Political Independence Is ‘Essential’ For Pensions

Pension plans must be free to make decisions without political interference at a time when governments are looking to tap retirement pots to meet economic goals, according to a top investor at one of Canada’s largest pension funds.

Maxime Aucoin, head of total portfolio at C$390bn ($306bn) Caisse de dépôt et placement du Québec (CDPQ), said in an interview that it was “essential” for pension plans to retain their independence on how they both allocate funds and pay key staff.

CDPQ, which manages some public pension plans as well as insurance plans, operates independently from the government. It has a dual mandate to maximise returns for more than 6m members while also contributing to Quebec’s economy, providing an example of how pensions must balance sometimes competing priorities.

The plan holds C$68bn of listed and private assets in the province and is the second-biggest shareholder in aviation company and regional champion Bombardier.

Aucoin told the Financial Times that the fund’s focus on governance provided it with “relative independence from the political sphere”. He added that the “beneficiaries of your pension plan are not the government”.

Like many other mega-sized global retirement funds, CDPQ has in recent years reduced its holdings in Canada in preference to diversifying investments across global markets with different growth profiles, with the Asia-Pacific region an area of particular focus.

However, Moody’s cautioned in its review of CDPQ in June that in a weaker economy, the plan could come under political pressure to support Québec “in a way that eroded its ability to achieve the optimal return for depositors”.

CDPQ is far from alone in facing these risks, according to analysts and industry participants.

Blake Hutcheson, chief executive and president of Omers, the C$114bn Toronto-based public pension fund, told the FT “when I look around the world a lot of pension plans are instruments of the government”. Hutcheson also highlighted the importance of independence from political pressure, saying it was something that made many Canadian pension pensions “out-punch our weight class”.

The comments follow a warning from the Paris-based OECD watchdog that the coronavirus pandemic has led to increased political pressures on pension funds.

“Given budget constraints, some governments are calling on private institutional investors, such as pension funds, to play a bigger role in financing the economic recovery,” said Stéphanie Payet, pension analyst with the OECD.

Australia’s government has urged superannuation funds to help cushion the blow from the coronavirus crisis by funding company bailouts.

The UK government last year called for workplace pension schemes, which oversee more than £1tn in assets, to invest more in UK infrastructure projects and early-stage companies to help the country “build back better”.

In June 2021, Alok Sharma, president of COP26, the climate change conference, challenged global pension funds — with a total $47tn under management — to play a leading role in creating a “clean, green and prosperous future”.

“Although there may be room for investing further in the economic recovery, there is a risk that investing domestically, in selected sectors, or in complex financial products may deliver poor value for members, or worse than they otherwise would have gotten from other investments,” the OECD’s Payet said.

This is an important topic, one that is self-evident to me and those working within the pension industry, especially here in Canada where our large pensions have set the governance standard that others throughout the world are trying to emulate.

It is critically important that large pensions operate in the best interests of their members, without political interference.

In theory, this sounds easy and sensible. We want our pensions to be run by people who answer to their members, not to political apparatchiks that have their own agenda.

In practice, however, there's always some political pressure in the background because governments are sponsors of these large public pensions and they can influence decisions or let their thoughts be known (publicly or privately).

Even when governments claim "we don't meddle in pension investments," I can assure you, at some level there are conversations taking place with high ranking government bureaucrats who exert some level of influence. They may not be running the show, far from it, but their views will be known and they might have more influence than people think.

And this is where things can get tricky.

My fear is that I see incrementalism slowly creeping into the way our pensions are being run.

Don't get me wrong, I'm a stickler for diversity in all its forms, including diversity of views.

I think it's important to listen to the views of plan members, government bureaucrats, the public and other stakeholders but at the end of the day, we can't lose sight of the purpose and mission of these large pensions, namely, to maximize returns without taking undue risks and make sure they have enough assets to cover their long-dated liabilities.

Period. That's it, that's all. Pensions aren't there to "save the world" or to beat global stock market benchmarks every single year, pensions exist first and foremost to serve their members by ensuring they will all retire in dignity and security.

Now, don't get me wrong, ESG investing is here to stay. Our large Canadian pensions see the writing on the wall and so do their global counterparts.

As the Great Gretzky once famously said: "I skate where the puck is going to be, not where it has been."

Where is the world heading? I'm not talking about next year or over the next five years, I'm talking about the next 25 to 50 years.

The world is decarbonizing fast. You don't need to attend COP26 or any other fancy conference which big shots like Mark Carney attend, you know the world is necessarily changing and we are in the midst of a great transition.

But the key word there is "transition".

I read Part 1 of John Mauldin's outlook, A Path-Dependent Year—WWJD?, and he summed it up nicely:

"I look forward to transitioning to a clean energy world but the key word is transitioning. It’s going to take time and it seems some clean energy proponents want it done today instead of over time. This creates shortages and raises prices."

And there are a lot of opportunities and risks in the transitioning phase of a long-term secular cycle.

Our pensions need to have the freedom to operate at arm’s length from political interference to capture these opportunities and transition their portfolios slowly but surely over time to reflect the reality of the world they operate in.

But again, the focus must always be on taking decisions that are in the best interests of their members, not in the best interests of their local, provincial (state) or federal governments.

It's a bit nuanced, there are obviously overlapping interests, but the key point is this, pensions exist to serve their members, not as an extension of the government to promote some agenda, no matter how worthwhile that agenda may be.

Well, didn't CDPQ invest billions to make the REM project and didn't the Quebec government invest in this project too?

Yes but the germination of this project came from CDPQ, not the government, and it's not a charity, it's a multibillion project looking to collect a decent return for CDPQ's members over the long run.

The government has its say (mostly on regulating user fares) but it's not running the show.

This is an important distinction.

What worries me is the coronavirus pandemic has led to increased political pressures on pension funds, and in many cases pensions are taking politically motivated decisions which are not in the best interests of their members.

The same goes when large pensions are pressured by activists to make decisions that fulfill some agenda that sounds right, like divesting from oil & gas.

Why not? Just divest, it's easy. Right?

Wrong. When large pensions divest from oil & gas, all they're really doing is transferring the risk on to some other fund which doesn't take engagement or ESG investing seriously.

Recently, Canada's largest pension fund, CPP Investments hosted the Alberta Energy & Growth Forum in Calgary featuring a line-up of industry leaders speaking about investment trends, innovation, and the future of the Canadian energy industry:

The purpose of the event was twofold: demonstrating the value CPP Investments provides through our global reach, sophisticated investment approach and market-leading returns, as well as communicating our approach to investing as we navigate the global challenge of climate change.

The agenda covered timely topics related to the importance and evolution of the Canadian energy sector. In his opening remarks, President & CEO John Graham touched on how the sustainability revolution is a full economy-wide transition, much like the digital revolution that started in the 1990s. He also spoke about where CPP Investments sees attractive investment opportunities across the entire energy spectrum, and how we are working to better anticipate the transition pathways of our investments.

The featured panel focused on the future of energy. In this session Graham and Chief Sustainability Officer Deb Orida joined top executives and thought leaders from the Alberta energy sector. They discussed how an industry with a strong track record of adaptation can further evolve, as traditional energy companies increasingly pursue opportunities in carbon capture, renewables, hydrogen, and technological innovation.

Graham closed the panel with three key take-aways from the discussion:

- There is an important, positive shift underway from looking primarily at the investment risks of climate change to the financial opportunities of decarbonization;

- Collaboration is needed to go beyond general agreement on reducing emissions to action; and that

- Alberta and Canada have a great story to tell as they navigate the energy transition, given their strong track record of innovation, technology, and experience.

You can read a copy of John Graham’s speech from the Forum here.

I highly recommend you read John Graham’s speech from the Forum here and appreciate the perspective he's elucidating.

In particular, I note this passage:

Finally, I want to share our approach to safeguarding the value of our existing portfolio throughout the energy evolution. And, how we plan to utilize our knowledge of the energy transition to seek out and capitalize on the transition potential of companies across the energy spectrum.

The transition landscape remains in its early years. Yet it’s premature of the market to write off entire sectors like oil and gas before having viable, scalable alternatives in place.

For some sectors the road ahead is clear. For other essential sectors such as chemicals, steel or agriculture the path is less clear.

Where we see attractive return opportunities, we can provide capital to facilitate the transition of these vital sectors. These sectors support the net zero economy of the future and need viable, clean substitutes as demands grow.

That’s why we are deliberately building up the internal competency to help our investee companies by giving them partnership driven capital and supporting them as they adopt more sustainable business models and practices.

We’re also actively working with companies in our portfolio that are early in their transition and facing pressures to become net zero. We’re helping them improve their ESG disclosure, anticipate and interpret the regulatory or policy landscape and, sharing our institutional knowledge built through our global investing experience.

We bring the full-weight of the “CPPIB-advantage” by providing global, cross-asset class data and insights into climate changes’ physical and transition related risks. We are not walking away, we are rolling up our sleeves.

We are looking for opportunities to support innovation and transformation in power generation and utilities, many parts of the oil and gas value chain, vehicle transport, cement and construction and agriculture.

If we seed and build the right businesses today, they will become the unicorns of tomorrow’s low-carbon economy.

I think this passage is critically important, CPP Investments and other large Canadian pensions aren't walking away, they're rolling up their sleeves engaging with investee companies and investing in tomorrow's disruptive innovators.

But in order to do this properly, they need to continue to operate at arm's length from the government.

In fact, I would argue the pandemic has exposed serious governance lapses at our governments and that our public health agencies need to operate more independently, just like our large public pensions and other Crown corporations.

Lastly, some thoughts on this endless pandemic.

Take the time to read Mark Wiseman and Jay Clayton's Barron's article on what we can learn from our Covid-crisis failures:

From me and Jay Clayton in @barronsonline:

— Mark Wiseman (@MarkDWiseman) January 7, 2022

In our new article - What We Can Learn from Our Covid-Crisis Failures - Jay and I discuss how, and why, governments must learn from crises and modernize risk-management practices.https://t.co/mZ10EqNBfU

Also, let me publicly support the Quebec government's announcement today to impose a tax on people refusing to get vaccinated for no legitimate reason:

Quebec to impose 'significant' financial penalty against people who refuse to get vaccinated https://t.co/glyXZdO5iQ pic.twitter.com/lu28FnNBht

— CTV News (@CTVNews) January 11, 2022

I got into some Twitter disputes with people who claim the government can do the same with obese people and smokers and reminded them that unlike COVID, those aren't contagious airborne viruses that can bring our healthcare system to its knees in a matter of weeks.

Quebec may be the first in Canada, and in North America, to impose a tax

on the unvaccinated, but it's far

from the first in the world.

It's worth noting Greece imposed a fine on unvaccinated a little over a month ago.

At the time, the country lagged behind the rest of Europe, with 62% of the total population fully vaccinated, versus a continental average of 66%.

Prime Minister Kyriakos Mitsotakis stated this:

"It’s not a penalty. I’d say it’s a health levy, motivation for precaution, a boost to life, but also an act of justice towards the vaccinated majority. We can’t have people being deprived of public health services they need because certain others have dug in their heels and refuse to do what is self-evident.”

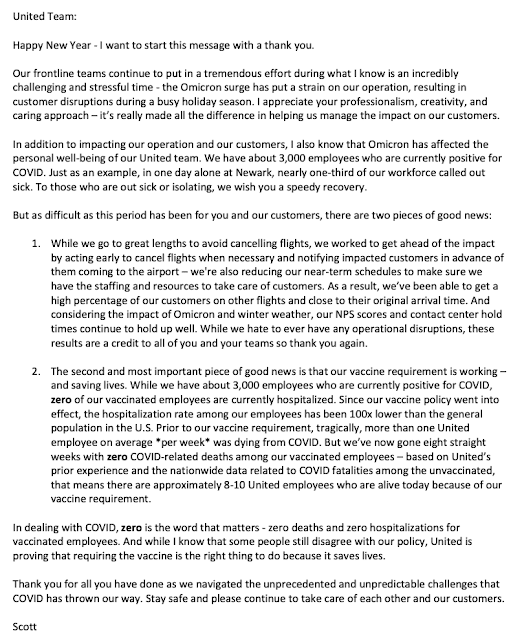

At the risk of repeating myself over and over, the vaccines do not guarantee anything, they don't prevent transmission but they significantly reduce risk of hospitalization and death, something that United CEO Scott Kirby told employees late Monday in a letter addressed to them:

So, let's all do the right thing, hopefully without government coercion and make sure we do our part to bring the end of the pandemic a few steps closer.

Below, Ontario Teachers’ Pension Plan isn't only investing to make a good return for their members, they're also investing to make a mark. The clip below highlights how they're offering outstanding service and retirement security for their members while leaving a lasting, positive impact on the world.

Comments

Post a Comment