Imogen-Rose Smith, contributing editor at ImpactAlpha, wrote a comment this week, O Canada, how do your pension plans get high ESG scores when you’re up to your neck in tar-sands oil?:

When in doubt, publish a list. It’s a media truism.

The trick

works for not-for-profits too. New America, a Washington D.C. think

tank, put itself on the ESG map with a biennial list of the world’s most

“responsible” global institutional asset owners, the behemoth pension,

insurance and sovereign wealth funds that own the global economy. The

most recent Responsible Asset Allocators Index, or RAAI, came out in November.

The

index suggests progress on responsibility, albeit plodding, among

global asset owners, with the average score reaching 52% in 2021, up

from 48% in 2019 and 44% in 2017.

But let’s be blunt: the list is stupid.

I should be more kind – new year, new me and all that. And I’ve overseen plenty of dumb lists in my time (RIP Trader Monthly).

But

it’s a disservice to the cause to rank Alberta Investment Management

Corp., or AIMCo., in the world’s top dozen allocators for

responsibility. Or to rank Saudi Arabia’s Public Investment Fund higher

than, say, the Illinois University Retirement System.

Such

rankings reflect the broader failures of ESG and sustainability

disclosure by institutional allocators. They are keen, and encouraged,

to tell the world all the good ESG investments they are making. They

offer far less transparency around their negative impacts.

The Responsible Asset Allocators Index,

and others like it, don’t take a 360-degree view of the more than 250

sovereign wealth and government pension plans in its orbit. The rankings

rely on what the world’s largest allocators say they do, rather than

what they actually do. The analysis falls short when it comes to the

real-world impact of the plans’ entire investment portfolios.

Step

forward, AIMCo. Founded in Edmonton in 2008, Alberta Investment

Management manages $95 billion in assets. AIMCo ranks among the top

dozen industry leaders on New America’s responsible allocators list,

with a score of 100.

Canadian pension plans have long been held

up as a model for other institutions, particularly those in the U.S. But

the rating for Alberta’s largest financial institution came as a

surprise to me.

If you know anything about Alberta, besides that

it is cold and dark in winter, it is that it is one of the world’s

major producers of tar sands oil and gas.

The Athabasca oil fields are the fourth-largest oil reserves in the

world – and among the dirtiest. Historically AIMCo’s portfolio has been

overweight to oil and gas, particularly in Alberta. This fossil fuel

conundrum is, of course, an issue more generally for Canada, which wishes to be a global leader on climate change but also to tap its sweet sweet oil and tar sands.

“Let’s face it, for many, many years Alberta was Canada’s leading engine of growth,” AIMCo’s Dale Macmaster told the Canadian press in July. MacMaster said the fund is reducing its energy exposure and increasing its investments in renewables.

But

AIMCo’s continued commitment to building Canada’s oil shale industry is

not mitigated by these green commitments. Indeed, they are undermining

the global effort to transition to a clean energy future.

Oil patch

I

do not question the dedicated work that goes into the responsible

allocators index by Scott Kalb, ex- of the Korea Investment Corp., and

his team of researchers from the Fletcher School at Tufts University.

The rankings use 30 variables in their analysis, but the gaps allow

funds to rank highly on the RAAI, even if they are funding activities

hated by environmentalists and many ESG and impact investors, like shale

oil pipelines.

In AIMCo’s case, this includes a partnership with

TC Energy, formerly known as TransCanada Corp. builders of the Keystone

XL Pipeline, one of the most controversial shale oil infrastructure

projects in North America. In 2019 AIMCo, a TC Energy shareholder, agreed to acquire 85% of the Northern Courier Pipeline, an inter-Alberta shale pipeline.

The Wall Street Journal, recently published an excellent article by Vipal Monga on the money flowing into Alberta’s oil fields, headlined, “One of the World’s Dirtiest Oil Patches Is Pumping More Than Ever.”

Tar

sands oil production is expected to continue for two decades or more,

Monga writes even though “Major oil companies, under pressure from

investors and environmentalists, are fleeing Canada’s oil sands.

Investment in existing projects has stalled, and banks are refusing to

fund new ones.”

Instead, “Local companies have stepped in to keep

working the existing mines and wells,” Monga writes. “Last year, the

oil sands were on track to deliver more oil than ever.”

The Biden

administration has put something of a wrench in Keystone XL, but it

hasn’t diminished TC Energy’s hunger to tap Alberta’s oil patch.

Canadian Prime Minister Justin Trudeau, beloved during the Trump era for his boyish charm and seeming normalcy, recently

committed more than $3.4 billion to acquire the part of the Keystone XL

pipeline system that taps the Alberta oil patch from TC Energy. The

government says it does not want to be a long time owner; Canadian

pension funds and other investors have expressed interest in the asset.

AIMCo has a controversial 2015 mandate from the Alberta government to invest in local economic growth. The Alberta government stepped in to backstopsome of the firm’s Keystone XL debt.

AIMCo is no stranger

to the oil patch in its backyard. My former boss, Jagdeep Bachher,

joined the University California Regents in 2015 from AIMCo., where he

had been a deputy CIO. At the time, the university’s Regents were

debating divestment from fossil fuels, a decision it ultimately took.

Bachher likes to joke that at AIMCo, he thought investing in oil and gas

was a good thing.

AIMCo’s 2021 responsible investment

report says the fund has $3.2 billion of assets in low or no-carbon and

renewable infrastructure investments. But in AIMCo’s nearly $10 billion

infrastructure portfolio, more than one-quarter of the holdings are in

pipelines and midstream companies, and another quarter are in integrated

utilities. Its major investments include Pungent Energy, a Washington

state utility company that provides natural gas services (yes, blah blah

blah, natural gas is a transition fuel) and Howard Midstream Energy, a

Texas based midstream energy business. AIMCo backed Howard, which owns

and operates natural gas and crude oil pipelines and natural gas

processing plants, refined product storage terminals, to build a major

renewable diesel facility in Port Arthur, Texas.

Working with oil

and gas suppliers is what AIMCo does. The Northern Courier Pipeline

purchase helped TC Energy release $1.5 billion in funding. TC Energy’s

Russ Girling explained that the capital would help the energy company

fund its $30 billion capital program. “We look forward to working with

AIMCo as we realize the benefits of this partnership and financing

opportunity,” Girling said.

And when Razor Energy Corp., a Calgary-based junior oil and gas development company, announced

it was deferring an interest payment on its $50 million credit facility

with AIMCo, it said it “is grateful to be partners with AIMCo and the

continued support as both a major shareholder and senior lender.”

To its credit, and one of the reasons for its high RAAI score, AIMCo does account

for its climate impacts under the recommendations of the Task Force on

Climate-related Financial Disclosures, or TCFD. But even the TCFD has

gaps, especially when it comes to Scope 3 greenhouse gas emissions that

include the actual use of the fossil fuel pumped and piped by AIMCo’s

portfolio companies (see, “Investors press oil majors to address emissions from products”).

“We

do not take into account emissions that emanate from the use of

companies’ products, also known as Scope 3 emissions,” AIMCo says, “as

data is limited, and invites double counting.”

AIMCo has seen an outflow of talent amid criticism and upheaval. In November 2020 the fund’s then-CIO (error: then-CEO!) announced

plans to step down after an investigation into losses earlier that

year, as COVID shutdowns tanked oil prices, found “unsatisfactory” risk

controls and called for a culture change.

There was a ruckus

when the Conservative Alberta government voted to have AIMCo take over

day-to-day administration of the province’s teacher pension assets. A

November 2021 report

from the Canadian policy research network Parkland Institute called for

a complete governance overhaul of the Alberta sovereign wealth fund.

ESG doubletalk

I am no purist. I know that

the path to the clean-energy transition goes through, and includes, the

fossil fuel industry. I think that issues such as job creation and

supporting energy sector workers and their communities are vital both to

sustainable investing and the success of the clean energy transition.

There is a case for AIMCo’s continued investment in the fossil fuel

sector, in the context of a broader transition away from carbon toward

renewables. And with an understanding of what that means.

That is not the case AIMCo is publicly making.

Rather,

AIMCo, and other institutional investors, use their Responsible

Investment report to highlight their ESG bona fides, and their annual

financial report to provide a snapshot of their investment portfolios.

Neither report gives a true account of the impact a pension plan or

sovereign wealth fund investments is actually having on the, you know,

real world.

I’m not accusing AIMCo of falsifying or misstating

anything. But the incompleteness of AIMCo’s Responsible Investment

reports and related disclosures may have been what tripped up New

America (RAAI says it constantly updates and refines their methodology)

The cognitive dissonance this reporting doublethink can cause is evident in AIMCo’s performance report

published last November, The fund highlights the Global Sovereign

Wealth Fund center, which ranked AIMCo third on its ESG scorecard. And

AIMCo was a finalist for the International Corporate Governance Network

Global Stewardship Award. It’s not only RAAI that thinks AIMCo is just

dandy.

Yet, on the very same page under “investments” the fund

also announced that it had added a new partner to its investment in the

Northern Courier Pipeline, which consists of two 90 km pipelines for

transferring bitumen and its diluted products from Fort Hills to Fort

McMurray, Alberta. The project complements Keystone

XL, which was intended to transport Canada’s shale oil into the U.S.

(The partnership includes economic participation by Indigenous

communities, a huge tick for ESG investing.)

“Alberta has an

enormous amount of carbon beneath its soil. If it gets dug up and

burned, then it will be calculably harder to limit the damage from

climate change,” climate activist Bill McKibben wrote in “We Love You, Alberta—Just Not Your Tar Sands,” in The New Yorker in July.

Burning

the estimated 173 billion barrels of oil in Alberta, by one

calculation, would produce about 112 billion tons of carbon dioxide,

McKibben reported, or 28% of the world’s total remaining carbon budget.

“There’s no way that a country with less than one per cent of the

world’s population can lay claim to more than a quarter of the

atmosphere,” McKibben wrote.

McKibben added that he and other climate activists are subjects of an “anti-Alberta energy inquiry” by a government commission.

G is for governance

I love you too,

Alberta. I once spent a lovely summer cleaning hotel rooms in Banff. The

cleaning part was awful, and I was terrible at it, but Banff was

lovely, as was Lake Louise. I learned about country music, got picked up

by a drunk driver hitchhiking, and was chased by an elk. You have cowboys.

AIMCo

is not the only pension plan or sovereign wealth fund to have such

limited ESG accounting and reporting, especially in large infrastructure

investments. See here

for how an agriculture investment in Maui by the Canadian government

pension plan PSP might not be as ESG, and community, friendly as PSP’s

Responsible Investment reports suggest.

In 2021, PSP entered into a joint venture

with Pretium, a New York-based alternative investment firm, to invest

$700 million into single-family residential housing. U.S. Sen Elizabeth

Warren has been raising awareness

around the impact on affordability of private-equity capital moving

into residential housing. Warren called out Progress Residential LLC, a

property company backed by Pretium.

PSP ranks as a “finalist” on the RAAI, and is generally considered to be a pretty good ESG investor.

Or

take British Columbia Investment Management Corp., which scores as

highly as AIMCo on the RAAI. Like AIMCo. BCI invests in Canadian oil

sand companies. Last May, Reuters reported

that cumulative investment by the country’s top five pension funds,

including BCI, in Canada’s top four oil sands producers had jumped to

$2.4 billion, up 147% from a year earlier. Reuters suggests the pension

funds fancy themselves helping these businesses transition to a clean

energy economy.

“We have a big problem with pension funds saying

we believe in engagement, not divestment, but there’s no sign of this

engagement,” says Adam Scott, director of the Toronto-based pension

activist group Shift. “The very act of owning them (oil sands companies) implies the funds do not support transition.”

ESG

rankings generally look at reporting, not governance. That let’s

investors like the California Public Employee Retirement Fund, or

CalPERS, avoid demerits for governance issues. And the New York Common

Retirement Fund, among the most progressive U.S. institutional investors

when it comes to ESG, does not get criticized by ESG commentators for

having a sole fiduciary, even though such a structure has been seen as a

contributor to corruption.

But this failure to focus on

governance presumably goes some way to explain how the RAAI rates Saudi

Arabia’s Public Investment Fund higher than the Illinois University

Retirement System. The state of Illinois has passed legislation

mandating that all public plans in the state take ESG factors into

consideration when making investment decisions. Saudi Arabia is, well, Saudi Arabia.

Efforts like the Responsible Asset Allocators Index

have encouraged more transparency around ESG investing. The average

RAAI score for ESG integration has risen to 46%, from 32% in 2017. So

progress is being made.

The danger is that these largest and

most influential of funds will spend their time and energy raising their

ESG rankings, rather than actually changing what they do. And that,

unfortunately, is where we still are.

Oh boy, where do I begin?

Let me be nice and praise Ms. Rose-Smith for writing this comment and not holding back.

Even though I totally disagree with her on many points, she does raise some interesting points worth noting.

The main problem is she has an obvious bias and axe to grind with AIMCo primarily but with other Canadian pensions too.

I think the biggest problem I have with this comment is the not-so-vague message: "Oh Canadian pensions, if you're not divesting from oil & gas, then you're not part of the solution, you're part of the problem!"

Excuse me? What a bunch of hogwash!!

I recently wrote a comment on why political independence is essential for pensions, especially Canadian pensions which need to operate at arm's length from the government to ensure their long-term success.

I stated that I'm concerned with incrementalism slowly creeping into the way our pensions are being run and added:

Don't get me wrong, I'm a stickler for diversity in all its forms, including diversity of views.

I

think it's important to listen to the views of plan members, government

bureaucrats, the public and other stakeholders but at the end of the

day, we can't lose sight of the purpose and mission of these large

pensions, namely, to maximize returns without taking undue risks and make sure they have enough assets to cover their long-dated liabilities.

Period.

That's it, that's all. Pensions aren't there to "save the world" or to

beat global stock market benchmarks every single year, pensions exist

first and foremost to serve their members by ensuring they will all

retire in dignity and security.

Now, don't get me wrong, ESG

investing is here to stay. Our large Canadian pensions see the writing

on the wall and so do their global counterparts.

As the Great Gretzky once famously said: "I skate where the puck is going to be, not where it has been."

Where

is the world heading? I'm not talking about next year or over the next

five years, I'm talking about the next 25 to 50 years.

The world

is decarbonizing fast. You don't need to attend COP26 or any other fancy

conference which big shots like Mark Carney attend, you know the world

is necessarily changing and we are in the midst of a great transition.

"I look forward to transitioning to a clean energy world but the key word is transitioning.

It’s going to take time and it seems some clean energy proponents want

it done today instead of over time. This creates shortages and raises

prices."

And there are a lot of opportunities and risks in the transitioning phase of a long-term secular cycle.

Our

pensions need to have the freedom to operate at arm’s length from

political interference to capture these opportunities and transition

their portfolios slowly but surely over time to reflect the reality of

the world they operate in.

But again, the focus must always be on

taking decisions that are in the best interests of their members, not in

the best interests of their local, provincial (state) or federal

governments.

It's a bit nuanced, there are obviously overlapping interests, but the key point is this, pensions exist to serve their members, not as an extension of the government to promote some agenda, no matter how worthwhile that agenda may be.

To her credit, Ms. Rose-Smith understands transitioning away from oil & gas takes time but the comment is so slanted and basically ridicules the Responsible Asset Allocators Index.

You should read my comment on Canada's most responsible asset allocators to gain a deeper appreciation for the criteria and methodology behind this index and why we should be proud of our large pensions and their responsible investing activities.

My biggest pet peeve with the comment above is it takes bits and pieces of activities at AIMCo and other pensions without appreciating how far they have all come in terms of responsible investing.

She doesn't mention CDPQ, arguably the leader in responsible investing in Canada and the world, or OTPP or CPP Investments for that matter.

Recently, Canada's largest pension fund, CPP Investments hosted the Alberta Energy & Growth

Forum in Calgary featuring a line-up of industry leaders speaking about

investment trends, innovation, and the future of the Canadian energy

industry:

The purpose of the event was twofold: demonstrating the

value CPP Investments provides through our global reach, sophisticated

investment approach and market-leading returns, as well as

communicating our approach to investing as we navigate the global

challenge of climate change.

The agenda covered timely topics

related to the importance and evolution of the Canadian energy

sector. In his opening remarks, President & CEO John Graham touched

on how the sustainability revolution is a full economy-wide transition,

much like the digital revolution that started in the 1990s. He also

spoke about where CPP Investments sees attractive investment

opportunities across the entire energy spectrum, and how we are working

to better anticipate the transition pathways of our investments.

The featured panel focused

on the future of energy. In this session Graham and Chief

Sustainability Officer Deb Orida joined top executives and thought

leaders from the Alberta energy sector. They discussed how an

industry with a strong track record of adaptation can further evolve, as

traditional energy companies increasingly pursue opportunities in

carbon capture, renewables, hydrogen, and technological innovation.

Graham closed the panel with three key takeaways from the discussion:

There is an important, positive shift underway from looking

primarily at the investment risks of climate change to

the financial opportunities of decarbonization;

Collaboration is needed to go beyond general agreement on reducing emissions to action; and that

Alberta and Canada have a great story to tell as they navigate

the energy transition, given their strong track record of

innovation, technology, and experience.

You can read a copy of John Graham’s speech from the Forum here.

I highly recommend you read John Graham’s speech from the Forum here and appreciate the perspective he's elucidating.

In particular, I note this passage:

Finally, I want to share our approach to safeguarding the value of our existing portfolio throughout the

energy evolution. And, how we plan to utilize our knowledge of the energy transition to seek out and

capitalize on the transition potential of companies across the energy spectrum.

The transition landscape remains in its early years. Yet it’s premature of the market to write off entire

sectors like oil and gas before having viable, scalable alternatives in place.

For some sectors the road ahead is clear. For other essential sectors

such as chemicals, steel or agriculture the path is less clear.

Where we see attractive return opportunities, we can provide capital to facilitate the transition of these

vital sectors. These sectors support the net zero economy of the future and need viable, clean

substitutes as demands grow.

That’s why we are deliberately building up the internal competency

to help our investee companies by giving them partnership driven capital and supporting them as they

adopt more sustainable business models and practices.

We’re also actively working with companies in our portfolio that are early in their transition and facing

pressures to become net zero. We’re helping them improve their ESG disclosure, anticipate and

interpret the regulatory or policy landscape and, sharing our institutional knowledge

built through our global investing experience.

We bring the full-weight of the “CPPIB-advantage” by providing global,

cross-asset class data and insights into climate changes’ physical and transition related risks.

We are not walking away, we are rolling up our sleeves.

We are looking for opportunities to support innovation and transformation in power generation and

utilities, many parts of the oil and gas value chain, vehicle transport, cement and construction and

agriculture.

If we seed and build the right businesses today, they will become the unicorns of tomorrow’s low-carbon economy.

I think this passage is critically important,

CPP Investments and other large Canadian pensions aren't walking away,

they're rolling up their sleeves engaging with investee companies and

investing in tomorrow's disruptive innovators.

But in order to do this properly, they need to continue to operate at arm's length from the government.

The Alberta Management

Investment Co. is focusing on all three legs of the environmental,

social and governance stool this year and beyond.

The

government-owned pension investment manager is addressing a range of ESG

issues, from integrating climate risk to building a more diverse

workforce to advancing its risk governance in 2021, according to its

11th annual responsible investment report.

On the environment front, almost a quarter (24 per cent) of its direct

infrastructure assets under management are committed to net zero by

2050. And while climate change is front of mind, the AIMCo’s chief

executive officer noted its roots in an energy-rich province.

“Alberta is the energy hub of Canada and a centre of generation,

production, research, know-how and technology,” said Evan Siddall (pictured), the AIMCo’s new CEO as of July,

in the report. “Our province can offer leadership that promotes

economic development and positions both energy producers and consumers

to succeed in a low-carbon economy. At AIMCo, we intend to invest

additional resources in support of a climate strategy that spans asset classes.”

When

it comes to social factors, the AIMCo has developed a comprehensive

diversity, equity and inclusion action strategy and plan, as well as

issued a formal DEI statement of commitment this year.

“The global

pandemic served as a wake-up call on the materiality of systemic risks

such as climate change, human capital management and diversity, equity

and inclusion,” said Alison Schneider, vice-president of responsible

investment at the AIMCo since late last year,

in the report. “We are working on being more efficient and proactive in

our processes, adding DEI and climate disclosure to every engagement

and in developing ESG analytics such as a scorecard for private equity

to more effectively capture ESG performance trends.”

The

investment organization has also been focusing on governance issues

this year, pointing to the example of Tanger Factory Outlet Centers Inc.

in its report. Tanger had received low support for its advisory vote on

executive compensation, including qualified support from the AIMCo “due

to concerns regarding a disconnect between pay and performance.” The

AIMCo’s engagement with Tanger focused on executive compensation,

including changes the company made to its 2021 program, based on

shareholder feedback.

“Governance is the final leg of the ESG

stool and long a priority among institutional investors,” said Siddall.

“In 2021, we substantially advanced our risk governance. Looking ahead,

we will promote efficiencies in streamlining our decision-making

processes and we will require strong governance among our investee funds

and companies.”

I commend the work Alison Schneider, Vice President, Responsible Investment and her team are doing at AIMCo.

And they don't have pushover clients, especially when it comes to responsible investing.

In fact, at the end of last year, the Alberta Union of Provincial Employees called on AIMCo to “quantify the climate risks of its

investments and adopt a path to net zero.”:

The AUPE’s call for action was one of three environmental resolutions

for which the union’s membership voted in favour during its annual

convention held earlier this month, according to a press release.

“Pensions are some of the most hard-fought gains that working people

have ever won,” said James Sullivan, the AUPE’s environmental committee

chair, in the release. “It’s up to us to make sure that those pensions

are stable. Quantifying climate risk would help achieve that.”

In an emailed statement to Benefits Canada,

the AIMCo said it acknowledges that climate change is an urgent and

compelling matter requiring immediate action from all players. “As

Alberta’s investment manager, we recognize the business imperative of

integrating climate change into our investment processes, to both

enhance and protect our clients’ risk-adjusted investment returns over

an extended time horizon.

“We believe that large-scale, long-term

investors like AIMCo have an essential role to play in the coming energy

transition. AIMCo has been measuring its carbon footprint since 2016, a

process that has since advanced to include a portion of all major asset

classes and is committed to engaging with our clients to determine a

climate action plan and go-forward strategy that most closely aligns

with their objectives.”

The statement also pointed to the AIMCo’s recent responsible investing report,

in which the government-owned pension investment manager outlined plans

to address a range of environmental, social and governance issues, from

integrating climate risk to building a more diverse workforce to

advancing its risk governance. “We strive to adopt best-in-class

ESG-integration strategies across asset classes and investment processes

to better identify our ongoing assessment of risk and value,” read the

statement.

Additionally,

the AIMCo said it’s consulting with its pension fund clients, including

the Alberta Public Service Pension Plan and the Local Authorities

Pension Plan to arrive at a climate action plan and go-forward strategy.

Plan members of the Alberta PSPP and the LAPP are members of the AUPE.

“LAPP

Corporation has an ongoing, almost daily dialogue with AIMCo on

responsible investing, with climate change and environmental risk

factors high on the list of investment considerations,” said Chris

Brown, president and chief executive officer of the LAPP Corp., in an

emailed statement to Benefits Canada. “While AIMCo works

continuously to update and integrate its oversight of ESG factors, our

corporation and our sponsor board are refining our policies and

processes as well, to ensure we are providing direction to

AIMCo that reflects the expectations of our sponsors.”

The

AUPE has a seat on the LAPP’s sponsor board, which has identified

climate change as a “primary risk” in the plan’s long-term funding

policy, said Brown. For its part, the LAPP Corp.’s board of directors is

currently working to develop the terms of an updated responsible

investment policy for the LAPP’s funds, which will review best practices

around climate risk measures and carbon capture metrics.

“AIMCo

has announced it will consider viable options to decrease the

portfolio’s emissions trajectory over time,” said Brown. “After

consulting with its clients, it expects to update its plan regarding

implementation of climate-related targets early next year.”

Other

resolutions adopted by the union include a just transition toward net

zero for workers and a proposal for a green, new deal that includes

providing union jobs through an expanded public sector; modernizing

public infrastructure to adapt to climate change; recognizing Indigenous

rights and treaties; and building a society that is ecologically

sustainable and socially fair.

As you can read, AIMCo's clients are very engaged when it comes to responsible investing, providing direction that reflects their expectations.

But AIMCo's clients are not calling for divesting out of oil & gas, that would be insane, akin to asking CDPQ not to invest in Quebec's economy.

As I keep telling my readers, divesting is easy but it's downright foolish, all it does is transfer the risk on to another fund that couldn't give a damn about ESG.

And there's a cost to divesting, a serious cost.

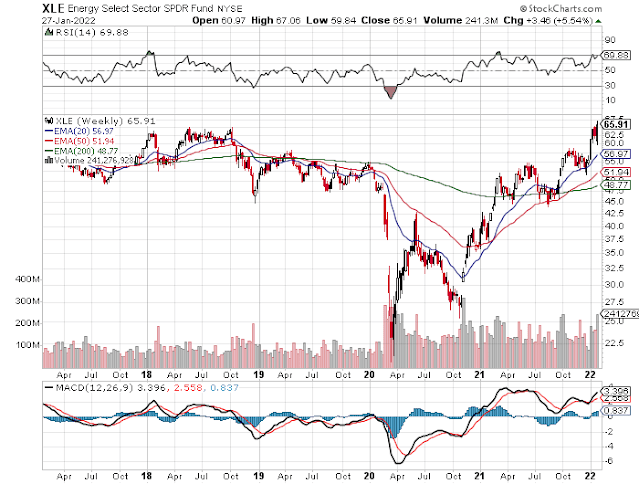

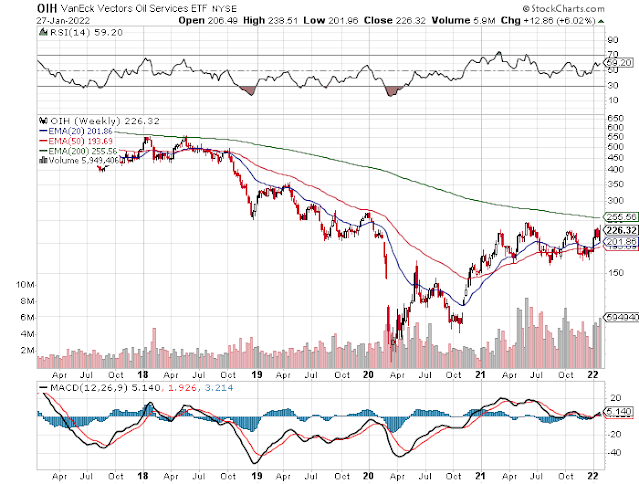

Energy was the top performing sector last year by a lot and there's more room to run higher this year, especially in oil service stocks:

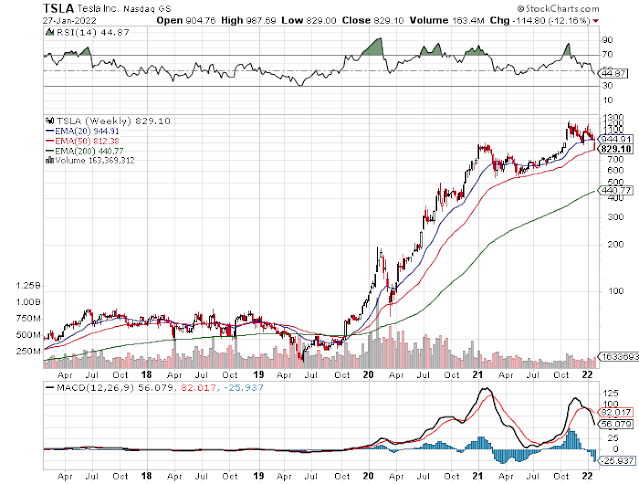

I know, investing in traditional energy isn't cool, buying Tesla shares is cool:

Don't get me started, there's so much nonsense out there in ESG investing, I can write a book on it.

Lastly, I will state where Imogen-Rose Smith's comment struck a chord with me is that Canada's large pensions need to do a better job communicating how their responsible investing activities are making a real world difference.

It's simply not enough to spew out an annual responsible investing report, do a video clip and share with your members and stakeholders real world examples of things you're doing which are making a difference and focus on all three legs of ESG, not just the "E".

Below, Rob West, founder of Thunder Said Energy – an energy consulting firm, understands that the total decarbonization of the energy industry will be fueled by political attitudes around the world over the next few decades. However, West argues that proponents of ESG investing fail to understand that this transition will involve massive investment in fossil fuels and cooperation with villainized oil majors.

He explains his framework for total decarbonization of the energy industry by 2050, and highlights the new technologies and investment vehicles that will be necessary to drive the transition (filmed on October 18, 2019 in New York).

Update: A friend sent me this after reading my comment:

Why Environmentalists Pose a Bigger Obstacle to Effective Climate Policy than Denialists https://t.co/bM7yayJHFm

Comments

Post a Comment