Carmen Reinicke and Hakyung Kim of CNBC report the Dow closes more than 100 points higher on Friday, but notches third straight week of losses on rate fears:

U.S. stocks were mixed on Friday as stubbornly high inflation and a rebound in rates continued to weigh on investor sentiment.

The Dow Jones Industrial Average rose 129.84 points, or 0.39% to end at 33,826.69. The 30-stock index rallied from lows of the day boosted by shares of Amgen and United Health, which gained 2.69% and 2.41% respectively.

The S&P 500 shed 0.28% to end the day at 4,079.09, and the Nasdaq Composite fell 0.58% to close at 11,787.27. Energy was the biggest laggard. Devon Energy dropped 4.29%, dragging down the S&P 500.

Yields on the 10-year and 2-year U.S. Treasury bonds hit levels not

seen since November, weighing on equities early in the session.

Stocks

are mixed on the week. The Dow ended down 0.13% for the week, its third

negative week in a row — a first since September. The S&P 500 has

shed 0.28% for the week, its second negative week in a row. The Nasdaq rose 0.59% on the week.

Investors

continue to worry about how the economy and equities will hold up as

the Federal Reserve hikes rates to tame stubbornly high inflation. In a Friday speech,

Federal Reserve Governor Michelle Bowman said there’s a long way to go

before the central bank reaches its target of 2% inflation.

“We

have been in a very contentious tug of war between the equity markets

and the Treasury markets,” said Art Hogan, chief market strategist at

B.Riley. While Treasurys are signaling that the Fed is going to hold

rates higher for longer, equities are not listening and instead looking

for a soft landing.

“Equity investors seem to be looking through a couple more rate hikes and looking forward to a pause,” he added.

The moves came after major averages shed more than 1% on Thursday, after the Labor Department said the producer price index — an inflation metric that tracks wholesale prices — rose 0.7% last month. That was more than economists expected.

Next week, investors will continue to watch earnings season for signs of consumer strength or weakness. Home Depot, Walmart and Etsy are scheduled to report results next week.

Noel Randewich of Reuters aslo reports S&P 500 ends down as investors fret about interest rates:

The S&P 500 ended lower on Friday, weighed down by Microsoft and Nvidia as investors worried that inflation and a strong U.S. economy could put the Federal Reserve on pace for more interest rate hikes.

The see-saw session on Wall Street followed economic data this week that pointed to elevated inflation, a tight job market and resilience in consumer spending, giving the Fed more room for to raise borrowing costs.

Goldman Sachs and Bank of America forecast three more rate hikes this year and by a quarter of a percentage point each, up from their previous estimate of two rate rises.

Traders are expecting at least two more rate increases and see the Fed rate peaking at 5.3% by July as central bank attempts to cool the economy and reduce inflation.

"A dark cloud has drifted over the stock market in the last two weeks based on a higher watermark for the Fed funds rate," said Jake Dollarhide, chief executive officer of Longbow Asset Management in Tulsa, Oklahoma.

"The jobs numbers aren't getting weaker, and it's hard to go into a recession with a strong labor market at the same time. That means the Fed could push the button and move rates higher," Dollarhide said.

Microsoft Corp (MFST) fell 1.6% and Nvidia (NVDA) dipped 2.8%, both weighing on the S&P 500 as the yield on 10-year Treasury notes hit a three-month high.

The CBOE Volatility index (.VIX), also known as Wall Street's fear gauge, traded above 20 points for a second session in a row.

Of the 11 S&P 500 sector indexes, six rose, led by consumer staples (XLP), up 1.29%, followed by a 1% gain in Utilities (XLU). Energy dropped 3.65%, with Exxon Mobil losing 3.8%.

The S&P 500 declined 0.28% to end the session at 4,079.09 points.

The Nasdaq fell 0.58% to 11,787.27 points, while Dow Jones Industrial Average rose 0.39% to 33,826.69 points.

For the week, the S&P 500 fell 0.3%, the Dow lost 0.1% and the Nasdaq climbed 0.6%.

The S&P 500 has gained about 6% so far in 2023, while the Nasdaq has rebounded about 13% following deep losses last year.

Adding to recent worries about monetary policy, Fed Governor Michelle Bowman said the central bank will need to keep raising interest rates until it makes much more progress tackling inflation. Richmond Fed President Thomas Barkin said the central bank still needs to raise interest rates, but that it could stick with quarter-point increases.

Moderna Inc (MRNA) fell 3.3% after its experimental messenger RNA-based influenza vaccine delivered mixed results in a study.

Deere & Co (DE) surged 7.5% after the world's largest farm equipment maker raised its annual profit and beat quarterly earnings expectations.

Lithium miners Livent Corp (LTHM), Albemarle Corp (ALB) and Piedmont Lithium Inc (PLL) slumped between 10% and 12% due to concerns about weakness in Chinese prices for the EV battery metal.

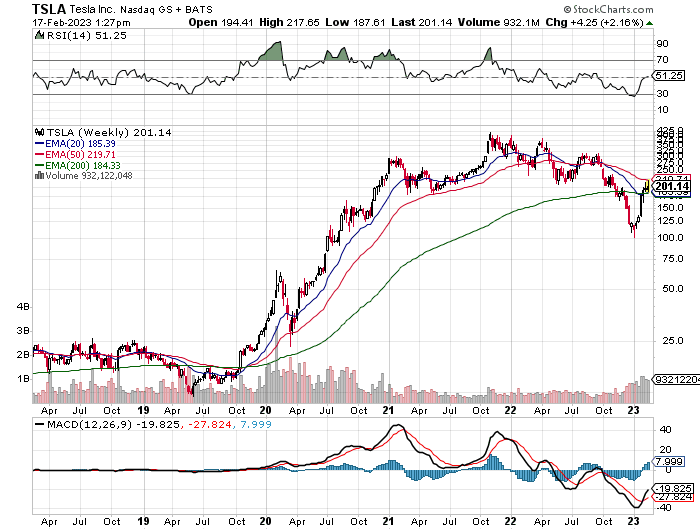

The most traded company in the S&P 500 was Tesla Inc , with $42.9 billion worth of shares exchanged during the session. The shares rose 3.10%.

U.S. stock markets will be closed on Monday on account of Presidents' Day.

Advancing issues outnumbered falling ones within the S&P 500 (SPX) by a 1.1-to-one ratio.

The S&P 500 posted eight new highs and one new low; the Nasdaq recorded 75 new highs and 68 new lows.

Volume on U.S. exchanges was relatively light, with 10.6 billion shares traded, compared with an average of 11.7 billion shares over the previous 20 sessions.

Before I get to what top funds bought and sold in Q4 2022, the macro backdrop is extremely important here.

Amazingly, the question of whether or not we will have a soft, hard or no landing is still out there.

David Randall of Reuters reports: What recession? Strong economy buoys US stocks, though Fed casts shadow:

Signs of strength in the U.S. economy have buoyed stocks in the face of rising Treasury yields and hawkish Federal Reserve expectations, though some investors believe the rally may be on borrowed time.

Stronger-than-expected reports on employment, retail sales and inflation have pushed up expectations for how much higher the Federal Reserve will need to raise rates and ignited a surge in Treasury yields - typically a negative development for stocks.

Yet the robust data has also dispelled fears of an impending recession that plagued Wall Street at the end of 2022, giving investors a reason to hold on to equities, at least for now. The S&P 500 is up 6.6% for the year-to-date, even as benchmark 10-year Treasury yields have risen nearly 50 basis points from their lows of the year.

Only 24% of global fund managers now expect a recession, down from 77% in November, a recent survey by BofA Global Research showed.

“Everyone came into the year thinking that there’s an imminent recession in the first half of 2023,” said Charlie McElligott, managing director, cross-asset strategy at Nomura Securities. “They got caught off guard because there’s much more resilient domestic and global growth.”

Yields vs stocks

Investors’ resolve can be seen in the resilience of the Nasdaq Composite Index, home to many of the tech and growth stocks that were particularly sensitive to higher yields last year, when it registered a 33% loss.

Based on historical regression, the Nasdaq should have sold off between 5% and 10% based on the increase in two-year yields since the Fed meeting earlier this month, according to a report from analysts at JPMorgan, including chief global markets strategist Marko Kolanovic. Instead, the index is up 0.3% over that time, and is up 13.3% for the year to date.

Some investors say the market’s resilience is unlikely to last much longer, especially if yields keep rising. Higher Treasury yields can weigh on stocks as they offer equities investment competition, increase companies borrowing costs and hurt valuations.

Many also believe that a recession has been delayed but not avoided. A severe downturn could await in the second half of the year, especially if rebounding inflation forces the Fed to keep rates at a higher level for longer to cool prices.

“The market in equities is just not appreciating that there will be more stepping on the brakes from the Fed and more earnings at risk of going lower,” said Torsten Slok, Chief Economist at Apollo Global Management. “Everyone wants to buy the dip in the stock market but the risk is that with inflation at 6.4% the Fed is just not done."

There are already signs that investors may be growing nervous over the economy’s strength. The S&P 500 dropped 1.4% on Thursday, helped in part by a stronger than expected U.S. producer price index reading.

Bearish investors also note other factors that tend to weigh on stocks have reared their heads in recent weeks. Real yields - which measure return on Treasury yields after inflation - have turned higher, taking the yield of the U.S. 10-year Treasury Inflation Protected Security near its highest level since early January. That can dull the allure of stocks, which are seen as far riskier than U.S. government bonds.

Rising yields have also arrested a decline in the U.S. dollar, which tumbled from a two-decade high in the latter half of 2022 but is now up nearly 3% from its low of the year against a basket of currencies. A stronger dollar tends to hurt the profits of U.S. multinationals and exporters.

In BoFA's survey, 66% of fund managers said the move in stocks, which began in October and has seen the S&P 500 rise 14% from that month's lows, was a bear market rally rather than a new bull market.

Still, some investors believe risks are tilted in favor of stocks, with the bulk of the Fed’s monetary policy tightening likely in the rearview mirror and valuations broadly lower after last year’s 19.4% selloff in the S&P 500.

Lara Reinhard, senior portfolio strategist at Janus Henderson Investors, is avoiding technology and growth stocks but focusing on shares of companies that pay out dividends as a hedge against inflation.

“We are starting at more normal valuations and in some cases cheaper valuations than in the last few years,” she said.

Meanwhile, stocks are getting strong support from retail investors, who pumped a record net average of $1.51 billion per day into U.S. stocks over the last month, according to Vanda Securities.

"Retail investors have plenty of dry powder in the form of capital parked in money market funds that could be deployed in the equity space once confidence about future market returns increases more broadly," the firm's analysts wrote.

Indeed, retail investors have been pouring record money into stocks and hedge funds are turning risk-on by gobbling up technology shares, after largely

missing out on the new-year rally in the stock-market’s biggest winners:

In the last month, retail investors poured an average of $1.51 billion per day into U.S. equities, the highest amount ever recorded: VandaTrack pic.twitter.com/rPRaLYcpcK

And

suddenly, strong growth and persistent inflation have investors

contemplating a new course for the economy in the coming year — a "no landing" scenario.

Essentially,

whether rapidly rising rates would quickly choke off economic growth

and inflation, or gradually slow growth and price increases. In other

words, would the Fed cause a recession, or just an economic slowdown?

The

newly-coined "no landing" outcome instead considers a scenario in which

inflation doesn't actually cool while economic growth continues, even

as interest rates remain elevated amid the Federal Reserve's attempts to

tamp prices down.

In the view of Apollo Global Management's chief economist, Torsten Sløk, there are growing signs of the market pricing in this outcome.

"In

other words, the market is saying that inflation will be significantly

higher in a year’s time than the Fed’s 2% inflation target," Sløk said

in a recent note. "Put differently, instead of expecting a recession and

lower inflation, short-term inflation expectations are rising and

becoming unanchored."

Sløk highlighted the recent pick-up in

one-year inflation breakevens, which are approaching 3% after the

aforementioned run of strong economic data in January, suggesting

investors are coming around to the idea of inflation remaining higher

for longer.

One-year

breakeven inflation expectations are rising and approaching 3%, driven

higher by the strong January employment report and yesterday’s CPI

report. (Source: Torsten Slok, Apollo)

But according to at least one economist, this narrative investors appear to be betting on is "nonsensical."

"Because

we're in this highly volatile environment, and because there is so much

uncertainty, we've now seen a number of different ways to interpret or

call what we're seeing in the economy,” EY Parthenon chief economist

Gregory Daco said in an interview.

A landing — however it may ultimately look — is going to happen eventually, in Daco's view.

The

economy operates in a cyclical pattern, growing until it reaches its

peak and then contracting before hitting a trough and rebounding again

into an expansion phase.

"No landing does not make any sense,

because it essentially means the economy continues to expand, and it's

part of an ongoing business cycle and it's not an event — it's just

ongoing growth," he added. "Doesn’t that entail that the Fed will have

to raise rates more, and doesn’t that increase the risk of a hard

landing?"

Federal

Reserve Chair Jerome Powell speaks at The Economic Club of Washington,

D.C., U.S, February 7, 2023. REUTERS/Amanda Andrade-Rhoades

Sløk

also indicated the no landing scenario would be likely to bring back

the volatile market action we saw in 2022 because it reintroduces

uncertainty about inflation and the Federal Reserve.

But the Federal Reserve hasn't exactly given reason for uncertainty: officials have consistently asserted for months that rates are likely to rise above 5%.

Federal Reserve Powell has said as much himself:

"There has been an expectation that [inflation] will go away quickly

and painlessly; I don’t think it’s guaranteed that's the base case," he

cautioned last Monday at the Economic Club of D.C. "It will take some

time."

And Sløk's own expectations for how the Federal Reserve

will handle this scenario align more with Daco's thinking than current

market pricing.

"The Fed will have to be more hawkish to ensure

that inflation expectations do not drift too far away from the FOMC’s 2%

inflation target," Slok said in a note.

Which suggests officials may in fact need to raise rates higher, increasing the risk of a "hard landing" in the end.

No doubt, as the Fed increases rates, the risks of a hard landing rise exponentially.

But as I keep warning here, the aggressive and swift increases in rates in the US and all over the developed world are already hurting cyclical sectors like housing and autos, and it's only a matter of time before it spreads to other industries and turns into a very nasty and prolonged global recession.

And while today's comment focuses on what top managers did in the stock market last quarter, the macro backdrop will increasingly dominate investment decisions.

In fact, the top performing hedge fund last year was Haidar Capital Management, a small fund that bet big on inflation, gaining 193% in 2022, earning it the top spot:

NEW: A small hedge fund’s bet on inflation generated a 193% return — one of last year’s biggest.

Generally speaking, last year was a great year for large macro funds.

Erin Ardvenlundof Pensions & Investments interviewed Ken Tropin who explained how Graham Capital posted double-digit gains in dismal 2022 by betting on hawkish Fed:

Macroeconomic hedge

funds aim to anticipate moves in financial markets, such as the

direction of interest rates, currencies, stocks, bonds and commodities,

and these funds were among the few to make money in 2022. Kenneth "Ken"

Tropin's hedge fund Graham Capital Management was among the winners.

The $18 billion hedge fund firm, based

in Rowayton, Conn., posted double-digit returns in 2022 net of fees in

its discretionary and quantitative macro funds. Graham's winning wager

was based on an early hawkish view on interest rates, as the firm

correctly forecast that the Federal Reserve and other central banks

would tighten faster and with more hikes than Wall Street expected.

About 65% of the assets are institutional investors.

Graham's five-largest global macro

funds are the Tactical Trend Series A fund, which gained 30.78% in 2022

and 3.31% in 2021; the Graham Quant Macro Series A, up 15.34% last year

compared with -1.57% in 2021; the K4D-15V fund, which gained 37% vs.

1.41% in 2021; the Absolute Return Series A, up 20.51% and 4.72%,

respectively; and the Prop Matrix fund, returning a 31.62% last year and

6.52% in 2021.

By comparison, the HFRI

Macro Total index returned 8.99% in 2022, according to HFR, the

research firm tracking the global hedge fund industry.

In an interview with Pensions & Investments,

Mr. Tropin shared what he sees for 2023, and what helped the firm's

positions last year. The conversation has been edited for length and

clarity.

Q: What's changed about the markets today?

A: If you look at 2010 to 2021, equities had an enormous return over

that 11-year period, largely fueled by stimulus from central banks, the

(Bank of England), the (European Central Bank) and the Fed. It was a

terrific time to be an investor in beta. You did well if you bought

every dip in the stock market. That changed a lot in 2022.

Q: Last year, you successfully predicted the Fed would hike more times and more quickly than everyone else on Wall Street. How?

A: In the second half of 2021, people thought the Fed would hike only 25

to 50 basis points in 2022. The Fed was still in QE mode. Then the Fed

realized inflation was getting way higher than they were comfortable

with, had to shift gears and delivered 350 basis points of hikes.

Our economists did a very good job of

moving from consensus forecast to hawkish. That was helpful to some of

our traders in shorting fixed income.

Q: Where do you see the fed funds rate this year or next?

A: The market thinks we will peak at

5.25% or something like that in September. A different question is: Will

we stay there a little longer than people would like? People were

expecting cuts in the last third of this year. Those expectations have

evaporated.

If you look at the start of the

hiking cycle, the Fed delivered 350 basis points of hikes instead of

100. The BOE, the ECB and Fed want to really be convinced that inflation

is lower than it is now.

Q : Can you explain the historical magnitude of 2022 rate hikes?

A: The best way to think about the

period July 2010 to July 2021 is that the ECB, BOE and Fed over 11 years

made 13 25-basis-point hikes. In 2022, we saw the equivalent of 40

25-basis-point hikes in one year by three central banks. That created a

really constructive backdrop for macro hedge funds and continues to be

interesting for what we do. We'll see a lot of volatility and a lot of

opportunity.

Q: Why did macro hedge funds outperform compared to other strategies last year?

A: We were fortunate and grateful to perform at a time where traditional

assets had a tough year. The traditional 60-40 portfolio had its worst

year since 1937. So to be able to achieve compelling results in an

environment that was not very good for our clients is gratifying for

sure.

Q: What are you hearing from pension funds and plans now?

A: Institutional investors are

interested in macro in the current environment. They're very realistic

that we may not have the results in '23 that we had in '22. But they

will be compelling enough for it to be a valuable allocation in the

portfolio. One reason: Macro funds aren't correlated to other hedge

funds or a 60-40 portfolio. If your macro manager does good risk

management and generates good returns, then it's very diversifying.

Q: How did your experience help, for instance, working at John W. Henry & Co.?

A: In 1982, I joined Dean Witter to

take over their fledgling hedge fund practice. I was there for seven

years. In 1989, I joined John W. Henry's firm as CEO and ran his firm

for four-and-a-half years. In 1993 we parted company and I was fortunate

in that I had a long relationship with the Paul Tudor Jones

organization, and he encouraged me to start my own hedge fund with him

as a strategic investor. In July 1994, I started with proprietary

capital, my own and Tudor's and we remain close friends to this day.

He's still an investor.

Q: Anything you are now do differently?

A: In the early days

of our industry, markets weren't as efficient. The trend-following

trading systems I invented in 1993 and 1994, they're still doing well,

and it's good for trend following. We want so many more sources of alpha

than just momentum-based trading. So we've worked really hard at

designing different ways of generating alpha than just momentum.

We began doing discretionary trading

in 1998, and today it's one-third of our assets, or just under $6

billion. We've also worked very hard at building fundamental quant

models that use other inputs, such as value, carry and fundamental data,

all those different signals. We have Graham Quant Macro, which has a

very nice returns and is about 60% to 70% correlated to trend following.

Q: What are you forecasting in energy, metals and currencies?

A: In '22, one highlight was the dollar got really strong. It rose 20%

to 25% against a basket of currencies. Right now the dollar's in a

little bit of a trading range. Rates in the U.S. are higher than

European rates. The perception in the market is that the Fed is going to

start cutting in the last third of this year. If that turns out not to

be true we may see some dollar strength again. But right now we're in a

trading range. Our positions in the dollar are just slightly long.

We're slightly long gold, but it's

been kind of unimpressive. If there was ever a year you wanted gold to

perform, it was last year when we had the highest inflation in 30 or 40

years. And gold went up a little. It's a bit of an underperformer.

Energy's come off a lot of highs in the third quarter, but I'm still favorably inclined to energy.

Our green policies on a global basis

are such that there's not a lot of oil and gas development in the U.S.

We need green policies, but it creates a constructive backdrop for

energy prices.

And some of the supply bottlenecks

will clear up, but they haven't yet. We did have a very warm winter in

Europe; that was helpful. I'm friendly toward the price of energy at

this time. Prices could move up 10% to 15% from here.

In 2022, we had rates go up quite a

bit, we were short fixed income, short equities and long the dollar and

commodities. So we did well. A strong combination of positions. Now

there continues to be volatility in all those markets. At the moment,

we're at fair value for the dollar but I think that will change.

Q: Why is Japan on your radar?

A: What's going on in Japan is, they

continue to cap on 10-year bonds at 50 basis points. A lot of people

think they'll have to capitulate and let interest rates move higher.

Their inflation is at a 40-year high. That's an interesting market to

keep an eye on. If the central bank capitulates, the Japanese bond, the

dollar-yen and the Nikkei would sell off.

Q: What's your warning to investors about U.S. equities?

A: I wouldn't be too confident as an

investor. We had 350 basis points of hikes last year and another 25-50

basis points this year. That's going to cause the economy to contract.

Equities aren't that far from their highs at the end of 2021. So maybe

we're 10% to 15% off the highs. But for example, the FTSE, the U.K.

market, is at its all-time high. That seems to me a mispricing if you

think the tightening by all three central banks simultaneously will

contract the global economy.

Q: Exogenous shocks might be more significant, then, such as China reopening? War with Taiwan? Dirty bomb in Ukraine?

A: It's all of those. The most

relevant one is what happens in Ukraine. We continue to see no

resolution that's obvious. You wonder how desperate Putin could get,

whether China continues to get more aggressive with the U.S. These are

low probability tail events. I don't predict any of these things. But I

also wouldn't be so complacent about them.

A more relevant question is: What

happens in the 2024 race for U.S. president? That to me right now could

have a profound effect on markets. Look at the effect on central bank

policy. The Fed tries to be neutral to who's in office. (Former

President Donald) Trump put a lot of pressure on (Fed Chairman Jerome)

Powell to cut rates. And he's a pro-business guy. Who knows if Trump

gets the nomination. But that's an example of how it could affect

markets we trade.

Q: If the GOP nominee wins the White House, what does that mean for markets?

A: It's too soon to

say. It's going to create uncertainty, which is helpful in that as a

macro manager, we like to see markets moving. And uncertainty is a

catalyst for that. If you're an interest-rate trader, and rate policy is

on hold, there's less to do, than when there are lot of hikes or cuts.

We can't say with confidence we get the move right. But the opportunity

set is profoundly greater when central banks are on the move.

Q: What's your take on markets like cryptocurrency that collapsed last year?

A: One concern I had...was crypto was

so volatile. I had a hard time understanding how it could be an

alternative currency when it had annual volatility off the charts. There

were a lot of aspects about the infrastructure I find interesting —

blockchain is a technology that has quite a bit of legs to it.

We trade crypto futures in a very

tiny way, with no impact on our performance. We don't have an edge in

crypto. I've learned if I don't have an edge, stay out.

Top level, investors over the last

decade or so have been very fortunate to have terrific returns from

traditional investments and hedge funds, and have outsized results

compared to previous market cycles, say, between 1990 and 2000, or even

the weak markets of 2000-2002. We just had an 11-year period, because of

all the stimulus, that was unusually good. Investors have to be more

sophisticated going forward. Macro is one of the opportunities for

investors to get a source of alpha that's typically uncorrelated to

equities and fixed income.

He's right, the last 11 years have been terrific, mostly because inflation was low and central banks kept lowering rates and engaging in QE, massively expanding their balance sheets to address the GFC and more recently, the pandemic.

That is all changing fast as central banks have embarked on a tightening campaign and QT, letting their balance sheets shrink by letting securities they purchased run their course, not adding more purchases.

And if rates stay higher for longer and QT continues, macro hedge funds will enjoy another boom decade.

Of course, if rates keep climbing as the Fed stays in tightening mode to stave off inflation, the risks are that it is overdoing it, slamming the breaks too hard, and something will break:

Fed tightening ‘always breaks something’: S&P 500 will drop to 3,800 by March, warn Bank of America strategists https://t.co/QPKY0yy9Rf

Moreover, I agree with Mohamed El-Erian, the Fed won't be able to bring inflation down to 2% without crushing the economy" but I don't agree with him when he says: “You need a higher stable inflation rate. Call it 3 to 4%.”.

The Fed won’t be able to get US inflation down to its 2% target without “crushing the economy:” said @elerianm told @FerroTV. “You need a higher stable inflation rate. Call it 3 to 4%.” https://t.co/wQBqBk1FBC

Nobody knows what will break but judging from past crises, when it breaks, it will break hard and markets will get clobbered more.

And the transmission mechanism from markets to the economy will only add fuel to the economic fire.

This transmission mechanism from markets to the real economy isn't well understood by economists, but it's real and typically hits credit markets first as rates rise:

Goldman: The proportion of corporate bonds in the iBoxx index of investment-grade debt that yield less than three-month Treasury bills spiked to 32% in early February. pic.twitter.com/BWjKhiq14r

And keep in mind, the leading indicators are already in contraction mode pointing to a hard landing ahead:

6-month annualized % change in Leading Economic Index from @Conferenceboard remains in negative territory (consistent with prior recessions) but hooked slightly higher in January to -7% (recent low was -7.7%) pic.twitter.com/2f48ViDkAe

Just as the lagging and coincident indicators rose 0.2% in January to new highs and are all the focus, the index of leading indicators dropped 0.3% and has declined now for 10 straight months, a 100% iron-clad recession forecaster. pic.twitter.com/AW6a9dkOkY

Clearly, these surveyed CEOs have no idea how strong and resilient the economy is, causing inflation to be sticky, which the Fed must bring to heal. pic.twitter.com/HFNXTvfzmI

And while short-term bonds are back, others are warnig we might be entering an era where the 60/40 could really fail you:

#Bonds are back. The gap between the yield on 6-month T-bills and the earnings yield on the S&P500 is closing. The last time it was this tight the #iPhone had yet to be released, frosted tips were a thing, and Destiny’s Child was topping the charts. pic.twitter.com/wtqSRzdGoF

The problem with 60/40 last year wasn’t so much the stocks — but the bonds. We expect stocks to tank sometimes. It’s why we expect them to pay us the big bucks long-term. But we don’t expect bonds to fall 18% in a year. So much for stability.

That’s been the big problem in previous lost decades. Bonds barely kept up with inflation in the 1960s, and they lost money in real terms in the 1940s and 1970s. Rising inflation leads to rising interest rates, and someone holding long-term bonds ends up a two-time loser. Their coupon payments are worth less and less in real terms. And they can’t take full advantage of new, higher interest rates because they are locked into old, lower rates.

They’d have been better off with cash — including, in investment terms, Treasury bills, savings accounts and money-market funds. Wall Street hates “cash” though, claiming that, despite its stability and liquidity, it offers terrible long-term returns. Clients are always being urged to swap their money from cash to products that actually generate fees — or as they say, “returns.” Investors are often told to “put that money to work.” But last year it went “to work” and took home a negative salary of 23%, as bonds, as well as stocks, did far worse last year than Treasury bills.

This is not a one-off. Actually, a modern Rip Van Winkle would have been better off leaving his money in Treasury bills than 10-year Treasury bonds for an astonishing 33 years last century, from 1949 to 1982. The difference wasn’t slight, either. Short-term bills generated twice the total returns over that period to bonds.

Warren Buffett has given instructions that after he dies his fortune should be invested mostly in stocks but with 10% in Treasury bills — not bonds. British financial consultant Andrew Smithers reached a similar recommendation when he did a very long-term analysis for his former Cambridge University college (which was founded in 1326, so we really are talking long-term). Cash, not bonds, offered a more reliable counterweight to stocks, Smithers found. His preferred alternative to 60/40 was 80/20: 80% stocks, 20% bills.

Meanwhile, Wall Street can stop pretending it doesn’t understand why 60/40 failed last year. It knows full well. Treasury bonds were almost guaranteed to fail sooner or later because they already locked in negative real, inflation-adjusted yields. At the start of 2022, a 10-year Treasury bond had a yield, or interest rate, of 1.5%. Not only was the Federal Reserve’s official long-term target 2%, but the actual inflation rate at the time was 7%, and the bond markets were expecting it to average 2.6% over the next decade. Inflation-protected Treasury bonds took the madness further: They locked in negative real interest rates. They were guaranteed to lose purchasing power over time.

The message to me is you can trade those Treasury bonds but don't buy and hold them unless you are certain inflation and rates have peaked.

And we really can't say for certain that a) inflation has peaked for good and b) rates have peaked for good.

As far as markets, an earnings recession is just getting underway and it will be a long and painful one, which is why I still maintain we are entering the brutally cold phase of the bear market.

So don't get carried away thinking the decent start to the year will keep on going, it most certainly won't:

Layoffs are gaining momentum and this is especially true in the Technology sector. Layoffs are just the inverse of the earnings outlook. S&P 500 Forward Earnings are now officially declining and interest rates tell us that this will likely continue for another two years. pic.twitter.com/4yb0OVa3xd

This is what a sentiment driven rally looks like! This is the S&P with Housing Starts which has historically been a tight fit ... until now. Folks that see this as the beginning of a new Bull Market should compare today with what occurred at the depths of the 2020 bear market. pic.twitter.com/XMiXKJzW79

Those of you praising China's economy reopening should be careful. Higher commodity prices take a few months to show up in U.S. inflation trends but that dynamic is in the pipeline. For a Fed that seems incapable of forecasting anything this could send the Dot Plot even higher. pic.twitter.com/cOR4M413oN

For those who don't enjoy daily whiplash from recession to expansion, by pundits who can't remember what they said :5 minutes ago - the recession in 2007 was backdated eight months before Lehman. Six months before the inflation peak.

Again, the macro backdrop is dismal, very dismal and the worst lies ahead, all you need to do is look at housing and how big investors are backing away:

The housing market has cooled so much that even deep-pocketed investors are backing off https://t.co/VvhQCxfZkX

So take the information below with a shaker of salt because most of these trades are over.

Top Funds Q4 Activity

I took a lot of time going into macro because it's by far the most important thing to understand as you sift through what Druckenmiller and company bought and sold last quarter.

David Randall and Carolina Mandl of Reuters report that 'Big Short' manager Burry, Farallon among hedge funds making bets on China:

"Big Short" investor Michael Burry, Farallon Capital Management, and Coatue Management were among the prominent hedge fund managers who took large bets on Chinese companies ahead of the reopening of the country's borders in January after nearly three years of restrictions, securities filings showed on Tuesday.

Burry, who came to fame ahead of the 2008 financial crisis by betting against U.S. real estate, added a new position of 75,000 shares in Chinese e-commerce company JD.com Inc (9618.HK) and a new position of 50,000 shares in Chinese tech giant Alibaba.com (9988.HK), filings show.

Burry was featured in the 2010 nonfiction book "The Big Short" by Michael Lewis which was made into a popular movie five years later.

Farallon, meanwhile, added 2,197,000 shares of Alibaba, while Coatue added 4,796,186 shares of Alibaba and 1,221,551 shares of JD.com.

The moves come as China's reopening has prompted record inflows into emerging market equities, according to data from Bank of America Global Research, and helped lift assets ranging from crude oil to European luxury goods makers in anticipation of a re-emergence of demand.

China began taking steps to end its zero-COVID policy, which was among the world's strictest anti-coronavirus regimes, in December. It officially reopened its borders in early January.

The SSE Composite index is up 6.6% for the year to date, slightly behind the 7.9% gain in the U.S. benchmark S&P 500.

Hedge fund managers' positions were revealed in 13F filings that show what fund managers owned at the end of the quarter. While they are backward-looking, these filings are one of the few public disclosures of hedge fund portfolios.

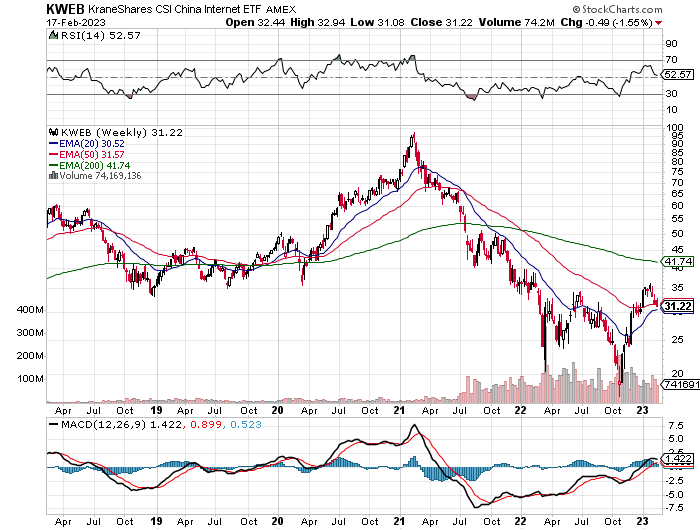

I wouldn't get too excited about Chinese large cap (FXI) or internet (KWEB) shares going forward, but they did pop nicely in Q4 and are worth monitoring:

Insider Monkey went over what some top funds did last quarter:

David Einhorn’s Greenlight Makes Changes to the Hedge Fund Positions (TipRanks) David Einhorn, Founder and President of Greenlight Capital

exited his stakes in Intel (INTC), Rivian Automotive (RIVN), and News

Corp. (NWS) in Q4, according to the hedge fund’s 13-F filing. The hedge

fund has opened new positions instead in Coya Therapeutics (COYA) with

1.13 million shares, Tenet Healthcare (THC) with 296,300 thousand

shares, and Funko (FNKO) with 234,300 thousand shares.

Why Billionaires Paul Tudor Jones and George Soros Bought Up Horizon (HZNP) Stock (Business Insider)

Two billionaires – Paul Tudor Jones and George Soros

— acquired shares of Horizon Therapeutics (NASDAQ:HZNP) stock, a

drugmaker, last quarter. On Dec. 12, Horizon agreed to be acquired by a

giant pharmaceutical company, Amgen (NASDAQ:AMGN). Jones and Soros’

Purchases of HZNP Stock: In the fourth quarter of 2022, Tudor Investment,

Paul Tudor Jones’ hedge fund, bought 648,600 of HZNP stock. The

purchase marked the first time the fund acquired shares in Horizon.

Family Offices Whiff on Tech Rally as Hedge Funds Get Boost (Bloomberg)

Money managers for the ultra-wealthy dumped beaten-down technology

stocks during the fourth quarter, right before the market rallied in

2023, while their hedge fund counterparts took a different tack. Both

Iconiq Capital and the investment firm for the Walton family’s fortune

sold shares of cloud-computing company Snowflake Inc., which surged 20%

this year through Tuesday after a steep slide in 2022. Stan Druckenmiller’s Duquesne Family Office also exited Microsoft Corp. and Amazon.com Inc. in the fourth quarter, according to a regulatory filing.

Billionaire George Soros Confirms Huge Bet on Tesla And Elon Musk (The Street)

The legendary financier continued to buy Tesla shares in the fourth

quarter despite the electric vehicle maker’s stock market rout. Elon

Musk asked a provocative question to George Soros

last month. The question was related to the way Soros uses his money

and indirectly about the numerous donations the legendary financier

makes. “Do you actually know where your money is going?” Musk said on

Jan. 16, referring to Soros.

‘Big Short’ Manager Burry, Farallon Among Hedge Funds Making Bets on China (Reuters)

“Big Short” investor Michael Burry, Farallon Capital Management, and Coatue Management

were among the prominent hedge fund managers who took large bets on

Chinese companies ahead of the reopening of the country’s borders in

January after nearly three years of restrictions, securities filings

showed on Tuesday. Burry, who came to fame ahead of the 2008 financial

crisis by betting against U.S. real estate, added a new position of

75,000 shares in Chinese e-commerce company JD.com Inc (9618.HK) and a

new position of 50,000 shares in Chinese tech giant Alibaba.com

(9988.HK), filings show.

Zero Hedge also did its usual summary of what hedge funds bought and sold last quarter:

A funny thing happened right before hibh-beta tech stocks set off on a

torrid, record-breaking January meltup: not only did hedge funds dump

most of these beleaguered names, they also shorted them in record quantities (something which we correctly predicted would

lead to the frenzied short squeeze that carried over into February),

and nobody took the wrong side of that trade more than family offices

for the ultra-wealthy, who as we learned in today's 13F barrage sold

tech stocks during the fourth quarter right before the market rallied in

2023.

Some examples: according to Bloomberg, both Iconiq

Capital and the investment firm for the Walton family’s fortune sold

shares of cloud-computing company Snowflake, which has surged 20% this

year after a steep slide in 2022. Stan Druckenmiller’s Duquesne Family

Office also exited Microsoft in the fourth quarter, right before the

tech giant gained 13% since the start of January, after falling 29% last

year. Druckenmiller also exited Amazon.com after initiating the

position in the third quarter; Glenview and Whale Rock also dumped the

stock. AMZN fell 50% in 2022 but is up 19% so far this year.

Not

everyone was selling, of course: some hedge funds, those who had been

forced to liquidate their tech holdings earlier, were smart enough to

dial up their bets on the sector in the fourth quarter. Lone Pine

Capital boosted its Microsoft stake by 23%. The stock was also the

biggest holding of Tiger Global Management (although whatever you do at

home kids, don't try to replicate anything Tiger Global does).

Meanwhile, like a true value investor, Seth Klarman’s Baupost Group more

than tripled its Amazon stake; while Tiger Cub Lone Pine boosted its

position by 44%.

That said, the iconic Druckenmiller didn't liquidate his entire tech

book and made at least one smart tech bet: Nvidia, which according to

Bloomberg now makes up about 4% of Duquesne’s $2 billion US equity

portfolio. Nvidia, seen as a benefactor of the rise of AI, has rallied

57% this year. It remains to be seen if Nvidia - which two years ago

soared when it was viewed as the benefactor of crypto mining - will also

crater once the AI craze is gone and when people tire of trying to

jailbrake the woke ChatGPT.

Here are some of the other findings from the latest volley of 13F reports, as compiled by Bloomberg:

Bonds

are back: Elliott and Soros Fund Management both disclosed positions in

corporate-bond exchange-traded funds during the fourth quarter. Elliott

disclosed a position in HYG, a high-yield corporate bond ETF. And Soros

Fund Management purchased about $255 million worth of LQD.

Glen

Kacher’s Light Street exited Tesla - right before the stock doubled -

and healthcare platform GoodRx Holdings Inc. The fund bought shares of

AMD valued at $22.3 million and Netflix Inc. valued at $19.3 million.

Harvard

University’s endowment is backtracking on educational services company

Laureate Education. After starting a position in the company last

quarter, it exited its entire stake, selling all 101,800 shares. The

school continued to increase its stake in Grab Holdings by about 40%,

snapping up $3.7 million more shares of the company, making it the

endowment’s fourth-largest US holding.

Yale University’s

endowment continued to increase its existing position in Procept

BioRobots after starting a position in the company last quarter. The

school also hit the reverse button on oil and gas company Riley

Exploration Permian after starting a new position last quarter. Yale

kept its two other holdings, in Vanguard and iShares ETFs, unchanged.

In

was a boring quarter for Berkshire which trimmed some of its financial

holdings, reducing its shares in U.S. Bancorp, Bank of New York Mellon

and Ally Financial; it also slashed its recent brand new stake in Taiwan

Semi (more here).

Einhorn's

Greenlight Capital added Tenet Healthcare to its disclosed investments

and exited Intel in the fourth quarter; it added to its holdings in

Kyndryl Holdings and decreased its stake in Resideo Technologies. Green

Brick Partners was the biggest holding, representing 28% of disclosed

assets

Soroban exited Yum! Brands Inc. from its disclosed

investments and boosted CSX Corp. in the fourth quarter, it also

decreased its stake in Lowe’s. CSX Corp. was the biggest holding,

representing 22% of disclosed assets.

Glenview added Universal

Health Services Class B to its disclosed investments and exited

Amazon.com Inc. It also decreased its stake in Aptiv Plc; Cigna Corp.

was the biggest holding, representing 15% of disclosed assets

Maverick

Capital’s 13F revealed a fund in turmoil: Tiger Cub Lee Ainslie added

122 new buys, though most of the new positions were small, and exited 90

previously established positions. His biggest addition was 1.4 million

shares in Catalent Inc., a company that provides delivery technologies

and development solutions for drugs, biologics and consumer health

products. The firm also started a new position Credo Technology,

snapping up 1.06 million shares. On the other hand, it liquidated its

entire stake in Carvana, selling 735,710 shares. Maverick lost around

30% last year.

Elliott Investment Management LP added IShares

iBoxx High Yield Corporate Bond ETF to its disclosed investments and

boosted Pinterest Inc. Class A in the fourth quarter, according to a 13F

analysis by Bloomberg.

Troubled crypto bank Silvergate, which

is also the most shorted Russell name with two thirds of the float

short, saw several brand name hedge funds open new positions in the 4th

quarter, at the same time as Soros Fund Management took a modest levered

bet in the form of SI puts (more here).

Icahn

Enterprises LP boosted Icahn Enterprises LP to its disclosed

investments and reduced Cheniere Energy in the fourth quarter; Icahn

Enterprises LP was the biggest holding, representing 70% of disclosed

assets

David Tepper’s Appaloosa Management sold 300,000 shares

of Meta Platforms during the fourth quarter; the stock represented about

5% of Appaloosa’s $1.3 billion US equity portfolio as of the fourth

quarter. Appaloosa added new positions in Walt Disney. Caesars

Entertainment and Aptiv during Q4. Judging by recent events, Tepper is

most likely out of Disney already. Tepper also added to holdings in HCA

Healthcare; Constellation Energy was Appaloosa's biggest holding,

representing 15% of disclosed assets

Viking Global increased its

stakes in BioMarin Pharma and UnitedHealth Group. Viking outperformed

rivals last year thanks to bets on health-care stocks, which comprised

about one-third of its portfolio at the end of the year. Its hedge fund

ended the year down 2.4%.

WIT, the investment firm that manages

the Walton family’s fortune continued to be a fan of exchange-traded

funds. WIT LLC, which stands for the Walton Investment Team, has a $3.6

billion US equity portfolio that’s mostly comprised of low-cost ETFs

(because, of course). WIT also continues to bet on emerging markets. Its

biggest holding is the $73.5 billion Vanguard FTSE Emerging Markets

ETF. WIT threw in the towel on Snowflake, the cloud computing company,

and Verve Therapeutics, a genetic medicines company, during the fourth

quarter.

Interestingly, hedge funds bought TSMC shares while Buffett was dumping them last quarter:

Hedge funds bought TSMC shares last quarter just as Warren Buffett reversed course and sold 86% of his short-term stake https://t.co/fQrO7J0LUN

As I stated in my last post on personal reflections on Ontario's first annual Pension Awareness Day, my best advice remains to follow me and don't get tied up trading in stocks:

So I get asked a lot: "If you're so bearish where do you put your own

money?" I have no problem sharing this with you. I see the next 2 years

being really, really ugly.

Right now, I am long US dollars. After an incredible start of the year

taking risks in some biotechs (TGTX, MRTX) and not sleeping well, the bulk of my

money is now invested in the Invesco DB US Dollar Index Bullish Fund

(UUP).

I'm back to sleeping like a baby, recuperating from brutally painful

sciatica, feeling A LOT better (will one day write a post on addressing

sciatica as I hate it with a passion).

Next, I am waiting for the yield on the US 10-year Treasury note to

climb above 4.5%, maybe even above 5%, after which I will put the bulk

of my money into the iShares 20+ Year Treasury Bond ETF (TLT).

Going into a crisis and with the Fed and other central banks still in

tightening mode, I see a beautiful trade setting up for long bonds and

am in no mood to risk more than 5% of my capital, and even that.

There will be plenty of trading opportunities along the way, no doubt

about it -- like trading Tesla Long and mostly SHORT -- but you need to

be really good to take advantage of those opportunities, and you need to

stay disciplined and sweep the table when you're up big (and cut losses

fast).

Most hedge funds and other alternatives funds will get creamed during the subsequent two years, I'm pretty confident of this.

As far as Tesla, I think it's going to be volatile but it remains the best short out there:

Alright, I've rambled on enough, time to wrap it up.

Please remember to donate any amount under

my picture on the top left-hand side of my blog via PayPal options.

Now, have fun looking into the portfolios of the world's most famous money managers.

The links below take you straight to their top holdings and then click to see where they increased and decreased

their holdings (see column headings).

Top multi-strategy, event driven hedge funds and large hedge fund managers

As the name implies, these hedge funds invest across a wide variety of

hedge fund strategies like L/S Equity, L/S credit, global macro,

convertible arbitrage, risk arbitrage, volatility arbitrage, merger

arbitrage, distressed debt and statistical pair trading. Below are links

to the holdings of some top multi-strategy hedge funds I track

closely:

These hedge funds gained notoriety because of George Soros, arguably the

best and most famous hedge fund manager. Global macros typically

invest across fixed income, currency, commodity and equity markets.

George Soros, Carl Icahn, Stanley Druckenmiller, Julian Robertson have

converted their hedge funds into family offices to manage their own

money.

These funds use sophisticated mathematical algorithms to make their

returns, typically using high-frequency models so they churn their

portfolios often. A few of them have outstanding long-term track records

and many believe quants are taking over the world.

They typically only hire PhDs in mathematics, physics and computer

science to develop their algorithms. Market neutral funds will

engage in pair trading to remove market beta. Some are large asset

managers that specialize in factor investing.

Top Deep Value, Activist, Growth at a Reasonable Price, Event Driven and Distressed Debt Funds

These are among the top long-only funds that everyone tracks. They

include funds run by legendary investors like Warren Buffet, Seth

Klarman, Ron Baron and Ken Fisher. Activist investors like to make

investments in companies where management lacks the proper incentives to

maximize shareholder value. They differ from traditional L/S hedge

funds by having a more concentrated portfolio. Distressed debt funds

typically invest in debt of a company but sometimes take equity

positions.

These hedge funds go long shares they think will rise in value and short

those they think will fall. Along with global macro funds, they

command the bulk of hedge fund assets. There are many L/S funds but

here is a small sample of some well-known funds.

I like tracking activity funds that specialize in real estate, biotech,

healthcare, retail and other sectors like mid, small and micro caps.

Here are some funds worth tracking closely.

Mutual funds and large asset managers are not hedge funds but their

sheer size makes them important players. Some asset managers have

excellent track records. Below, are a few funds investors track closely.

Pension Funds, Endowment Funds, Sovereign Wealth Funds and the Fed's Swiss Surrogate

Last but not least, I the track activity of some pension funds,

endowment, sovereign wealth funds and the Swiss National Bank (aka the Fed's Swiss surrogate). Below, a

sample of the funds I track closely:

Below, Bloomberg's Sonali Basak reports on the takeaways from this quarter's 13F disclosures by hedge funds.

Next, JPMorgan Asset Management's Meera Pandit joins 'Closing Bell: Overtime' to discuss why she sees red flags ahead for stocks and believes the U.S. is headed for a recession.

Third, Stanley Druckenmiller, Duquesne Family Office founder, speaks from CNBC's Delivering Alpha conference about his macro economic outlook and what a looming recession in 2023 means for investors. Druck spoke in late September and he's right, a hard landing is coming, and something likely far worse than investors expect.

Fourth, a Pensions & Investments interview with Ken Tropin, chairman, founder and principal of Graham Capital Management and a long-time veteran of the managed futures space.

Fifth, George Soros urges India's Narendra Modi to respond to questions regarding the turmoil surrounding Gautam Adani's business empire, calling the prime minister and the billionaire "close allies." Soros made the remarks in speech ahead of the Munich Security Conference. Sounds like Soros has a Big Short on India.

Sixth, Mohamed El-Erian, chief economic adviser at Allianz and Bloomberg Opinion columnist, says he hopes the Federal Reserve can tolerate US inflation above its 2% target. "I don't think they can get CPI to 2% without crushing the economy, but that's because 2% is not the right target," he says on "Bloomberg The Open."

Seventh, Roger Ferguson, former Federal Reserve vice chairman, joins 'Squawk Box' to discuss the Federal Reserve's next moves on rates, how Ferguson would handle rate hikes and the timeline of the effects of the Fed's rate hikes.

Eighth, whether you like it or not, generative AI like ChatGPT and Stable Diffusion are about to change not only how you work, but how the content you consume is produced. Forbes spoke with a number of leading voices in the AI space to determine both the benefits and the dangers of this next wave of technological innovation, and find out why both tech giants as well as cutting edge startups are racing to grab their share of the market.

Will AI take over the hedge fund space and do a better job for zero fees? Stay tuned!

Lastly, a classic scene from Margin Call, my favorite movie on the GFC. "Be first, be smarter or cheat." This is exactly how hedge funds make their money, and some of them cheat and cheat big, which is why institutional investors pay them 2 & 20 to manage billions.

Comments

Post a Comment