The Canadian Press reports CDPQ posts 4.2% return for first six months of 2024:

The Caisse de dépôt et placement du Québec (CDPQ) posted a return of

4.2 per cent for the first six months of 2024, underperforming its

benchmark index of 4.6 per cent.

However, the average annualized

return over five years was higher than the benchmark portfolio for

Quebecers' nest eggs. At 6 per cent, compared with 5.3 per cent for the

benchmark, it represents nearly $14 billion in added value, according to

the Caisse.

On Wednesday, the Caisse presented an update on its

results for the first half of the year. As of June 30, 2024, CDPQ's net

assets stood at $452 billion, an increase of $18 billion compared with

the end of 2023.

CDPQ's President and CEO reported that the

months of January to June were marked by various factors. These ranged,

he said, from modest global economic growth, to the U.S. Federal Reserve

postponing anticipated rate cuts, to strong stock market performance

"which continued to be linked to a historic level of concentration in a

handful of technology stocks."

"During this period, our diversified portfolio performed well

overall, and our depositors' plans also remain in excellent financial

health. Discipline is needed going forward, as the second half of the

year has already seen its share of ups and downs and volatility,"

commented Charles Emond in a news release.

With regard to its

real estate portfolio, the Caisse reported a negative return of 3.6 per

cent over six months, compared with an index return of -0.9 per cent.

The institution attributed it in particular to difficulties in the

office sector and the high interest rate environment, which weighs on

financing costs.

Mark Mann of Bloomberg also reports Quebec’s CDPQ gains 4.2% as stocks offset real estate losses:

(Bloomberg) -- Caisse de Dépôt et Placement du

Québec scored a 4.2% return in the first half of the year, as big gains

in public and private equities helped the fund overcome losses on real

estate and bonds.

Chief Executive Officer

Charles Emond cited multiple factors that drove investment results.

Stock markets enjoyed a tech-driven boost, while stronger-than-expected

economic growth in the U.S. meant that North American bond yields rose —

hurting fixed income returns.

Quebec’s

public pension manager outperformed the market with 13.6% gain in its

equity markets portfolio, above the benchmark of 13.2%. Private equity

holdings gained 6.9%.

Discipline is required

for the second half of the year, which has “already seen its share of

twists and volatility,” Emond said in a statement.

CDPQ’s

infrastructure portfolio continued to perform well with a six-month

return of 5.3%, beating its benchmark index by 100 basis points.

Real estate remained a drag on returns, however.

That group lost 3.6%, reflecting the troubles in the office sector and

the pain of higher interest rates.

Total assets under management grew to $452 billion.

Earlier today, CDPQ issued a press release announcing it posted a mid-year 2024 return of 4.2% over six months and 6.0% over five years:

Net assets of $452 billion, up nearly $18 billion

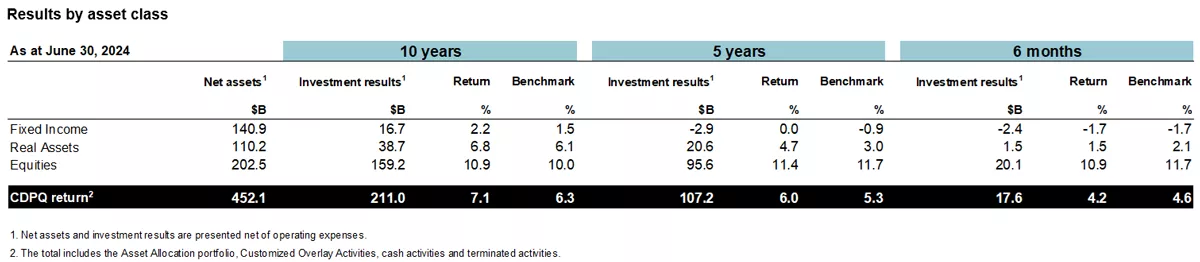

Annualized return of 7.1% over ten years

Depositors’ plans in excellent financial health

CDPQ today presented an update of its results as

at June 30, 2024. Over six months, the weighted average return on its

depositors’ funds was 4.2%, below its benchmark portfolio’s 4.6%. Over

five years, the average annualized return was 6.0%, above its benchmark

portfolio’s 5.3%, representing nearly $14 billion in value added. Over

ten years, the average annualized return was 7.1%, also higher than its

benchmark portfolio, which stood at 6.3%, producing over $26 billion in

value added. As at June 30, 2024, CDPQ’s net assets

totalled $452 billion.

“The

first half of the year was characterized by different factors: strong

stock market performance that continued to be linked to a historic level

of concentration in a handful of tech stocks, the U.S. Federal

Reserve’s deferral of many rate cuts that were anticipated at the

beginning of the year and modest global economic growth,” said Charles Emond, President and Chief Executive Officer of CDPQ. “During

this period, our diversified portfolio performed well overall and our

depositors’ plans also remain in excellent financial health. Discipline

is in order going forward, as the second half of the year has already

seen its share of twists and volatility.”

Return highlights

Fixed Income: Rising long-term bond yields erase high current yield

In

the first half of the year, long-term (10-year) Canadian and U.S.

government bond yields rose by 40 and 49 basis points, respectively,

whereas the markets expected significant easing from central banks at

the beginning of the year that did not materialize. This is due to a

U.S. economy that appeared resilient until more recently and inflation

that slowed but remained above the long-term target. In this

unfavourable environment for bonds, CDPQ recorded a return of -1.7% over

six months, in line with its benchmark index. Fixed income portfolios

provided a high current yield of 3.1% during this period, due to the

premium on private credit activities. However, this performance did not

offset the decrease in value resulting from the portfolio’s strong

sensitivity to rates, which reflects the need to match depositors’

long-term liabilities.

Over five years, the asset class’s

annualized return was 0%, above its index’s -0.9%. The class was still

affected by the historic increase in rates starting in 2022. The impact

was, however, offset by the good performance of all credit activities.

Real Assets

Infrastructure: Robust and sustained performance

The

infrastructure portfolio’s solid performance over the years continued

in the first half of this year. Over six months, the return was 5.3%,

above its benchmark index’s 4.3%, driven notably by the transportation

sector, particularly ports and highways, as well as the energy sector.

Over

five years, the annualized return was 10.2%, against the index’s 4.5%

return. The portfolio played an important role in limiting the impact of

high inflation on the total portfolio, given the context of recent

years. Well diversified, it benefited over the period from all sectors

it is exposed to and, in particular, from favourable positioning in

renewable energies and port assets, two priority sectors in

infrastructure. We also note the strategic materializations carried out

in recent years by the teams.

Real Estate: Challenging office conditions still affecting portfolio performance

The

real estate industry’s challenges in recent years persisted in the

first half of the year, in particular due to the difficulties of the

office sector and the high interest rate environment that weighs on

financing costs. In this demanding context, the portfolio posted a

return of -3.6% over six months, compared with the index’s -0.9%. The

logistics sector contributed positively to the return, but could not

fully mitigate the fall in value in the office sector, especially in the

United States.

Over five years, the portfolio’s annualized return

was -0.6%, below the index’s 0.8% return. Since the portfolio’s

repositioning toward sectors of the future such as logistics and

residential in 2020, the gap between the returns of the portfolio and

the index has narrowed.

Equities

Equity Markets: Solid performance in a context of historically concentrated gains

The

strong growth of stocks related to artificial intelligence was the

dominant theme in the first half of the year, propelling the main

indexes to record levels. In this context, where earnings are

concentrated in these few companies, the Equity Markets portfolio still

managed to outperform its index with a more diversified return. Over six

months, the portfolio posted a 13.6% return, above its index, which

earned 13.2%. The positive difference stems from excellent stock

selection by internal managers.

Over five years, the annualized

return was 9.8%, compared with 10.5% for the index. The difference is

mainly explained by the portfolio’s marked underweighting in major tech

stocks at the beginning of the period.

Private Equity: Key sectors drive performance

In

the first half of the year, the portfolio posted a return of 6.9%,

resulting from the performance of companies in sectors such as consumer

goods, industrials and finance. The index recorded a return of 9.6%,

which reflects in part the significant weight of public markets in

its composition.

Over five years, the portfolio’s annualized

return was 14.3%, compared with 13.0% for the index. Among the reasons

for the performance over the period is the good selection of direct

investments in the technology, finance and consumer sectors.

Québec: An important contribution to economic vitality

In

Québec, CDPQ’s teams have delivered numerous transactions and projects

to stimulate the Québec economy in a sustainable way, including:

Support to grow companies

An investment of $500 million to support National Bank’s acquisition of Canadian Western Bank

Support for Nuvei,

one of the most advanced technology providers in the global payments

industry, in its transformation into a privately held company, bringing

its value to over USD 6 billion

An investment of $125 million in Levio, a leading consulting firm specialized in large-scale digital transformations, to support its North American expansion plan

Support for Lemay,

a leading architecture and design firm, whose growth projects CDPQ has

been supporting for 10 years, for its acquisition of Fusion Énergie

An equity stake in QSL International, a key maritime logistics player that is headquartered in Québec City

Major real estate and infrastructureprojects

CDPQ Infra’s master plan, the Plan Circuit intégré de transport express (CITÉ), to improve mobility in the Communauté métropolitaine de Québec

Start of dynamic testing for the Réseau express métropolitain (REM), in Greater Montréal, on a first segment of the Deux-Montagnes branch

Recent

proposal submission by the Cadence team led by CDPQ Infra as developer

partner, as part of the procurement process for the High Frequency Rail (HFR) project between Québec City and Toronto

Reopening of the 9th floor of the Centre Eaton de Montréal, a heritage site in the heart of the city

A more sustainable economy

Financial backing for Norda Stelo,

a renowned engineering firm present in more than 50 countries, for its

acquisition of InnovExplo, creating a new force in the field of critical

minerals that are essential to the energy transition

Participation in a $136 million round of financing in FLO, a major leader in transportation electrification that CDPQ has supported for nearly a decade

Integration of real estate subsidiaries: An important milestone in the history of CDPQ

The

first half of the year saw the implementation of a major project for

CDPQ: the integration of its real estate subsidiaries, Ivanhoé Cambridge

and Otéra Capital, to benefit from the full potential of a simplified

organization and to generate efficiency gains. Note that this

integration, which began in January, will be completed by the beginning

of 2026 and will ultimately represent annual savings estimated at

approximately $100 million through the synergies achieved.

ABOUT CDPQ

At CDPQ, we invest constructively to generate sustainable returns

over the long term. As a global investment group managing funds for

public pension and insurance plans, CDPQ works alongside its partners to

build enterprises that drive performance and progress. We are active in

the major financial markets, private equity, infrastructure, real

estate and private debt. As at June 30, 2024, CDPQ’s net assets totalled

CAD 452 billion. For more information, visit cdpq.com, consult our LinkedIn or Instagram pages, or follow us on X.

In the afternoon, I had a chance to catch up once again with Vincent Delisle, EVP and Head of Liquid Markets at CDPQ to go over mid-year results (recall, I recently spoke to Vincent about why CDPQ allocated C$600 million to Fiera Capital).

I want to begin by thanking Vincent for taking some time to talk to me on a very busy day and also thank Kate Monfette and Jean-Benoit Houde for setting up this Teams meeting.

Before I get to my discussion, despite trailing the benchmark, the results are solid and exactly in line with what Teachers' reported yesterday for its mid-year results (coincidence since they have different asset mixes).

I'm going to tell you right away that I like talking to Vincent because he's a real markets guy, a liquid markets guy so we really got into it and I can literally talk to him an hour easy just about markets.

I began by asking him to provide me with a broad overview by asset class of the results.

Vincent replied:

I'll go very general in terms of the overall because Charles usually handles that but I'll give you some of the highlights we shared with everyone this morning.

Some context on their first half. Bond yields went up. Turns out the 6-7 Fed rate expected by the markets didn't pan out. Not much of a surprise when you look at the resiliency of the US economy in the first half and the fact that the CPI even if it is heading lower is at the upper end of where the Fed would want it to be.

And the other thing is market concentration. I keep talking about this, it keeps popping up. I thought 2023 was tough in terms of concentration but turns out 2024 is even more vicious in terms of how the S&P was led by you know, forget about Mag-Seven but Nvidia really hitting the concentration bucket there.

In this context, our number 4.2% in the first six months versus 4.6% for the benchmark, obviously led by Public Equities which had a very good semester and Infrastructure which for us keeps delivering. Fixed Income got hit by the increase in bond yields.Private Equity did well but tough comp because 50% of their benchmark is liquid markets. Although we are seeing some improvement in Real Estate relative to where we were in 2020 and 2021, it's still a tough environment for real estate as an asset class.

So, to sum up, concentration, yields going up, six months is a short window but we like the fact that most of our strategic focus and changes that were initiated four years ago are working and it's mainly coming from the Infrastructure and Public Equities books.

That was a good overview and I told Vincent that last year at this time, we covered 2023 mid-year results and talked about how they implemented systematic/quant portfolios in Public Equities and that went well, so I asked him if that performance has continued or in an environment where volatility is picking up, will it be more challenging for these systematic strategies?

Vincent replied:

First, our result in Public Equities in the first half is the consequence of very solid stock selection both from our fundamental and quant team. Last year was all about quants to be honest, in the first half of 2024, the value add came from our quantitative team and bottom up team. I'm very happy because the systematic factors have been held up by momentum, less the case on the fundamental side.

Last few weeks, we've seen a shift, somewhat of a retreat in the Big Tech names but they're holding on pretty well.

When we talked last year, quant for us was a big story because we went from nothing to a lot. This year, we haven't changed the allocation much and the amount of money they're managing hasn't changed at al this year.

Where we've been active -- no pun intended -- in Public Equities is we internalized a bit more. We reduced some of our exposure to external portfolio managers and the reason is quite simple, we have a good quant team and a good fundamental team, so we increased a bit of the exposure to the bottom-up (fundamental) group.

So good first half and the volatility of the last few weeks, they're holding up ok, I'm happy.

I told Vincent that yesterday I had a discussion with their peers at Ontario Teachers' (see comment here) and one of the discussions that came up was the debate between active versus passive as well as they're looking into their benchmarks because they're really tough to beat, but most importantly, they're looking at internal versus external active management and where it makes sense to allocate.

I told him that I feel 2024 is a continuation of 2023 but volatility is picking up because the lagged effects of rate hikes are starting to creep into markets:

For those wondering if the last two weeks were random ... not likely. Volatility usually starts to pick about 2.5 years after the beginning of Fed tightening. It's not a perfect relationship, but if it was, we would be staring at higher volatility into the second half of 2025. pic.twitter.com/XPHihSJ9sJ

Passive/ active, beta versus alpha, this is something I think about every single day. One of the things we initiated in 2021 shortly after I joined is we moved our portfolio managers to style benchmarks rather than generic benchmarks.

The portfolio construction aspect is obviously very important so from a portfolio construction standpoint, we choose the beta and then ask managers to beat it so it's alpha that's much more difficult to churn. So, all the comments I made on our internal teams having a good start of the year, this is al relative to style benchmarks rather than the generic MSCI World or S&P 500.

It's very challenging for long-only portfolio managers to outperform in this market because of concentration so the way we are dealing with this is we want ot have much more control on the beta, on the passive, and wherever we can find talent to add value over that beta, we've had good success in recent years.

Having said that, when concentration stops, there will be a tailwind out there for all portfolio managers that aren't succumbing to FOMO. We saw this post-2000, it's happened before, it will happen again, leadership will broaden out but when this happens, will it be because of the excellence of portfolio managers or can you just buy the S&P Mid-Cap Index or go lower market cap?

I read your note yesterday, and I talk to Gillian quite often, beta vs alpha, passive vs active is definitely top of mind for us as well.

On the Long/ Short space, we find it more attractive to find talent, on the long-only side, it's been more difficult.

I told Vincent that 22 years ago, I was working in Mario Therrien's team, in charge of managing a significant directional hedge fund portfolio made up of top global macro funds, L/S Equity, CTAs and a few short sellers and one or two fund of funds (I had a lot of work to fix that portfolio after inheriting it).

[Side note and fun facts: We were the first in Canada among the big pension funds to invest in Bridgewater back then but I can't take all the credit there as Alan and Simon at McGill Capital (private family office) got me onto those guys. That's how I eventually met Ray Dalio when I moved on to PSP and Gordon Fyfe was with me and teased me all the way home after an irritated Ray blurted out at me when I pressed him on deleveraging and deflation: "What's your track record?

Good times, I laugh at it now thinking back but I got to meet some extraordinary talented managers including Andreas Halvorsen, founder and CEO of Viking Global, one of my favorite L/S funds.]

Anyway, I told Vincent that in my experience, very few L/S funds are actually good at shorting stocks, you have some great stock pickers but shorting isn't their strength (some short sellers were good sometimes but returns are way too volatile and not worth having those funds over the long run, just like tail-risk funds).

To be fair, in these markets, it's very tough shorting markets, as you can short Nvidia one day and make a killing and lose it all and more the very next day (then again, Nike and Disney were great shorts this year).

On style indexes, I totally agree, had many hedge fund managers that were trying to pull fast ones on me going long small cap stocks back then and using the S&P 500 as a benchmark.

Told Vincent I trade a lot of biotech stocks and look at the SPDR S&P Biotech ETF (XBI) and follow top biotech funds and in my experience, the very best ones trounce this ETF.

It's the same for other sectors, you need to understand the beta of the managers well to see if they're really offering value.

We next moved on to Fixed Income and told Vincent yesterday when I was talking to Jo, Gillian and Stephen I forgot completely that rates backed up in the first half of the year and my trader's head was still thinking of that massive rally in the long end we saw in recent weeks.

I told him that I remembered last year when we spoke, he told me that the 10-year US Treasury bond yield might go back down to 3% but it will be tough to go lower and definitely not to pandemic levels.

I asked him if that still remains his thinking this year, whether he thinks a recession has already started in the US and whether we are headed for a hard or soft landing (I'm in the hard landing camp).

He responded:

I'm very humble when it comes to predicting where rates are going. What I find interesting in looking at the 10-year chart right now is you go back to the end of 2022 -- so Q3 2022 -- we've had one, two, three and this is the fourth time that the market is trying to price Fed easing. It's been wrong on the first three occasions and where it really hurt people in the first half of this year is wee entered 2024 with the market pricing six to seven rate cuts and we didn't get any.

Right now the claims -- there are too many numbers out there but some are more relevant to others -- claims have gone from low 200Ks to 230-240K, the pace of job growth has been decelerating, it's been quite notable on the consumer side over the last one to two months. We've had the 10-year yield trading below its 200-day moving average for the first time since 2020.

I think the safe scenario here is that the US is slowing down. Hard or soft landing, honestly, is not where I spend most of my time. Landing to us is important to get so we are adapting the portfolio to lower rates, and I think with lower rates and evidence the economy is slowing, it will eventually challenge the concentration aspect we are seeing in public equities.

If yields go down, how low can they go? Not that low. (US) Inflation is still at 2.9% (annualized), best case scenario is it goes back to 2%, the term premium is going to go higher so ballpark for us, 3.5% is a level we would consider neutral for US 10-year Treasury yield. Could you see 3%, yes, but the low three would become quite attractive (to short? that's what I think he meant).

He mentioned that they are adapting the portfolio as they see the macroeconomic environment shifting so I asked him if they make big tactical calls so for example, if rates back up to 5% again, they raise their exposure to Fixed Income.

Vincent replied:

In Liquid Markets, I'm in charge of Fixed Income headed by Marc Cormier, Public Equities and tactical Asset Allocation. That's where we house our internal TAA, that's where we have some global macro hedge fund exposure, and that's where we overweight a specific portfolio over the other.

And that team has a systematic process, a rules-based process, and I like that because you can be encumbered with your own personal biases when you try to look at all this stuff. but to your question, absolutely, we have the tools and the means to be agile when the market gives us opportunity to overweight equities over fixed income, we can do it with futures, overlays or redirect money from one portfolio to the other.

In other words, that is an important source of internal alpha at CDPQ.

Given we talked about Fixed Income, I also asked him about Private Credit which falls under Marc Cormier's team and whether it continues to deliver or do they see a slowdown as billions enter that market.

He responded:

We still like what we see in Private Credit. Currently, the yield-to-maturity of our Fixed Income portfolio is 6.2%, 3ish comes from our government bond exposure and 7.5% comes from our Private Credit exposure.

We are not seeing that much stress in balance sheets.We have a very thorough diligence process any time we award money. We are seeing a lot of refinancing this year in private credit, not as much new deals. I hear you that a lot of money is coming to the asset space but we are seeing more refinancing than new deals in there so there's not over-hyped activity from where we are sitting.

With infrastructure private credit, and I probably answered this a year ago, the answer there would be similar. When we look out 5 years and onward, private credit in infrastructure on a risk-adjusted basis is still very attractive.

I then moved on to Private Equity noting a recent article I covered where Martin Longchamps explained in detail how they used the secondaries market and are focusing more on mid-market space to address an overallocation issue.

I asked Vincent about what is going on in that portfolio and agreed with him if half the benchmark or more is made up of public equities, good luck beating that benchmark.

Vincent replied:

I'll give you some very general comments about that portfolio, I'm not the one to talk about it and I don't know it as much in-depth.

The overallocation we had in private equity is very similar to all the other pension funds. It's basically the denominator effect.

Martin was brought in a few years ago, did a great job in running a few secondaries, reshifting the portfolio to have a better balance between external fund investments, co-investments and internal investing.

On a 5-year basis, it's been a great contributor for us, 14% versus 13% for the index, so solid outperformance there.

Last hing I'd mention about this portfolio is all the concentration risk we are seeing in public equities, when that unwinds, private equity will do better than the public market comparison.

Like I said, looking at 5-year returns on the MSCI World annualized, it's around 11-12%, that's 5% minimum over what it's supposed to generate so we like that asset class, we like the pivot that Martin has done there, relative to public equivalent, it's been a tough two years but mean reversion and less concentration we think will help.

I agree and noted when I spoke to Charles Emond three or four years ago, he told me they were taking more tech risk in private equity but with concentration risk in Mag-Seven being so prevalent, why would they take more risk in tech in private equity, doesn't make sense, so that portfolio needed to be reshifted to exclusively focus on value so when there is a dislocation in public equities, that portfolio should start outperforming on a relative basis again.

Vincent replied:

Absolutely and you know what we did to this point and one thing Charles brought is a philosophy of always challenging ourselves and not be afraid to be agile and change our minds along the way.

Four, five years ago, the plan was to do more tech in private markets, then all of a sudden 2022 arises, the Nasdaq drops 33% and we realized, let's stop doing private tech and let's shift that money into public tech.

That was one way to be agile and obviously, I wouldn't be doing this today but that was a great call to shift the emphasis from private tech in 2021 and 2022 to taking these bargains in these mid to small-cap techs in the US and that's what we did, we shifted that money into the public equity portfolio.

I then quickly shifted to real estate which remains problematic, offices are dragging down returns, logistics are doing well, and asked Vincent how the integration of Ivanhoé Cambridge is going.

He replied:

It's still early days but the objective of this integration is to make sure we are more efficient, that we have all the expertise in one place. We call it Caisse de dépôt unie -- Unified CDPQ -- and it's really showing off.

Rana just took over a few months ago, she's doing so in an environment where after shopping centers, now it's the office space but she's a solid investor, used to be in our infrastructure team, she turned around Otéra and she's getting the support from everybody in the executive committee and investment committee.

So, tough space, we are happy that the performance is better than what we are seeing from some peers. We are happy that our performance is much better than it would have been had we done nothing and we are also reflecting on the fact that real estate is not going away. We need space bu tit's redefined space in residential, multifamily, logistics and even office there are some opportunities there.

Early days in the integration but so far we are heading in the direction that prompted Charles' decision to integrate the subsidiaries.

In closing, I told him the Quebec portfolio under Kim Thomassin's watch continues to do well, I saw the announcement earlier this week that CDPQ will invest $158 million in WSP to help it expand in the US.

I noted that Stephen McLennan told me yesterday hey are focusing on the US elections and the knock-on effects depending on who wins and seeing volatility picking up, so I asked Vincent what is keeping him up at night in the second half of the year.

He replied:

One thing is for sure, I've been involved in public markets for a long time, I've been head of Liquid Markets here for 4 1/2 years, I expect volatility all the time.i expect to be surprised in the next few months.

The discussion we had earlier, with the way the US macro outlook is shaping out, slowing down, lower inflation, Fed rate cuts, I think the performance of our Fixed Income portfolio is going to continue to improve in the second half. that's similar to what we saw last year when fixed income markets had a very strong finish to the year.

With the positioning we have, out Fixed Income portfolio should generate 6 to 6.5% with yields flat to slightly flat. So that's one area where I think we will see a difference in the second half versus the first half.

The narrowing spreads between US rates and Japanese rates is also something very important. A lot of hoopla last week in Japan, I don't think it's over, we don't think it's over.

Two dominating themes in the market over the last few years are Japan and Mag-Seven and I think they're linked together. These two trades have been sucking up all the leadership, so if Japan's carry trade unwinds, it also means new leadership globally and in public markets so we are zeroed in to what does the slowdown mean for our Fixed Income portfolio and when does the broadening out in public equities really take hold.

I told him it's amazing he ended the conversation on that topic because it's a subject I've been trying to wrap my head around.

JPMorgan thinks half of the carry trade has unwound, I personally thought there was much ado about this unwinding but there's no question as the yen weakened to historic lows, hedge funds and large quant funds took on more leverage to buy more Mag-Seven stocks, so if there's further unwinding, it could get really ugly if the yen rallies again (not sure the BoJ is going to take part in that this time).

Vincent replied:

It's something to look at. To JPMorgan's credit to help their recommendation, the yen went from 160 to 140 so have we've seen a big move already? Yes, we've seen a big move. The thing is if the yen doesn't go back to 160 and drifts lower to 140 or 135, it ain't over.

There's a lot of hope in the markets that winning trades -- a lower yen and stronger Mag-Seven -- come back with a vengeance, and when you manage a liquid portfolio, these two themes are intertwined and they have to be front and center.

We ended it there, like I said fantastic discussion on the markets and I can talk to Vincent all day about markets, he really knows his stuff and is a really nice guy to bounce ideas off of.

Below, CEO Charles Emond said everyone should be reassured the CDPQ pension plans of all its clients are in excellent financial health.

Also, watch Charles Emond's interview on Zone Economie tonight (in French) discussing their mid-year results and why their objective is to be diversified and deliver the returns the depositors need to meet their long-term obligations. Listen to the discussion, well worth it.

Comments

Post a Comment