

Nasdaq $QQQ hitting resistance at its 50D moving average along with a bearish engulfing candle. Not ideal! pic.twitter.com/3woVy5VSaA

— Barchart (@Barchart) August 24, 2023

Not since the Tech Bubble have small cap stocks traded at this large of a discount relative to the overall equity market pic.twitter.com/m9tX84G7Ip

— Barchart (@Barchart) August 25, 2023

We shall see what September and October bring, too soon to tell.

Below, Federal Reserve Chairman Jerome Powell delivers remarks at the Federal Reserve's annual symposium in Jackson Hole, WY on Friday.

Next, Jeremy Siegel, University of Pennsylvania's Wharton School professor of finance, joins 'Closing Bell' to discuss what the market reaction to Powell's Jackson Hole speech says about the state of monetary policy, strong productivity despite a labor market slowdown, and the risk of commodity price inflation rising further.

Third, Jim Bianco joins Bloomberg to recap Powell's Jackson Hole Speech, Bond Yields & the Stock Market with Scarlet Fu and Sonali Basak.

Fourth, Lawrence H. Summers, Former US Treasury Secretary discusses US inflation, the need for another rate hike and shares his thoughts on Powell's speech. He speaks with David Westin on "Wall Street Week Daily."

Lastly, Lori Calvasina, RBC Capital Head of US Equity Strategy and Scott Chronert, Citi US Equity Strategist discuss the effect of rising yields on US equities. Calvasina is starting to see outflows in equities, while Chronert is still bullish on earnings in 2024.

Comments

Post a Comment