Charles Emond on CDPQ's Big Push Into Europe and the UK

One of Canada’s largest pension fund managers has unveiled plans for a C$15bn ($12bn) spending spree on private assets in the UK and Europe in a significant expansion of its efforts to drive up returns offshore.

Caisse de Dépôt et Placement du Québec (CDPQ), the C$400bn global investment group, told the Financial Times that it plans to deploy around those funds to the region over the next four years, with the UK standing out because of its “pro business” stance.

The investment manager’s allocation to Europe stands at roughly 14 per cent of its international portfolio and is “concentrated in the UK and France,” Charles Emond, president and chief executive of CDPQ, told the Financial Times in an interview.

“We anticipate growing this figure in the coming years mainly due to opportunities we see across Europe for private investments in our sectors of expertise and interest, including financial services, financial technology, private credit, infrastructure, real estate, healthcare and the energy transition,” Emond said.

CDPQ, which invests on behalf of pension and insurance plans with millions of members and policyholders, said it will continue to invest in the UK and France, but was also “looking closely” at other European countries such as Germany, Spain and those in the Nordic region. Over six months to the end of June this year CDPQ posted a return of 5.6 per cent, above its benchmark index’s 4.4 per cent return.

As part of its plans to bolster its European portfolio, the group expects to boost the size of its London team from 40 to up to 70 over the next year and a half. “Europe generally provides opportunities but the UK (with C$22bn of investments) is at the centre of all of that,” added Emond.

CDPQ revealed its European ambitions as cash-strapped governments around the world court foreign capital in an effort to tap finance for infrastructure programmes and fund their switch to low carbon economies.

Emond was one of dozens of global asset management leaders who attended a UK government investment summit in London last week hosted by Boris Johnson, prime minister. “I must say I was impressed with the sales pitch,” said Emond. “They really stand out as pro-business.”

He added: “I think the UK is positioning itself as a leader in sustainability and sustainable investment.”

CDPQ is also one of the biggest investors in the world in renewables, such as wind farms and solar power — areas the UK and other governments see as prime targets for private investment.

In September, CDPQ announced plans to accelerate its climate strategy by taking measures including offloading oil producers from its portfolio by the end of 2022 and holding C$54bn of green assets by 2025.

Emond said it was getting harder to find green assets at a good price: “ESG inflows is record on record, so buying existing renewable assets you are paying through the nose,” he said.

Similarly, he said infrastructure was “a crowded space” with supersized institutional investors, including Australian and Dutch pension funds, vying for the same deals. Around C$150bn of the C$400bn portfolio is in assets that do not trade on public exchanges including private equity, real estate and infrastructure.

As part of its global investment ambitions, CDPQ also plans to increase its exposure to China from around 4 per cent of its overall portfolio at present to 5 to 10 per cent in the years to come. Around three-quarters of that slice is in public equities, with smaller allocations to private equity and real estate.

China is under increasing focus over its human rights record, but Emond said the investment could square with the fund’s ESG principles. “I understand and acknowledge the broader social issues but the reality is there’s [a] way to make responsible investing in China in some companies but you have to be selective,” he said.

A decade ago the fund was two-thirds invested in Canada and a third the rest of the world, with that proportion now flipped and “we are continuing on that trend because you have to be diversified”.

“There is much capital chasing the same assets. You got to be smart about what you buy where you buy.”

Excellent interview with Charles Emond, CDPQ's President and CEO.

A few things struck me from this interview.

First, what a total shift on Europe from his predecessor, Michael Sabia, who was once quoted as stating this:

“There’s a dark night going on in Europe, a dark and foggy night where bad things come out of trees and bite you. It’s a pretty scary place. In Europe there are investments to be made, and I think it’s possible to be successful there but there’s no place in the world, other than maybe emerging markets, where the word selectivity is fundamentally important.”

To be fair, that was back in 2013 and scars of the European credit crisis were still fresh.

I can't blame Sabia for being very cautious on Europe back then.

Since then, things have changed for the better. Yes, we had Brexit and the pandemic but fundamentals in Europe seem a lot better these days.

Still, there are challenges. In a recent blog comment, Alfred Kammer of the IMF discusses Europe’s post-pandemic economic challenges:

We project that fiscal deficits of key advanced European economies will decline by around 4 percentage points of GDP in 2022, a far larger pivot than the one that followed the global financial crisis. This pivot mainly represents an unwinding of pandemic-related support, with only a part of the resources reallocated toward stimulating hiring and investment. Its impact on growth in 2022 would only be countered to a limited extent by that of disbursements of Next Generation EU funds in support of EU countries’ post-COVID recovery and resiliency plans. The assumption is that private demand has strengthened sufficiently to offset the reduction in government stimulus, driving the European economy along a smooth recovery rather than off a fiscal cliff.

Bringing back jobs

Yet risks abound. To be clear, the concern here is not that governments would sit tight if there were new virus waves or other major shocks. Rather, it is that growth in advanced economies settles at a paltry 1 percent or less toward the end of 2022 rather than the 2–3 percent rates that we are currently projecting. Fiscal policy is not able turn on a dime. And central banks would not be well placed to help, given that policy rates are already about as low as they can go. Every quarter of delay in achieving full employment will then add to the challenge of bringing people back into jobs. The issue is much less of a concern for emerging European economies, mainly because they deployed less stimulus and enjoy higher potential growth rates. Nevertheless, they would suffer from reduced demand for their exports from their advanced European counterparts.

Higher inflation, on the other hand, has been largely driven by forces that can be expected to fade over time. As during the 2010–11 recovery from the global financial crisis, energy has been the biggest driver, largely reflecting the strong rebound of economic activity, which has returned oil prices to the range that prevailed during pre-COVID years.

Europe has met the COVID-19 pandemic with audacity and imagination and is enjoying a strong but bumpy economic recovery. It now faces two policy challenges: controlling inflation and dialing back fiscal support. While there is considerable uncertainty about inflation, central bankers have plenty of experience dealing with it and can deploy their tools quickly and flexibly. By contrast, unwinding the emergency spending measures governments undertook to support their economies is a major, complex endeavor. If policymakers get it wrong, they risk a repeat of the tepid growth that followed the global financial crisis of 2008.The recent surge in natural gas prices also reflects short-term factors—including dwindling inventories following a harsh winter and hot summer in 2021, shortages in renewables output in some places, and less supply. Adjusting for the energy-price “down and up” annual inflation rates computed over a 24-month horizon are close to pre-COVID ranges, as shown in the chart. This is the case even though supply-chain disruptions and associated bottlenecks are putting pressure on durable-goods prices, particularly as demand has bounced back quickly.

These supply-demand mismatches are expected to subside in the course of 2022 as consumption patterns normalize, inventories are restocked, and trade bottlenecks, in particular the supply of shipping containers, are resolved. Moreover, inflation in the euro area has also been driven by one-off factors, such as the expiration in Germany of a cut to the Value Added Tax enacted in January 2021.

Second-round effects

None of the factors now driving inflation would respond to changes in monetary policy. Rather, monetary policy would need to ensure that they don’t trigger a wage-price spiral. Fortunately, the risk of such second-round effects is limited in many advanced European economies, where labor-market slack remains significant. For example, we estimate that hours worked are still some 3 percent below pre-COVID levels. And at pre-crisis employment, central banks struggled with inflation that was too low, not too high. All of this is not to deny that there is considerable uncertainty surrounding the duration of shocks to prices and the precise amount of slack in advanced economies. But, all in all, our as well as analysts’ forecasts and market-based measures of inflation expectations suggest that the European Central Bank will again find it hard to achieve its medium-term objective of inflation around 2 percent.

In several emerging European economies, where output and employment are already close to pre-COVID levels, the ground for second-round effects is more fertile. Also, inflation expectations have begun to move up, and wages are likely to react more strongly as slack in the labor market continues to diminish. These economies have, rightly, started raising their policy rates toward levels preceding the pandemic. While watching carefully how wages evolve, even there central banks do not need to rush this process given the temporary element in inflation.

Maintaining momentum

In short, policymakers could easily find themselves in a situation that looks eerily similar to that of the early stages of the recovery from the global financial crisis more than a decade ago. There is a strong case for cutting very high fiscal deficits. But this will also require strong revenue growth and therefore strong activity, which could usefully be supported with additional transfers targeted at households in need, more spending on hiring incentives, and investment tax credits. Getting the pace of withdrawal of fiscal support exactly right will be tricky . Erring on the side of withdrawing too little fiscal support rather than too much seems the better course of action, especially in those economies with ample fiscal space, so as to guard against the risk of undercutting the momentum of the recovery.

Anyway, getting back to Charles Emond's FT interview, the focus will clearly be on the UK where CDPQ is expected to increase its team from 40 up to 70 but they are “looking closely” at other European countries such as Germany, Spain and countries in the Nordic region.

In terms of sectors, the areas of focus will be private investments in CDPQ's sectors of expertise and interest, including financial services, financial technology, private credit, infrastructure, real estate, healthcare and the energy transition.

Interestingly, Charles was quoted as stating: “I think the UK is positioning itself as a leader in sustainability and sustainable investment.”

I would agree with this and have publicly touted UK private equity firm Earth Capital but there are other excellent UK funds doing great work on sustainable investing.

What else caught my attention? Charles stating it was getting harder to find green assets at a good price: “ESG inflows is record on record, so buying existing renewable assets you are paying through the nose.”

Several people have told me this, including Jo Taylor, OTPP"s CEO who told me returns on wind and solar investments have come down considerably to low single digits.

Lastly, on China, there's definitely a balance going on there.

CDPQ and others need to partner up with the right partners there too in order to gain access to profitable investments across many areas, including renewable energy projects.

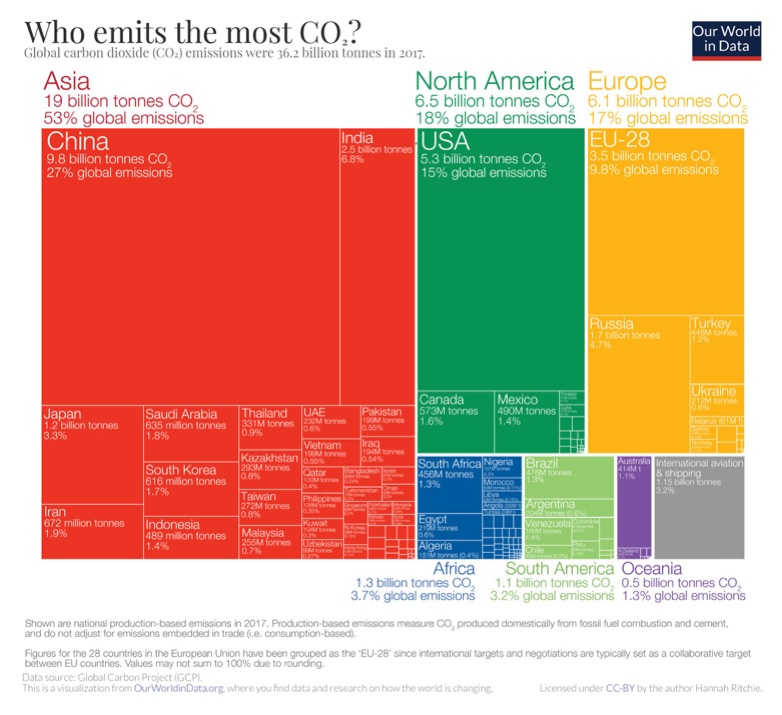

A friend of mine texted me two charts while I was writing this comment up:

Pretty eye-opening charts, you see that while China is a leader in renewable energy, it's still the worst CO2 emitter in the world by far.

There are tremendous challenges and opportunities in China and clearly the green economy there is a huge opportunity for CDPQ and other large Canadian pensions.

Alright, let me wrap it up by mentioning many current and former CDPQ employees were saddened to learn of Michel Nadeau's passing last week. He had a long stint at CDPQ which spanned almost two decades and will be remembered by many for his charisma, charm and intellect. CDPQ put out a press release here.

Below, Charles Emond (CDPQ) joins the FCLT Global podcast to discuss the organization's unique "double mandate" - providing long-term financial returns for depositors and providing constructive capital to Quebec's economy. Charles provides insight into CDPQ's latest climate investing initiatives, including a 60% reduction in the portfolio’s carbon intensity by 2030 and a new $10B transition envelope to decarbonize major carbon-emitting sectors.

Also, in a recent series, Gregory Perdon, Co-Chief Investment Officer at Arbuthnot Latham & Co. Limited, talks through the major players and how global events are predicted to affect the UK’s place in the global economy going forward.

Comments

Post a Comment