OMERS Posts 3.2% Return in 2011

Doug Alexander of Bloomberg reports, Omers Posts 3.2% Return in 2011 Led by Private Investment Gains:

Doug Alexander of Bloomberg reports, Omers Posts 3.2% Return in 2011 Led by Private Investment Gains:Ontario Municipal Employees Retirement System, a pension fund manager in Canada’s most- populous province, posted a 3.2 percent return on investments last year, led by private equity, real estate and infrastructure holdings.

Net investment income was C$1.7 billion ($1.7 billion), the Toronto-based pension fund manager said today in a statement, compared with C$5.5 billion in 2010. Assets climbed 3.4 percent to C$55.1 billion from C$53.3 billion a year earlier, as gains in private investments offset declines in stocks and bonds.

“Our 2011 results are therefore a tale of two halves -- strong positive returns in private markets, and negative returns in the public markets,” Michael Nobrega, the chief executive officer, said at a press conference today in Toronto.

Omers, as the fund is known, beat the 0.5 percent average return of Canadian pension funds, based on a Jan. 23 report by RBC Dexia Investor Services Ltd.

Returns from infrastructure holdings were 8.8 percent in 2011, down from 10 percent in 2010, according to the statement. Real estate returned 8.4 percent, compared with 7.5 percent in 2010. Strategic investments gained 7.2 percent last year after returning 7.7 percent in 2010. Stocks and bonds lost 0.2 percent in 2011, compared with an 11 percent increase in 2010, as markets declined.

Markets Fell

Canada’s benchmark S&P/TSX Composite Index (SPTSX) fell 11 percent and the MSCI World Index declined 7.6 percent in 2011.

Omers said its deficit increased to C$7.3 billion in 2011 from C$4.5 billion a year earlier as a result of the 2008 global economic decline and increasing liabilities as members age. Omers manages pensions for more than 400,000 retired and active municipal employees in Ontario.

Omers is anticipating more opportunities this year in private market investments in Canada, the U.S. and the U.K., according to Michael Latimer, the chief investment officer. The fund is looking to expand in emerging markets, though “it’s not in a rush,” and North America and the U.K. remain its focus, he said.

Omers, which invests in high-quality real estate properties, may consider bidding on Scotia Plaza in Toronto, according to Latimer. Bank of Nova Scotia said last month it plans to sell its Toronto headquarters, drawing attention of firms including Canada Pension Plan Investment Board.

Nobrega also commented on a C$3.73 billion takeover offer by a group of banks and pension funds for Toronto Stock Exchange owner TMX Group Inc., saying the deal might fall apart because of its structure, rejection by regulators or “deal fatigue.”

Status Quo ‘Unacceptable’

Omers isn’t part of Maple Group Acquisition Corp., which in May proposed to buy TMX in an offer challenging a friendly deal between TMX and London Stock Exchange Group Plc. The LSE-TMX deal was scrapped in June after failing to get enough shareholder support. Calling the status quo “unacceptable,” Nobrega said he hoped the London exchange would revisit a TMX takeover if Maple’s bid fails.

Caisse de Depot et Placement du Quebec, Canada’s biggest pension fund manager, said yesterday it generated a 4 percent return last year with net investment income of C$5.7 billion.

Tara Perkins of the Globe and Mail commented on OMERS' swelling deficit reporting, OMERS earns 3.17 per cent as deficit climb:

The Ontario Municipal Employees Retirement System saw its funding deficit climb in 2011, despite positive investment returns, as the crash of 2008 continues to inflict pain on its portfolio.

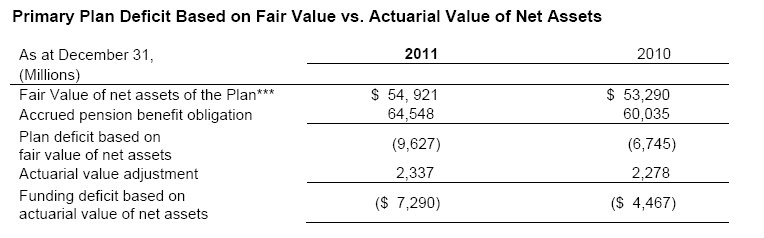

The plan, which invests on behalf of almost 420,000 members, said Friday that its funding deficit climbed to $7.3-billion last year from $4.5-billion a year earlier.

The increase is the result of the dramatic losses that the plan had in 2008, which it phases in over a five-year period according to actuarial rules, chief executive officer Michael Nobrega told reporters at a press conference. “We had a surplus in 2007,” he noted.

But the losses incurred three years ago continue to sting, at a time when pension plans grapple with headwinds such as an aging population, low interest rates, and an unpredictable investment climate.

Recent surveys have suggested that Canadian pension plans saw their funding fall by almost 15 percentage points throughout 2011, leaving many with large shortfalls.

With the pension sector struggling as the baby boomers enter retirement, governments are considering a number of initiatives to bolster the retirement savings industry, some of which could benefit OMERS, Mr. Nobrega said.

He welcomed recent comments by Ted Menzies, the Conservative Minister of State for Finance, which suggest that pension plans will be allowed to compete with banks and insurers to manage Pooled Registered Pension Plans, a new pension scheme being rolled out by Ottawa.

Mr. Nobrega was also happy to see Ontario’s much-publicized Drummond report recommend that the province look at increasing efficiencies within the pension system, something he hopes will lead to consolidation.

He said that Ontario needs pension “champions” that have world-class headquarters, and “you can’t do it by having six, seven, eight pension funds in the $10-billion range.”

Mr. Nobrega added that the Drummond report could result in OMERS’ members seeing little or no salary increases in the near future, a development that would likely have a positive impact on the plan’s liabilities but a negative impact on its contributions down the line.

In the meantime, OMERS said continued investment returns (which it hopes will be between 7 and 11 per cent annually over the long-term) and temporary contribution increases from members as well as benefit reductions should return the plan to surplus within 10 to 15 years. Mr. Nobrega said he doesn’t think further contribution hikes or benefit cuts will be necessary.

OMERS earned 3.17 per cent on its investments, or $1.7-billion, in 2011, and its assets rose to an all-time high of $55.1-billion.

Canada’s benchmark S&P/TSX composite index fell 11 per cent last year. But a rebound in the final quarter allowed plans, on average, to avoid investment losses, according to RBC Dexia Investor Services.

It was OMERS’ private market portfolio – which includes assets such as infrastructure, real estate and private equity holdings – that kept its returns afloat while stock markets tanked. The private market portfolio generated a return of 8.2 per cent, while the public markets portfolio had a return of negative 0.22 per cent.

At the end of the year OMERS had 42 per cent of its assets in private markets, and 58 per cent in public. It has been shifting away from public holdings in recent years – in 2003, the mix was 18 per cent private and 82 per cent public. Its goal is to have roughly 47 per cent private and 53 per cent public.

Within its portfolio, OMERS also shifted away from stocks toward bonds in the second half of last year in an effort to decrease its risks.

It continues to hold more fixed-income investments, which now make up more than 30 per cent of its total portfolio, chief investment officer Michael Latimer said during a press conference. That’s up about 12 percentage points from the start of 2011.

While OMERS’ executives acknowledged fixed income might be risky these days, Mr. Latimer said it is difficult to keep up returns.

You can go over OMERS' 2011 results by viewing their press release and by going over the breakdown in the fact sheet. First, let's go over their long-term results (click on image to enlarge):

As you can see, OMERS is outperforming its benchmark over the last 10 years. Every plan should publish these long-term results.

Next, we go over the results of the various asset classes (click on image to enlarge):

As you can see, public markets underperformed their benchmark (-0.22% vs. 1.26%) while private markets all outperformed their benchmarks led by private equity (7.23% vs. -5.58%).

Indeed, the strong outperformance of private markets was underscored by Michael Nobrega, OMERS' President and CEO, and used to justify the shift into private markets since 2003.

Here is where I part ways with Mr. Nobrega and the rest of Canada's pension leaders claiming that private markets are the way to go. While there is no denying that 2011 was a volatile year in public equities, there are a few things that people should understand about the risks of private markets:

- Private markets are not a panacea and they are heavily influenced by trends in public markets

- Correlations of private to public markets have crept up over the last few years as pension funds shove billions into private equity, real estate and infrastructure.

- The low interest rate environment adds fuel to the fire in raising these correlations

- Private markets are illiquid and officially valued on an annual basis when funds get audited. Such stale pricing can lead one to erroneously conclude that private markets are less volatile.

- Private markets carry other risks like political and regulatory risks that are often underestimated and under-appreciated.

- And last but not least, benchmark abuse is rampant in private markets, which is why all these large Canadian pension plans have been beating their overall benchmark in the last few years claiming to "add value" in private markets. This has allowed senior pension fund managers to reap huge bonuses in the last few years.

Now, to be fair, there is "added value" in private markets. And unlike most pension funds, OMERS and their Canadian counterparts are investing directly in private markets and this takes specialized skill set.

Unfortunately, none of these large funds post the internal rate of return (IRRs) net of fees and other costs (like currency hedging) of their direct investments versus their fund investments. Moreover, with few exceptions (AIMCo, for example), there is no clear explanation of benchmarks used to evaluate and justify the risk taken in private markets.

One senior pension fund manager shared these comments on why pension funds do not report IRRs of their direct holdings in private markets:

I think it is avoid short-term performance chasing, and bury as much as one can and play to the long-term, that would a reason why to not disclose, some merit to this.

The history of asset allocation also separates asset mix and scale from asset class returns. IRR is a size, dollar and time weighted calculation. AIMR for institutions uses time-weighted. Hence why firms often describe their average annual returns, which mean nothing but does exclude the scale decision.

Of course, they may not disclose because it doesn’t look good, and when people change etc. the history can be hard to climb out from under IRR.

The better question is why are all asset classes, and pension funds as a whole, not using IRR, or at least as a supplement when discussing a specific mandate. Ever increasing size of plans yet size really doesn’t get taken into account in any area.

The ‘way things are done' is powerful but CalPERS, and Caisse at one time, did disclose IRR, I guess when it served a purpose, or when that’s all their early systems could track.

This is why I take all this talk of 'shifting assets into private markets' with a grain of salt. It drives the guys and gals in public markets at pension funds absolutely bananas watching their private market counterparts reaping huge bonuses and justifiably so.

Importantly, it's much harder to beat public market benchmarks in stocks and bonds than beating some bogus benchmark in private markets that does not reflect the risk and beta of the underlying portfolio.

I have been beating that drum for the longest time, writing on bogus benchmarks in alternatives and why when it comes to evaluating and comparing pension funds and asset managers, it's all about the benchmarks stupid!

Is it worth investing in private equity, real estate and infrastructure? Yes, absolutely, especially if you invest directly and co-invest like most of the large Canadian pension plans are doing. They lower fees and control investments to help them realize larger gains. But you have to benchmark these investments appropriately and make sure that you're paying senior pension fund managers accordingly based on the risks they're taking in private markets.

Finally, OMERS and Ontario Teachers are pension plans, which means they manage assets AND liabilities. As seen below, OMERS' deficit swelled last year to $7.2 billion (click on image to enlarge):

OMERS discusses how they will address this deficit in their 2011 Report to Members (annual report will be released later). It includes temporary contribution increases, temporary benefit changes, and as stated above, a shift into private assets to "reduce the Plan’s exposure to stock markets that are expected to be highly volatile in the next several years."

While OMERS has built strong expertise in private markets, it remains to be seen whether this approach will benefit the plan over the long-term. I take a more balanced and skeptical view of shifting a huge portion of pension assets into private markets which carry their own set of risks.

Below, Jane Rowe, senior vice president of Teachers’ Private Capital, the investment arm of the Ontario Teachers’ Pension Plan, talks about the plan's return on investments and the role of private equity in the plan's strategy. Rowe, speaking with Cristina Alesci on Bloomberg Television's "Money Moves," also discusses some of her industry picks and compensation programs that attract top talent.

Comments

Post a Comment