Bert Clark, President and CEO of IMCO, recently posted on LinkedIn the six factors they think are crucial to consider when designing the optimal asset mix:

Of all the decisions investors make, asset mix selection is the one that drives performance and affects the overall level of risk and investment returns the most.

It’s a big decision, and one that we take advising our clients on, very seriously.

These are the most important questions we address when helping our clients choose the asset mix that’s right for them:

What are their objectives? Is it return-focused or is it to maintain a certain level of funded status or contribution level?

What is the right number of asset classes?

What are the likely future returns, correlations and risks of various asset classes?

Does the asset mix enable clients to meet their liquidity obligations?

What current economic, capital market or other factors are relevant?

How does the asset mix leverage IMCO’s advantages, such as scale, access to private markets, and our clients’ long investment horizon?

Offering unbiased asset mix advice is key to driving value for our clients. Their asset mix selection acts as our blueprint for building tailored investment solutions that enable them to meet their financial obligations.

You can read the paper "Achieving the Right Balance" here.

Since it's short, I also embedded it below:

Now, it's important to note that IMCO is like CDPQ, BCI and AIMCo in that it has many clients with different asset mixes to reflect their liabilities and risk tolerance. Clients choose their asset mix based on their risk tolerance and return expectations.

OTPP, OMERS and HOOPP and large pension plans which manage assets and liabilities and since they don't have many clients (OTPP only has one basically), they can set the asset mix and match assets with liabilities to reduce funding risks.

The critical thing to remember is IMCO, AIMCo, BCI and CDPQ can only recommend an asset mix to a client, they cannot impose it.

My own personal view is this is stupid but clients like to work with their own actuaries who recommend an asset mix based on their liabilities profile.

I get it but the reason I think it's stupid is pension funds have investment experts who are paid millions to manage assets so their clients should trust them implicitly to also recommend the best asset mix for them.

But clients want to "own" their asset mix, whatever that means, but it has all sorts of governance issues attached to it, like who is exactly responsible for recommending an asset mix and what if they're completely off, costing clients a lot of lost performance.

Under Leo Kolivakis's super governance rules, I would force clients to publish the asset mix they recommended over last 5 or 10 years and then compare their performance with the asset mix recommended by AIMCo, IMCO, BCI and CDPQ.

And in both cases, I'd force them to publish who is responsible for deciding the final asset mix.

Remember, most of the returns at any pension fund or any institutional investor are determined by the asset mix.

The late David Swensen who used to run Yale's mighty endowment fund for years, used his own Swensen portfolio which Optimized Portfolio describes well here and below:

What Is the David Swensen Portfolio?

The

David Swensen Portfolio – also called the David Swensen Lazy Portfolio –

comes from portfolio manager David Swensen, who was the CIO at Yale

University from 1985 until his death in May, 2021. You can get his book Unconventional Success: A Fundamental Approach to Personal Investmenton Amazon here,

which details how retail investors can use the portfolio outlined below

to mirror the Yale Model, though note that the specific portfolio

Swensen used for the Yale endowment is not exactly the same as the

Swensen portfolio below because he was able to use somewhat “exotic”

products only available to institutional investors like private equity,

hedge funds, venture capital, etc.

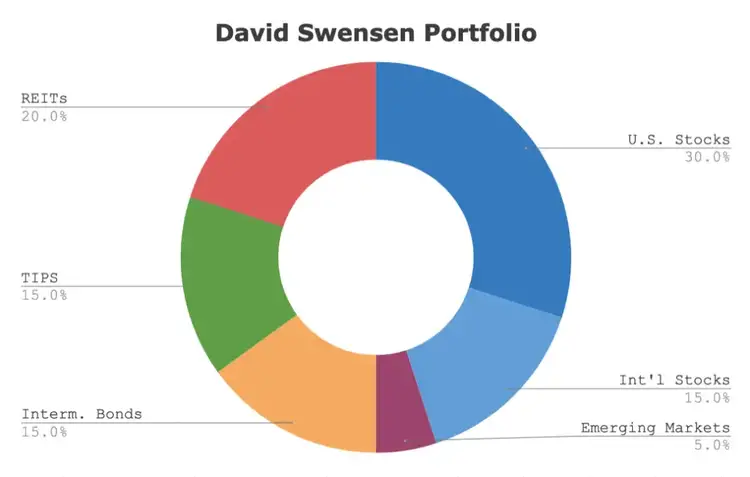

The David Swensen Portfolio asset allocation looks like this:

30% Total Stock Market

15% International Stock Market

5% Emerging Markets

15% Intermediate Treasury Bonds

15% TIPS

20% REITs

Similar to the Ivy Portfolio, we see a heavy 20% allocation to REITs. Unlike that one though, the Swensen Portfolio doesn’t include commodities, and I like that. I also like that this portfolio does not use gold.

Swensen had a particular affinity for TIPS, or Treasury Inflation Protected Securities, a relatively new type of treasury bond indexed to the CPI, the common measure of inflation. This is interesting, as most lazy portfolios ignore TIPS altogether or give them a smaller allocation. Rick Ferri is fond of TIPS as well, suggesting that retirees should probably have them as half of their fixed income allocation.

In this sense, the Swensen Portfolio is not unlike the famous All Weather Portfolio,

attempting to sail through different economic environments unscathed,

though Dalio uses gold and broad commodities as an attempt at inflation

protection instead of TIPS. In fairness, TIPS weren’t even around yet

when Dalio first proposed the All Weather Portfolio’s components.

I also agree with Swensen’s use of treasury bonds and exclusion of corporate bonds. He maintained, like I do, that treasury bonds offer superior downside protection

alongside stocks, and corporate bonds don’t sufficiently compensate the

investor for their extra risk. That said, 15% in intermediate

treasuries is not really going to provide much protection. I think it

would probably be more sensible to make them long bonds instead of

intermediate.

Furthermore, TIPS and intermediate bonds are likely

unsuitable, unnecessary, and almost certainly suboptimal for the young

investor with a long time horizon and high tolerance for risk.

In my opinion, this portfolio is better suited for retirees and those

approaching retirement, but at that point I’d also want to increase the

bonds.

The Swensen portfolio relies heavily on REITs, having them

comprise 20% of the total portfolio. This seems a bit odd to me, as we

now know REITs are not a distinct asset class,

are not a reliable inflation hedge, and don’t offer much of a

diversification benefit. Moreover, their returns seem to be explained by

exposure to the Size, Value, and Credit factor premia,

thus they can be replicated with small cap value stocks and

lower-credit bonds. I don’t have a problem with 10% or so in REITs, but

20% seems like too much in my opinion when that valuable space could be

given to stocks or bonds.

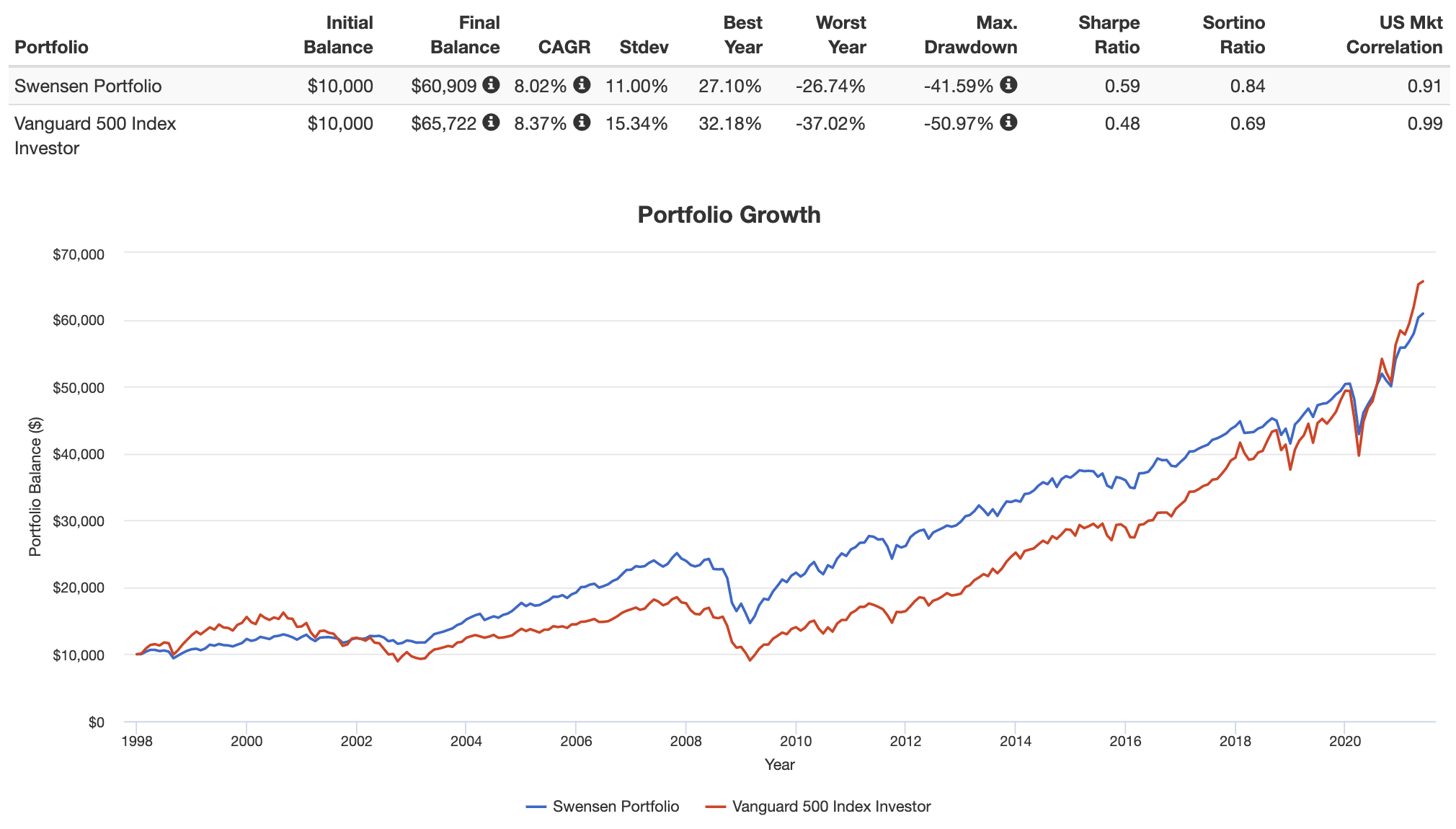

David Swensen Portfolio Performance

For

the period 1997 through May, 2021, the David Swensen Portfolio and the

S&P 500 have been pretty close from a pure returns perspective, with

the former obviously having a higher risk-adjusted return (Sharpe) due to its lower volatility:

Source: PortfolioVisualizer.com

David Swensen Portfolio ETF Pie for M1 Finance

M1 Finance is

a great choice of broker to implement the David Swensen Portfolio

because it makes regular rebalancing seamless and easy, has zero

transaction fees, and incorporates dynamic rebalancing for new deposits.

I wrote a comprehensive review of M1 Finance here.

Utilizing mostly low-cost Vanguard funds, we can construct the David Swensen Portfolio pie with the following ETF’s:

VTI – 30%

VXUS – 15%

VWO – 5%

VGIT – 15%

SCHP – 15%

VNQ – 20%

You can add the David Swensen Portfolio pie to your portfolio on M1 Finance by clicking this link and then clicking “Add to Portfolio.”

The key part in the aobve which I highlighted is this: "though note that the specific portfolio

Swensen used for the Yale endowment is not exactly the same as the

Swensen portfolio below because he was able to use somewhat “exotic”

products only available to institutional investors like private equity,

hedge funds, venture capital, etc.

The reason endowment fund superstars like Swensen got paid well is to outperform the lazy portfolio that can be easily reproduced using passive indexes.

Swensen invested in top VC funds, top private equity funds and hedge funds to deliver even better risk-adjusted returns (with a lot less liquidity, of course) than his "lazy" portfolio which almost matches the S&P 500 returns over the long run with less risk.

[Note: I'd love to compare the long-term performace of Canada's large pension funds to the Lazy Swensen Portfolio above]

I recommended one of Bernstein's books to a friend of mine who is a cardiologist at Stanford and he has been implementing the asset mix Bernstein recommends and rebalances his portfolio once a year and he has done very well over the last 20 years. "I don't have time for this stuff, I'm busy researching so I find his approach intuitive and easy to do in practice."

Now, reblancing a portfolio is important and it doesn't only have to be once a year, it can be once a quarter if you're a large investor or more often as some asset classes swing more than others (stocks, corporate bonds, commodities, etc.).

For most people, a 60/40 portfolio has delivered solid gains over the last two decades with less risk except of course last year where stocks and bonds got killed as inflation hit a 40-year high.

Going forward, if we run into a 1970s wage inflation spiral that causes stagflation, we might just see the weakest returns for the 60/40 portfolio for an extended period of time.

Stagflation isn't good for Canada's large DB pensions because they guarantee cost-of-living adjustments, so high inflation for longer impacts their ability to stay fully funded (this is why they all adopted conditional inflation protection, removing guaranteed inflation adjustments for a period of time when the plan is underfunded and restoring it when it's fully funded..this works well for mature plans which have more retirees than active members).

The worst thing for al pensions is a long period of debt deflation as liabilities shoot up and all assets -- public and private -- get clobbered.

That's why you need a healthy allocation to nominal bonds, just in case this happens.

Right now, there is a lot of uncertainty for many people, not for me.

I do not follow any lazy asset mix, my objective is to trounce not only the S&P 500 year in and year out but to also trounce elite hedge funds I cover, taking more risk of course (do not trade a lot but when I have conviction, I go all in and go for the jugular).

I call it the Zorba the Greek portfolio and you should try it once in a while to see what it really feels like making a killing or fearing the risk of ruin in real life.

After making a killing on a couple of biotechs during the first six weeks of the year (TGTX, MRTX) and getting out right before President Biden gave his state of the union address, I'm all in the US Dollar ETF (UUP) waiting for the yield on the US 10-year Treasury note to cross above 5% so I can start shifting more into US long bonds (TLT).

I'm also having fun betting against Tesla, my favorite ESG pinata, via the AXS TSLA Bear Daily ETF (TSLQ) and also betting against NVIDIA (NVDA) via the AXS 1.25X NVDA Bear Daily ETF (NVDS).

As you know, I'm bearish, even more bearish than Francois Trahan who is openly bearish and posts great stuff on Twitter here and LinkedIn here.

I too post a lot of great stuff on Twitter here and LinkedIn here.

In case you haven't noticed, I love markets, can talk markets almost 24/7 but I have a lot of other interests like health, sports, politics, philosophy and exposing nonsense I see on ESG and diversity, equity and inclusion window dressing (wait for it, a doozy is coming up).

As George Carlin once noted: "BS is the glue that binds us as a nation."

There is so much BS everywhere, we are literally swimming in it and most people don't even realize it.

The smart ones do but they remain quiet fearing reprisal from their employers who are neck deep in woke culture nonsense.

I fear nothing and answer to nobody but the guy in the mirror, and my wife who is the real boss!

One thing I do not like about IMCO's approach to its asset mix is this part:

Investors should not spend a lot of time trying to predict

what is hard to predict: Very near-term developments, or very

long-term changes to society, technology, economies, or the

markets. But they do need to adapt their portfolios to the

current investing environment.

IMCO releases an annual World View, which sets out our

analysis on the current investing environment and the

strategies investors should consider as they navigate

prevailing trends, opportunities, and risks.

They better get their "World View" right over the next couple of years or else they're in big trouble.

Let me be blunt, I hate when people say "you can't predict the future."

BULLOCKS! At major inflection points, I can predict the future and it's very grim, so prepare for a hard landing and a deep and prolonged global recession, and adjust your asset mix accordingly:

"at the moment, it is clear that we are firmly in the no landing scenario... it could be that we have to wait until 2024 before we find out what comes after no landing."

I obviously do NOT agree with Apollo's Slok on the no landing scenario, that is a pipe dream, just like Bank of America CEO Brian Moynihan's prediction os a 'slight' recession is deusional:

Bank of America CEO predicts most people won’t even notice ‘slight’ recession, but warns interest rates won’t come down for at least a year https://t.co/xIjbnk7SDY

No wonder his stock got clobbered over 6% today along with many other financials (XLF) led by the fallout in SVB Financial group (SVIB) whose stock cratered 60% today and is down another 22% in after-hours.

Oh yeah, it's rock n' roll time, the brutal phase of the bear market is just getting underway, I can feel it, I can taste it, there's blood in the water!

Yes, it's different for pensions, they have deep pockets and a long investment horizon, but even they should be asking the same questions I am asking, namely why risk so much in alternatives when the risk-free rate is so high?

And some asset classes like real estate, are going through their Darwinian moment of truth:

Alright let me wrap it up there, I can go on and on and on about "optimizing your asset mix" but unless you have really smart people like me on your team, you're not optimizing anything and only following terrible advice your brokers are offering you.

My best advice for institutional clients is get ready for a deep and protracted global economic slump which will impact all your assets, private and public. There will be no place ot hide and it will be a long, tough slug ahead.

Have fun optimizing that!!

Below, the David Swensen Portfolio, as the name implies, is based on the late David Swensen’s management of the Yale endowment fund. Here we’ll take a look at its components, performance, and the best ETF’s to use in its construction.

Second, Alan Blinder, former Fed vice chair, joins 'Closing Bell: Overtime' to discuss the Fed and what he expects its next moves to be. I disagree with him, he's not paying attention to wage inflation and what the Fed is saying.get ready for two more 50 bps rate hikes.

Third, CNBC's Hugh Son joins 'Fast Money' to report that shares of Silicon Valley Bank have continued to slide as VCs and others continue to pull money from the bank.

Fourth, George Maris, Janus Henderson Investors co-head of equities - Americas, says he's seeing a changed economic dynamic for global investors. He speaks on "Bloomberg Markets: The Close."

Lastly, when all else fails, remember the wise words of Zorba the Greek: "A man needs a little madness to cut the rope and be free." You need madness to make money in these schizoid markets, especially when all hell breaks loose.

Comments

Post a Comment