Protecting Pensioners of Traditional Defined Benefit Plans

In Canada, pension promises made to employees by employers are not guaranteed by insurance contracts. Rather, they are secured by requiring that the employer set aside assets in a pension fund independent of the employer, which delivers future pension promises should the employer lose the ability to support the pensions with enterprise assets.

Where the current system falls short, however, is when an employer goes out of business and a pension plan becomes wound up. Scenarios like this often run the risk that the assets set aside to deliver the promised pensions may not be sufficient, resulting in negative consequences for plan members, especially retirees who are without the means to replace lost retirement income from other sources.

The question begs: Is there is a better approach to addressing underfunded pension plans? We explore some potential answers in our paper Protecting Pensioners of Traditional Defined Benefit Plans: A New Approach to Solvency Funding and Benefit Reductions on Plan Wind-up, newly released as part of the CIA insight statement series.

Rethinking how we protect pensions

The current system for winding up underfunded defined benefit (DB) pension plans divides the segregated pension fund among all plan beneficiaries on a pro-rata basis according to the value of their pension entitlement. This means that if the available funds represent, for example, only 90% of the value of the collective promises, then each beneficiary sees a 10% reduction in their pension. This approach can leave older workers and retirees vulnerable.

Recognizing that older workers and retirees tolerate less risk, as there is less time and fewer options to remedy the negative impact of lost pensions, we suggest a new approach: rethinking the allocation of investment risk to members of DB plans.

Our proposal operates on the premise that retiree pensions would be better protected if the approach to solvency funding and benefit reduction rules acknowledged that younger workers tolerate greater risk and have more opportunities to recover from pension losses.

To this end, we suggest that governments consider the following changes to help protect older workers and retirees:

- Change solvency funding rules to target different solvency ratios for different categories of members and to determine different “tolerable” cutback levels in case of plan wind-up.

- Implement new risk sharing measures to reflect different risk levels tailored to different age groups.

- Allow entities to continue administering assets and benefits for any interested member who is retired or eligible to retire on plan wind-up.

- Implement a pensioners guarantee fund in all jurisdictions to limit cutbacks to prescribed “tolerable” levels.

- Allow interested members to make optional contributions or transfers from another vehicle to restore any portion of their benefit cutback on plan wind-up.

Recognizing that all plan members do not have the same appetite for the risks taken by the plan could lead to risk management measures that attribute experience gains and losses differently to different subgroups of plan members. What this means is that a plan could differentiate the risk levels desired on behalf of retirees in a certain age group versus active workers in a certain age group and determine different funded ratios for each group based on the experience gains attributed in reference to those desired risk levels.

Although there is no “silver bullet” that can solve all problems in the case of underfunded DB plans at wind-up, adopting some or all these changes could help to better protect older workers and retirees approaching and living in retirement.

Discussion questions

We would like to hear your comments and generate discussion that could help improve this proposal. Below is a list of possible aspects to address, although we invite you to focus on the ones that interest you most. Please note that all questions are intended for single-employer DB plans in the private sector.

- Do you think the paper’s proposals offer a realistic approach to dealing with solvency funding and benefit reductions on plan wind-ups?

- Is the proposal to increase solvency funding targets for older workers and retirees, while reducing them for younger workers, an improvement over the status quo?

- Is the proposal to tie benefit reductions to solvency funding targets (which vary by age) an attractive approach?

- What obstacles would you expect in implementing the proposed measures?

- What parts of the proposal are most appealing to you?

- What parts of the proposal would you reject?

- What alternative approaches would you suggest be considered?

- Do you think plan demographics should be a factor considered by the administrator in determining the level of risk included in its investment policy? Do you think many plans determine their level of investment risks based on their membership demographics? Do you think that when assets are commingled, then all members should share equally the gains and losses resulting from the overall plan risks? Do you think that attributing gains or losses differently to different member sub-groups on a notional basis is desirable or feasible?

- Do you agree that older members and retirees have less tolerance for a potential benefit cutback? Do you think this factor should be considered in determining how to allocate a plan’s wind-up deficit and cutback benefits? Do you agree that a member’s expected remaining lifetime is an indicator of their opportunities for taking future risks in the hope of making up cutbacks?

- Do you think that when members take risks individually after plan wind-up in the hope of making gains and offsetting their benefit cutbacks that they deserve to be the sole beneficiary of those gains because they also take an equal risk of suffering losses?

- Do you think it would be beneficial for retirees to participate in a run-out scheme that takes moderate risks for a few years before purchasing insured annuities? Do you think retirees who participate in a run-out scheme should be protected against potential losses from moderate risks by a guarantee fund, based on the proposed level of tolerable cutbacks? Or would you prefer a protection at a different level (e.g., 100% or some percentage of the tolerable cutbacks)? Do you think a run-out scheme should include the proposed group (i.e., members already retired or who choose to retire upon plan wind-up) and on an optional basis, or what would you prefer? Do you think the run-out scheme should attribute risks differently among its sub-groups? Do you think a run-out scheme should be administered by a government entity, by a plan administrator having fiduciary responsibilities, or by private commercial entities?

- Do you think members should be allowed to fund their own cutbacks with optional transfers from their individual registered accounts? Or in some different manner that you could suggest?

- Do you have any comments about other alternatives that are mentioned in the paper and about the reasons presented in the paper for not recommending them?

- Do you think some of the proposed measures could be appropriate for some types of plans other than those mentioned (i.e., single-employer DB plans in the private sector)?

Comment below to share your thoughts and keep the conversation going.

This article reflects the opinion of the author and does not represent an official statement of the CIA.

Please take the time to download and read this paper by clicking on the download button here.

This paper written by two top actuaries is excellent and offers many great insights.

The paper goes over the current weakness in plan solvency backstops and highlights the impact, particularly on older workers and retirees, of DB plan wind-ups where the plan assets are insufficient to pay all of the promised benefits.

It suggests that policy- makers should consider the various degrees of risk taken on behalf of different categories of plan members and the capacity of members to bear such risk.

I had a chance to talk to one of of the co-authors of this paper, Joe Nunes, last week to go over their findings and recommendations.

Let me first thank Joe for taking the time to talk to me and also thank Sandra Caya, Director, Communications and Public Affairs at the Canadian Institute of Actuaries for setting up the conference call and sending me the material.

Joe began by telling me the onus of this insight paper was simply this: "Is there a better way to protect older workers and retirees who are members of a corporate defined benefit plan in case the company goes bankrupt and the plan is wound up?".

The authors make a very persuasive case that policy and regulations should target the most vulnerable members of a corporate DB plan, ie older members who do not have the luxury of time to make up for any shortfall in pension savings if the plan winds up.

Below, I bring to your attention section 4.2 of the paper going over revised solvency funding targets (pages 13-16):

Rather than requiring pension plans to fund all solvency liabilities at 85%, solvency funding rules could define targets that are not uniform for different categories of members. Instead of a one-size- fits-all approach, this could involve differentiations based on certain eventual benefit reductions that could be mitigated by the members continuing to take some investment risk for the remainder of their life, considering that younger members have more capacity to make up larger cutbacks than older members. This is consistent with the view that a plan member who has been retired for many years needs better protection than a plan member who is still many years away from retirement.

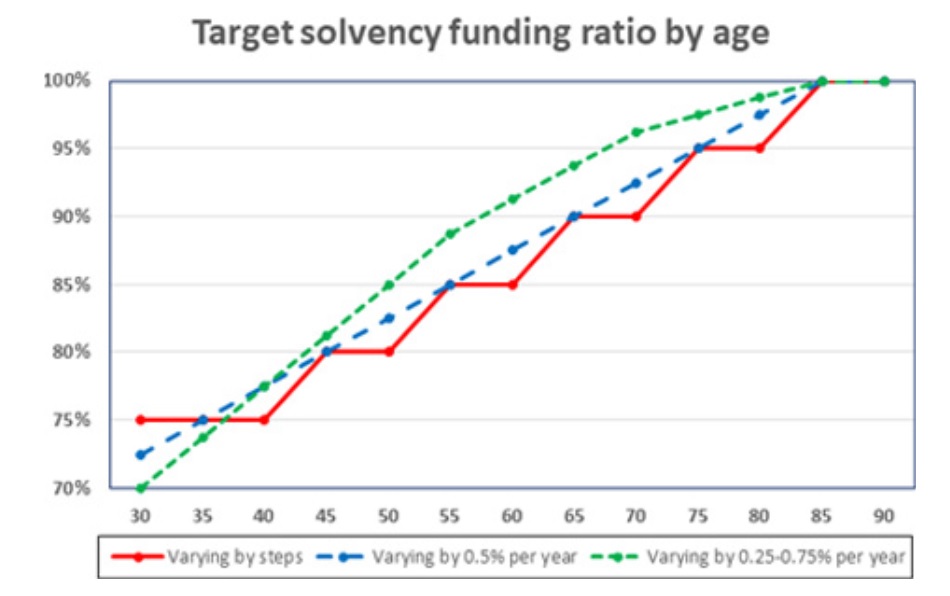

Here is an illustration of such differentiation based on varying the level of eventual benefit cutback that might be considered “tolerable” for different subgroups of members, given their presumed capacity to compensate those cutbacks by taking future investment risks:

For example, the solvency valuation for a retiree who is 70 years old would include only 90% of the benefits expected to be paid in the future, while for an active member who is 40 years old, the solvency target for that member’s future expected benefits would be 75%. Each actuarial valuation would need to calculate the target solvency liabilities separately for each member and then the total target solvency liability would be compared to the total plan assets to determine the deficit that is required to be funded and the amortization payments.Alternatively, the rules could stipulate that the tolerable cutback for each member is to be calculated as 0.5% times their remaining life expectancy (assuming most plan members are currently expected to live up to approximately age 85). For example, in a rather simplified fashion, someone at age 65 expected to have approximately 20 years left to live would be assigned a 10% tolerable cutback, while someone at age 35 expected to have approximately 50 years left to live would be assigned a 25% tolerable cutback. Such a tolerance of 0.5% per year left to live means that members would be assigned a target of 0.5% in average yearly investment gains to achieve over their remaining life expectancy, compared to the discount rate used to calculate their wind-up liability, representing the present value of their expected future pension payments.

However, we have already noted that younger members are usually willing to take more investment risk than older members, which means they would have a better chance of achieving future investment gains in early years than older members taking more limited risks. It might be more appropriate to vary the tolerance in benefit reduction over different stages of each member’s remaining life expectancy. Therefore, rather than using a fixed percentage of potential investment risk and gain for all future years, another variation that might be preferred by regulators could be to vary the annual percentage to reflect an investment mix that is more conservative at older ages. For example, the annual target investment gains used to calculate the tolerable cutback could vary from 0.75% below age 55 to 0.25% above age 70, with an intermediate rate of 0.50% between ages 55 and 70.

The following graph illustrates the different approaches mentioned above:

The resulting target to be funded by different plans would obviously vary depending on each plan’s distribution of liabilities by age groups (and depending on the levels of targets that are prescribed). Generally, a relatively more mature plan could have an overall target close to 90% while a relatively less mature plan could have an overall target close to 85%.The following table shows the estimated results for two plans with substantially different liability distributions (based on the above option with targets varying by steps):

I must admit, the rationale behind these proposals makes a lot of sense to me from a practical and theoretical viewpoint.

In particular, if the aim is to protect the most vulnerable members if the plan winds up for any reason, then why not target solvency funding ratio by age to better protect older members?

Of course, I couldn't resist but share this paper with two of Canada's foremost actuaries, Bernard Dussault, Canada's former Chief Actuary and Malcolm Hamilton who was a partner at Mercer for many years before retiring.

Let me begin with Bernard's feedback first:

I still have to make a second reading of the second half of the CIA paper but thought you might appreciate having as soon as possible my comments thereon.

This CIA paper “ … suggests that retiree pensions would be better protected if the solvency funding regime framework and the benefit reduction rules on wind-up recognized the premise that younger workers can tolerate greater risk and have more opportunities to recover from pension losses“. I do not agree with this suggestion because my view is that protection and risk tolerance should not prevail over equity. The value of one’s pension should in any event relate to its present actuarial value (PAV), which depends on age, sex and amount of accrued pension and valuation assumptions such as mortality, indexation and investment yield, rather than exclusively to age. In other words, the allocation of an outstanding partial fund upon plan wind-up should be in proportion to the PAV of each member’s accrued pension, measured using the assumptions used in the actuarial valuation report. The remaining fund could then survive until the last member’s or survivor’s death or used to purchase private guaranteed annuities.

I pursue as follows in point form my further comments (consistent with my attached proposed financing policy for Defined Benefit pension plans) on the CIA paper.

- “Allow entities to continue administering assets and benefits for any interested member who is retired or eligible to retire on plan wind-up.” is a very good and better alternative to above allocation but should apply to ALL MEMBERS.

- I am not in favour of:

- guaranteed (by government or else) funds because they increase the pension contributions while not fully guaranteeing the benefits it might (if not does) invite to anti-selection (i.e. plan sponsor thereby not as much or no longer interested/concerned in the investment risk)

- solvency valuation because they require that the assumed yield on investment be set as if all of the pension fund were invested in bonds, which unrealistically largely increases the pension plan debt and thereby the special (debt amortization-related) contributions, which happens to be the main cause of the volatility in the amount of contributions from one year to the next.

- Business insolvency laws should give priority to the unfunded portion of the pension obligations even if the sponsoring of private pension plans by employers is voluntary (not mandatory) because pension credits/accruals become member’s ownership as soon as they are paid for..

- Contribution holidays should not be allowed in any event, e.g. using actuarial surplus to reduce contributions required of employers, because they correspond to an improper withdrawal of surplus.

- The Income Tax Act (ITA) of Canada overarching rule that restricts employer contributions when the amount of surplus exceeds a certain limit is reasonable though imperfect, as it should compel that any such excess of scheduled contributions or pension fund be directed to an account to be used eventually exclusively for pension purposes, e.g. a return to the pension fund if and when the pension plan’s current surplus no longer exceeds the ITA “certain limit”.

- Investment risks: The approach used from several large Canadian private pension plans of prudently investing net contributions in large diversified (e.g. 75% in equities, no more than 10% in secured liquid funds) portfolio works so well in the long run that a any reduction in equity investments in order to reduce contributions volatility is not appropriate, as it reduce average long term return on the fund and consequently increase the required level of contribution. Besides, mature plans might in some cases require more than 10% of secured liquid funds.

- I take this opportunity to

- attach an email array pertaining to the assumptions prescribed by the Canadian Institute of Actuaries for the valuation of commuted (transfer) values. This is relevant to pensioners’ security because these assumptions contribute to lowering a plan funded percentage (ratio of the plan fund to its liabilities).

- Ask Malcolm whether he knows the answer to my question, i.e. “Upon what principle is based the setting of specific assumptions for the calculation of Commuted Values”. In the email array, the CIA President states “I do not agree with your proposal that CV should be based on assumptions selected by each actuary in his actuarial valuation. This would lead to the CVs being calculated according to a wide range of assumptions at the discretion of each actuary. This would not be a good public policy and I can tell you that it would likely not be tolerated by the regulators. Your concern about the effect on the possible reduction in funding ratio is valid. But, each regulatory authority has taken measure to address this concern.” What would be the regulators’ concern about using assumptions subject to same CIA rules as those applying to the valuation of pension plans?

- FYI, as a matter of semantics: I am surprised that in the pension world, the word “(pension plan) deficit” is generally (if not always) improperly used to refer to “(pension plan) debt”.

I also asked Malcolm to share his thoughts on this paper:

I am familiar with this Insight Statement as I reviewed two earlier drafts. Nunes and Charbonneau are excellent actuaries. Their analysis is thorough; their opinions are clearly expressed; their recommendations, with which I disagree, are well-intentioned and controversial.

Before sharing my concerns I will make four points of a general nature.

- Insight Statements represent the opinions of the authors, not the opinions of the actuarial profession or the majority of actuaries. The authors' opinions are presumably shared by some of the actuaries who approved the statement's publication. Beyond this, not much can be said.

- The statement addresses the benefits paid by private sector pension plans that are terminated with insufficient assets by insolvent plan sponsors. It is not an issue for public sector pension plans or for defined contribution pension plans. It is usually not an issue when interest rates are at the levels we once considered normal.

- Defined benefit pension plans are not funded through "allocated" funding instruments. There is no allocation of contributions, expenses or investment income to individual members. The fund is held for the collective benefit of all members. The members are entitled to the benefits set out in the plan document, not to an identifiable share of the pension fund.

- When a pension plan winds up, we can determine the market value of the assets and we can determine the amount needed to pay everyone the benefits they are owed. If the assets are insufficient we can determine the extent of the shortfall as a percentage of the market value of the assets but we cannot actuarially allocate this money to individual members. The obvious, simple, understandable and apparently fair way to do this is to pay all members the same percentage of the amount they are owed. For example, if the assets cover 80% of the plan's wind up liabilities then every member will receive 80% of what they are owed. This is what the law requires and what the authors question. It is also, of necessity, arbitrary.

The paper makes many good points and useful suggestions. I will not attempt to summarize these. It will be remembered for proposing that older members, in particular retired members, receive preferential treatment if the plan's assets are insufficient to cover its wind up liabilities. This preferential treatment will be at the expense of younger members. The justification first appears at the bottom of the first page.

"As workers age and, in particular, after workers retire, they can tolerate less risk since there is much less time and many fewer options available to remedy the negative impact of lost pensions."To remedy this the authors advocate larger reductions for younger members to pay for smaller reductions for older members. The methodology is neither easily explained nor easily understood. If a plan is 80% funded upon windup, pensioners over the age of 85 would keep their full pensions (vs. the 20% reduction imposed by the current rules). To pay for this, active employees approaching retirement (55 to 64) would have their reductions increased from 20% to , say, 30%. The reduction for members under 45 would jump from 20% to 50%.

The authors believe that their proposal is transparently reasonable and that it will be accepted enthusiastically by elderly pensioners and, hopefully, begrudgingly by younger members. I respectfully disagree. The proposed rules are quite complicated and entirely arbitrary. They are unlikely to be embraced by those they harm. More importantly, why do we think that the current approach treats older members unfairly?

Who has the most to lose when a pension plan winds up with insufficient funds? It isn't the youngest members - they haven't been in the plan long enough to earn much of a pension, hence they have little at risk. It isn't the oldest pensioners - they have been drawing full pensions for decades and have already recovered most of what they were owed at retirement. The group most at risk is the group that recently retired and the group that will soon retire. They have worked for decades to earn their pensions and, so far, have received little or nothing. Now they are without a job and relying on the pension plan for three decades of income. The authors say that these members are better able to cope with the loss of part of their pension than are much older members because they have more time and more options for remedying the loss. This is wishful thinking at best. They are unemployed and in their 60s. Their education, training and experience may not compare favorably to younger candidates for the jobs they must seek. If they commute their pensions they are looking at negative real interest rates, over-priced stock markets and predatory financial institutions to deliver the opportunities they need to mitigate their losses.

An older pensioner losing 20% of a pension that might be paid for another 5 years loses one year of pension income. A recently retired member losing 20% of a pension that might be paid for another 25 years loses 5 years of pension income. It's the same 20% but 5 times the loss because the recently retired pensioner has 5 times the life expectancy and 5 times the exposure. I have a hard time seeing how reducing the older pensioner's loss to zero and increasing the younger pensioner's loss to 7.5 years of pension income is a step in the right direction.

The status quo has several advantages - precedent, simplicity, clarity and a superficial equity. The proposed approach has none of these unless you buy the notion that elderly means vulnerable and deserving of preferential treatment. Once we decide to go down that road we will discover that it is a road without end. Aren't women more vulnerable than men (longer life expectancy, lower income)? Perhaps we should take income into account, or net worth, or home-ownership, or health, or the ability to turn to family for financial support.

Age is a very blunt instrument on which to hang an assessment of vulnerability.

WOW! Absolutely great insights from Malcolm and Bernard and I thank them dearly for sharing them with my sophisticated audience.

I cannot share anything on the actuarial merits of this paper and certainly cannot match the brain power of these two titans, but let me share some things I did mention to Joe Nunes.

I'll also tell you right away Malcolm will not agree with my recommendation.

What I told Joe is I'd like to see the creation of another (alas!) large, well-governed federal public pension fund that amalgamates all the assets of Canadian corporate defined-benefit plans, offloading the risk of these plans from companies to the federal government's balance sheet.

"Well, Leo, how Trudeau-esque of you, that's all we need, another large Canadian pension fund backstopped by the federal government."

Hear me out. There's no arguing that Canada has some of the best, if not the best pension investment managers and pension plans in the world.

We got the governance right, the risk-sharing right, the approach right allowing these pension managers to run their operations internally, significantly reducing costs.

In other words, why are we trying to tinker with policy to ensure every member of a corporate defined-benefit plan can retire in dignity and security?

Let's focus on what we know works well and do the right thing over the long run.

Joe Nunes heard me out but he wasn't sure we need to create another large federal pension fund. "We already have CPP Investments and smaller plans like CAAT (DBplus) and OPTrust (Select) that can do this."

I am all for the success of the plans but my thinking was do something that focuses exclusively on corporate DB plans and since CPP Investments is already huge and caters to so many Canadians, I think it makes sense to start something new here.

Anyway, I've rambled on long enough, hope you enjoyed the great actuarial insights in this post.

Once again, I thank Joe Nunes, Sandra Caya, Bernard Dussault and Malcolm Hamilton.

Below, Susan Daley explains the nuances and advantages of defined benefit pension plans.

Comments

Post a Comment