Have Pensions Succumbed to Casino Capitalism?

On March 1st, the Financial Times' Donald MacDonald reported that pension funds' long term view demands active role:

Forgive my skepticism, but while I applaud greater international collaboration on fixing the global financial crisis, I find it completely disingenuous that global pension funds are banding together now, after the crisis clobbered them in 2008, to respond by using "responsible investment initiatives."The reported 20 per cent decline in the value of pension fund assets in OECD countries in the first 10 months of last year has meant the current round of pension fund valuations is unlikely to bring much cheer to pension beneficiaries or their sponsors.

Those numbers are a powerful reminder to all institutional investors that decisive action is needed to protect our investments over the long-term.

So perhaps this is an appropriate occasion to consider how this crisis might change investor behaviour in the months and years to come. Will the behaviour of pension funds (particularly larger ones) better match the fact that their long-term horizons for liabilities and investments and diversified portfolios give them a direct and genuine fiduciary interest in the long-term economic health and wellbeing of the world?

To rebuild trust and confidence within financial markets, investors need fundamental improvements in risk management and transparency. To help achieve those goals, some suggest a commitment to active ownership must surely be at the heart of any successful long-term response from institutional investors.

That is why the global asset owners who sit on the board of the UN-backed Principles for Responsible Investment (PRI) are issuing a statement today asking fellow institutional investors to acknowledge, as owners and clients of many of the institutions involved, some responsibility for the behaviours that led to the crisis and to work together to respond to it.

There are four priorities for action from institutional investors and our agents.

The first is to acknowledge how a flawed understanding of some complicated financial instruments put not only our immediate investments at risk, but also the wider global economy.

To remedy this, institutional investors need to exercise proper due diligence of the investment chain and enhance our capacity to research, understand and address the full range of risks and opportunities.

This range includes environmental, social and corporate governance (ESG) issues, which can be material to the interests of beneficiaries and clients, and a thorough assessment of counterparty risk.

The accumulation of toxic assets, and unsustainable risk-taking, lay at the epicentre of this financial earthquake and these are the sorts of issues a more holistic approach to investment research should detect.

We should also consider how to encourage the fund managers, asset consultants, brokers and research providers they work with to ensure those agencies can also address ESG issues.

The second priority for investors is to consistently monitor companies and ensure risks are managed properly.

Collectively, we need to put greater resources into shareholder engagements.

More active ownership enhances accountability and should reduce the need for one-size-fits-all regulatory responses. There is no doubt that properly managed regulation, both hard and soft, with proper oversight, will be an important part of building well-functioning markets. However, regulation alone is not enough. Investors must take it upon themselves to ensure assets are managed in the best interests of end beneficiaries and clients. Where investors are restricted from exercising such shareholder rights they should engage actively with governments and market authorities.

The third priority is to tackle the lack of transparency that was such a major contributor to the severity of the crisis.

As active owners, investors should work with investee companies to ensure comprehensive and systematic disclosure of the information they need in order to make responsible investment decisions. Ensuring the disclosure of information on ESG and other issues will enhance investors’ understanding of their underlying investments and avoid a repeat of recent mistakes.

When it comes to transparency investors must also practice what they preach. We should publicly disclose the measures we are taking to respond to the crisis and our responsible investment activities in general.

Finally, if we are to address the problems facing the economy then investors must adopt a collaborative approach. Many of the problems, particularly around systemic issues, are too great for any investor to tackle on their own.

That is an ambitious agenda. However many institutional investors are already responding to the crisis using the Principles for Responsible Investment Initiative as a robust framework for action.

I invite all institutional investors to consider becoming signatories to the PRI and join a global network of peers working to address these priorities.

I am going to expose some inconvenient truths about pension investments and tell you all about the pension gambles that have gone sour.

One of the signatories of the Principles for Responsible Investment (PRI) is the Caisse de dépôt et placement du Québec. Today, its former president, Henri-Paul Rousseau said that the Caisse's difficulties were due to events beyond his control:

Henri-Paul Rousseau strode to his own defence Monday, insisting the fruits of his nearly six-year reign at the Caisse de dépôt et placement du Québec left the pension fund manager so flush it can easily ride out a prolonged market downturn.But his rosy portrayal of his own management of the Caisse, delivered before an overflowing crowd that included dozens of Montreal business elites, failed to quell widespread criticism in Quebec that the heady returns earned by the pension fund manager in previous years masked a risky investment policy with flaws that became punishingly apparent when markets crashed.

The Caisse, Canada's biggest institutional investor, posted a minus-25-per-cent return in 2008, equivalent to a $39.8-billion loss – far underperforming the median return of minus-18.4-per-cent at large Canadian pension funds. But Mr. Rousseau said he is not to blame for that.

Mr. Rousseau, who quit the Caisse in mid-2008 only months into his second five-year mandate, attributed the bulk of the pension fund manager's difficulties to events beyond his control that arose after his departure. His sudden move to a senior job at Power Corp. of Canada came before the global market meltdown left the Caisse scrambling to unwind billions of dollars in derivatives contracts and sell stocks to generate quick cash.

“No diversification policy or risk management policy on earth can protect you from that kind of synchronized effect, which happened for the first time in 80 years,” he told more than 700 people who paid up to $95 to hear his version of the Caisse debacle.

“The financial history of 2008 was essentially written five months after I left. I don't believe I am trying to escape my own responsibility by pointing this out.”

The hour-long speech – broadcast live on Quebec's all news channels – was a major happening in Quebec, where the fortunes of the Caisse are closely monitored by politicians and the public. The institution, which saw its net assets slide to $120-billion as of Dec. 31, manages the assets of more than two dozen provincial pension and insurance funds, led by the Quebec Pension Plan.

Mr. Rousseau's decision to plead his own case follows weeks of public debate about the Caisse and wrangling between the governing Liberals and opposition parties regarding parliamentary hearings into the 2008 debacle. Groups representing retirees have also called for a public inquiry.

There has been palpable anger about management of the province's so-called “nest egg” and immediate reaction to Mr. Rousseau's speech suggests it is not about to dissipate.

Pressed later by reporters, however, Mr. Rousseau said he had nothing to apologize for. “I won't take responsibility for the [global] financial crisis.” He also expressed doubts about the usefulness of a public inquiry. “What they'd find would be essentially what I've just said [in the speech] – whether [the inquiry] is public, private or extraterrestrial.”

Mr. Rousseau chalked up the Caisse's dismal 2008 performance to two major factors: strict accounting rules that forced the Caisse to write down the book value of its real estate assets, even though they continue to generate strong revenue, and a currency hedging policy that he actually deemed to be more conservative than the one followed by most other pension funds.

Mr. Rousseau criticized so-called mark-to-market accounting rules that forced the Caisse to slash the value of its real estate holdings by 30 per cent, though hundreds of its properties will see rents increase this year.

And though Mr. Rousseau took “full responsibility” for the Caisse's decision to invest $13.2-billion in now highly devalued non-bank asset-backed commercial paper, he minimized its impact on the Caisse's overall results. The $3.9-billion writedown taken in 2008 on the Caisse's remaining $12.8-billion in non-bank ABCP, he stressed, represented only 10 per cent of the Caisse's overall losses last year.

On top of that, he blamed the mid-2007 breakdown of the domestic non-bank ABCP market on a “small exception” in Canada regarding the lack of enforceability of liquidity guarantees provided by banks. And whereas central banks around the world rushed to support their own ABCP markets, he noted that the Bank of Canada stood on the sidelines.

That froze more than $32-billion in toxic paper on the books of the Caisse and other investors. Half of the paper is held by Quebec-based institutions, an anomaly Mr. Rousseau dismissed as “one of life's mysteries.” Mr. Rousseau also called on the Bank of Canada to add non-bank ABCP to its list of eligible securities under the central bank's sale and repurchase policy. The move would inject $15-billion into financial markets and free up institutions such as the Caisse to invest the funds elsewhere.

The Caisse has taken a total of $6-billion in provisions against its non-bank ABCP. But Mr. Rousseau expressed confidence that its actual losses on the paper will come in well below that figure. Besides, he added, superior returns during his tenure left the Caisse with a $15-billion cushion over what it would have earned had it only matched its historical performance.

Mr. Rousseau should run for public office. If that wasn't a 'Clintonian confession' of what went wrong at the "Basket Caisse", I don't know what is. Jay Bryan of the Montreal Gazette is right, all he did was offer a series of half-truths.

Moreover, Diane Urquhart reminded me of something much more important tonight:

The three dozen families who own more than $1 million of the toxic ABCP lost their right to sue in the courts for remedy of their damages due to the Caisse being a dominant player in this market and the ABCP Companies' Creditors Arrangement Act court proceedings.

Henri Rousseau, former CEO of the Caisse, simply gets to say he made a mistake and walks away from the ABCP fiasco with his Caisse severance and bonuses intact. We cannot say this for the lost life savings of these hardworking contributing families stuck with the damages Henri Rousseau left in his wake.

Hopefully, the Investment Industry Regulatory Organization of Canada, the Ontario Securities Commission and Quebec's L'Autorite des marche financiers will correct this clear injustice by facilitating a securities industry settlement for the lost lifesavings of these three dozen families, who were entitled to rely on suitable money market products offered by their securities dealers.

Diane knows exactly what is at stake here. Behind those big multi-billion dollar pension funds are millions of anxious workers who worked all their lives to retire in dignity and security.

Little did they know that those entrusted with their life savings are placing huge bets on what Michael Hudson refers to as Casino Capitalism backed up by a kleptocratic class:

Michael wrote that article back in September and has since written many excellent articles, including his most recent, The Language of Looting, where he explores the nationalization of American banks in great detail.The financial machines that placed the trades that bankrupted A.I.G. were programmed by financial managers to act with the speed of light in conducting electronic trades often lasting only a few seconds each, millions of times a day. Only a machine could calculate mathematical probabilities factored in regarding the squiggles up and down of interest rates, exchange rates and stock and bonds prices - and prices for packaged mortgages. And the latter packages increasingly took the form of junk mortgages, pretending to be payable debts but in reality empty flak.

The machines employed by hedge funds in particular have given a new meaning to Casino Capitalism. That was long applied to speculators playing the stock market. It meant making cross bets, lose some and win some - and getting the government to bail out the non-payers. The twist in the past two weeks' turmoil is that the winners cannot collect on their bets unless the government pays the debts that the losers are unable to cover with their own money.

One would have thought that this requires some degree of control over the government. The activity probably never should have been licensed. In fact, it never was licensed, and hence nor regulated. But there seemed to be a good reason: Investors in hedge funds had to sign a paper saying that they were rich enough to afford to lose their money on this financial gambling. Your average mom and pop investors were not permitted to participate. Despite the high rewards that millions of tiny trades generated, they were deemed too risky for the uninitiated lacking trust funds to play with.A hedge fund does not make money by producing goods and services. It does not advance funds to buy real assets or even lend money. It borrows huge sums to leverage its bet with nearly free credit. Its managers are not industrial engineers but mathematicians who program computers to make cross-bets or "straddles" on which way interest rates, currency exchange rates, stock or bond prices may move - or the prices for packaged bank mortgages. The packaged loans may be sound or they may be junk. It doesn't matter. All that matters is making money in a marketplace where most trades last only a few seconds. What creates the gains is the price fibrillation - volatility.

This kind of transaction may make fortunes, but it is not "wealth creation" in the form that most people recognize. Before the Black-Scholes mathematical formula for calculating the value of hedge bets, this kind of put and call option was too costly to provide much profit to anyone except the brokerage houses. But the combination of powerful computers and the "innovation" of almost free credit and free access to the financial gambling tables has made possible a frenetic back-and-forth maneuvering.

So why has the Treasury found it necessary to enter this picture at all? Why should these gamblers be bailed out, if they had enough to lose without having to become public wards by going on welfare? Hedge fund trading was limited to the very rich, for investment banks and other institutional investors.

But it became one of the easiest ways to make money, loaning funds at interest for people to pay out of their computer-driven cross-trades. And almost as fast as it was made, this revenue was paid out in commissions, salaries and annual bonuses reminiscent of America's Gilded Age in the years prior to World War I - years before the income tax was introduced in 1913. The remarkable thing about all this money was that its recipients didn't even have to pay normal income tax on it. The government let them call it "capital gains," which meant that the money was taxed at only a fraction of the rate that incomes were taxed.

The pretense, of course, is that all this frenetic trading creates real "capital." It certainly does not do so in the classical 19th-century concept of capital. The term has been decoupled from producing goods and services, hiring wage labor or from financing innovation. It is as much "capital" as the right to conduct a lottery and collect the winnings from the hopes of the losers. But then, casinos from Las Vegas to riverboats have become a major "growth industry," muddying the language of capital, growth and wealth itself.

For the gaming tables to be closed and the money paid out, the losers must be bailed out - Fannie Mae, Freddie Mac, A.I.G. and who knows what to come? This is the only way to solve the problem of how companies that already have paid out their revenue to their managers and stockholders instead of putting it in reserves are to collect their winnings from insolvent debtors and insurance companies. These losers also have paid out their income to their financial managers and insiders (along with the usual patriotic contributions to the political candidates on the key committees in charge of deciding the nation's financial structuring).

This has to be orchestrated well in advance. It is necessary to buy politicians and give them a plausible cover story (or at least a well-crafted set of poll-tested euphemisms) to explain to voters just why it was in the public interest to bail out gamblers. Good rhetoric is needed to explain why the government should let them go into a casino and let them keep all their winnings while using public funds to make good on the losses of their counterparties.

What happened on September 18-19 took years of preparation, capped by a faux ideology crafted by public-relations think tanks to be broadcast under emergency conditions to panic Congress - and voters - right before the presidential election. This seems to be our September election surprise.

Under staged crisis conditions, Pres. Bush and Treasury Secretary Paulson are now calling for the country to come together in a War on Defaulting Homeowners. This is said to be the only hope to "save the system." (What system is this? Not industrial capitalism, or even banking as we know it.) The largest transformation of America's financial system since the Great Depression has been compressed into just two weeks, starting with the doubling of America's national debt on September 7 with the nationalization of Fannie Mae and Freddie Mac. (My computer's spellchecker will not permit me to use the euphemism "conservatorship" that Mr. Paulson applied to bailing out the Fannie Mae and Freddie Mac fraudsters.)

Economic theory used to explain that profits and interest were a return for calculated risk. But today, the name of the game is capital gains and computerized gambling on the direction of interest rates, foreign currencies and stock prices - and when bad bets are made, bailouts are the calculated economic return for campaign contributions.

But this is not supposed to be the time to talk of such things. "We must act now to protect our nation's economic health from serious risk," intoned Pres. Bush on September 19. What he meant was that the White House must make the Republican Party's largest group of campaign contributors whole - Wall Street, that is - by bailing out their bad gambles. "There will be ample opportunity to debate the origins of this problem. Now is the time to solve it."

In other words, don't make this an election issue. "In our nation's history there have been moments that require us to come together across party lines to address major challenges. This is such a moment." Right before the presidential election! The same guff was heard earlier on Friday morning from Sec. Paulson: "Our economic health requires that we work together for prompt, bipartisan action." The broadcasters said that half a trillion dollars was discussed for this day's maneuverings.

Much of the blame should go to the Clinton Administration for leading the call to repeal Glass-Steagall in 1999, letting the banks merge with casinos. Or rather, the casinos have absorbed the banks. That is what has put the savings of Americans at risk.But does this really mean that the only solution is to re-inflate the real estate market? The Paulson-Bernanke plan is to enable the banks to sell off the homes of five million home mortgage debtors faced with default or foreclosure this year! Homeowners with "exploding adjustable-rate mortgages" will lose their homes, but the Fed will pump enough credit into the mortgage-lending agencies to enable new buyers to go deeply enough into debt to take the junk mortgages off the hands of the gamblers who presently own them. Time for another financial and real estate bubble to bail out the junk mortgage lenders and packagers.

America has entered into a new war - a War to Save Computerized Derivative Traders. Like the Iraq war, it is based largely on fictions and entered into under seeming emergency conditions - to which the solution has little relation to the underlying cause of the problems. On financial security grounds the government is to make good on the collateralized debt obligations packaged (CDOs) that Warren Buffett has called "weapons of mass financial destruction."

Hardly by surprise, this giveaway of public money is being handled by the same group that warned the country so piously about weapons of mass destruction in Iraq. Pres. Bush and Treasury Secretary Paulson have piously announced that this is no time for partisan disagreements over this shift of public policy to favor creditors rather than debtors. There is no time to make the biggest bailout in election history an election issue. Not an appropriate time to debate whether it is a good thing to re-inflate housing prices to a level that will continue to oblige new home buyers to go so deeply into debt that they must pay some 40 percent of their take-home pay on housing.

Remember when President Bush and Alan Greenspan informed the American people that there was no money left to pay Social Security (not to mention Medicare) because at some future date (a decade from now? 20 years? 40 years?) the system might run a deficit of what now seems to be merely a trivial trillion dollars spread over many, many years. The moral was that if we can't figure out how to pay, let's plow the program under right now.

Mr. Bush and Greenspan did have a helpful solution, of course. The Treasury could turn Social Security and medical insurance money over to Bear Stearns, Lehman Brothers and their brethren to invest at the "magic of compound interest."

What would have happened to U.S. Social Security had this been done? Perhaps we should view the past two weeks' events as having assigned to Wall Street gamblers all the money that has been set aside since the Greenspan Commission in 1983 shifted the tax burden onto FICA wage withholding. It is not retirees who are being rescued, but the Wall Street investors who signed papers saying that they could afford to lose their money. The Republican slogan this November should be "Gambling insurance, not health insurance."

This is not how the much-vaunted Road to Serfdom was mapped out to be. Frederick Hayek and his Chicago Boys insisted that serfdom would come from government planning and regulation. This view turned upside down the classical and Progressive Era reformers who depicted government as acting as society's brain, its steering mechanism to shape markets - and free them from income without playing a necessary role in production.

The theory of democracy rested on the assumption that voters would act in their self-interest. Market reformers made a kindred happy assumption that consumers, savers and investors would promote economic growth by acting with full knowledge and understanding of the dynamics at work.

But the Invisible Hand turned out to be accounting fraud, junk mortgage lending, insider dealing and a failure to relate the soaring debt overhead to the ability of debtors to pay - all of this mess seemingly legitimized by computerized trading models, and now blessed by the Treasury.

Having invested with some of the world's best hedge fund managers while working at public pension funds, I want to be very careful and not paint all hedge funds with the same brush. Any hedge fund that abuses leverage thinking they are bigger than the market inevitably blows up when positions go against them (think LTCM and Amaranth and I would add Freddie, Fannie and AIG to a long list of blow-ups).

But the best hedge funds try to consistently produce high risk-adjusted returns that are not correlated to any market. In financial lingo, this is what's called "pure alpha" - absolute returns that are not correlated to stock or bond markets (ie. "beta").

Pension funds know all about beta because they are highly exposed to equities:

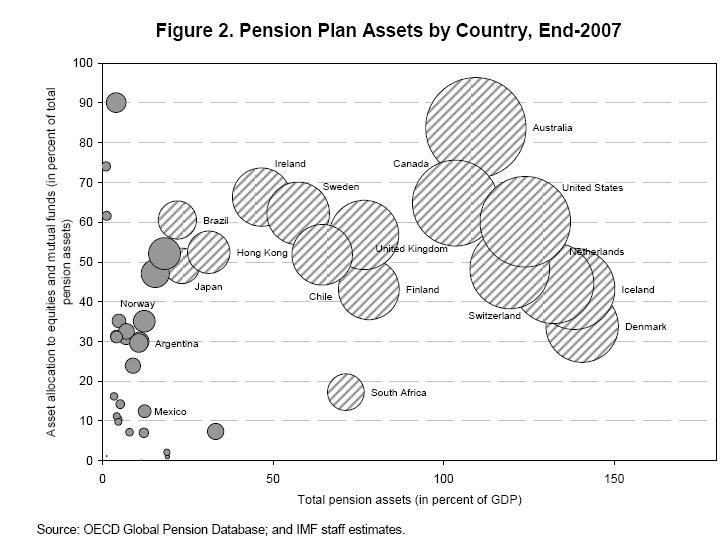

And what is the Pension Benefit Guaranty Corporation doing? As I wrote in my comment, Who Will Rescue Workers and Pensioners, the PBGC is "diversifying" away from stocks and bonds into alternative investments like hedge funds, private equity and real estate.One of the fiscal implications of the current financial crisis is the effect on funded pension plans in many OECD countries. Some of the countries’ pension fund portfolios have high exposure to equities and mutual funds. Many of the mutual funds in these countries are also heavily invested in equities.

The following diagram shows the Pension Plan Assets held by Country as of 2007 end (click to enlarge):

Source: IMF

Research Paper: The State of Public Finances: Outlook and Medium-Term Policies After the 2008 Crisis published March 6,2009

The stripped circles in the above figure shows that 16 countries have pension fund investments in equities and mutual funds greater than 10% of GDP. The countries with high exposure to stocks are Australia, the U.S., Canada, Iceland, The Netherlands, Switzerland, Denmark, and the U.K. Of the emerging market countries South Africa, Chile, and Brazil are more exposed. Countries such as Mexico, Argentina and Norway have limited exposure to the equity markets.

In the US, the asset base of pension plans for the various government workers is huge. At the end of October 2008, the $4 Trillion assets held by these plans had fallen by roughly $1 Trillion. As these plans are defined-benefit plans, the governments will make efforts to fill the gap in the future years either by raising the contributions from current employees or by raising taxes. However this does not affect the social security plan since those assets are not invested in the markets.

If employers go under taking the defined-pension plans with them, then the Federal agency Pension Benefit Guaranty Corporation (PBGC) guarantees payment to plan participants. However this creates a huge liability for the federal government.

According to a Mercer study in the US, the pension plans of the S&P 1500 companies have lost half a Trillion $ in 2008, of which 80% was lost in the last quarter.

The PBGC is basically following the same broken pension model that killed most pension funds. That, along with the bull that killed pension funds, is why we are facing the biggest pension crisis of the post-WWII period.

Why were pension funds so reckless in their investment decisions? How could they not have seen that they were contributing to systemic risk by shoveling billions of dollars into commodities, hedge funds, real estate, private equity, CDOs, etc.? What were they possibly thinking selling CDS just like AIG?

What infuriates me is that these so-called pension experts claim they did not see this crisis happening. They ignored the warnings of people like Nouriel Roubini, Robert Shiller, Dean Baker, and a host of others. All they had to do was recognize the securitization bubble that led to a common dominator of failure.

Instead, most pension fund managers were too busy shoveling billions into alternative investments - in what increasingly looks like a global Ponzi scheme - so they could easily beat their bogus benchmarks and then claim bogus alpha, allowing them to collect real bonuses to fatten up their wallets. As I have stated many times, when it comes to pension investments, It's All About the Benchmarks, Stupid!

They all wanted to be measured against Yale's yardstick and they all got decimated by Harvard's horror. And just like Harvard's endowment, the worst is yet to come:

Harvard officials have announced that they expect that the university's endowment will have dropped by 30 percent when the accounting for 2008 is done. But Steven M. Davidoff, a professor of law at the University of Connecticut, argues that the university may be in worse shape than it has so far conceded. In his view, the grimmest effects of the popping of the "education bubble" -- the unsustainable spending-and-investment strategies pursued at Harvard and elsewhere -- will unfold over the next few years.

The problem, argues Davidoff, a former corporate lawyer at the elite firm Shearman and Sterling, in a piece published on the New York Times's Dealbook, lies in the proportion of Harvard's endowment tied up in illiquid assets -- in private equity and real-estate, for example. That's money Harvard does not have immediate access to (doubly so in a bad economy). In 2007, Davidoff estimates, 26 percent, or $11.2 billion, of the endowment was illiquid, including $5.16 billion in private equity.

Not only has private equity taken a bigger hit than stocks, but many private-equity arrangements include a commitment for continued payments by investors. Harvard has in the neighborhood of $8 billion in payments committed to private equity through 2017, Davidoff estimates.

One possible result: a downward financial spiral. The proportion of Harvard's endowment that is illiquid could grow, through 2012, from roughly 25 percent to 40 to 44 percent. That will happen as Harvard uses its liquid holdings to meet its private-equity obligations (which will compete with academic needs). And the growing portion of the endowment that is basically untouchable will magnify the strain caused by low or negative returns from the rest of the endowment.

It's complicated stuff, but the implications are clear, if Davidoff's assumptions hold: scaled-back plans and across-the-board austerity -- on a campus that once had money to burn -- as the education bubble goes pop.

It's not just the education bubble that popped. The whole "alpha bubble" popped, ending the great pension con job and bringing about an alternative investment nightmare that continues to haunt pension funds.

The end result of this reckless collective behavior will be an era of deflation unlike anything we have ever seen before. By the way, with the exception of South Korea and Turkey who escaped the carnage by allocating a high proportion of their assets in government bonds, most pension funds are not prepared for a protracted period of deflation.

The tragedy in all of this is that most workers who contribute to their pension plans are not being properly informed about the risks pension funds managers are taking with their contributions. Only when disaster strikes do the masses get agitated and become concerned.

It's time we clear the pensions fog once and for all, ensuring that our pension funds follow the highest possible governance standards based on full transparency, clear accountability and open communication with all stakeholders.

Pension funds need to become part of the solution, but to do this they first need to clean up their own house and stop gambling away the life savings of millions of hard working people who can't afford to bet their retirement on Casino Capitalism.

Comments

Post a Comment