Caisse Delivers $4.1B Value Added in H1 2010

The Caisse de dépôt et placement du Québec, Canada's largest pension fund, reported its results for the first half of 2010:

The Caisse de dépôt et placement du Québec, Canada's largest pension fund, reported its results for the first half of 2010:The Caisse de dépôt et placement du Québec announced today that the weighted average return of the depositor funds for the first half of 2010 amounted to 2.33%, compared to -0.74% for its overall portfolio’s benchmark index.

The Caisse outperformed the markets by 307 basis points (3.07%), leading to $4.1 billion in value added compared with the benchmark index. The Caisse’s net assets stood at $135.8 billion, as at June 30, 2010, compared to $131.6 billion, as at December 31, 2009.

“The markets were challenging and volatile in the first half of the year, with sharp declines in global stock market indicators and significant concerns about European and U.S economic outlooks," said Michael Sabia, Caisse President and Chief Executive Officer.

“Despite this fact, the Caisse navigated this unfavourable environment well. Our results reflect the work of our asset managers during this period. We find it particularly encouraging that we could produce $4.1 billion in value added compared with the markets. This was largely due to the Caisse’s range of measures to solidify its foundations, add rigor to every activity and increase its flexibility.”

“In my opinion, this also indicates that our portfolios are more robust and stable than before," said Mr. Sabia.

“Despite our many achievements during the first half of the year, we still have much to do. Our goal is to provide consistent, long-term returns to our depositors,” said Mr. Sabia. “This will continue to be a challenge, since we expect markets to remain volatile for some time.”

KEY ACHIEVEMENTS

In the first half of the year, the Caisse was very active, managing both its portfolio and balance sheet. Here are some examples of its key achievements:

• New depositor portfolio offer: The new specialized portfolio offer aims to better meet the needs identified in consultation with depositors in 2009 (see attached information sheet).

- This is a simplified, more flexible offer that makes it easier for depositors to establish their investment policies and, in turn, better meet their specific needs.

• ABTN: In the first half of the year, the Caisse conducted some hedging in accordance with its risk management strategy, which substantially reduced the ABTN portfolio’s attributable risk, by about 45%, minimizing the effect of market movements.

• Underweight in Equity portfolios: In addition, the Caisse implemented a proactive underweight strategy in its Equity portfolios due to increased market risk, particularly related to the European crisis.

• Reduced leverage: The Caisse eliminated its private equity portfolio leverage and continued its strategy of reducing it in its Real Estate portfolio:

- The leverage ratio (total assets versus liabilities) continued to decline, reaching 21%, as at June 30, 2010, compared to 23% (as at December 31, 2009) and 36% (as at December 31, 2008).

- The consolidation of our balance sheet continued with the completion of the $8 billion financing program announced in fall 2009 and completed in June 2010. This financing was used to repay short-term debt and better match financing sources and financed real estate assets. This program did not increase the Caisse’s total leverage.

• Cost control: Consistent with its recent commitments, the Caisse took these measures with the aim of controlling operating expenses and remaining in the league of best-in-class managers. The institution is also on track to achieve its 2010 objectives.RETURNS AS AT JUNE 30, 2010

“Given a challenging market environment, the results of the first half of 2010 reflect the fundamental quality of our assets,” said Roland Lescure, Executive Vice President and Chief Investment Officer of the Caisse. "They are also the result of proactive asset allocation that takes the market environment into account.”The four main factors behind the $4.1 billion in value added are the following:

1. The excellent performance of the Private Equity portfolio (+14.7% return), due primarily to operational improvements by many portfolio companies, which increased their profits.

2. The superior performance of the Caisse’s fixed income portfolios (+6.0% return), mostly from corporate and real estate debt investments.

3. The good performance of the Investments & Infrastructure portfolio (+10.1% return), which benefited from the substantial gains of its large portfolio investments.

4. A proactive underweight in Equity portfolios.

Furthermore, the Equity Markets portfolios (with a -5.5% return) were negatively affected by the repercussions of Europe’s public finance crisis, China slowdown fears and U.S. economic uncertainty. New York’s S&P 500 dropped by 7.2% (in Canadian dollars) and Toronto’s S&P/TSX Composite fell 2.6% in the first half of the year. In May 2010, the Dow Jones Industrial also experienced its largest monthly decline since 1940.

Finally, the Real Estate portfolio posted a slightly positive return during the period, benefiting from the gradual recovery in sector fundamentals since July 2009. This recovery was more evident in Canada and the U.K. Other markets experienced more nuanced improvements. After a difficult period in 2009, shopping mall and office building sector returns were positive in the first half of the year. The hotel sector, however, continued to decline.

The table below provides more information on the Caisse's overall performance during the first half of 2010 according to the new specialized portfolio offer’s asset classes:

"Since we expect markets to remain turbulent, we will continue to monitor developments very closely and will be ready to respond quickly whenever it’s necessary,” added Mr. Lescure.

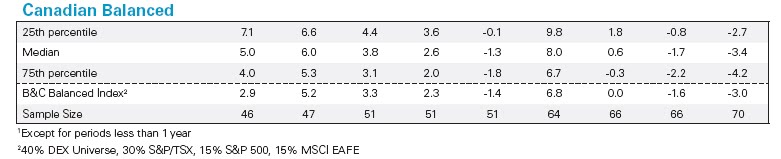

Anyway you slice it, these results are very impressive. How impressive? Take a look at the table below, taken from Brockhouse Cooper's Canadian Manager Universes for Q2 2010 (click on image to enlarge):

As you can see, the median return of Canadian Balanced funds was -1.7%, and the 25th percentile return was -0.8%. The Brockhouse Cooper Balanced Index (40% DEX Universe, 30% S&P/TSX, 15% S&P 500, 15% MSCI EAFE) delivered -1.6% during the first half of 2010.

Moreover, as noted in this CTV article, the Caisse outperformed its peers:

A survey by RBC Dexia has estimated that the assets of Canada's pension fund managers fell by 1.4 per cent in the first six months of 2010 due to faltering global equity markets.

The Caisse delivered 2.33% in the first half of 2010, compared to -0.74% for its overall portfolio’s benchmark index, outperforming its benchmark by 307 basis points (3.07%). Admittedly, private equity accounted for the bulk of the value added, but don't discount the value added from fixed income, infrastructure and tactical asset allocation.

The Caisse did take a negative 5.5% hit in its public equity markets portfolio, primarily due to the repercussions of Europe’s crisis, China slowdown fears, and US uncertainty, but public markets have stabilized since Q2 2010.

How do these results compare to CPPIB's results? The Canada Pension Plan Investment Board ended the FY 2011 first quarter with a loss on invested assets of $1.7-billion, or 1.3%. But these quarterly results do not take into account private markets which are only valued at the end of their fiscal year (March 31st).

The Caisse's fiscal year ends at the end of December and unlike other large funds, they report the performance of their private market holdings twice a year. As I stated before, the Caisse's benchmarks for private assets, especially real estate, are the toughest benchmarks among the large public pension funds.

You can read more on the Caisse's first half performance in the Globe & Mail, Digital Journal, the CBC, CTV, the National Post, and Bloomberg.

I continue to believe that the Caisse is on the right path. There is still a lot more work that needs to be done but you got to give Mr. Sabia and the senior managers at the Caisse the credit they deserve. These are very difficult markets to navigate through, and they are doing a great job, focusing on risk management, governance, and being nimble and opportunistic on asset allocation decisions. Let's hope they keep it up in the second half of the year.

Comments

Post a Comment