Marissa Schlueter of OMERS Ventures posted a comment on spotting next generation healthcare opportunities:

Here’s a radical understatement: The last couple years have been tough.

But

— at least for me personally — tough times also provide the opportunity

for reflection and change. Going into 2022, I have a much better sense

of who I am, what I value, how I learn and where I want to be. And

that’s as a health tech investor at OMERS Ventures.

I’ve

long entertained venture capital as a potential career in the back of

my mind. Now feels like the ideal moment. I’m hoping to take my

experience with public equity research at Melius Research, as well as

private company research at CB Insights to help trend spot and identify

the next generation of opportunities in health-tech.

Why VC?

For years, friends and family have joked that I’m a professional student — and they’re not wrong.

My

previous roles have relied on my ability to consume large amounts of

data, synthesize actionable insights and communicate those learnings to

key stakeholders as they evolve. VC gives me a perfect forum to do what I

do best in service of finding great founders and helping them build

their businesses.

As

nerdy as this sounds, I’m genuinely excited to help founders build and

refine their financial models, dig into user and company performance

metrics, conduct competitive and market landscaping analyses, and

identify strategic growth opportunities.

I’ve

also come to realize how much I value purposeful, mission-driven work.

At the micro level, this affords me the opportunity to really make an

impact on entrepreneurs making healthcare better. After all, when they

win, we all win.

Why OMERS Ventures (OV)?

I should start by explaining what OV is.

For

the uninitiated, OV is the VC arm of OMERS (Ontario Municipal Employees

Retirement System), one of Canada’s largest pension plans with around

$100B in net assets. With teams in Toronto, London, and Palo Alto, OV

makes multi-stage (Series A to C, with the occasional, exceptional Seed)

investments in growth-oriented startups across North America and

Europe.

As

is often the case in venture, people are paramount, and I knew I

couldn’t make the jump with just anyone. Specifically, I wanted a team

with a strong culture of collaboration, mentorship, and diversity. It

was also important for me to join a team that viewed their portfolio

companies as valued partners instead of strictly as investments.

Where I’m rolling up my sleeves

Below are just some of the health tech themes, segments, and end markets I look forward to digging into as a VC.

Many

of these are personal to me — I’ve either experienced the problem

firsthand or have dear friends and family members who have. They also

overlap with what I’ve observed (during the last few years at CB

Insights) as relatively under-appreciated pockets of opportunity for

tech integration and advancement.

If you’re a founder focused on any of these areas, reach out to me at mschlueter@omersventures.com — I’d love to learn more about what you’re working on.

– — — — –

Wraparound care

A

growing number of startups are using digital technology to productize

supplementary health/social services and integrate them into next-gen

care delivery models. These wraparound services — which may include

coaching, social counseling, dietetics, companionship, peer/community

support, navigation, coordination, education, prescription management,

transportation assistance, etc. — aim to enable more holistic,

personalized, seamless and higher-quality care.

While

covering the telehealth space at CB Insights, I saw many point

solutions being used for distinct applications/populations, including

lifestyle coaching for type 2 diabetes prevention (e.g. Lark Health,

Noom), companionship for aging seniors (e.g. Papa), and peer support for

recovering addicts (e.g. MAP Health Management, Marigold Health).

But

given increased focus on social determinants, shifting consumer

expectations, and expansion of verticalized virtual care delivery, I

think this trend is in its early innings.

Over

the next few years, I expect digitally-enabled wraparound care to

become more commonplace and also more comprehensive as next-gen care

models emerge for specific demographics (e.g. age, gender, race,

socioeconomic status, sexual orientation, etc.) and medical conditions

(e.g., cancer, CKD, IBD, HIV/AIDs, etc.).

In

the near-term, I’ll be keeping a particularly close eye on the

integration of mental/behavioral health and peer/community support into

care for patients with rare, complex, debilitating, life threatening,

and stigmatized conditions.

In

response to the pandemic, many health systems, patients, families, and

even clinical trial sponsors/CROs increasingly sought out home-based

alternatives for care traditionally delivered in institutional care

settings like hospitals and skilled nursing facilities (SNFs). But while

the shift to home-based healthcare was accelerated by the pandemic,

there are several reasons it could persist.

“Hospital-at-home” (HaH) for acute & post-acute care:

A growing body of research supports HaH’s ability to demonstrate

material cost savings, reductions in readmissions and lengths of stay,

and improvements in clinical outcomes and patient satisfaction ratings.

CMS has also signaled a willingness to reimburse for Medicare HaH

services during the public health emergency (PHE) with the

implementation of the Acute Hospital Care At Home waiver program. Though

there are some issues to be sorted out, the program is a move in the

right direction from a reimbursement angle and industry stakeholders (Advanced Care At Home Coalition) are aggressively advocating for its extension beyond the PHE.

The startups highly levered to this shift are raising some serious capital:Medically Home just announced a $110M Series D led by strategic investor Baxter International, and last year, DispatchHealth raised $200M in Series D financing at a $1.7B valuation. We’re also seeing M&A activity here: Admedisys picked up Contessa Health for $250M and Best Buy acquired Current Health for $400M.

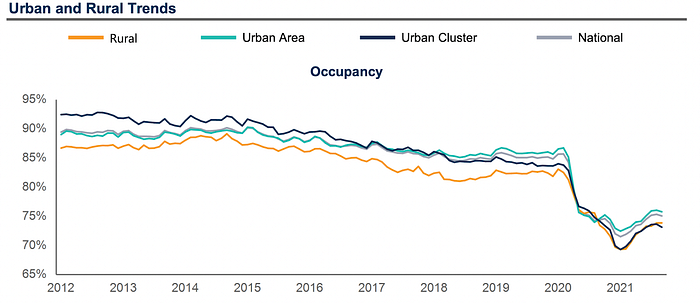

Extended care for aging and disabled patients: Aging

and disabled patients and their families have been shifting away from

SNFs in favor of home-based care for the better part of the last decade.

The pandemic only accelerated that trend. Though SNF occupancy has

bounced back slightly from its all-time low (early 2021), the pace and

magnitude suggest we will not be seeing 85%+ occupancy again for quite

some time… if ever.

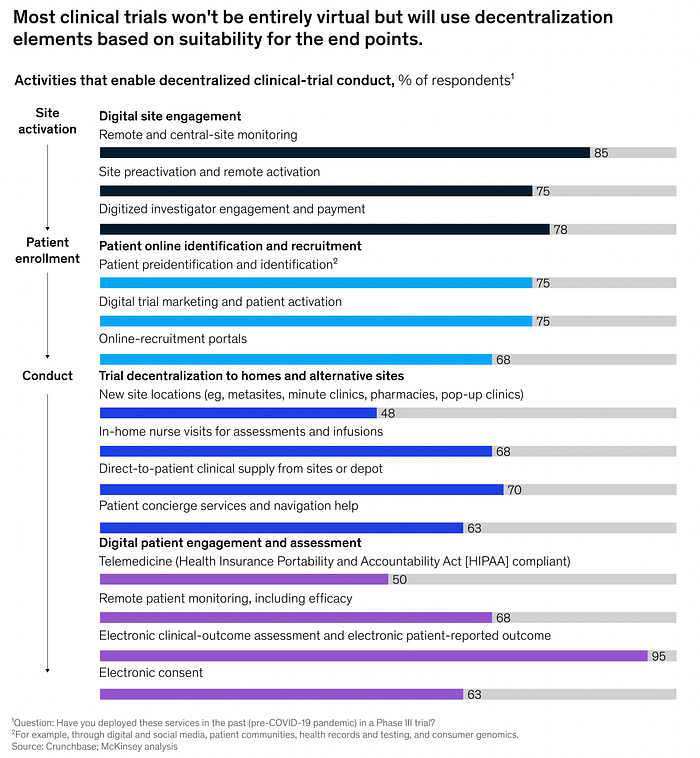

Decentralized clinical trials (DCTs): During

the pandemic, mass decentralization happened out of necessity. But the

tech demonstrated valuable benefits: it allowed clinical trial

investigators to reach larger, more diverse patient pools, work more

efficiently, reduce participant dropout, and generate cost savings for

sponsors. Having had that experience, the vast majority of clinical

trial sponsors and CROs expect virtual trials to be a big component of

their portfolios going forward, with most activities conducted in

participants’ homes (according to a McKinsey survey).

For

any/all home-based care programs/paradigms, tech will be absolutely

critical to the economics, clinical impact, and patient experience —

from identifying eligible participants, to coordinating care, optimizing

staffing & logistics, remotely monitoring patient vitals &

self-reported symptoms, and more.

While

at-home Covid testing may be the most immediately relevant application,

the overarching market opportunity for decentralized testing is much

more expansive.

We’re

already seeing at-home testing solutions tailored for routine

screening, high-risk screening (CKD, prediabetes), fertility screening

(male & female), low acuity diagnostics (UTIs, STIs, common

respiratory viruses, food sensitivities), and even pharmacogenomics

(birth control selection).

I

expect this list to expand, especially as more care is delivered in the

home (acute/post-acute, aging-in-place, clinical trials, etc.) and on

the back of some material business developments over the last year or

so.

The

interest is coming from all angles of the market — we’ve seen: virtual

care providers bolting on at-home testing assets (Ro’s acquisition of Kit), at-home testing players acquiring virtual care businesses (23andMe acquiring Lemonaid Health), traditional diagnostics giants getting their foot in the door (BD’s acquisition of Scanwell), and digital infrastructure being built to support the trend (Truepill’s diagnostics launch).

But

even beyond at-home testing, there are tremendous opportunities to

bring diagnostics closer to the POC — whether that’s in an exam room, at

the patient’s bedside, in a community health center, at a retail

pharmacy, etc. — because doing so significantly reduces test turnaround

time (compared to sending samples out to a reference lab), which in turn

can shorten treatment response times, improve patient outcomes, and

reduce costs. This is particularly critical for conditions like sepsis

and hospital-acquired infections.

Digital pharmacy & DME fulfillment

Digital pharmacies like Capsule, Medly, and Alto

have been around for several years but the pandemic really catapulted

their growth. The same goes for DTC virtual care/pharmacy fulfillment

(“telepharmacy”) companies like Ro, Thirty Madison, Nurx, Pill Club, etc.

Again,

I think this phenomena will outlast the pandemic. And so do major tech

& retail players: for example, Uber has partnered with ScriptDrop

and Amazon and Walmart launched their own digital pharmacy offerings.

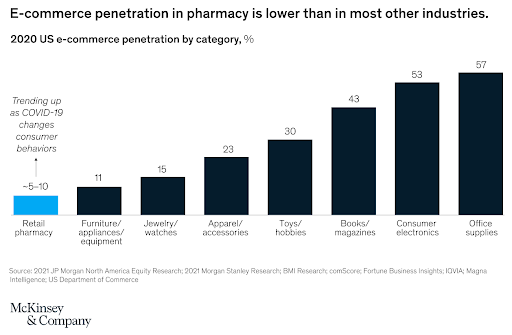

So, why the optimism?

The opportunity is massive. According to McKinsey,

only 5–10% of the US retail pharmacy market ($460B) happens online.

That’s less than half the penetration rate seen in other industries like

apparel, consumer electronics, and office supplies. While some drug

classes are legally prohibited from being prescribed online (per the

Ryan Haight Act), enforcement was relaxed during the PHE and some think we could see a permanent reversal of the law in 2022.

2.

Consumers increasingly demand convenience. The proliferation of digital

health services during the pandemic has given consumers more power in

choosing where/when/how they receive care. And when the choice exists,

consumers will always choose the more convenient option, all else equal.

Once in place, these expectations are very hard to reverse, and for

those reasons I think digital pharmacy/direct-to-patient medication

delivery will only grow in demand.

3.

More care is happening at home. New opportunities for digital pharmacy

will emerge as more care shifts out of institutional care settings and

into patients homes. Patients who would normally get their medications

on-site at a SNF, for example, now need a different service to fill that

gap — for disabled patients or those who no longer drive, digital

pharmacy/home delivery is a perfect fit for that.

Another

tangentially related area I’m interested in is tech improving durable

medical equipment (DME) logistics & fulfillment. Roughly 1 in 4 US

seniors rely on DME in some way but getting and maintaining it can be a

very confusing and complicated process for those living at home.

Companies like Tomorrow Health and Better Health

are using tech to improve stakeholder connectivity, optimize supplier

matching, streamline order & refill processes, and improve

transparency & patient choice.

Caregiver support & empowerment

According to the National Alliance for Caregiving

(NAC), a greater proportion of US adults are taking on unpaid

caregiving responsibilities each year. In 2020, 21.3% served as a

caregiver to a family member or friend compared to 18.2% in 2015. On top

of that, a greater proportion are providing care to 2+ people: 24% did

so in 2020 vs. 18% in 2015.

The NAC attributes these findings to:

“The increasingly aging baby boomer population requiring more care

Limitations or workforce shortages in the health care or long-term services and supports (LTSS) formal care systems

Increased efforts by states to facilitate home- and community-based services

Increasing

numbers of Americans who are self-identifying that their daily

activities, in support of their family members and friends with health

or functional limitations, are caregiving

Regardless

of the causes, we’re witnessing a “caregiving crunch” that’s only

projected to grow more acute in the future. According to Lisa D’Ambrosio,

a research scientist at the MIT AgeLab, “shifting demographics will

lead to a drop in what’s known as the caregiver support ratio: the

number of adults ages 45 to 64 who are available to provide care to

those 80 and older. Between 1990 and 2010, the caregiver support ratio

hovered at around 7 caregivers per care recipient, but by 2030 the ratio

is estimated to decline to 4 to 1, hitting 3 to 1 by 2050.”

Tech

is unlikely to solve this problem entirely but it certainly could have

outsized impact on low-touch caregiving activities like social

engagement/companionship, medication management, care coordination,

transportation & meal assistance, etc. DUOS,

which emerged from stealth in 2021, is an interesting example as it

pairs aging adults with dedicated personal assistants to help with these

“social determinants of aging,” leaving high-touch activities to be

managed by caregivers.

I’m

also interested in businesses looking to support caregivers’ mental

health and wellbeing. One company integrating mental/emotional health

within a broader suite of caregiver support tools is ianacare, which just recently raised $12.1M in Series A financing.

Palliative care

Contrary

to popular belief, palliative care is not synonymous with hospice and

isn’t exclusively meant for the very elderly or terminally ill. Though

it was originally developed for those purposes, palliative care has

evolved into its own medical speciality that caters to people of all

ages and all types of serious medical conditions including heart

disease, AIDS, MS, stroke, liver disease, and more.

Instead

of treating underlying conditions, palliative care teams — a

multidisciplinary mix of physicians, nurses, social workers, mental

health professionals, and chaplains — focus on alleviating patients’

symptoms and meeting their emotional, spiritual, and quality of life

goals. They also serve as critical support systems for patients’

families and caregivers and as care coordinators with patients’ primary

physicians. Importantly, unlike hospice, palliative care can be — and

often is — delivered alongside curative or life-prolonging treatment.

Studies

have consistently demonstrated palliative care’s ability to drive

meaningful improvements in quality measures, resource utilization, and

costs. As a result, it’s been one of the fastest growing

fields in medicine. Between 2000 and 2016, the percentage of 50+ bed

hospitals with a palliative care team tripled from just 25% to over 75%.

Despite its growth, palliative care remains underutilized. Roughly 60% of people who would benefit don’t get it. Two of the biggest reasons have been consumers’ lack of awareness and physicians’ hesitation to initiate discussions with their patients. But those things are beginning to change

— and demand is rising — in response to the pandemic. Telemedicine has

also begun to alleviate some of the access and supply shortage

challenges (e.g. Vynca, Devoted Health, Mettle Health).

But as utilization picks up, there will be greater need for other digital health tools

to improve patient/family/caregiver education,

patient-provider-palliative care team information sharing and

communication, symptom management, advance care planning, family

grief/bereavement counseling, and more.

Unique solutions for HCP shortages & burnout

Skilled

labor shortages and rising burnout have long plagued the US healthcare

system but, now with omicron, are growing increasingly more acute by the

day. Presently, the healthcare workforce is on the brink of a “Great Resignation,” which could send deleterious ripple effects throughout the entire healthcare system.

Despite

all the progress we’ve seen in health tech, in aggregate, these

innovations have failed to make a difference on the very people the

system depends upon.

Many

virtual care companies, for example, claim that they’re helping address

HCP shortages, but in my opinion they’re more so reshuffling when/where

the available HCPs dedicate their hours. Tech-enabled workflow

efficiency gains will only move the needle so far — maybe allowing them

to see a few extra patients per day on the margin. To fundamentally

address the supply shortage, we need to see more dedicated investment

into training and upskilling.

I’m also eager to see tech that improves HCPs’ quality of work life — e.g. by reducing information/tech overload (e.g. Wellsheet), relieving them of documentation duties (e.g., DeepScribe, Suki), providing intuitive clinical decision support, guiding them through difficult conversations, helping them develop stronger relationships with patients, instilling a sense of purpose, etc.

There’s

not going to be one fix-all, of course. But hopefully, in time, a

confluence of health tech solutions can help turn this ship around.

Provider directories & care navigation

I’ll keep this one short because my colleague Chrissy Farr sums it up nicely in her blog post here.

There’s one thing I’d like to add to her analysis:

Until

recently, provider directory and care navigation tech focused mostly on

the employer market, but the need for these solutions is becoming

increasingly relevant to the masses now that DTC health services are proliferating.

As

competition heats up, consumers will grow more discerning of where

they’d like to spend their out-of-pocket dollars. Beyond price, DTC

providers will be increasingly assessed for things like wait time,

cultural competency, ancillary services (e.g. prescription delivery,

at-home labs, etc.), patient reviews, etc.

Prior authorizations / utilization management

There

are two main types of waste that cost the healthcare system $1.1T

annually: administrative waste ($700B) and clinical waste ($445B).

Over

the last decade, a lot of time, money, and energy has been spent on

addressing administrative waste — understandably, since it’s a bigger

piece of the pie — but disproportionately fewer resources have been

devoted to tackling clinical waste.

We’re

starting to see that change. A growing number of startups are now using

tech to improve prior authorization processes and, ultimately,

utilization management. Some examples include: Olive, Cohere Health, and Banjo Health.

Medicaid—

Investment into Medicaid-focused businesses has historically been

limited due to concerns about scalability and profitability. But many of

these concerns are actually rooted in misconception. With Medicaid enrollment at record-level highs (almost 25% of the US population) and the rest of the healthcare system “[speeding] up its digital transformation by 10 years,”

it’s irresponsible to ignore technology that could make healthcare more

equitable, affordable, and accessible for a population that’s long been

overlooked and underserved.Cityblock

has been a standout for several years now but we’re only just beginning

to see other types of Medicaid-focused businesses emerge, like Circulo Health and Waymark.

Specific cultural communities —

There’s growing appreciation of the need for culturally competent HCPs

and healthcare organizations, with a wave of health tech companies like Hurdle Health, HUED, Health in Her Hue, and Pride Counseling emerging and established players like Grand Rounds/Doctor On Demand (now renamed Included Health)

acquiring culturally-competent businesses. Companies that specialize in

cultural competency education, training, and credentialing (e.g., Violet) will likely play important roles as this recognition grows.

Children & adolescents —

Pediatric health tech businesses have been in vogue recently, but

really just in one area: mental/behavioral health. There’s so much else

that goes into childhood development that’s not getting much attention.

I’d be interested in seeing health tech businesses working on pediatric

nutrition/healthy eating, allergy & immunology, endocrinology,

reproductive/sexual health, and sleep medicine. I’m also interested in

companies working on improving urgent & primary care in school

settings.

Women — Again, I’ll leave this one to Chrissy. This is a topic both of us are passionate about so will continue to be a big focus of ours going forward.

Specific conditions & specialties

To

avoid going down a million other rabbit holes (I’ll save that for

another time…), here’s a short laundry list of specific conditions and

medical specialties I want to dig into. None of these are truly

uncharted territory from a health tech point of view but they do likely

have pockets of untapped opportunity and definitely have areas in need

of improvement.

If

you’ve got unique experience, perspective, or intel on any of these and

how technology could play a bigger/better role in the future, please

reach out.

Pediatric

oncology — e.g., solutions to help parents/families to navigate care,

communicate with care teams, receive emotional support/counseling, etc.

Fertility — e.g., businesses aiming to improve the success rate and affordability of fertility care

So

as you can tell, this is a fairly exhaustive list. And I had to hold

myself back from including more. If you’re working in any of these

areas, I’d love to hear from you!

This is a fantastic, in-depth comment from Marissa Schlueter of OMERS Ventures.

She really covers a lot of the important trends and goes into detail (you can read more about the challenges and opportunities in healthcare here).

I read it last week and started following her on Twitter here.

OMERS Ventures is the venture capital (VC) arm of OMERS. With teams in Toronto, London, and Palo Alto, it

makes multi-stage (Series A to C, with the occasional, exceptional Seed)

investments in growth-oriented startups across North America and

Europe.

You can view all their investment, operational, legal and finance professionals here and the team is led by Michael Yang, Managing Partner out of the San Francisco.

I like their thematic approach to investing. They understand the big macro trends and focus on investing in high growth disruptive companies making an impact of various sectors of the economy.

But understanding big macro themes and making money investing in venture capital are two entirely different things.

I want to make it very clear, investing in venture capital was always and will be always be difficult.

First, competition for talent is intense.

For example, VC heavyweights including Sequoia, Bessemer Venture Partners, Lightspeed

and General Catalyst have all either opened new offices in Europe or started

notable expansions in the last 12 months. Hussein Kanji, co-founder of Hoxton Ventures in London, told CNBC that

the big US VC firms are finding it “super, super hard” to hire the

right people in Europe.

Also, the era of cheap money is coming to end and with that, a lot of speculation that drove hyper-growth tech stocks, meme stocks and cryptocurrencies to the moon has come to an end.

If these "super bubbles" are bursting and tech stocks enter a bear market, it will make it that much tougher for VC funds to realize on their investments because the IPO window will close.

This doesn't mean that OMERS Ventures can't compete, it most certainly can and will compete, it just means the environment is becoming that much harder for anyone investing in venture capital.

This is why the investment process in venture capital is critical as is extreme discipline.

Now more than ever, you need the right internal team, the right external partners and the ability to execute on a sound strategy.

Still, whether it's healthcare, the energy transition or other new or traditional sectors, venture capital is critically important for all of Canada's large pensions, they need to invest in tomorrow's disruptive technology companies to realize on their long-term return targets.

On a related topic, Bruce Power, a holding company of OMERS Infrastructure, announced today that it is forming a partnership with Isogen, paving way for production of life-saving medical isotopes:

Bruce Power and Isogen (a partnership between Kinectrics and

Framatome) have completed the installation of a groundbreaking Isotope

Production System (IPS), making Unit 7 the first power reactor in the

world with installed capability to produce Lutetium-177 (Lu-177).

Lu-177 is a medical isotope used in the treatment of various cancers,

such as neuroendocrine tumours and prostate cancer. In the future, this

system will also have the ability to produce other isotopes for medical

uses.

“This installation of the IPS is an exciting milestone on our journey

to becoming the first power reactor in the world to provide a scalable,

game-changing solution in the supply of life-saving medical isotopes

for the global medical community,” said James Scongack, Bruce Power’s

Chief Development Officer and Executive Vice President, Operational

Services. “Our medical isotope program and the IPS installation are a

result of years of innovation and development in partnership with

Isogen, Saugeen Ojibway Nation, and ITM, and will provide large-scale

capacity to help produce medical isotopes, which will be used across the

world in new treatments to fight cancer.”

With the new system now installed, activities will shift to planned

commissioning along with preparation activities for commercial

production that will follow once these activities and regulatory

submissions are successfully completed.

“Ontario is leading the way in the production and supply of medical

isotopes around the world,” said Hon. Todd Smith, Ontario’s Minister of

Energy. “I’m proud of the innovative work being done by Bruce Power and

its partners in the supply chain, including Framatome and Kinectrics.

Their efforts are helping to further cement our position as an

international isotope superpower, while providing critical medical tools

to help meet the needs of patients battling cancer.”

Lu-177 offers doctors an alternative to traditional chemotherapy by

deploying a “seek-and-destroy” dose to target cancer cells, while

limiting damage to surrounding healthy tissues and organs.

The IPS was developed and manufactured by Isogen, a joint venture

between Framatome and Kinectrics, which is focused on developing

innovative isotope production technologies.

“The installation and successful transfer of the first target marks a

major accomplishment and successful implementation of Framatome

Healthcare technology; the first Isotope Production System in a power

reactor for commercial production of therapeutic medical isotopes,” said

Curtis Van Cleve, President and CEO of Framatome Canada Ltd. “We

applaud the dedication and efforts of our partners at Bruce Power,

Saugeen Ojibway Nation, Kinectrics, ITM and our team, and the support of

their families that allowed them to see this installation through.”

“The installation of the IPS is the result of countless hours of

support from many people at Bruce Power, Framatome, Kinectrics, Saugeen

Ojibway Nation and our suppliers,” said David Harris, CEO of Kinectrics.

“The entire team demonstrated tremendous dedication, especially during

the pandemic. This was a critical step to enable the production of

Lutetium-177 for our partner, ITM, and to fortifying a strong, reliable,

and large-scale global supply chain of life-saving isotopes, that both

physicians and patients can depend on.”

With its new IPS system, Bruce Power will conduct the irradiation of Ytterbium-176 (176Yb) as a first step in the production of no-carrier-added Lutetium-177 (n.c.a. 177Lu).

Processing of the irradiated Ytterbium-176 for the production of n.c.a.

Lutetium-177, as well as the global supply of n.c.a. 177Lu, will be handled by ITM Isotope Technologies Munich SE (ITM),

a leading radiopharmaceutical biotech company that is one of the

largest and most reliable producer of Lu-177 for pharmaceutical use.

“The successful installation of this production site builds an

important milestone in our partnership with Bruce Power and Isogen to

scale up the production of high-quality medical radioisotopes,” said

Steffen Schuster, CEO at ITM. “We look forward to the upcoming launch of

the IPS and are proud to contribute with our unique manufacturing

methodology to yield high-quality n.c.a. 177Lu and to make it accessible for cancer patients worldwide.”

The installation of the IPS is a significant step in the landmark

isotope project, which is a partnership that began more than three years

ago with over 400 dedicated professionals working on various stages of

the project.

In November 2021, Bill Walker, MPP of Bruce-Grey-Owen Sound,

introduced a Private Member’s motion – which passed with all party

support – to assert Ontario’s leadership role in the production and

supply of medical isotopes as a strategic priority for the province.

Today’s announcement exemplifies that Ontario continues to be the

forefront of medical isotope technology.

“I want to congratulate Bruce Power, Framatome and Kinectrics on this

important accomplishment,” said MPP Walker. “Ontario has long been

looked to as a leader in the medical isotope space, and these partners

are playing an important role in the global supply chain to provide

patients around the world with life-saving cancer treatments and

diagnostic tools.”

Bruce Power will market the new isotope supply in an historic

collaboration partnership with Saugeen Ojibway Nation (SON). The

partnership project with SON, named “Gamzook’aamin Aakoziwin,” includes

an equity stake for SON and a revenue-sharing program that provides a

direct benefit.

“From the initial concept in 2019 to production expected in 2022, our

Gamzook’aamin Aakoziwin project is on track to meet an ambitious

timeline to have isotope supply ready to meet the increasing demand from

doctors and cancer patients around the world,” said Chief Lester

Anoquot, Chippewas of Saugeen First Nation. “Saugeen Ojibway Nation is

proud of the part we have played and will continue to play in this

project.”

“Short-lived medical isotopes are essential tools for doctors and

researchers in the fight against cancer, and this project will provide a

much-needed source of these isotopes for patients close to home, in our

communities, and around the world,” added Chief Veronica Smith,

Chippewas of Nawash Unceded First Nation.

“Thanks to the investments being made into the Bruce Power site

today, we can look to the future and realize a vital role in providing

life-saving medical isotopes to the world, while also supplying clean,

reliable and low-cost electricity to Ontario, growing the economy and

fostering innovation for decades to come,” said Hon. Lisa Thompson,

Minister of Agriculture, Food and Rural Affairs, and MPP for

Huron-Bruce.

You can learn more about how Bruce Power is helping to keep hospitals safe, and also diagnosing and treating cancer at www.brucepower.com/isotopes.

About Bruce Power Bruce Power is an electricity

company based in Bruce County, Ontario. We are powered by our people.

Our 4,200 employees are the foundation of our accomplishments and are

proud of the role they play in safely delivering clean, reliable,

low-cost nuclear power to families and businesses across the province

and life-saving medical isotopes around the world. Bruce Power has

worked hard to build strong roots in Ontario and is committed to

protecting the environment and supporting the communities in which we

live. Formed in 2001, Bruce Power is a Canadian-owned partnership of TC

Energy, OMERS, the Power Workers’ Union and The Society of United

Professionals. Learn more at www.brucepower.com and follow us on Facebook, Twitter, LinkedIn, Instagram and YouTube.

About Isogen

Isogen is a joint venture between Framatome and Kinectrics,

whose mission is to enable the use of CANDU reactors to produce the

medical isotopes needed to treat and diagnose patients with serious

diseases world-wide. Isogen’s enabling partnerships with Bruce Power and

ITM allows us to produce the world’s largest and most reliable supply

of life-saving, short-lived, therapeutic medical isotopes.

About ITM Isotope Technologies Munich SE

ITM, a radiopharmaceutical biotech company, is dedicated to providing

the most precise cancer radiotherapeutics and diagnostics to meet the

needs of patients, clinicians and our partners through excellence in

development, production and global supply. With patient benefit as the

driving principle for all we do, ITM is advancing a broad pipeline,

including two phase III studies, combining its high-quality

radioisotopes with targeting molecules to develop precision oncology

treatments. ITM is leveraging its leadership and nearly two decades of

radiopharma expertise combined with its worldwide network to enable

nuclear medicine to reach its full potential for helping patients live

longer and better. For more information please visit: www.itm-radiopharma.com.

Quite impressive, Bruce Power is an incredible company, a true leader in nuclear power generation, medical isotopes and more.

And it's an important holding of OMERS and its members.

Below, Startup Health sat down with Chrissy Farr, a health tech investor at OMERS Ventures,

where she focuses on women’s health and behavioral health.

In this

interactive chat, Chrissy talked about her priorities for the remainder

of the year, including focus areas of women’s and behavioral health, as

well as her experience making the change from being a full-time

journalist covering the health-tech beat at major publications like CNBC

and Fast Company to a venture capitalist, and how that has impacted her

view on company storytelling. She also gave the inside scoop on OMERS

Ventures and how to position yourself to get on her, and the broader

company’s, radar.

Second, Eric Kimberling, CEO of Third Stage Consulting, discusses the changes and challenges facing the healthcare industry and how technology is driving improvement for healthcare.

I also embedded an older CNBC clip on whether telemedecine is the future. It's interesting for two reasons. It shows you how the pandemic only intensified a trend but it also shows you how much hype was built into these stocks, many of which have been clobbered over the last six months.

Lastly, Linda McLachlan interviews John Ruffolo, founder of OMERS Ventures and founder of Maverix Private Equity. John is inspirational and truly incredible. Listen carefully to his wise insights and why you should say what you mean.

Comments

Post a Comment