Stéphane Rolland of The Canadian Press reports Quebec's public pension fund reports loss of 5.6 % in 2022:

Quebec's public pension fund manager, the Caisse de dépôt et placement du Québec, reported a loss of 5.6 per cent in 2022 — a year marked by a simultaneous decrease in both stock and bond markets.

Net assets declined by $18 billion to $402 billion as of Dec. 31, according to the results released Thursday.

President

and CEO Charles Emond stressed that the first half of the year was

marked by the worst concurrent correction of stock and bond markets in

50 years.

"Facing this abnormal context, all our asset categories

succeeded in surpassing their indexes, even though there were very few

places to hide for investors."

Traditionally, bonds offer a

certain protection against stock market corrections in a diversified

portfolio, but the scale of interest rate hikes sent the bond market

downward last year.

The loss of 5.6 per cent is better than the 8.3 per cent decline in its benchmark portfolio, the Caisse noted.

Over

a period of five years, the Caisse had an annualized return of 5.8 per

cent. Over 10 years, the annualized return was eight per cent.

In

2022, the Caisse made $4 billion in new investments in Quebec. The total

value of its assets in Quebec reached $78.4 billion. Last December,

Emond announced a new goal of reaching $100 billion in Quebec assets by

2026.

The total cost for internal and external investment

management as of Dec. 31 decreased to 48 cents per $100 of average net

assets, or 0.48 per cent, down from 0.57 per cent.

Cool on cryptocurrencies

The

environment is going to become difficult for stock markets, predicted

Emond, who said rates will have to go up a bit more to contain stubborn

inflation, and there will be an economic slowdown.

"I had said that 2022 would be historically demanding. The year 2023 won't be very different."

Senior

vice-president and head of liquid markets Vincent Delisle said

investors are nursing hope that central banks will temper their ardour.

He said the market isn't ready to swallow the tough pill on offer from

central banks, and there's a risk the market will be a little

disappointed.

Emond also said the Caisse has given up on

cryptocurrencies after its misadventure with Celsius Network. The 2021

investment in a cryptocurrency interest and loan platform evaporated in

less than a year, swallowing $200 million.

"We won't do that again," Emond said when asked about how the Caisse will manage cryptocurrency risks in the future.

He

added that the Caisse has filed a legal complaint against the platform

for "false and misleading information" on its financial situation.

Mathieu Dion of Bloomberg News also reports Canada’s CDPQ is slammed by bond rout in worst year since 2008:

The historic bond market rout did not spare

the Caisse de Depot et Placement du Quebec, causing the pension manager

to post its worst results since the global financial crisis.

Canada’s second-largest public fund lost 5.6 per cent and saw net

assets fall to $402 billion (US$297 billion), down $18 billion from the

prior year. Its fixed-income portfolio was shredded by the rapid rise in

interest rates, falling almost 15 per cent.

The result would have been much worse if not for CDPQ’s holdings of

industrial property, infrastructure and private equity, all of which saw

gains. If the firm held a traditional portfolio of 60 per cent stocks

and 40 per cent bonds, assets would have plunged to $367 billion, Chief

Executive Officer Charles Emond said at a news conference.

CDPQ’s total return was its worst since 2008, but it outperformed a

mixed benchmark that was down 8.3 per cent, the firm said in a

statement.

Real estate and infrastructure investments were two of the brightest

spots, with the Caisse posting low double-digit gains in each. “Our

strategy now focuses on more logistics and more residential, and fewer

shopping centers and offices,” Emond said.

Public stocks were down 11.3 per cent — outperforming the S&P 500

— while private equity was up 2.8 per cent. CDPQ did not benefit from

the surge in energy stocks as it exited from oil production in 2021. The

fund reduced its exposure to the technology sector and increased its

holdings in more defensive segments such as insurance, pharmaceuticals

and telecommunications.

AZURE POWER

After writing off a US$150 million investment in bankrupt

cryptocurrency lender Celsius Network LLC last summer, the Caisse

stumbled with its majority stake in India’s Azure Power Global Ltd. The

renewable-energy firm has lost two-thirds of its value since the end of

August, when the new CEO stepped down and the company disclosed a

whistleblower complaint about possible “manipulation of project data and

information by certain employees.”

Rating agencies have downgraded Azure’s debt and the company still

hasn’t filed an annual report for the fiscal year that ended last March.

The Caisse holds a 56 per cent interest in the company.

“There are ongoing investigations. On the aspect of the situation

itself, as soon as the Caisse was informed, Azure did everything it had

to do,” Emond said.

“For us, we will not compromise on the governance or ethics of this

company. The next steps will be the conclusions of the investigation.

The story is not over. It is too early to talk about losses. Looking to

the future, all the options are on the table.”

Maiya Keidan of Reuters also reports, Canadian pension fund CDPQ posts first negative annual returns since financial crisis:

Canada's second-largest pension fund Caisse de dépôt et placement du

Québec (CDPQ) on Thursday reported investment losses and a drop in net

assets for 2022 as aggressive rate hikes led to turbulence across global

markets.

CDPQ's investments were down 5.6% for the year ended Dec. 31, compared with a 13.5% return for full-year 2021.

Central

banks across the world raised interest rates last year to tame

decades-high inflation, increasing the odds of a recession and hurting

returns for investors.

"The

year 2022 provided an environment filled with several challenges, with

spiking inflation, historic interest rate hikes by central banks and

rising geopolitical tensions," Chief Executive Officer Charles Emond

said.

Annual net assets plunged C$18 billion ($13.31 billion) year-over-year

to C$402 billion, resulting from falling values in fixed income that

experienced a sharp downturn due to the fastest monetary tightening seen

in decades.

CDPQ also took a hit

from the crypto winter due to its failed $150 million investment in

crypto firm Celsius, which filed for bankruptcy protection in July.

In August, CDPQ said it was exploring legal options and would no longer invest in crypto companies.

Last

month, the Bank of Canada became the first major central bank to say it

would hold off on further moves to let the effects of past hikes sink

in. The central bank over the past 11 months has lifted interest rates

at a record pace to 4.5% to curb inflation.

Earlier

this month, Canada Pension Plan Investments Board reported a rise in

its net assets in its third fiscal quarter of 2023, helped by gains in

private equity, real estate and credit investments.

Francis Vailles of La Presse also reports, Solid even when markets dip (translated from French):

This is the big question I was asking myself before D-Day: will the Caisse de dépôt's portfolio have been able to resist the bear market of 2022? Will he have done relatively well under the circumstances?

Why this question? Because the talent of a fund manager is not only assessed when the markets go up, but also when they go down. Since the famous debacle of 2008, when the Caisse had lost 25%, all the leaders of the Caisse had sworn that the portfolio had become more resilient, able to face the worst waves.

So what has finally transpired? The answer is definitely positive. Our collective woolen sock (bas de lain) lost some feathers during this extraordinary year 2022 when interest rates exploded higher, but it did significantly better than the stock and bond markets, and much better than its benchmark index.

For ordinary mortals, its negative return of 5.6%, or -24.6 billion, is anything but a good performance. But placed in the context where the stock market deflated by 8.7% in Canada and 18.1% in the United States, combined with a 16% drop in the American bond market, the performance of the Caisse becomes reassuring.

Better still: the managers achieved the 3rd best performance in the history of the Caisse if we compare it to its benchmark index, the one that tracks the same type of assets held by the Caisse, and which was -8.3% in 2022.

In short, this favorable difference of 2.7 percentage points between the Caisse's return (-5.6%) and that of its index (-8.3%) translates into added value of $10.4 billion. for depositors. Only the years 2010 and 2021 had done better.

Specifically, in 2021, the Caisse had obtained a return of 13.5% in a bull market, a difference of 2.8 points with its benchmark index, which was the second performance in its history.

"We are able to beat comparables in both bull and bear markets," Caisse CEO Charles Emond told reporters in the conference room.

Often, small savers are advised to put 60% of their portfolio in the stock market and 40% in the bond market, through balanced mutual funds or others. However, if the Fund had followed this breakdown in 2022, it would not have lost 5.6%, but 11.3%.

In short, the wallet has passed the test, so far.

What explains this good relative performance? Essentially, the Caisse's strong presence in the real estate, infrastructure and private equity markets. You will tell me that for these sectors, it is difficult to make a valid comparison with peers, to find solid benchmarks, unlike the stock market. Either.

Except that over five years, these distinct investment choices made by the Caisse in infrastructure and private placements maintain better returns than the benchmark. As for real estate, the gap has been favorable for two years, after the Caisse cleaned up its portfolio.

Another success of the Caisse: its investment decisions for the bond market, which caused it to lose 1.5 percentage points less than the benchmark, or 14.9% against 16.4%.

Lastly, its return on the stock markets (-11.3%) was similar to that of the benchmark, but this performance was achieved when the Caisse had exited from oil and gas, one of the only sectors to have resisted the collapse of 2022.

Speaking of oil and gas, many detractors have criticized the Caisse for its withdrawal from the oil sector and its firm commitment to the green economy. It's all well and good, the greenery, we heard, but not at the cost of seeing our pension funds amputated.

However, in response to this question from me, Charles Emond said that for five years, the Caisse has achieved a compound annual return of 20% with renewable energies, while the oil sector would have given 7%.

Readers will find me too soft on the Caisse, but it's hard to miss: in January, the institution was named "Fund of the Year 2022" by Global SWF, an organization that studies the activities of around 400 funds in the world.

Reason for this recognition: "for its impact on the development of Quebec, for its leadership with sovereign and public investors on a global scale, for its significant investment activity in 2022 and, more broadly, for its contribution to the industry advancement,” reads the SWF website.

Another distinction: the Fund ranked 1st out of 59 pension funds in 2022 for its contribution to sustainable finance.

I have been an ardent critic of the Caisse de depot for 20 years, and I remain so. The institution is making missteps, as seen with Celsius, Azure Power Global and Otera Capital, and the media must pick up on them. I dare to believe that these media criticisms, in fact, contribute to making our Caisse better.

The fact remains that the retirement funds of teachers, nurses, construction employees, certain municipal officials and all workers (via the Quebec Pension Plan) are in good hands, after all. Should we stop saying it?

The bet of La Presse Affaires

Every year, the journalists of La Presse Affaires try to predict the result of the Caisse de dépôt the day before its publication. The winner this year? Martin Vallières, who had predicted a negative return of 5.5%, or 0.1 point less than the performance of the Fund (-5.6%). Honorable mentions to Jean-Philippe Décarie (-5.9%) and Nathaëlle Morissette (-5%). Yours truly was among the pessimists (-8.8%) and the 17 people who took part in the game had an average of -3.6%.

I would like to take part in that prediction game because I predict OTPP (despite FTX due diligence disaster, lazily relying on Sequoia Capital) and OMERS will deliver the best results among Canada's Maple Eight for calendar year 2022 (HOOPP is a wildcard, it might pull off top spot, not counting them out!).

Before I tell you where Francis Vailles of La Presse got it wrong, especially on Fixed Income, let me first go over CDPQ's press release going over its 2022 results (Francis Vailles, Gérald Fillion and I should go for lunch at Milos on OSBL’s tab and I will set them straight on "la magouille à la Caisse"):

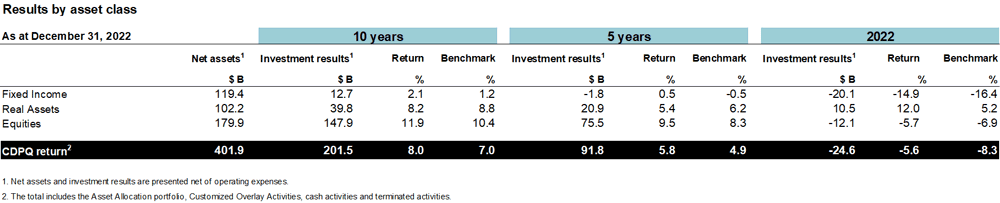

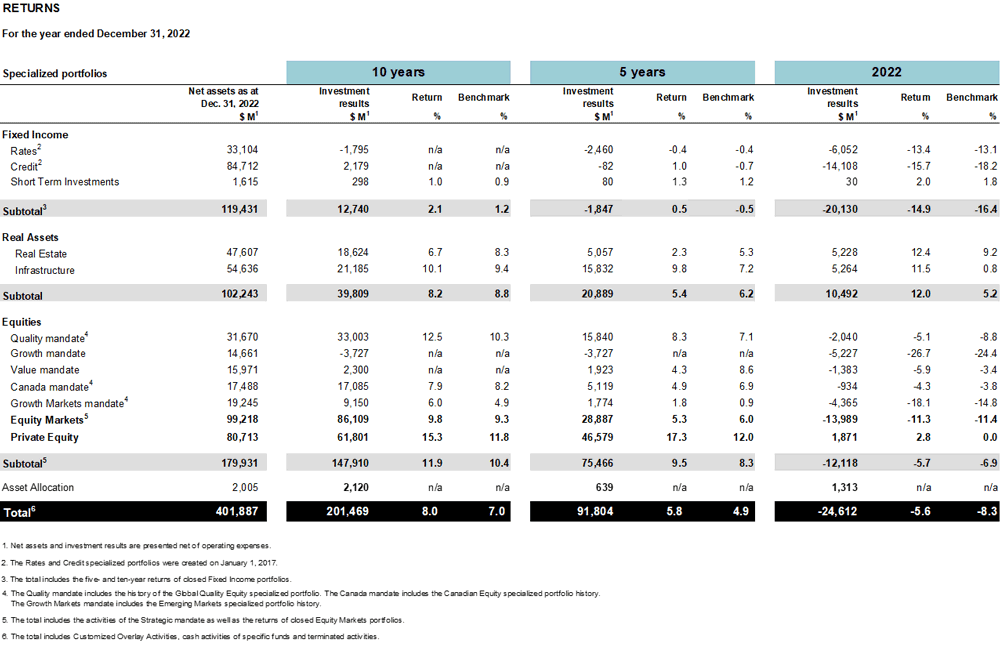

CDPQ today presented its financial results for the year ended December 31, 2022. The weighted-average return on its depositors’ funds was -5.6% in 2022, compared with -8.3% for the benchmark portfolio, representing over $10 billion in value added. Over five years, the annualized return was 5.8%, above the 4.9% of the benchmark portfolio and producing nearly $18 billion in value added. Over ten years, the annualized return was 8.0%, also higher than its benchmark portfolio which stood at 7.0%, generating $30 billion in value added. As at December 31, 2022, CDPQ’s net assets totalled $402 billion.

CDPQ manages the funds of 48 depositors and the one-, five- and ten-year returns presented as at December 31,

2022, represent the weighted average of these funds. Each CDPQ

depositor has its own investment horizon and tolerance for risk. As

such, their results vary based on their investment policies, which

evolve over time. In 2022, the spread in the returns for

CDPQ’s eight main depositors was especially wide, ranging from -3.9% to

-8.0% for one year, all above their respective benchmarks.

“The year 2022 provided an environment filled with several

challenges, with spiking inflation, historic interest rate hikes by

central banks and rising geopolitical tensions. The first half of the

year was marked by the worst concurrent correction in the stock and bond

markets in 50 years, which posted negative returns from

-10% to -30%. In this unusual context, and with few places for investors

to hide, all of our asset classes outpaced their respective indexes,” explained Charles Emond, President and Chief Executive Officer of CDPQ.

“For a second straight year, but in strongly contrasting market

environments, we outperformed our benchmark portfolio. The strategic

initiatives we undertook in recent years and our disciplined execution

created value added performance for our clients. These two factors

combined with our sound diversification strategy position us well for

what may come up next, as the sharp volatility—that we are still

witnessing today—could persist for some time,” he added.

Return highlights and achievements

The worst simultaneous correction of the stock and bond markets in 50 years affected CDPQ’s portfolio in 2022.

Accordingly, the $18-billion decrease in CDPQ’s net assets largely

results from falling values in Fixed Income, a class that experienced a

sharp downturn due to the fastest monetary tightening seen in decades.

In addition, while the flagship indexes of the major stock markets

experienced a severe correction, the Equities class also posted a

negative return, but resisted better given the preponderance of Quality

stocks in the Equity Markets portfolio and the good operational

performance of companies held in Private Equity. Activities in Real

Estate and Infrastructure performed very well against rising inflation.

Investment results for CDPQ are $91.8 billion over five years and $201.5 billion over ten years.

Fixed Income: The class absorbs the biggest impact

in light of historic interest rate hikes, but still outperforms its

benchmark index due to credit activities

The cycle of rate increases was particularly rapid in 2022.

The reopening of the economy, global conflicts, including the war in

Ukraine, and persistent supply chain and labour market issues prompted

central banks to sharply increase interest rates to slow down the

historic rise in inflation. This rattled market expectations: in the

United States, the Federal Reserve increased its target rate from 0.25% to 4.5% during the year 2022, even though it had planned an increase to only 1.0% following its December 2021

forecast. In this context, CDPQ recorded a -14.9% one-year return in

Fixed Income, above its benchmark index’s -16.4%. The higher duration in

the Fixed Income portfolios, which allows for better diversification

and better matching with depositor liabilities, was favourable in recent

years, but affected 2022 performance in an environment of rising rates.

The $2.3 billion in value added generated in 2022

stems from all credit mandates, particularly Sovereign Credit and

Corporate Credit. The Fixed Income class posted an annualized five-year

return of 0.5%, above its benchmark index’s -0.5%. All five credit mandates also contributed to this performance.

Furthermore, the 2022 market environment presented a good number of

opportunities at attractive entry rates, and the teams made more than

$15 billion in private credit investments and commitments.

Included among them, in Infrastructure Financing, was a stake in a loan

of USD 400 million to Fundamental Renewables, a U.S. lender focused on clean energy projects. With its contribution to EUR 485 million

in financing, CDPQ also supported KKR & Co.’s acquisition of

Albioma SA, a French energy producer that aims to end coal use by 2025.

This is also the first transaction for CDPQ’s $10-billion transition

envelope dedicated to decarbonizing the heaviest-emitting sectors. In

Corporate Credit, we note a loan to support the growth of Eqwal, a

network of orthotics offices in France. In addition, in Real Estate

Debt, CDPQ’s subsidiary Otéra Capital continued to deploy in the United

States through a loan as part of USD 675 million

in total financing granted for the construction of the highest tower in

Texas, a mixed-use real estate project that is aiming for LEED Gold and

WELL Bronze certifications, among others.

Real Assets: Excellent performance by the Real Estate and Infrastructure portfolios despite inflation

The one-year return of the Real Assets class, which includes the Real Estate and Infrastructure portfolios, was 12.0%, well above the 5.2%

of its benchmark index. The class also demonstrated its diversifying

role, which limited inflation’s impact on the total portfolio. Over five

years, the annualized return was 5.4%, below its index’s 6.2%, due to the impact of the pandemic on the Real Estate portfolio at the beginning of 2020, particularly in the shopping centres sector. The Infrastructure portfolio continued to perform well over the period.

Real Estate

For one year, the Real Estate portfolio recorded a return of 12.4%, significantly above its benchmark index’s 9.2%, driven by the CDPQ real estate subsidiary’s repositioning in 2020

toward more promising sectors, including logistics. The residential

sector also contributed positively to performance, while the office

sector continues to undergo a significant transformation. Over five

years, the annualized return was 2.3%, below the index’s

5.3%, due to the historic prevalence of shopping centres in the

portfolio, which now represent its smallest sector.

During the year, the Ivanhoé Cambridge teams were active, with over 70 acquisitions and sales totalling $15 billion,

in sectors aligned with its strategic repositioning. For example, in

Australia, the real estate subsidiary partnered with Scape in an

investment of nearly AUD 1 billion in the

student housing sector. In Germany, Ivanhoé Cambridge concluded a

strategic partnership with NVELOP, a logistics real estate specialist,

on two transactions totalling over one million square feet. Lastly,

Ivanhoé Cambridge invested in Cohabs, a Brussels-based company

specialized in coliving in Europe and the United States.

Infrastructure

The Infrastructure portfolio posted a one-year return of 11.5%, strongly outpacing its benchmark index, which posted 0.8%.The difference represents over $4 billion

in value added and can be explained by the good performance of

transportation and renewable energy assets. Over five years, the

portfolio produced an annualized return of 9.8%, above its benchmark portfolio, which stood at 7.2%. This performance results from the portfolio’s exposure to growth sectors, particularly renewable energy.

In 2022, the Infrastructure team continued to rigorously deploy in a fiercely competitive market for quality assets. It made $10 billion

in new investments and commitments, and expanded its global reach.

Among them is a first investment in Japan, in Shizen Energy, a renewable

energy leader in the country, that could ultimately total USD 474 million.

In Europe, CDPQ also enhanced its positioning in sustainable mobility

with the acquisition of Akiem, the leading provider of locomotive

leasing services in the region. In Latin America, CDPQ acquired the

power transmission network of Terna in Brazil, Peru and Uruguay for over

EUR 265 million, marking the creation of a

CDPQ platform dedicated to electricity transmission on the continent.

Lastly, CDPQ invested USD 2.5 billion

alongside longstanding partner DP World in port infrastructure in the

United Arab Emirates that is well positioned to benefit from global

trade routes and supply chains.

Equities: A class that resists better, with a return above the benchmarks in an atypical and volatile year

The Equities asset class, which includes the Equity Markets and

Private Equity portfolios, generated a one-year return of -5.7%, above

its benchmark portfolio of -6.9%. Over five years, the annualized return

was 9.5%, also above the benchmark’s 8.3%, with over $10 billion

in value added, resulting from the robust performance of Private Equity

over the period and the resilience of stocks in the Quality mandate,

the largest in Equity Markets.

Equity Markets

In 2022, stock markets experienced a strong correction and showed

unusual volatility. In fact, the post-pandemic upsurge in inflation,

accelerated cycle of interest rate hikes and amplified geopolitical

tensions caused stock markets to shed value after reaching record highs

at the end of 2021. For example, the flagship U.S. S&P 500 index posted -18% in local currency in 2022.

In this extremely demanding environment, the Equity Markets

portfolio’s return was -11.3%, just above its benchmark index’s -11.4%,

despite the exit from oil production and the exclusion of the tobacco

industry, which are among the only sectors to have generated strongly

positive results during the year. Among the positive factors, we note

the portfolio’s focus on the quality of company fundamentals, with a

favourable positioning in more defensive segments such as insurance,

pharmaceuticals and telecommunications, as well as dynamic portfolio

management during the year. In contrast, growth and emerging market

stocks had a more challenging year. The 2022 performance influenced the five-year annualized return, which stood at 5.3%,

below the benchmark index’s 6.0%. The difference is due in part to the

portfolio’s low exposure to certain technology giants in the first half

of the five-year period, when their stocks soared.

Private Equity

The Private Equity sector held its own against the difficult market context. The portfolio recorded a 2.8% return in 2022, above its benchmark index, which posted a neutral return of 0%.

The difference is attributable in part to the growth of private company

earnings and advantageous positioning in the health care and insurance

sectors. Over five years, the portfolio produced an annualized return of 17.3%, higher than its benchmark portfolio’s 12.0% annualized return, generating nearly $14 billion

in value added. This performance also stems from the strategic themes

that comprise the portfolio, including the digitization of the economy,

health care and insurance, as well as the quality operational management

of assets, which is even more important in times of economic

uncertainty.

Québec: An active year in a slowing market, with an enhanced ambition of $100 billion in Québec assets by 2026

In 2022, CDPQ made $4.0 billion in new investments and commitments in Québec. Its total assets rose slightly to $78.4 billion, including $62.2 billion in the private sector, despite growing economic uncertainty that dampened the volume of transactions worldwide.

“In Québec, we continued to fully play our role, by executing

transactions in various sectors and for companies of all sizes, and by

fostering connections for our portfolio companies to help them grow here

and abroad. In addition, we announced our ambition to reach $100 billion in assets by 2026.

Globally, we’re the most active pension fund manager in our local

economy, and our presence significantly increased during the turbulent

period of the last few years. Every day, our teams are at work to

support Québec companies,” added Charles Emond.

Among the transactions this year are investments in large companies

such as Pomerleau, in which CDPQ made an additional investment of $150 million

to support this construction leader’s plan for growth across Canada. We

also note the acquisition, alongside equal partner Fonds de solidarité

FTQ, of a 65% stake in Nortera, previously called Bonduelle

Americas Long Life, which specializes in processing and selling

vegetables, thereby keeping the company’s headquarters in Brossard.

Additionally, CDPQ supported technology company Plusgrade in its

acquisition of the Points platform for USD 385 million, creating a new global ancillary revenue leader for the travel industry.

CDPQ was also active among Québec SMEs, investing $10 million in modular furniture retailer, Cozey, in a round of financing totalling $15 million,

to support its strategic development plan for the United States,

accelerate its growth in Canada and expand its product offering. Another

example is the investment in Bouthillette Parizeau, an engineering firm

with numerous projects that provide solutions to fight climate change.

Lastly, CDPQ invested in COREALIS Pharma, a Laval-based company that has

become a North American leader in its sector.

For the Réseau express métropolitain (REM), several key steps were

completed during the year, including finalizing infrastructure work and

the complete electrification of the South Shore branch. In addition,

dynamic testing was conducted to validate the functionality and

reliability of the systems in various conditions, including in adverse

winter conditions. The REM’s South Shore branch is scheduled for

commissioning in spring 2023.

Ivanhoé Cambridge continued to play an active role in Québec,

including through the creation of a Québec hub to ensure the global

management of the real estate subsidiary’s investments and projects

related to economic development in the different regions. In the

Capitale-Nationale region, it concluded a strategic partnership with

Douville, Moffet & Associés (DMA) for the redevelopment of the

Laurier Québec commercial property and the densification of the site,

including the acquisition by DMA of a share in three assets in the

region: Laurier Québec, Édifice Champlain and Tour Frontenac. In

Montréal, Ivanhoé Cambridge rolled out initiatives for the downtown’s

revitalization, including unveiling The Ring at Esplanade PVM. The real

estate subsidiary and its partners also invested close to $200 million

in Haleco, a unique project at the intersection of Old Montréal and

Griffintown, which stands out for its mixed-use approach (residential,

commercial and offices) and will include community housing to create a

quality neighbourhood catering to residents’ needs. The project also

plans to obtain LEED Platinum certification and incorporates a

low-energy design.

Internationally recognized expertise and sustainability approach

On January 1, 2023, CDPQ was named 2022 Fund of the Year by Global

SWF, a global reference that analyzes the activities of around 400 sovereign

wealth and public pension funds. CDPQ received this prestigious

recognition for its global leadership among investors, its sustained

investment activities in 2022, its contribution to Québec’s

economic development, and, more broadly, its contribution to advancing

its industry, notably on ESG matters.

Among other distinctions received during the year—and a sign of its

leadership in sustainable investing—CDPQ ranked first among the 59 main

pension funds in the World Benchmarking Alliance’s Financial System

Index. This international organization measures the private sector’s

contribution to achieving the U.N.’s Sustainable Development Goals and

published its first index in 2022 as part of COP27 in Egypt.

More details on CDPQ’s sustainable investing strategy, including its

progress on climate targets, the advancement of its commitments and

initiatives in terms of equity, diversity and inclusion, as well as

governance, will be presented in the Sustainable Investing Report

published in the spring.

Financial reporting

CDPQ incurs costs to conduct its activities, including operating

expenses, external management fees and transaction costs. As at December 31, 2022, the total cost for internal and external investment management is down from the prior year, standing at 48 cents per $100 of average net assets, compared with 57 cents per $100 of average net assets in 2021. CDPQ’s cost ratio compares favourably with that of its peers.

The credit rating agencies reaffirmed CDPQ’s investment-grade ratings

with a stable outlook, namely AAA (DBRS), AAA (S&P), Aaa (Moody’s)

and AAA (Fitch Ratings).

ABOUT CDPQ

At CDPQ, we invest constructively to generate sustainable returns

over the long term. As a global investment group managing funds for

public pension and insurance plans, we work alongside our partners to

build enterprises that drive performance and progress. We are active in

the major financial markets, private equity, infrastructure, real estate

and private debt. As at December 31, 2022, CDPQ’s net assets totalled CAD 402 billion. For more information, visit cdpq.com, follow us on Twitter or consult our Facebook or LinkedIn pages.

CDPQ is a registered trademark owned by Caisse de dépôt et placement du Québec and licensed for use by its subsidiaries.

Now, I was invited last Thursday to attend the results along with journalists but I was at Kinatex Rockland taking care of my sciatica, so I wasn't able to attend.

CDPQ's 2022 Results: Pension Pulse Analysis

Alright, enough on my ongoing sciatica issues, you really don't care, you're reading this comment because CDPQ is the first of the Maple Eight to report and you want my brutally honest opinions and analysis and I promise to state them below:

First, overall results were actually very good given the terrible first half of the year last year where both stocks and bonds got clobbered hard. In fact, according to the latest survey from RBC Investor & Treasury Services (I&TS), Canadian defined benefit (DB) pension plans posted hard-hitting losses in 2022 despite a positive final quarter, losing 10.3% in 2022. The reason? Most Canadian DB plans do not have the expertise to manage assets internally and they certainly aren't invested globally in private markets like real estate, infrastructure and private equity and if they are, they're paying big fees and generating mediocre returns. So trust me when I tell you CDPQ's 5.6% loss while it sounds huge in dollars, was actually relatively good compared to average Canadian DB plan which was down 10.3% in 2022 as stocks and bonds got hit.

Second, while CDPQ's results are excellent relative to most Canadian peers, they're not going to beat OTPP and OMERS which both have a higher allocation to Private Markets. Also, as I stated two weeks ago when I covered CPP Investments' Fiscal Q3 results, according to my calculations, the CPP Fund's' calendar year result was -2.6% for 2022, but I also stated these figures are NOT official yet and subject to review (sources tell me that CPP Fund's calendar year results will likely be closer to CDPQ's once they finalize valuations in private markets).

Third, Global SWF recently named CDPQ 2022 fund of the year and conducted an interview with Chalres Emond, its President and CEO. I covered this here and explained why in my opinion, CDPQ is THE global leader in responsible investing and it has nothing to do with the fourth pillar of the climate strategy it unveiled last year -- ie, exiting out of oil production.

Fourth, the press release notes the weighted-average return on its depositors’ funds was -5.6% in 2022, compared with -8.3% for the benchmark portfolio, representing over $10 billion in value added and over five years, the annualized return was 5.8%, above the 4.9% of the benchmark portfolio and producing nearly $18 billion in value added and over ten years, the annualized return was 8.0%, also higher than its benchmark portfolio which stood at 7.0%, generating $30 billion in value added.

That last point is where things get tricky, very tricky! Francis Vailles of La Presse commends them and even notes:

Another success of the Caisse: its investment decisions for the bond

market, which caused it to lose 1.5 percentage points less than the

benchmark, or 14.9% against 16.4%.

This is where my BS detector went off, thinking of previous discussions I had with Simon Lamy who had a long stint as an extremely successful fixed income portfolio manager at CDPQ and was forced out for BS political reasons.

In my opinion, Simon Lamy, not Marc Cormier, should be the EVP and Head of Fixed Income at CDPQ, and if anyone has an issue with this, email me and I will set you straight, as the latter has been there far too long and doesn't have a good management style (for example, you do not force Brian Romanchuk, the greatest fixed income senior analyst CDPQ ever had to do stupid PowerPoint charts, that is a total waste of his talent, which is why he rightly resigned from the organization, he was fed up!).

Anyway, Simon and I used to hook up once a year for our annual lunch at Milos and he would always tell me, there are not that many ways to beat your index: either you take duration risk, credit risk, liquidity or illiquidity risk or leverage and directional risk.

It's obvious CDPQ didn't have the right duration calls but to be fair, I think the depositors (clients) choose their asset mix (which is stupid in my opinion).

If you look at OMERS which posted a net gain in 2022 of 4.2%, you'll note great performance of private markets (Private Equity and Real Estate posting gains of 13.7% and 13.6% respectively, and Infrastructure gaining 12.5%) and you'll also see Bonds (-3.8%) and Credit (3.4%) offset each other:

“Our significant allocations to private investments and focus on

short-term credit over long-term bonds protected OMERS from the worst

period of market losses incurred by investors since the 2008 global

financial crisis,” said Jonathan Simmons, OMERS Chief Financial and

Strategy Officer. “At the same time, investing sustainably continues to

be a priority and we have successfully lowered the carbon intensity of

our portfolio by 32% since 2019, exceeding our 2025 carbon reduction

target.”

Again, OMERS has 56% of its assets in Private Markets which has excellent assets and they realized a lot of gains, so it’s not fair to compare their overall results to CDPQ's (I suspect OTPP also did very well).

And they choose their asset mix, not the clients, which gives them more flexibility.

But the really important point is this, what is the benchmark governing the Fixed Income group at CDPQ and is it an appropriate one given according to their 2021 Annual Report, in 2021, CDPQ made investments and private credit commitments of close to $20 billion.

The 2022 Annual Report isn't available yet but the press reease notes:

Furthermore, the 2022 market environment presented a good number of

opportunities at attractive entry rates, and the teams made more than

$15 billion in private credit investments and commitments.

Included among them, in Infrastructure Financing, was a stake in a loan

of USD 400 million to Fundamental Renewables, a U.S. lender focused on clean energy projects. With its contribution to EUR 485 million

in financing, CDPQ also supported KKR & Co.’s acquisition of

Albioma SA, a French energy producer that aims to end coal use by 2025.

This is also the first transaction for CDPQ’s $10-billion transition

envelope dedicated to decarbonizing the heaviest-emitting sectors.

$20 billion in private credit in 2021 and another $15 billion in 2022, pretty soon you're talking about real money in private credit, an area that makes me extremely nervous!!

Who is underwriting all these loans and what percentage of unitranche loans are made up of second lien loans (20, 30, 40%?).

None of this is discussed by reporters because with all due respect, reporters aren't investment analysts and we can't expect them to really dig into benchmarks like yours truly.

That is my strength, when my BS detector goes off, I'm all over it like flies on bullshit!!

I looked at the RBC press release on how the average Canadian DB plan lost 10.3% last year and it stated this:

Canadian pensions had their largest annual fixed income decline in more

than 30 years, losing 16.8% over the 12-month period, compared to the

-11.7% return for the FTSE Canada Bond Index. As central banks enacted

restrictive monetary policy to tame surging inflation, yields rapidly

rose across the spectrum. The weakness spread across the market, but

inflation-sensitive, longer-duration bonds were the most affected. The

FTSE Canada Long Overall Bond Index declined 21.8%, while FTSE Canada

Short Overall Bonds were down 4.0%.

CDPQ's press release notes:

CDPQ recorded a -14.9% one-year return in Fixed Income, above its

benchmark index’s -16.4%. The higher duration in the Fixed Income

portfolios, which allows for better diversification and better matching

with depositor liabilities, was favourable in recent years, but affected

2022 performance in an environment of rising rates. The $2.3 billion in value added generated in 2022

stems from all credit mandates, particularly Sovereign Credit and

Corporate Credit. The Fixed Income class posted an annualized five-year

return of 0.5%, above its benchmark index’s -0.5%. All five credit mandates also contributed to this performance.

Furthermore, the 2022 market environment presented a good number of

opportunities at attractive entry rates, and the teams made more than

$15 billion in private credit investments and commitments.

Included among them, in Infrastructure Financing, was a stake in a loan

of USD 400 million to Fundamental Renewables, a U.S. lender focused on clean energy projects. With its contribution to EUR 485 million

in financing, CDPQ also supported KKR & Co.’s acquisition of

Albioma SA, a French energy producer that aims to end coal use by 2025.

This is also the first transaction for CDPQ’s $10-billion transition

envelope dedicated to decarbonizing the heaviest-emitting sectors. In

Corporate Credit, we note a loan to support the growth of Eqwal, a

network of orthotics offices in France. In addition, in Real Estate

Debt, CDPQ’s subsidiary Otéra Capital continued to deploy in the United

States through a loan as part of USD 675 million

in total financing granted for the construction of the highest tower in

Texas, a mixed-use real estate project that is aiming for LEED Gold and

WELL Bronze certifications, among others.

Again, beating the -14.9% loss in Fixed Income represents an 160 bps gain above its

benchmark index’s -16.4% but they took credit risk and liquidity risk in private debt to achieve those gains.

And they underperformed the -11.7% return for the FTSE Canada Bond Index so forgive me if I'm not terribly impressed with CDPQ's Fixed Income results both on an absolute and relative basis!

"Il y a de la magouille dans vos benchmarks les boys, et j'aime pas ca".

"Mais t'es qui toi calice de Kolivakis, siboire, ferme ta grosse gueule!".

Don't shoot the messenger, I am just stating what is painfully obvious, that Fixed Income benchmark does not represent the credit and illiquidity risks taken in that portfolio!!

And that Fixed Income portfolio represents 30% of CDPQ's total assets ($119B relative to $402B) so it's really important to figure out what percentage is private debt (my calculations 33%), how much second lien loans in those unitranche loans and does the Fixed Income benchmark represent all these risks adequately?

Francis Vailles of La Presse and Gérald Fillion of RDI Économie don't understand benchmarks and neither are they paid to understand, it's incumbent upon CDPQ and all of Canada's Maple 8 to explain benchmarks in clear English or French, osti de tabernak!!

I'm going to keep all you guys and gals running our venerable large pensions honest, because you're all going to get the same questions from me.

And I get it, you all want to make $2,$3,$4,$5 million or more in total compensation a year and bang out at least five to six good years (or more in Gordon Fyfe's case) and ride off into the sunset with a huge defined-benefit pension paying you $250,000, $500,000 or more a year and never look back.

I'd probably be doing the same thing in your shoes but like most hard working stiffs in Canada, I don't have this luxury.

From 2021 Annual Report, page 116 (2022 Report not available yet):

Worse still, I am routinely discriminated against by CDPQ, PSP and rest of Canada's Maple Eight when I've applied to hundreds of positions over the last ten years that I'm eminently qualified for and we all know, it's because I have multiple sclerosis and I'm a straight shooter (managing career risk was never my forté, obviously).

So please, you might be able to pull the wool over the eyes of reporters and even your board members, you will never pool wool over my eyes without my BS detector going off (this is why I will never make it on the Board of these large pension funds, they are all terrified of me).

Again, I'll say it in French, j'aime pas la magouille!!!

Don't play us for fools while you pay yourselves multi-million bonuses in good and bad times, it's unethical and wrong.

Look at Infrastructure where the press release states this:

The Infrastructure portfolio posted a one-year return of 11.5%, strongly outpacing its benchmark index, which posted 0.8%. The difference represents over $4 billion

in value added and can be explained by the good performance of

transportation and renewable energy assets. Over five years, the

portfolio produced an annualized return of 9.8%, above its benchmark portfolio, which stood at 7.2%. This performance results from the portfolio’s exposure to growth sectors, particularly renewable energy.

At least here I can honestly say Emmanuel Jaclot and his team are busy buying great assets all over the world, partnering up with world-class partners but what exactly is the Infrastructure benchmark and does it appropriately reflect the risks taken in the underlying portfolio?

And in Real Estate, you can read this in the press release:

For one year, the Real Estate portfolio recorded a return of 12.4%, significantly above its benchmark index’s 9.2%, driven by the CDPQ real estate subsidiary’s repositioning in 2020

toward more promising sectors, including logistics. The residential

sector also contributed positively to performance, while the office

sector continues to undergo a significant transformation. Over five

years, the annualized return was 2.3%, below the index’s

5.3%, due to the historic prevalence of shopping centres in the

portfolio, which now represent its smallest sector.

Clearly, Nathalie Palladitcheff and her team have done a wonderful job repositioning that portfolio into logistics in Europe, Asia and elsewhere but what is the RE benchmark and does it accurately reflect the risks being taken?

At least in Public Equities, you now what the benchmarks are, you can't screw around with them. In Private Equity, less so but it is based on public equity indexes:

Equity Markets

In 2022, stock markets experienced a strong correction and showed

unusual volatility. In fact, the post-pandemic upsurge in inflation,

accelerated cycle of interest rate hikes and amplified geopolitical

tensions caused stock markets to shed value after reaching record highs

at the end of 2021. For example, the flagship U.S. S&P 500 index posted -18% in local currency in 2022.

In this extremely demanding environment, the Equity Markets

portfolio’s return was -11.3%, just above its benchmark index’s -11.4%,

despite the exit from oil production and the exclusion of the tobacco

industry, which are among the only sectors to have generated strongly

positive results during the year. Among the positive factors, we note

the portfolio’s focus on the quality of company fundamentals, with a

favourable positioning in more defensive segments such as insurance,

pharmaceuticals and telecommunications, as well as dynamic portfolio

management during the year. In contrast, growth and emerging market

stocks had a more challenging year. The 2022 performance influenced the five-year annualized return, which stood at 5.3%,

below the benchmark index’s 6.0%. The difference is due in part to the

portfolio’s low exposure to certain technology giants in the first half

of the five-year period, when their stocks soared.

Private Equity

The Private Equity sector held its own against the difficult market context. The portfolio recorded a 2.8% return in 2022, above its benchmark index, which posted a neutral return of 0%.

The difference is attributable in part to the growth of private company

earnings and advantageous positioning in the health care and insurance

sectors. Over five years, the portfolio produced an annualized return of 17.3%, higher than its benchmark portfolio’s 12.0% annualized return, generating nearly $14 billion

in value added. This performance also stems from the strategic themes

that comprise the portfolio, including the digitization of the economy,

health care and insurance, as well as the quality operational management

of assets, which is even more important in times of economic

uncertainty.

I note Martin Longchamps took over Martin Laguerre as Head of Private Equity despite that portfolio's strong long-term results and Helen Beck, the former EVP and Head of Public Equity left the organization less than two years after being nominated to that position.

I kind of feel bad for Helen because CDPQ foolishly exited out of oil & gas but heard there were philosiphical differences between her and Vincent Deslisle, the Head of Liquid Markets who is doing a great job.

Who else left CDPQ? Alexandre Synett who was appointed Executive Vice-President and Chief Technology Officer back in June 2020.

It seem like he took the fall for CDPQ's investment in Celsius, the now bankrupt crypto firm.

Alexandre is a good guy and it's too bad he made this investment but between you and me, others were asleep at the wheel and this investment, just like OTPP's investment in FTX, should have never happened, ever (CPP Investments was right never to touch this garbage).

I met Alexandre once at his brother-in-law's house in TMR. His brother-in-law, Johnny, runs a very successful business buying used cars at auctions and dealers across Canada and selling them in the US, pocketing millions over the years.

Like me, Johnny has progressive MS but he's in worse shape and still manages to get up at the crack of dawn every day, six days a week, to work 18 hours a day running this business and his perseverance and stamina are incredible, he's a legend and everyone in the used car business knows him (I once spent a day with him going to an auction and dealers and was completely wiped out!).

Johnny is looking at getting into the Phase II stem cell trials for MS at the Tisch center in NYC, and I'm rooting for him and hope Alexandre is doing well too (very smart guy and a good guy too).

Also, I heard Ivanhoe Cambridge gave packages to several senior managers and is cleaning up house.

While I like Nathalie Palladitcheff and think she's doing a good job, I don't like how she is placing her own minions in positions there (mostly French from France) and is getting rid of experienced people Dan Fournier hired, people you need during a deep and prolonged global recession!!

That is a rookie mistake by an inexperienced CEO and she has to be careful, times are changing fast in real estate and the good years are definitely over!

Lastly, I did read out to Charles Emond last week and sent him questions Friday morning but his assistant told me later that afternoon he departed for his vacation with his family (it is a week off for Quebecers with kids in French schools).

Now, it's also possible Charles didn't like my questions because I touched a lot of these subjects (not all) above.

I want to make it clear, I think Charles and most of the senior execs at CDPQ are doing a great job, I'm just a stickler for transparency, especially on benchmarks. I went over the 2021 Annual Report and there's not much there in terms of a detailed explanation on benchmarks like they used to do back in my days.

I also want to invite Charles and Vincent Delisle for lunch at Milos and I'll bring along Fred Lecoq, Simon Lamy and Pierre-Philippe Ste-Marie and we can talk markets and an idea I have about starting an internal multi-strategy absolute return fund at CDPQ.

I can even invite my buddy from Toronto who trades currencies and Eric Girard, Quebec's Finance Minister, who used to run a macro fund at the National Bank.

It's very simple, with rates rising, the bogeys on external hedge funds should automatically go up and most of them are underperforming, charging hefty fees for this underperformance.

I'd like to know exactly how well CDPQ's external hedge funds did last year, as well as CPP Investments and OTPP, and know what fees were being charged.

I asked that question to Charles as well but he left on vacation and I wish him a great week off!

Oh, and before I forget, Charles and CDPQ's Board should have a closed door session with my buddy who used to work at CDPQ Infra to get solid advice on what to do with that organization now that the REM Ouest is almost completed.

There are a lot of things CDPQ's CEO has to worry about, a lot of moving parts and there's a political dimension ot this job as the organization has a dual mandate, to maximize returns without taking undue risks (whatever that means) and to invest in and promote Quebec's economy which Kim thomassin and her team are doing well.

Alright, let me wrap it up there, I'll coever OMERS' reuslts tomorrow as I got to speak with Blake and Jonathan earlier and asked a lot of questions.

Below, an interview in French with Charles Emond on RDI Economie where he went over 2022 results and more. Great interview, take the time to watch it and listen carefully to his comments.

And earlier last week, my favorite strategist Francois Trahan, was also interviewed by Gérald Fillion and painted a very dark picture of the US and global economy, stating the outlook is apocalyptic.

I couldn't agree more, get ready, 2023 and 2024 are going to be very grim years, you really need to be well prepared and well positioned with the right team, or else you'll regret it for years to come.

By the way, Trahan also sat down for a long-form

interview with Canadian media legend Stephan Bureau last week. This one

was also recorded in French and well worth listening to.

Update: On Monday, Warburg Pincus, a leading global growth investor, announced the appointment of Martin Laguerre

as a Senior Advisor working with its Capital Solutions, Financial

Services and Business Services groups. "Mr. Laguerre will support the

firm in identifying and evaluating new investment opportunities, while

leveraging his knowledge of the Canadian markets as well as his vast

sector expertise and decades of leadership experience."

I am glad Martin bounced back but wonder if this hire was similar to that of Macky Tall's appointment at Carlyle, namely, it was a backroom deal between CDPQ and a large investment firm they invest in.

Comments

Post a Comment