Delphine Strauss of the Financial Times reports the rise in the UK state pension age drives record employment among 65-year-olds:

The latest increase in the UK state pension age has led to record highs in employment among 65-year-olds, while also prompting those living in poorer areas to work for longer.

Research by the Institute for Fiscal Studies, published on Tuesday, found that around 55,000 more 65-year-olds were in paid work in 2021 as a result of the gradual rise in the pension age, from 65 to 66, between late 2018 and late 2020.

The reform led to an additional 7 per cent of men and 9 per cent of women staying in work, taking the male employment rate at age 65 to 42 per cent — the highest since the 1970s. The female employment rate rose to a probable all-time peak of 31 per cent.

Emily Andrews, deputy director for evidence at the Centre for Ageing Better, the charity that funded the research, said it showed the higher pension age had been “an effective policy for extended working lives among the employed”.

However, the research also contained several warning signs for policymakers as they prepare for the pension age to rise to 67 from 2026 and as an independent review starts to consider the case for further increases to manage the fiscal pressures of an ageing population.

First, people living in poorer areas were much more likely to remain in work while waiting to become eligible for the state pension. After the change, the employment rate in the fifth most deprived local areas rose by 13 percentage points for women and 10 percentage points for men — compared with respective increases of just 4 and 5 percentage points in the fifth most prosperous areas.

Renters tended to stay in work more than homeowners, and those without qualifications were more likely to do so than those with a university education, the research showed, suggesting that financial necessity was driving their decisions.

Most of those who delayed retirement were likely to be better off financially as a result, even if they would have preferred to stop working earlier and have more leisure time, the IFS said. That was because they were predominantly working full-time, earning more than the lost pension income.

Jonathan Cribb, an associate director at the IFS, said this suggested there was “an unmet desire for many approaching state pension age to be able to work part-time, or more flexibly, than they are currently doing”.

More than 90 per cent of those affected by the rise in the pension age did not change their retirement plans, the IFS said. A majority still retire before the age of 65, either because of health problems or because they can afford to, while a significant minority choose to work for longer.

But a smaller group — including 5,000 who were unemployed and 25,000 who were unable to work for health reasons — had been particularly badly hit, the IFS said, because they were eligible for much less help through the benefits system than they would have been if eligible for the state pension.

Andrews said this pointed to the need for the government to “get serious about meaningful support to help workless people in their 60s get back into paid work”, so that further rises in the pension age did not “further harm those who are already disadvantaged by an ageist labour market”.

Laurence O'Brien, Research Economist at the Institute for Fiscal Studies

also wrote a comment for The Conversation that thechange in UK state pension age to 66 has seen big increase in working 65-year-olds, but particularly deprived women:

The UK state pension age has been rising in recent years, most recently with a staggered increase

for both men and women from 65 to 66 between December 2018 and October

2020. While the male state pension age had previously been 65 since the

late 1940s, for women this followed a previous rise in their state

pension age from 60 to 65 between 2010 and 2018.

Further increases have been legislated, starting with an increase for

both men and women from 66 to 67 scheduled between 2026 and 2028, as

the government attempts to counteract some of the pressures to the

national finances brought on by an ageing population. The government

also recently launched the second independent review

of the state pension age, to be published in May 2023, among whose

questions is to consider whether to bring forward by eight years plans

to raise the age to 68 by 2046.

But how are these increases to the state pension age likely to affect the labour market? In an ongoing programme of work at the Institute for Fiscal Studies, funded by the Centre for Ageing Better, we have examined in detail the effect of the recent increase in the state pension age from 65 to 66 on economic activity.

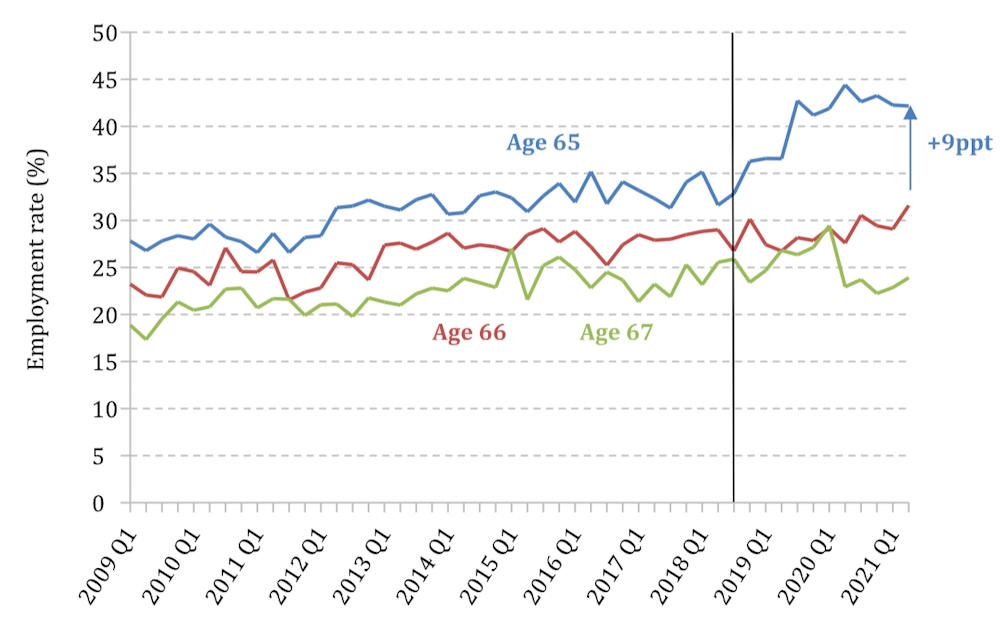

The reform increased employment significantly among older workers. As

you can see from the two charts below, it led to a marked increase in

the share of 65-year-olds in paid work. We can see that, between late

2018 and late 2020, the employment rates of 65-year-old men and women

jumped up by around ten percentage points each. This was not matched by a

similarly large increase in the employment rates of 66 and

67-year-olds, indicating that the state pension age rise was driving

this.

Employment rates of men aged 65-67

The black vertical line shows the

last quarter in which all 65-year-olds were over the state pension age

(2018Q3); ppt = percentage point.

Employment rates of women aged 65-67

The black vertical line shows the

last quarter in which all 65-year-olds were over the state pension age

(2018Q3); ppt = percentage point.

Overall, we estimate that the increase in the state pension age led

to an additional 7% of men and 9% of women staying in paid work at age

65 – this translates to around 55,000 extra 65-year-olds in paid work.

By mid-2021, the male employment rate at age 65 had risen to 42% (from

35%) and the female rate to 31% (from 22%).

Both are the highest seen since at least the mid-1970s and, at least

in the case of women, very likely to be the highest rate ever in the UK.

But, despite this increase, it still means that the majority of men and

women are not in paid work before they reach the state pension age of

66. However, employment rates at these older ages vary along several

characteristics, so it’s important to analyse how different groups

responded to the state pension age rise.

Unequal employment effects

In the most deprived 20% of areas, women’s employment rate at the age

of 65 rose by 13 percentage points and men’s by ten percentage points.

In contrast, in the most prosperous areas, female and male employment

rates at age 65 rose by just four and five percentage points

respectively. These results suggest that less-advantaged people are more

likely to continue to work as a result of the higher state pension age,

probably because many of them cannot afford to retire without state

pension income.

It is true that most of those who continue in paid work due to the

reform are likely to be financially better off by doing so, because

their extra earnings are likely to outweigh their lost pension income.

We find that most of the increase in paid work is full-time work,

despite the fact that 20 hours a week of employment at the UK adult

minimum wage (National Living Wage) of £8.91 per hour would be

sufficient to make up for the loss of a full new state pension.

But while financially better off, this is not to say that many of

these workers would not have preferred to have been able to retire

earlier and enjoy more leisure time. Delaying retirement may be

difficult and disruptive for many, so the government should prioritise

clear communication of changes to people’s state pension ages well in

advance – especially to less-advantaged groups whose retirement plans

may be more affected by the changes, and who have been found to be less aware of past state pension age reforms.

Not everyone changed retirement plans

Despite the large employment effects, it remains the case that more

than 90% of 65-year-olds (around 640,000 of them) have not changed

whether they are in paid work at age 65 purely because of the higher

state pension age. This is in large part because the majority of men and

women have already left the labour market before their 65th birthday,

while some others would have remained in paid work even if the state

pension age had remained at 65.

A group that faces obvious difficulties as a result of the higher

state pension age are those who would like to work but cannot, perhaps

because they can’t find a job, or because of health problems. We find

that the higher state pension age led to 5,000 extra unemployed

65-year-olds and an additional 25,000 65-year-olds who report that they

cannot work due to poor health.

Given the lower generosity of the working-age benefit system compared

to the state pension, this group will be of particular concern for

policymakers. In particular, ensuring that older jobseekers are

sufficiently supported – for example, by ensuring that Jobcentre staff

are attuned to their needs and challenges – to find appropriate work

becomes ever more important as the state pension age rises.

And Sarah Corker and Kevin Peachey of the BBC report women's state pension shortfalls a shameful shambles, MPs say:

A £1bn shortfall in state pension payments to tens of thousands of women has been branded "a shameful shambles" by a committee of MPs.

A

total of 134,000 pensioners missed out on their full entitlement owing

to errors at the Department for Work and Pensions (DWP) dating back to

1985.

Some of those failures risked being repeated during a correction programme, the Public Accounts Committee said.

The DWP said it was resolving cases as quickly as possible.

Why did women miss out?

The

problem relates to the "old" state pension system where married women

who had a small pension in their own right could claim a 60% basic state

pension based on their husband's record of contributions.

Widows

and divorcees have also been affected. Some will receive all their

entitlement, although years later than they should have done. Others

will only be able to claim for 12 months of missed payments.

Among

them is Jan Tiernan, from Fife, who was initially told she was not owed

any money. After nearly 100 pages of correspondence with the

department, she received £1,280, but believes she is owed more.

"You need a lot of energy, and when you are 80-years-old you don't have that kind of energy. It tires you," she told the BBC.

"I feel let down by the system."

She

said that the extra money would have made a lot of difference to

pensioners, from helping to pay heating bills to going towards a

holiday.

The

committee's report said the errors were the result of outdated systems

and heavily manual processing of pensions at the DWP.

Small errors that were not recognised added up to significant sums of money over the years.

In a damning report, it concluded:

The

failures have led to significant losses to taxpayers. Staff costs in

correcting mistakes by the end of 2023 are expected to reach more than

£24m

There is no plan for contacting families of pensioners who have already died, and who should receive some of their entitlement

The DWP has been "inconsistent" in paying pensioners interest on the money that was owed

It has ignored knock-on consequences of paying lump sums, including on benefits and social care provision, to those it underpaid

Other pensioners could be missing out and should receive clearer information about how to claim

The

committee said that there was a risk that the errors that led to

underpayments in the first place could be repeated in the correction

programme, the ninth such exercise since 2018.

There

was also concern that, by allocating staff to deal with this problem,

backlogs occurred in dealing with claims from new pensioners who

suffered delays in receiving their state pension at 66.

Meg

Hillier, who chairs the committee, said: "For decades DWP has relied on

a state pension payment system that is clunky and required staff to

check many databases - and now some pensioners and the taxpayer are

paying in spades.

"In reality, the DWP can never make up what people have actually lost, over decades, and in many cases it's not even trying.

"This is a shameful shambles."

Call for urgency

Among

a string of recommendations made in the report is that the DWP should

find cost-effective ways to update its computer systems.

The committee also said the DWP needed to make clear how it was treating underpayments related to divorced women.

Former

pensions minister Sir Steve Webb, who is now a partner at consultancy

LCP, first raised concerns about underpayments, and has called for

divorcees to be included having their entitlement checked.

"The

DWP's defensive reaction to questions and scrutiny over this issue

suggest that lessons have still not been learned," he said.

"There

are still far too many people missing out on the state pension to which

they are entitled and DWP needs to track them all down as a matter of

urgency."

A

DWP spokesman said: "Resolving the historical state pension

underpayments that have been made by successive governments is a

priority for the department and we are committed to doing so as quickly

as possible.

"We

have set up a dedicated team and devoted significant resources to

processing outstanding cases, and have introduced new quality control

processes and improved training to help ensure this does not happen

again. Those affected will be contacted by us to ensure they receive all

that they are owed."

I've been reading about changes to the UK state pension and how it disproportionately impacts women and those who are unable to work past 65-years-old either because of poor health or because they cannot find work.

I also read about the colossal mistakes the Department for Works & Pensions (DWP) has made to the pensions of many women, costing them a lot of money over the years, money which they will likely never see.

Pension policy around the world is critically important.

There are mega trends going on and what we are seeing in the UK is happening all over the world, it's important to understand how an aging demographics is putting pressure on state pensions and how governments respond.

I recently discussed China's ever grand pension problem, stating the Chinese Communist Party cannot ignore this growing problem indefinitely.

But in the UK cracks are appearing as millions of people on benefits are facing poverty as payments to rise by just half of inflation:

Millions of households could be plunged into further financial crisis

as benefit payments are set to go up by just a fraction of how much

goods will rise this year, a think tank has warned.

Payments for 10 million claimants are set to go up by 3.1% in April.

However inflation is expected to hit 6% and the new energy price cap will come into force around the same time.

Think tank, the Institute for Fiscal Studies (IFS), said the Department for Work and Pensions

should raise the payments by twice as much as planned if the poorest

households in Britain are to be supported through the cost of living

crisis.

It said an additional £3billion is needed in response to soaring energy bills and essentials such as food and rent, the Mirror reports.

Instead of a planned 3.1% increase, it said payments needed to rise by about 6% to protect lowest-income households.

Raising

benefits by this amount - even if just temporary - would mean

preventing a £290 real fall in benefit income year on year for the 10m

households in receipt of state support, the report said.

It is understood that the government is in talks to push forward the

warm homes energy discount to help 800,000 more homes in the coming

months, but even then, the scheme ends on March 31.

Households with typical energy usage face a £700 rise in annual bills without government intervention. That would put a typical annual energy bill close to £2,000.

Meanwhile, the rise in the state pension set for April amounts to an annual increase of less than £300.

One other policy being considered by Boris Johnson is to remove VAT on energy, saving homes around 5% on bills.

It comes as a planned 1.25% increase in national insurance will kick in from April.

With inflation soaring to multi decade highs, many in the UK and around the world are feeling the pinch.

Clearly, the poor, working poor and those living on foxed income are feeling the effects a lot more.

The great economist Milton Friedman once noted: "Inflation is taxation without legislation."

He was right and he also noted it disproportionately hurts lower income individuals and families.

When it comes to state pensions, I agree with those who think we need to adjust pension payments more often and in line with current inflation rate, especially for low income households.

More importantly, after reading this comment, you realize there are serious cracks in the the UK's state pension system and it's mostly impacting women.

Women are disproportionately impacted by pension poverty for a lot of reasons and all governments around the world need to recognize this and plan their pension policies accordingly.

What else can the UK do? It needs to study Canada's large pensions and try to adopt the same governance that led to their success.

There are many excellent UK pensions but when you look at the entire system, there's a lot of room for improvement.

Below, the Institute for Fiscal Studies looks at how household living standards have changed over the course of the pandemic, based on our annual Living Standards, Inequality and Poverty in the UK report.

And Irene Wise had been battling with the Department for Work and Pensions (DWP) for two years until it admitted she had been underpaid on her pension for eight years.

It's shameful that these women are being underpaid and then have to fight for what is owed to them.

Comments

Post a Comment