Sell The Rip on Wall Street and Thoughts From Davos

U.S. stocks rallied to close higher on Friday, as the S&P 500 and Dow snapped a three-session losing streak and the Nasdaq rose more than 2%, as quarterly earnings helped lift Netflix, while Google parent Alphabet climbed after announcing job cuts.

Shares of Netflix Inc jumped 8.46% as the streaming company added more subscribers than expected in the fourth quarter and said co-founder Reed Hastings was stepping down as chief executive.

Netflix's quarterly report comes as the technology and other growth-related sectors face hurdles due to the rising interest rate path of the U.S. Federal Reserve and recession worries that have led companies such as Microsoft Corp and Amazon.com Inc to lay off thousands of employees.

Alphabet Inc was the most recent company to announce job cuts as it said it was cutting 12,000 jobs, sending shares 5.34% higher.

The gains sent the communication services index up 3.96% as the top performer among the 11 major S&P 500 sectors, notching its biggest daily percentage gain since Nov. 30.

High-growth sectors such as communication services were among the worst performing in 2022 and were notably weaker in the last few months of the year as investors gravitated towards stocks with high dividend yields.

"Today’s action is probably because we had three down days so it got into a little bit of an oversold position and they are just doing a little bit of bargain hunting today," said Ken Polcari, managing partner at Kace Capital Advisors in Boca Raton, Florida.

"If people are viewing an opportunity, if they are getting more comfortable with the Fed’s narrative... investors are starting to buy into that narrative and saying 'OK that is the way it is, let’s look at the stocks that got really beaten up' because the market is a discounting mechanism."

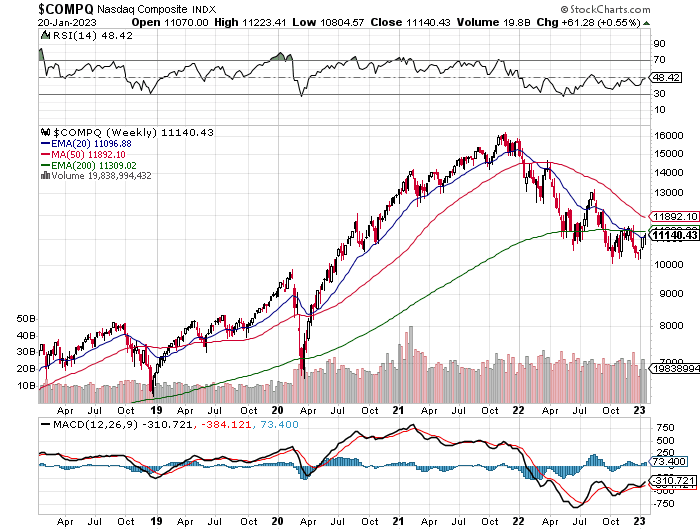

The Dow Jones Industrial Average rose 330.93 points, or 1%, to 33,375.49, the S&P 500 gained 73.76 points, or 1.89%, to 3,972.61 and the Nasdaq Composite added 288.17 points, or 2.66%, to 11,140.43.

For the week, the Dow lost 2.7%, the S&P 500 shed 0.66% and the Nasdaq gained 0.55%.

Comments from Federal Reserve officials have largely said they expect interest rates to climb to at least 5% this year as the central bank continues to try and tamp down high inflation. On Friday, Fed Governor Christopher Waller said the central bank may be "pretty close" to a point where rates are "sufficiently restrictive" to cool inflation, which gave an additional boost to equities.

The Fed is largely expected to raise rates by 25 basis points (bps) at its Feb. 1 policy announcement.

Still, concerns about corporate earnings persist as the U.S. economy shows signs of a slowdown and a possible recession.

Analysts now expect year-over-year earnings from S&P 500 companies to decline 2.9% for the fourth quarter, according to Refinitiv data, compared with a 1.6% decline in the beginning of the year.

Gains on the Dow were curbed, however, by a 2.54% fall in shares of Goldman Sachs Group Inc after the Wall Street Journal reported the Fed was probing the company's consumer business.

Volume on U.S. exchanges was 11.90 billion shares, compared with the 10.87 billion average for the full session over the last 20 trading days.

Advancing issues outnumbered declining ones on the NYSE by a 3.55-to-1 ratio; on Nasdaq, a 2.63-to-1 ratio favored advancers.

The S&P 500 posted one new 52-week high and four new lows; the Nasdaq Composite recorded 77 new highs and 20 new lows

Tanaya Macheel and Carmen Reinicke of CNBC also report stocks close higher Friday, Nasdaq notches third straight week of wins:

Stocks rallied on Friday to finish the week strong after briefly losing the momentum of the January rally.

The Dow Jones Industrial Average added 330.93 points, or 1%, to close at 33,375.49, while the S&P 500 advanced 1.89% to 3,972.61. Both indexes snapped a three-day losing streak. Meanwhile, the Nasdaq Composite rose 2.66%, with help from Netflix and Alphabet, to end the day at 11,140.43.

The Nasdaq was also the outperformer for the week, posting a 0.55% gain and its third positive week in a row. The Dow finished the week lower by 2.70%, and the S&P posted a 0.66% loss, both breaking two-week win streaks.

All of the major averages are still in positive territory for the year.

“We’re having a more emotional reaction that expected,” said Jeff Kilburg, founder and CEO of KKM Financial. “A lot of people got so pessimistic and we saw parabolic moves to kick off the year. Now, as expected, the markets aren’t going in a straight line.”

“We are finding a way to continue to move and have higher lows,” he added. “The higher lows put a little bit of confidence in the bulls. However, the technicals are still favoring the bears and selling rallies.”

Investors continued to monitor earnings reports and mega cap tech shares led the market higher. Netflix gained about 8.5% after posting more subscribers than expected even though its quarterly earnings missed analysts’ estimates. Alphabet rose more than 5% after the company announced it will lay off 12,000 employees.

“You’re seeing more weight go into some of the beat-up technology and because people are becoming a little bit more thoughtful of opportunity in the absolute tech wreck we saw in 2022,” Kilburg said.

Lewis Krauskopf of Reuters also reports a spate of earnings reports in coming weeks is set to test a recent bounce in technology and other megacap stocks, a category whose leadership position in U.S. markets has faltered after last year’s deep selloff:

The tech-heavy Nasdaq 100 index (NDX) has gained over 3% in 2023, double the rise for the S&P 500 (SPX). Shares of some megacap companies - which include those grouped outside of tech in sectors like communication services and consumer discretionary - have shot higher, with Amazon (AMZN), Meta Platforms (META) and Nvidia (NVDA) posting double-digit percentage increases.

Several factors are driving that outperformance, including investors piling into stocks they believe were overly punished in 2022. A moderation in bond yields, whose jump last year particularly pressured tech-stock valuations, is also likely helping the group, investors said.

Now, however, the focus is shifting to whether these companies can withstand a widely expected economic downturn while supporting valuations that some investors believe are too high.

"To keep this rebound going, the guidance for ’23 has to be less worse than what people are anticipating," said Peter Tuz, president of Chase Investment Counsel, whose firm recently pared its holdings in Apple (AAPL) and Microsoft (MSFT).

Tech and growth stocks led U.S. equity markets for years following the 2008 financial crisis, aided by near-zero interest rates. They struggled along with broader markets last year as the Federal Reserve raised rates to fight surging inflation, and some investors doubt they will regain the market's pole position any time soon. The Nasdaq 100 fell 33% in 2022, while the S&P 500 lost 19.4%.

The top six stocks by market value in late 2021 - Apple, Microsoft, Alphabet (GOOGL), Amazon, Meta and Tesla (TSLA) - have seen their collective weight in the S&P 500 fall from 25% to 18%, according to Strategas Research Partners.

That dynamic echoes a pattern seen after the market’s dot-com bubble burst after the turn of the century. The six biggest stocks at that time saw their collective weight in the S&P 500 decline to 5% from a peak of 17% over a number of years, according to Strategas.

"This leadership unwind ... is going to be one that is measured in years, not in months or quarters," said Chris Verrone, head of technical and macro research at Strategas.

EARNINGS TESTCompanies comprising over half the S&P 500's market value are due to report results in the next two weeks, including Microsoft, the second-largest U.S. company by market value, on Tuesday, Elon Musk's Tesla and IBM (IBM) on Wednesday and Intel (INTC) on Thursday. Apple, the largest U.S. company by market value, and Google-parent Alphabet report the following week.

Fourth-quarter earnings in the tech sector are expected to have declined 9.1% from a year ago, compared to a 2.8% decline for S&P 500 earnings overall, according to Refinitiv IBES.

A critical question for many megacaps, once heralded for their stellar growth, is whether they can increase revenue and profits significantly while cutting costs in the face of a possible recession.

Alphabet Inc (GOOGL) said Friday it is cutting about 12,000 jobs, or 6% of its workforce, the latest tech giant to announce layoffs. Microsoft on Wednesday said it would eliminate 10,000 jobs while Amazon started notifying employees of its own 18,000-person job cuts.

"The biggest positive could be if they could show a control of expenses while keeping at least reasonable growth intact," said Rick Meckler, partner at Cherry Lane Investments in New Vernon, New Jersey. "It’s a hard balancing act."

Valuations for tech and megacap companies have moderated after last year's selloff, though they still stand above those of the broader market. The S&P 500 tech sector still trades at a roughly 19% premium to the broader index, above its 7% average of the past 10 years, according to Refinitiv Datastream.Nonetheless, some investors are reluctant to bet against tech stocks.

The Wells Fargo Investment Institute counts tech as one of its favored U.S. sectors.

The firm expects an economic downturn and believes many tech companies have businesses that are resilient to economic uncertainty, said Sameer Samana, a senior global market strategist there.

"It’s just too important and too big a weighting not to participate," Samana said. "But the years of handily outperforming the S&P are probably now behind us.”

In related news, Reuters reports that BOJ Governor Haruhiko Kuroda, who addressed the World Economic Forum in Davos, Switzerland, said the central bank will maintain its "extremely accommodative" monetary policy to achieve its 2% inflation target in a stable, sustainable manner:

Alright, it's Friday and I will try to keep it short.In currencies, the dollar shot up against the yen after the BOJ governor's remarks.

The dollar rose as high as 130.60 yen and was last up 0.9% at 129.51. The greenback had its biggest percentage gain since early January.

"There are some doubts within the BOJ whether the boost in inflation in Japan is going to deliver them all the way back to 2%," said Thierry Wizman, global FX and rates strategist at Macquarie in New York.

At the same time, investors are debating whether the Federal Reserve's aggressive approach to tightening monetary policy to battle inflation might push the U.S. economy into recession.

U.S. Treasury yields rose as investors considered whether the Fed is likely to keep raising rates as far as it has indicated. Also, investors bet that a recent bond rally may be overdone in the near term.

Benchmark 10-year yields were last at 3.482%, after falling to 3.321% on Thursday, the lowest since Sept. 13 and just above its 200-day moving average. The yields have dropped from 3.905% at year-end, and from a 15-year high of 4.338% on Oct. 21.

In energy, oil prices rose and registered a second straight weekly gain as China's economic prospects improved.

Brent crude settled at $87.63 a barrel, up $1.47, or 1.7%. U.S. crude settled at $81.31 a barrel, gaining 98 cents, or 1.2%.

The same goes for the broader market, smart money is shorting it at these levels:

There are a lot of reasons why I remain bullish on the greenback but the big gains were made last year.

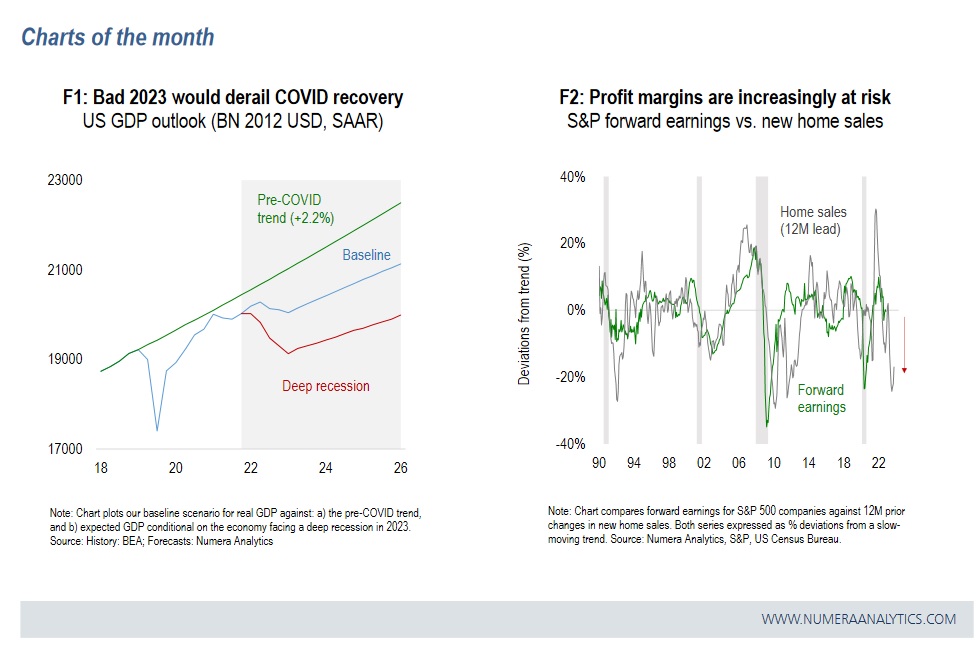

During the fall of 2021, we warned that the US economy’s rapid transition from reflation to overheating worsened the appeal of 60/40 portfolios. The key risk, as we correctly anticipated, was a surge in long term yields in response to high inflation and Fed tightening – weighing heavily on valuation sensitive ‘growth’ stocks.While no long only strategy delivered positive real returns in 2022, rotating away from tech and nominal bonds in favour of ‘value’ and defensive names helped limit portfolio losses. Risky assets today are trading at much cheaper valuations, which in combination with decelerating inflation has fueled a mini rally over the past few months.

The macro context, however, makes a sustained ‘bull’ run an unlikely outcome. In particular, our research points to a sharp slowdown in activity in 2023 and 2024 (F1), with persistently high inflation limiting the extent of Fed support. A weak earnings outlook (F2) and limited upside for valuations call for active sector and style rotation to generate strong returns.

If you don't know them, I suggest you subscribe to a free trial and learn more about Montreal-based Numera Analytics, they're truly excellent providing great macro research covering the world.

In his latest weekly commentary, A Sneak Peek Into Doctor Housing’s Portfolio For 2023, Francois Trahan notes in the email he sent out this morning:

Apologies for publishing a day later than usual this week, but I am back on the road meeting with clients. These face-to-face meetings are giving me a good sense of sentiment, and it’s clear that conditions have changed from a few months ago. Truth be told, pitching the bearish story had become fairly easy last September. Today, it is met with more questions, concerns, and doubts. It seems that investor consensus went from believing we are facing a recession to now thinking that any recession would be mild, or we may even get away with a soft-landing scenario.

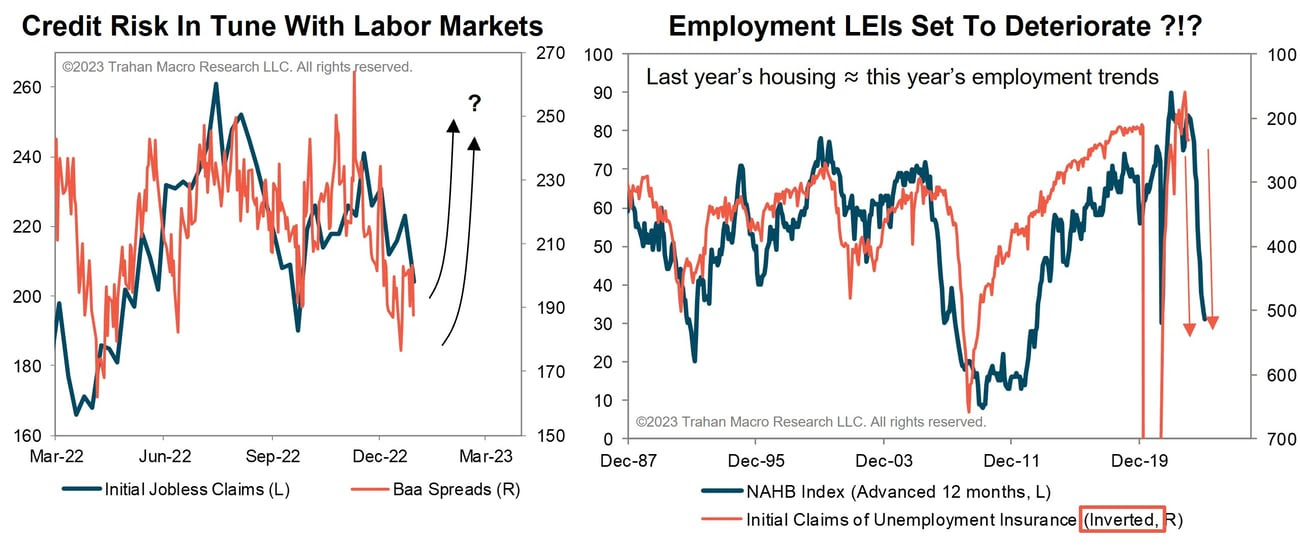

The short-term gauges we track argue that the bear market rally will likely end in the next 2-4 weeks and give way to a renewed downtrend in equities. This development should also help revert investors’ expectations back to the realities ahead: the dire economic outlook is the result of the most aggressive Fed tightening cycle in generations. Contrary to popular belief, the peak in headline inflation is not what has been driving equities higher these last few months. This is a story that everyone wants to be true as it implies better days ahead but unfortunately that is not the case.The driver of risk today is the economy. The market is fearful of slower growth. The chart above shows that credit spreads correlate best with Initial Claims and in all honesty the relationship is not in the direction we expected. Spreads are widening with every uptick in claims (and vice versa) thus pressuring P/Es. This is a market that fears a recession, and that outcome begins with weaker labor markets. The early-cycle housing industry (see chart above right) paints a grim view of Initial Claims and dictates a VERY bearish outlook for stocks. Today's report looks at what housing has to say about the economy, inflation, and of course financial markets.

Francois has posted a lot of great insights on Twitter here to back up his claims.

I showed the link earlier between housing and equity markets. The meltdown seen in leading indicators of housing point to a difficult year in markets and cyclical sectors especially. Housing will need to bottom before we can start to think about the low point of the recession. pic.twitter.com/ywhY75lRxM

— Francois Trahan (@FrancoisTrahan) January 21, 2023

Dr. Housing says the bear market rally is running on fumes! Time to sell cyclicals and buy things that make you yawn (Defensives)?

— Francois Trahan (@FrancoisTrahan) January 21, 2023

In the Macro Specialist Designation we discuss the usefulness of housing in forecasting the economy. This is especially true going into a downturn. pic.twitter.com/PAZk8B68r4

Don't get too excited about EPS reporting season ... the outlook is pretty terrible (see ISM advanced 12 months!). This might be the last positive quarter we see for quite some time. Just sayin'. pic.twitter.com/Qb1NoTDZPD

— Francois Trahan (@FrancoisTrahan) January 19, 2023

Here is a chart on housing you should all keep in mind:

Chart for future history books 👇 ht @Karl_Schamotta pic.twitter.com/WicIgwUp40

— Michael A. Arouet (@MichaelAArouet) January 21, 2023

As for me, I maintain that the Fed might even hike by 50 basis points at its next two meetings, although given recent inflation data came in better than expected, the market is pricing in two 25 bps hikes and then a long pause.

Still, if you look at financial conditions, don't be surprised if the Fed hikes by 50 bps at its next meeting:

And just like that financial conditions are where they were before rate hikes👇 (BBG) pic.twitter.com/PatXGc5KXB

— Michael A. Arouet (@MichaelAArouet) January 21, 2023

I also maintain the big risk this year is that wage inflation starts rising as the economy starts slowing.

So forget about headline inflation, keep your eyes peeled on wage inflation in the US and rest of the world.

In fact,Will Daniel of Bloomberg reports that top economist Mohamed El-Erian sees

inflation getting ‘sticky’ at 4%—and a growing chorus sees the dawn of a

new world in investing:

After raging to multiple four-decade highs in 2022, inflation has fallen steadily over the past six months. But now, an increasing number of economists and business leaders are worried that the trend won’t last. “I think inflation is going to get sticky in midyear at around 4%,” Mohamed El-Erian, the president of Queens’ College at the University of Cambridge, told Bloomberg on Friday.

The economist has been warning about the possibility of persistent inflation since August of last year, but he’s not alone anymore. Christian Ulbrich, CEO of JLL, a real estate and investment management firm, told the Financial Times this week that at the World Economic Forum in Davos, Switzerland, it was a common view among his executive peers that 4% inflation is the new 2% inflation.

Ulbrich believes that there are “a lot of fundamental trends”—including the decoupling of the U.S. and Chinese economies and the move toward green energy—which could even keep inflation “persistently around 5%.” You may think that’s a small difference, but two to three percentage points is a big deal when it comes to inflation.

Over the past decade, barring a brief blip in 2018, investors and businesses have become accustomed to extremely low borrowing costs that fueled soaring home and equity prices. But a world with 4% or 5% annual inflation would force central banks to keep interest rates higher for a longer duration, and that would probably have a ripple impact on stocks, further freeze the housing market, and force some corporations that skated by in the easy money era—the so-called “zombies” with high debt loads and weak cash flows—out of business. In short, it would be a very different financial world. Other economists’ and market watchers' comments indicate a growing consensus that this new world is coming into view.

The new inflation

Beyond global inflationary issues like the green energy transition, El-Erian explained that there’s been a shift in the main drivers of U.S. inflation in recent months that could prevent the Federal Reserve from hitting its 2% inflation target this year.

In 2022, inflation was mainly caused by rising goods, energy, and food prices. But now, the economist says that “mounting wage pressure” and rising prices in key areas of the services sector—including medical care and transportation costs—are driving price increases.

“This transition is particularly noteworthy because inflationary pressures are now less sensitive to central bank policy action,” he wrote in a Bloomberg op-ed Tuesday. “The result could well be more sticky inflation at around double the level of central banks’ current inflation target.”

In 2022, Fed officials raised interest rates seven times in order to tame inflation. And lately, their efforts have helped slow the steady rise of consumer prices, but El-Erian believes that central bankers don’t have the tools to efficiently fight inflation in parts of the services sector.

Some sectors of the economy are more readily influenced by rising interest rates than others. Take housing: When the Fed raises rates, mortgage rates follow, and that increases the cost of buying a home. It’s a sector that the central bank can have a very direct impact on, very quickly. The services sector isn’t the same.

When the Fed raises interest rates, things like medical care costs don’t immediately reprice like mortgage rates do. That’s partly why overall inflation rose 6.5% year-over-year last month, but services sector inflation when excluding volatile energy costs rose 7%, and transportation services costs—which includes things like bus and airfares—rose 14.6%, according to the Bureau of Labor Statistics.

El-Erian is also worried that core inflation, which excludes volatile food and energy prices, could prove difficult to tame because businesses are less likely to cut prices once they’ve been raised, even if their costs are falling. To his point, core inflation rose 0.3% month-over-month in December, while overall inflation fell 0.1%.

Lisa Shalett, chief investment officer of Morgan Stanley Wealth Management, also fears inflation could get stuck at 4%, and she laid out three main reasons why in a Wednesday article. First, the CIO warned that energy costs could rise over the next six months. Morgan Stanley is predicting oil prices will jump more than 20% to $107 per barrel by the third quarter of this year, and falling oil prices have helped push inflation lower in recent months.

Second, Shalett said the fading strength of the U.S. dollar could cause import prices to rise, exacerbating inflation. And third, “structural labor shortages” might lead to persistent inflation in parts of the services sector like El-Erian is worried about, she warned.

“The implication of these risks, along with many investors’ failure to acknowledge them, is that core inflation is unlikely to decline in a straight line through year-end toward the Fed’s target of 2%,” the wealth management veteran wrote. “Rather, the decline is more likely to stall out mid-year, with inflation staying closer to 4%—a development that could keep rates higher for longer and markets possibly stuck in a volatile waiting game.”

Former Treasury Secretary Larry Summers also warned at the World Economic Forum in Davos on Friday that inflation could get stuck above the Fed’s target.

“Inflation is down, but just as transitory factors elevated inflation earlier, transitory factors have contributed to the declines that we’ve seen in inflation and as in many journeys, the last part of a journey is often the hardest,” he told CNBC.

Summers argued that “the greatest tragedy” would be for central banks of the world to stop fighting inflation too early, arguing that we do not want to “fight this battle twice.” And El-Erian said on Friday that the Fed should raise rates by 50 basis points in February—instead of the widely expected 25 basis points—to fight sticky core inflation now instead of waiting until “the economy weakens,” arguing that slower rate hikes are more likely to cause a recession.

George Ball, chairman of the Houston-based investment firm Sanders Morris Harris, thinks we are in a new world, inflation wise. “I think you occasionally get a turning of the investment and economic age,” he told Fortune last month, “and we’re at one of those now after over a decade of near-zero interest rates.”

I agree with Larry Summers, a 1970s crisis awaits us if central banks relent on rates:

Summers Warns of 1970s Crisis If Central Banks Relent on Rates https://t.co/0MGGPXGi03 via @YahooFinance

— Leo Kolivakis (@PensionPulse) January 20, 2023

Going soft on inflation will plunge economies back into the recessionary depths of the 1970s and have “adverse effect on working people everywhere,” former US Treasury Secretary Larry Summers warned.

The remark is a response to suggestions from economists including Olivier Blanchard, a former International Monetary Fund chief economist, who have suggested lifting inflation targets from 2% to 3% to avoid recessions.

“To suppose that some kind of relenting on an inflation target will be a salvation would be a costly error, it would ultimately have adverse effect as it did in a spectacular way during the 1970s,” Summers, a professor of economics at Harvard and a Bloomberg TV contributor, told a panel at the World Economic Forum’s annual meeting in Davos, Switzerland.

Federal Reserve Chair Jerome Powell has repeatedly made clear that the US central bank has no plans to change its 2% inflation target.

Inflation peaked in double digits across much of the industrialized world but is expected to drop rapidly this year on the back of falling energy and commodity prices. However, core inflation will remain elevated as wage behavior and companies’ price setting has fundamentally changed, Swiss National Bank Chairman Thomas Jordan said on the same panel.

“It will be much more difficult to bring inflation from 4% to 2%,” he said. “We will see if that comes with a recession or not. Firms do not hesitate any more to increase their prices. That is different from two or three years ago and is a signal that it is not that easy to bring inflation back to 2%.”

“We also see a change in the behavior regarding wages. If you look at wage formation, this is very backward looking. Basically we take inflation from last year and we use this to set future salaries – the kind of fairness argument. Once inflation is high, the pressure from wages is here.”

Summers warned: “It would be a grave error for central banks to revise their inflation target upwards at this point. Having failed to attain the 2% target and having re-emphasized repeatedly the commitment to 2%, to then abandon the target would do very substantial damage to credibility. If you can adjust once, you can adjust again.”

“The counter-factual is not, ‘can we have more inflation and no recession, it is, ‘if we fail to deal with inflation, we are likely to have a more severe recession at some point.’”

Central bank chiefs on the panel all agreed that tighter monetary was still needed to bear down on inflation, which still close to 10% in the US, the Eurozone and the UK.

Summers also criticized central bankers’ operation of quantitative easing during the pandemic, which he said has added to the burden on taxpayers. Under QE, central banks were effectively swapping long-dated debt for very short-dated debt just as “every corporate treasurer in the world was terming out its debt” to take advantage of low interest rates.

The Fed is now carrying a mark-to-market loss on its balance sheet of around $800 billion, he said.

“In retrospect, I think that was highly problematic,” Summers said. “We need in addition to thinking about the stimulative aspects of QE to focus on the balance sheet debt maturity aspects of QE.”

I actually discussed all this an more in a post on LinkedIn here and got many comments and replies worth reading.

Below, Harvard Professor and former U.S. Treasury Secretary Larry Summers shares his thoughts on the economy's journey from secular stagnation to runaway inflation, and where central banks go from here. Take the time to read my LinkedIn post here and see al the comments.

Summers also explains why a potential US debt default could be so catastrophic, and on a potential soft landing, says sometimes "hope does triumph over experience.

Third, Blackstone CEO Steve Schwarzman said the US needs a new raft of leaders in both political parties. He spoke to Bloomberg from the World Economic Forum in Davos.

Fourth, Carlyle Group Co-Founder David Rubenstein joins Yahoo Finance Live anchors Brian Sozzi and Julie Hyman to discuss market uncertainty, investor sentiment, M&A dealmaking, and the outlook for the U.S. economy.

Fifth, Jamie Dimon, JPMorgan Chase chairman and CEO, joins 'Squawk Box' to discuss Dimon's thoughts on the economy, what Dimon is advising clients at this time and the United States' relationship with China.

Sixth, David Solomon, Goldman Sachs CEO, joins 'Squawk Box' to discuss what happened with Goldman's quarterly earnings results, the company's book value, and more.

Seventh, "We've gone through an easy period for the last 14 years and I believe that the coming period will be a harder period," Howard Marks, Oaktree Capital Management co-chair, says. Speaking with Carol Massar and Tim Stenovec on "Bloomberg Businessweek," Marks also discusses the state of the distressed debt market.

Ninth, NYU Professor Nouriel Roubini joins Yahoo Finance Live anchors Julie Hyman and Brian Sozzi from the 2023 World Economic Forum in Davos, Switzerland, to discuss the state of the labor market, a recession, Fed policy decisions, and the outlook for the economy.

Tenth, Eric Johnston, Cantor Fitzgerald's head of equity derivatives and cross asset, joins 'Closing Bell Overtime' to share why he still considers this a bear market, indicators of worsening conditions in the rate market and the cyclical nature of the unemployment rate.

Next, Tom McClellan, of The McClellan Market Report, joins 'Closing Bell Overtime' to offer historical insights into present market activity, signals of market bullishness, and looking at taxes as a percentage of GDP.

Lastly, a great discussion where David Wessel, senior fellow in Economic Studies at Brookings Institutions, and Ron Insana, CNBC senior analyst, join 'Power Lunch' to discuss the Fed's battle to tame inflation and their expectations for February's meeting and solution to the tight labor market.

Comments

Post a Comment